Executive Summary

The Bermuda (re)insurance industry appears to be at a crossroads. For the first time, the dominance of the island in the market seems to have been shaken by a unique combination of adverse pricing caused by an influx of capital and low catastrophe losses and economic conditions such as low interest rates.

The Bermuda market has grown from strength to strength over the past 70 years. From the day AIG set up on the Island in 1947, various catastrophes or shortages of capital in the market have led to a boom over the past 20 odd years, with wave after wave of insurers setting up.

Now, however, the "bigger is better" model seems to be dominating and mergers and acquisitions have been high on the agenda for the island's executives.

Xuber gathered a group of executives on the island to talk about market conditions, innovation, technological change and analytics.

What we found was an optimistic view of change and fighting talk about Bermuda's place as an innovator in the global marketplace by finding new solutions through the likes of insurance-linked securities (ILS), specialist start-ups and technological advances.

Many questions have been raised recently in the reinsurance market – and especially in Bermuda. How can the industry best utilise fundamental risk management differentiators such as analytics, underwriting expertise or complimentary intellectual capital? Is the current industry structure best suited to respond to emerging industry demands?

The report from this lively conversation covers three main areas: analytics, mergers and acquisitions, and Bermuda as an offshore domicile.

In the analytics section, the panel discussed how analytics and data can be better used now and in the future.

Singing from the same hymn sheet, the panel discussed the benefits of the global reinsurance marketplace and Bermuda's place within it.

The overriding agreement from the panel was that traditional underwriters will now add a layer of common sense to modelled results, interpret additional financial needs of their client, and interpret information feeding the models – not just rely on years of calibrated data by independent scientists.

Finally, the existence of models has helped to create new product lines and markets, such as terrorism coverage (terrorism was sold before models for it existed) and the ILS sector.

In M&A, the two challenges of cultural integration and combining multiple legacy systems were discussed as major constraints to growth following any consolidation activity.

The debate on M&A covered whether the current trend of 'big is best' would actually present any real long-term benefit for consumers or shareholders. Also discussed was the changing role of the investor – going from savvy stock pickers 10 years ago, to passive index investors who do not really understand the sector.

Bermuda as a domicile covered the efforts made by the island's regulator to achieve Solvency II equivalence while maintaining the island's reputation as centre of reinsurance knowledge and expertise. The panel agreed Bermuda was still the number one reinsurance jurisdiction in the world, despite competition from other domiciles who have set their sights on ILS.

History of the Bermuda Market

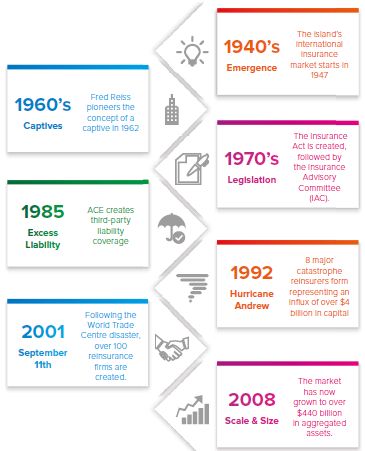

The Bermuda reinsurance market has continually evolved since the late 40s when the first insurance company was set up by AIG.

In the 1960s and 1970s, the captive insurance sector brought in the first major wave of insurance company formations on the island. Companies were then set up in the wake of the crisis in the excess liability insurance market in the 1980s, Hurricane Andrew in 1992, 9/11 in 2001 and Hurricanes Katrina, Rita and Wilma in 2005.

Following the 9/11 terrorist attacks, more than half of the new capital raised globally for the reinsurance market came to Bermuda.

Along with the capital flows came in talent and intellectual capital, as well as the building of an infrastructure that is geared to the re/insurance market and start-ups.

The magic combination of new capital and some of the keenest minds in the market has made Bermuda a powerhouse in risk management and it is now a major player in the insurance and reinsurance sector, second only to London and New York.

Milestones in Bermudian Insurance

Analytics

Due to its geographical isolation and the lack of legacy issues with start-ups, Bermuda has always prided itself in leading the way in electronic communication and the use of mathematical models to support underwriting decisions as part of day-to-day underwriting.

While modelling capabilities have been met with resistance in the past, due to perceptions that models are inaccurate for many lines of business, Brenton Slade, COO of Horseshoe Group, said the catastrophe models are only one portion of the whole analytical framework.

"The biggest benefit cat models have provided is to allow the industry to speak a common language when it comes to risk," said Mr. Slade. He added that analytics are developing into producing dynamic risk models that incorporate multi-factors of risk that are embedded in reinsurance firms – such as organisational risk, asset risk and liability risk.

