- Quoted companies incorporated in the UK are subject to mandatory greenhouse gas (GHG) reporting requirements

- Although the new Regulations come into force on 1 October they have retrospective effect, applying to any company financial year ending on or after 30 September 2013

- Although binding only on quoted companies, voluntary compliance with the Regulations is highly advisable for private companies aspiring to or preparing for IPO.

On 1 October 2013 new regulations1 come into force requiring UK quoted companies to report on the greenhouse gas ("GHG") emissions for which the company is responsible worldwide. Although only coming into force on 1 October, the regulations have retrospective effect as they apply to any company financial year ending on or after 30 September 2013. Consequently, many companies falling within the new rules must obtain and report on emissions for periods dating back to the beginning of their financial year 2013 - 2014. For example:

The regulations were originally due to come into force in April 2013, but were delayed until October to coincide with other changes to company reporting requirements implemented on that date. One result of that delay is a need to ensure that backdated information is captured and included within the reports.

Quoted companies

The regulations apply to companies that are:

- incorporated in the UK, and

- whose equity share capital is:

- officially listed on the main market of the London Stock Exchange, or

- officially listed in a European Economic Area State, or

- admitted for dealing on either the New York Stock Exchange or NASDAQ

Comply or explain

The regulations adopt a "comply or explain" policy to promote transparency and to recognise that the scale and complexity of a quoted company's global operations might make it extremely difficult to obtain reliable data, whether in respect of specific emissions, geographical locations or processes. Where that is the case, the company is required to identify and explain any significant gaps in its data.

The Financial Reporting Council Conduct Committee is responsible for enforcing the regulations. While aiming to work with companies to ensure compliance, the Committee has power to:

- enquire into cases where it appears that relevant disclosures have not been Provided

- apply to court for:

- a declaration that the annual reports or accounts of a company do not comply with the requirements, and

- an order requiring the directors to prepare a revised report or accounts

Non-compliance may also constitute an offence under Companies Act 2006:

- Offence A: failure to produce a directors' report, s 415

- Offence B: failure to comply with disclosure requirements, s 419

- Offence C: untrue or misleading statements, s 469

Penalties under the Companies Act 2006 regime range from a fine of up to £5,000 on summary conviction to an unlimited fine following conviction on indictment for more serious or extensive offences.

There is also the possibility of civil liability to shareholders for negligent - or possibly even fraudulent - misstatement.

Where must GHG information be reported?

Information on GHG emissions must be set out in the Directors' Report, which is the narrative section of the annual report. Information may also be included in the Strategic Report if it provides information about environmental matters necessary for an "understanding of the development, performance or position of the company's business". Information must be included in the Strategic Report if it is considered to be "material".

What is "Material"?

Under the International Financial Reporting Standard 4.1 (Presentation of Financial Statements) omissions or misstatements of items are material if they could individually or collectively influence the economic decisions that users make on the basis of financial statements. Materiality "depends on the size and nature of the omission or misstatement judged in the surrounding circumstances".

In practical terms, the question is whether including information on GHG emissions would provide an insight into (i) the company's main objectives and activities, and (ii) the principal risks it faces and how they might affect future prospects.

Organisational Boundaries

When reporting on its GHG emissions a company falling within the regulations must define its own "operational boundaries". A UK quoted company is expected to report on GHG emissions for which it is responsible worldwide, with the concept of "responsibility" extending to the operation of companies within a group and to business operations in other jurisdictions.

When fixing its operational boundaries for reporting purposes, a company may adopt an approach based on:

- Financial control

- Operational control

- Equity share tests, or

- Boundaries established in accordance with the Climate Disclosure Standards Board (CSDB) Climate Change Reporting Framework

The regime is based on the "comply or explain" principle. In this context, a company must make it clear if (and why) it has fixed its organisational boundaries in a way that excludes certain operations or geographical regions.

