BACKGROUND

The Ministry of Strategy and Finance ("MOSF") finalized scope of Combined Report of International Transactions ("CRIT") and confirmed taxpayers subject to the CRIT requirement through its official announcement dated April 14 (MOSF Announcement No. 2016-7). On April 6 (prior to the MOSF's announcement), the filing format of the CRIT was provided in Article 6-2 of Ministerial Decree of the Law for the Coordination of International Tax Affairs ("LCITA"), while taxpayers subject to the CRIT requirement were confirmed through the MOSF Announcement No. 2016-7. The requirement of preparing and submitting CRIT will be applicable from the fiscal year commencing January 1, 2016.

Accordingly, taxpayers with cross-border related-party transactions should carefully review whether they are subject to the CRIT requirements under the LCITA and its Decrees as well as the MOSF's Announcement.

DETAILS

1. Types of CRIT

There are two types of CRIT to be filed by taxpayers, namely the "local file" and "master file." The local file should provide information on the local taxpayer (local organizational structure and business information, etc.), major related-party transactions and information on transfer pricing for the same, and financial summary. The master file should include information on the organizational structure of the entire multinational group (which the taxpayer is a part of), description of businesses, intangible assets, financing activities, and financial summary.

2. Who is required to file CRIT?

Taxpayers (i.e., domestic and foreign corporations with a permanent establishment in Korea) that meet both of the criteria below will be required to file CRIT. Non-compliant taxpayers will be subject to a fine of KRW 30 million (approximately USD 30,000).

- Annual sales revenue in excess of KRW 100 billion (approximately USD 100 million) ; and

- Annual cross-border related-party transaction volume (sum of transactions involving goods, services, and loans) in excess of KRW 50 billion (approximately USD 50 million).

3. Scope of Master File

Unlike the local file in which a taxpayer discloses information about itself (and is responsible for submission of the same), the master file should include information on the entire multinational group (which the taxpayer is a part of). As mentioned above, the detailed scope of information to be included in the master file has been confirmed through the MOSF's Announcement (No. 2016-7).

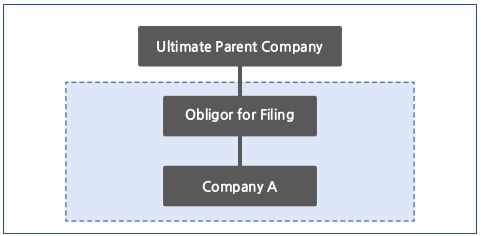

In principle, the master file should include information on all companies (including the local taxpayer) that are part of consolidated financial statements under the International Financial Reporting Standards (if the taxpayer is included in two or more consolidated financial statements, all companies under the consolidated financial statements that cover the ultimate parent company). For purposes of illustration, all companies within the solid line (i.e., ultimate parent company, obligor for filing, and Company A) in Figure 1 should be covered by the master file.

Figure 1

However, if the businesses conducted by the multinational group are divided into two or more business groups ("Exception 1") or the multinational group is under control of a holding company ("Exception 2"), the master file may be prepared for each business group (if Exception 1 is satisfied) or for each subsidiary (if Exception 2 is satisfied). We explain this in more detail below.

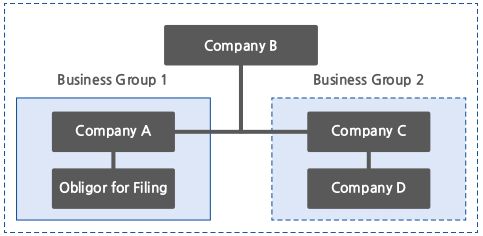

(1)Scope of master file if Exception 1 is satisfied: If the businesses carried on by a multinational group are divided into two or more business groups, the master file should include information on the companies covered by the consolidated financial statements prepared by the upper-most company within the business group that includes the local taxpayer (i.e., taxpayer required to submit local file). Business group for this purpose refers to all of the companies within the multinational group that independently conduct activities for added value creation in goods or services (such as manufacturing, shipping, marketing, HR, planning, finance, etc.), which prepare consolidated financial statements separately from other business groups. For illustration purposes, all companies within the solid line in Figure 2 below are covered by the master file.

Figure 2

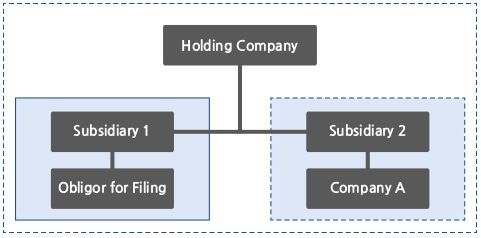

(2)Scope of master file if Exception 2 is satisfied: If a multinational group controlled by a holding company as defined under Article 2(1)-2 of the Korean Monopoly Regulation and Fair Trade Act has subsidiaries that conduct different businesses, the master file should include information on all companies covered by the consolidated financial statements which are prepared by the subsidiary in control of the obligor for filing of the master file. In Figure 3 below, all companies within the solid line (i.e., subsidiary 1 and obligor for filing) should be covered by the master file.

Figure 3

4. Representative Filer of Master File

When multiple taxpayers are included in the scope of master file as is the case for subsidiary 1 and obligor for filing in the above diagram, a single taxpayer can submit the master file as a representative. However, such filing is permitted for convenience in submission and the obligation to file the master file by the obligor for filing still exists. Thus, if the representative filer fails to submit the master file, the respective obligors for filing shall be subject to a fine. Taxpayers meeting the criteria below may serve as a representative filer:

- If taxpayers are in a parent-subsidiary relationship, the parent corporation;

- If there is no parent-subsidiary relationship amongst taxpayers (within the business groups), the taxpayer closest to the ultimate parent company (or subsidiary) in terms of the control relationship; or

- If there is no parent-subsidiary relationship amongst taxpayers and all taxpayers are at the same level in terms of control, one of the taxpayers.

5. Method of Filing the CRIT

CRIT should be filed with the competent tax office, and may be submitted electronically (through the national tax information network). The local file must be submitted in Korean, and the master file may be submitted in English on the condition that the master file will be translated into Korean and submitted within a month of filing in English.

6. Submission Deadline and Reasons for Extension

The CRIT should be submitted by the corporate tax return filing due date (i.e., within three months of the fiscal year-end). However, the tax office may extend the submission deadline up to a year if one of the following events occur:

- The relevant documents cannot be submitted due to reasons such as fire/disaster or theft;

- It is very difficult to submit the relevant documents due to the business facing a major crisis;

- The relevant books/documents are seized or provisionally held by authority;

- The closing date of fiscal year of the overseas related party has not lapsed;

- The relevant documents cannot be submitted by the deadline due to substantial time it takes to collect/prepare the same; or

- It is determined that the relevant documents cannot be submitted by the deadline due to reasons listed in 1 through 5 above.

Originally published in Tax News Alert 2016.04

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.