While the take up of vendor models is globally widespread, strong scepticism still remains for some that the whole nature of using simulated projection and estimations to price a risk removes the art of underwriting, supplementing it instead with pure science – which can be difficult to put into practise with volatile lines of business or a soft market.

"One of the biggest operating costs that we have in reinsurance is to fund these models. There's a lot of discussion in our organization around are we getting the value of that," says Mike Doyle, SVP Operations at Ariel Re. "There will always be built-in uncertainty in the models - we know that the models have shortfalls."

Some argue that the old view of models has made reinsurers scared of volatility, leading to underwriters wanting to only take on predictable risk, at the same time as clients increasingly wanting to lay off volatile risk.

"This is a real challenge in our industry with analytics – making those unpredictable risks insurable," admitted Robert Johnston, President at Aon Benfield Bermuda. "You cannot just drive certain classifications of risk into the 'uninsurable' category because there is not sufficient data or the data is too volatile. This market is about insuring the exception to the rule."

The market has done this in the past with terrorism, argues Damien Smith, EVP and Underwriting Director at Hiscox Re Bermuda. "That risk was pretty hard to rate, however now it has become a profitable line for many people," he says. Following huge client demand, the market found a way to insure against the threat of terrorist attacks and it has now become a profitable line of business. The industry is understanding the demand for cyber risk and is currently seeking capacity and appetite to find a way to securitise a potential new reinsurance product. However, Richard Clark, Business Development Director at Xuber, argued that the art of underwriting can be enhanced by science. "Underwriting has evolved into the interpretation and emphasis you put on that data, and that can be a valuable differentiator in a competitive marketplace," he said.

"You have to have better knowledge of the forces in the marketplace and the risk to have a better view on how to price it," added Claude Lefebvre, Chief Underwriting Officer at Hamilton Re. "You can't deny that more information adds value."

Understanding what is not reflected in the model is almost as important.

"A good underwriter won't just rely on a model. Any underwriter worth his salt will make his money based on current conditions along with the price of the contract," said Mr. Doyle. "That won't be spewed out of a model – that will come with experience, seasonality and knowing how to interpret the data."

Catastrophe models can be a valuable tool if it is understood how they work and what the limitations are. They have also contributed to the creation of a whole new marketplace – the ILS market. Without modelling data and index-based triggers, capital markets investors simply would not part with their capital.

"We take potential investors through what our underwriting approach is and why we use a multimodel portfolio system. We try to tell our investors all the things they are exposed to – that it's not just focused on a model," said Tim Tetlow, President at ILS Capital Management.

"I'm a complete believer in models and I'm also a total model sceptic," added Mr. Tetlow.

M&A

The topic of mergers and acquisitions (M&A) is a recurring debate in Bermuda. Mr. Lefebvre said that M&A is part of a cycle and tends to take place during the soft market. However, the latest round of activity seems to beg the question of whether bigger is actually better.

There were approximately 390 insurance transactions announced last year for a combined value of almost $50 billion, according to data compiled by Bloomberg*. That made it the industry's busiest year for deal making since 2008 - including transactions such as Renaissance Re's purchase of Platinum Underwriters Holdings – and the launch of XL Catlin following the largestever takeover of a Lloyd's of London underwriter at $4.1 billion.

Acquirers spent $17 billion on property and casualty, multi-line insurance and reinsurance deals - the most since 2011 – according to Bloomberg.

Meanwhile Axis Capital Holdings and Italian investment vehicle Exor are both bidding for Bermuda-based PartnerRe – suggesting a possibility that investors could be looking to fund the traditional reinsurer models.

"I'm not sure that being a company with $10 billion of capital necessarily provides access to much more business than being a $5 billion sized company, but in a merger situation it's not just about scale – it's also about creating efficiencies and widening the scope of your resources and capabilities," said Aon Benfield's Mr Johnston.

The current wave of consolidation is seemingly putting smaller companies under pressure to choose a dance partner before the music stops, with Stephen Catlin himself stating consolidation was inevitable so "why wouldn't you be on the front foot and be proactive - and choose the partner you want".

"The question is how many M&A deals actually increase shareholder value ? I believe you'll find the number is really small," said Brad Adderley, a Partner at Appleby. "I understand a M&A deal when you buy a company with a book of business that you didn't have access to, but I'm waiting to see if mergers of like for like companies in the end really make sense for the shareholders." "There are many challenges in terms of making sure you have the right synergies, looking at the loss of good employees," adds Chris Garrod, Partner at Conyers. "Sometimes the potential challenges that these deals face can far outweigh the benefits."

