On 29 May 2018, the Governing Council of the Community of Madrid approved the draft law on tax measures for the Community of Madrid for 2018

The draft contains important measures relating to Personal Income Tax, Inheritance and Gift Tax, and Transfer Tax and Stamp Duty, which are summarized below:

1. Personal income tax:

|

Deduction for birth (entered into force 1/1/2018) |

|

|

Deduction for housing rental (effective 1/1/2018) |

|

|

Decrease in the regional scale of personal income tax (entry into force 31/12/2018) |

|

|

Deduction for foster care (effective 31/12/2018) |

|

|

Deduction for school fees (entry into force 31/12/2018) |

|

|

Contribution deduction for a carer of descendants under 3 years of age (effective 31/12/2018) |

|

|

Deduction for contributions to the share capital of the social economy (effective 31/12/2018) |

|

|

Deduction for donations to Foundations (effective 31/12/2018) |

|

|

Deduction for investment in the acquisition of shares and holdings (effective 31/12/2018) |

|

2. Inheritance and gift tax (Effective 1/1/2019)

- A new bonus is established for both inter vivos and mortis causa acquisitions for transfers between 2nd and 3rd degree consanguineous collateral (siblings, uncles and nephews) of 15% and 10% respectively.

- Limit of application: When the taxable person himself requests or applies it when submitting his self-assessment or return.

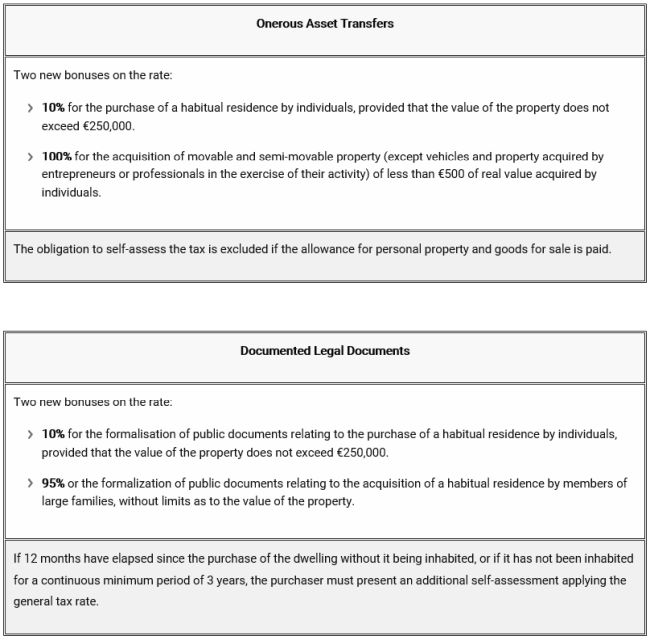

3. Transfer tax and stamp duty (Entry into force 1/1/2019)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.