Organisational boundaries may also be set in terms of time. For example, a company may elect to report on certain GHG emissions for a twelve month period differing from the company's financial year. However, if any such decision is made it must be disclosed and explained in the Directors' Report. Further, DEFRA guidance states that if emissions are reported for a period differing from the company's financial year, the majority of the emission reporting year should still fall within the period covered by the Directors' Report.

The objective is, in part at least, to prevent a company excluding from its report significant emissions attributable to an activity that ended during the current financial year or that began late in the current financial year. The requirement to "comply or explain" is intended to close down the scope for reporting on a selective basis to produce a misleadingly favourable picture.

What must be reported?

The new regulations require quoted companies to report the annual quantity of emissions in tonnes of carbon dioxide equivalent from activities for which the company is responsible, including:

- The combustion of fuel

- The operation of any facility

- The purchase of electricity, heat, steam or cooling by the company for its own use.

The report must cover the "Kyoto" GHGs: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF6). In calculating its information a company must use at least one "intensity ratio", expressing its annual emissions in relation to a quantifiable factor associated with the company's activities.

From the second reporting year onwards information from the first or "base" year must be presented alongside that of the reporting year to provide a rolling indication of changes (whether favourable or unfavourable) against the initial intensity ratio. The objective is to encourage behavioural change.

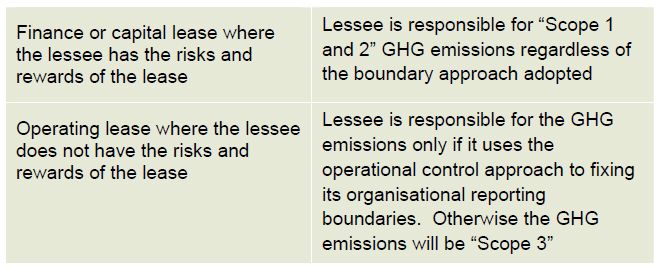

Deciding on responsibility

Each company is required to decide whether it is responsible for particular GHG emissions. Guidance issued by DEFRA acknowledges that the decision is not always straightforward, for example where buildings or assets are leased by or to the quoted company.

As a rule of thumb, DEFRA guidance suggests:

Where a lessee is not responsible, the presumption is that the lessor is responsible. The objective is to ensure that GHG emissions are captured, but not double-counted.

Special rules also apply to GHG emissions from sources that ought not to be wholly attributed to the reporting company. For example, carbon dioxide released by combustion of biomass for electricity or heat generation, or from processes such as industrial fermentation, should be reported separately. This is because carbon dioxide would in any event be likely to be released from those sources through natural decay. However, GHGs other than carbon dioxide released by those processes might fall within the company's reporting obligations. While natural decay might release sequestered carbon dioxide, it would not release nitrous oxide or methane associated with combustion or other industrial processes. Consequently, where biomass is used by a company it must decide whether those other GHG emissions are sufficiently "material" to require disclosure.

Overlap with other reporting regimes?

Quoted companies affected by the new regulations are already likely to be subject to reporting requirements - in particular those under the CRC Energy Efficiency Scheme, which has been in operation since 2010.

The new regulations are more extensive than CRC as they cover the full range of "Kyoto" gases. CRC, by contrast, is concerned only with carbon dioxide emissions. As with the special rules applicable to biomass combustion, a company falling within the CRC regime must decide whether GHG emissions such as methane and nitrous oxide, emitted in small quantities when fuel is combusted to generate electricity, ought to be reported.

Acting now to avoid non-compliance

A company's compliance is assessed after the end of its reporting year, and on the basis of its Strategic and Directors' reports. The new regime is firmly based on the principle of "comply or explain", meaning that the enforcing authority is bound to be at least as concerned with omission as with actual statements. The retrospective effect of the regulations must be taken into account. If data has not already been collected and analysed, it must be in place when those reports are being prepared, or its absence credibly explained.

Footnotes

1. Companies Act 2006 (Strategic Report and Directors' Report) Regulations 2013, SI 2013/1970

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.