Horseshoe Group's Mr. Slade believes that there would be less M&A activity in this cycle if management teams were brought to task over the rationale behind the proposed deal, and how it will serve shareholder value over the long term. "I think you would see far less deals and you would see a lot of capital returned back to investors – or deployed into new product lines as opposed to just expanding your equity base," he said.

The Threats & Opportunities of M&A

One school of thought is that much of the current M&A activity and the desire to increase the capital base is driven by investors. Investors, the capital providers to the space, are not giving any benefit to any skill outside of the pure market data, and therefore reinsurers are simply looking to increase their size. In an investor's eyes, they are simply an index-tracked fund.

"Passive index investors are the fastest growing source of capital. They don't get involved and don't understand reinsurance," said Mr Slade. "As long as you are a certain size, you fit somewhere in the index and they have to buy you to that level. Investors used to want to manage performance. It's completely changed now – they are increasingly passive and don't have the same demands on performance or meeting certain return or risk profiles. Its completely changed the way that reinsurers manage their business."

Regardless of the reason why a company chooses to consolidate – whether to access new product lines, different geographies, or simply to get bigger - the following issues are the same in the aftermath; marrying up two different cultures and harmonising different legacy systems. In a recent reinsurance study by Xuber, which quizzed global executives on the major issues currently in the industry, respondents said cultural integration was the biggest challenge reinsurers faced following a M&A, followed by integration of multiple systems – both presenting constraints on growth that can last for years.

Deciding on who wants to write what, what appetites are, who will survive, title inflation, who will be called what, or where the company will be based, can get bloody, and will almost certainly take management focus away from the executive suite.

"It begs two questions," said Jim Rice, Senior Business Development Executive at Xuber. "Do companies actually take culture into consideration when they're thinking about acquiring another company? And if they do, what actions do they take to mitigate those issues?"

Mr. Johnston said that when Aon Benfield merged, Aon spent a lot of time thinking about how to integrate Benfield and that six years on, Benfield is still "very much part of the DNA" with some key capabilities still enduring at the combined company.

While a clash of cultures may be the number one challenge in any merger deal, combining two companies and their legacy issues is another major issue. However, it can also be an opportunity. "If we want to move the industry to the next level, you have to start thinking about the data and the systems," argued Xuber's Mr. Clark. "How do we do a better job of capturing information and use it to our advantage?

"The thing that we are constantly asked is how can we refresh the legacy systems as an asset and leverage the data better, rather than it being masked and buried in outdated systems and processes.

"Looking at a market like Bermuda, where there are a lot of smaller organisations that have not got many legacy systems, they are in a position to be more entrepreneurial, better able to change and take new opportunities versus the mega big organisations that have multiple systems and processes – all made worse by M&A," he said.

Out of any M&A activity comes opportunities for those staying out of the dance – particularly for the smaller players, who can capitalise on dislocated teams of people and new lines of business. "It's a great opportunity for some of the smaller players and other carriers that are not involved in M&A activity because there's a dislocation - teams that are not happy with M&A, teams that will be let go, and a distraction by carriers dealing with M&A activities and not primarily focused on day to day" said Mr. Doyle. "It's up to other companies in the industry to identify these opportunities and to capitalise on those new teams and lines of business that are available."

"The social and cultural side is so important to any M&A activity," said Mr. Johnston. "If you don't manage the people correctly and integrate them into your environment, they will leave and take so much value out of the business. They are the guys who are at the base of your business and the strength – aside from any analytics, or data or technology you have behind the scenes.

Anyone who ignores people in the business will suffer the consequences."

Bermuda as a Domicile

Another cyclical trend follows on from any period of intense consolidation: start-ups cropping up to fill in the gaps left by the M&A activity. The reinsurance sector now has more choice than ever for where to set up a new carrier and their securitisations. Bermuda now faces strong competition from other domiciles which have set their sights on ILS, including London, Malta, Gibraltar and Puerto Rico.

"Bermuda as a jurisdiction is the number one captive market in the world; it is the number one ILS market in the world for growth and it has extremely strong localised insurance and reinsurance knowledge," said David Gibbons, Managing Director at PwC Bermuda. "Bermuda has the expertise and experience to weather the cycles and come back on top."

Mr. Smith agrees. "There's plenty of expertise in Bermuda that will take advantage of the market when it turns. There will be new companies and existing companies that will grow bigger - bringing on new ILS funds. I don't think we'll see the same number of new entities as in previous hard markets, rather existing companies managing the different forms of capital available to them"

When Bermuda emerged as an offshore domicile in the late 1990s, there was speculation about what would happen to these carriers after a big event, but Bermuda survived and is now considered the mainstream and accepted model for start-ups, as well as being the world's third largest reinsurance market.

Meanwhile, the island is moving closer to gaining Solvency II equivalence in order to position itself as an internationally recognised jurisdiction, and has removed any constraints to future growth by simplifying legislation to set up new carriers and securitisations on the island. As a result, the island has been at the forefront of the global boom in ILS investment. The Bermuda Stock Exchange saw a 53% increase in its ILS listings from 77 in 2013 to 118 in 2014, while 57% of the outstanding worldwide ILS stock is listed in Bermuda, according to the Bermuda Monetary Authority (BMA).

"How could a new start up who's thinking about forming in any offshore jurisdiction not choose Bermuda?" asked Appleby's Mr. Adderley. "Fundamentally I don't understand how a CEO can sit there and say we'll form in another jurisdiction when there's already a highly established marketplace here In Bermuda."

Hamilton Re's Mr. Lefebvre added: "It's easy to get a license, you can do it quickly. Talent is on the island, the brokers are here, the infrastructure is here. It's a real marketplace."

The island also prides itself on how nimble and responsive it is – illustrated by the past innovation in the Bermuda market to utilise new capital.

"There's no other credible reinsurance jurisdiction other than Bermuda where you can literally call the regulator in the afternoon and arrange a meeting the next day," said Mr. Garrod. "You just don't get that in Europe."

Mr. Adderley agreed. "The idea is that when you speak to the BMA you'll hopefully receive an answer quicker and hopefully they will engage in a dialogue with the client."

Bermuda itself used to be considered alternative, which is probably why it has embraced the so-called 'alternative capital' coming into the market and made itself receptive to new risks and strategies.

"We see a lot of things going on behind the scenes," explained Mr. Slade – using the life, longevity and casualty market as examples. "It's not the same situation as we saw in 2005 and 2007 where Bermuda was the reinsurance equivalent of the 'Klondike gold rush' - where there were a lot of new people coming to the island and it was unsustainable. We're getting back to the new normal, which is a more moderate level of growth, but behind the scenes there is so much innovation going on and a lot of new risks coming to the market."

What's Next for the Reinsurance Industry?

The reinsurance industry was not created to innovate – it was created as another layer of capital to buffer extreme events. The sector is trying to move forward and position itself to truly add value in addition to what the industry was originally designed to do, but there are hurdles – for example - to some extent, the unknown stifles innovation.

"It's really difficult to write something that you present to your board and say it's a new area and we think there's a lot of demand here, but it could potentially run at a loss initially." said Mr. Slade. "They will want to do something else, tried, tested, and historically profitable."

However, Bermuda has always been an environment that nurtures modernisation.

"There's a real opportunity to change our model, to change the product, to innovate, to write capacity where there is none, to understand the data, capture it and to automate it. We have not moved in a solid 20 years," argued Hamilton Re's Mr. Lefebvre.

"We haven't really innovated. We have not recruited outside the same type of talent – the underwriters, the actuaries, and people that fit that model. There's a real opportunity for the upcoming leaders and the younger, newer crowd to change the way insurance is perceived and works. This is the real challenge - who will take the step to modernise our world and the industry and take us to where we should be?"

There is no emerging consensus on where the global reinsurance market is headed, regardless of the emergence of ILS. However, it is clear that the so-called "winners" will be those that are focused on innovation and product differentiation – particularly from players that can anticipate future economic and industry trends.

Never before in the industry's history has the landscape been so quick to evolve, and never before has it been more important to have successful business models that are nimble relative to demand. This resonates with everything Xuber is doing in facilitating change and agility to allow reinsurance firms to clearly assess industry demand and adapt to it in the living, breathing risk landscape.

From the roundtable, it is clear that the industry must learn to change the way it views risk transfer and adapt by creating specialised risk management partnerships rather than to simply respond to transactional risk transfer requests. This will allow the industry to break through any existing boundaries and offer solutions that clients are asking for.

Those in the industry who are truly looking for the way forward are in dire need of differentiation, and the way to achieve that is through product innovation, championing niche markets, leveraging present-day technology and gaining greater insight from it, and seeking opportunities, which aren't necessarily in their comfort zone.

Bermuda's role as an innovator is clear, as is the optimistic view of change on the island, but most of the themes discussed have acted as a barometer of not just Bermuda, but as indicators for the rest of the market.

Article first published by Xuber, July 2015

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.