The Council of the European Union has on 21 March 2013 formally

approved the European Venture Capital Funds Regulation (EVCFR).

EVCFR is intended to enter into force on the same day as when the

Alternative Investment Fund Managers Directive shall be by latest

implemented on a national level, i.e. on 22 July 2013. By contrast

to AIFMD, EVCFR does not require any actions to be taken from local

legislators, being a directly applicable regulation in the EU

member states. The most recent version concerning venture capital funds and social entrepreneurship funds are available on

the European Commission's web pages.

EVCFR will affect the marketing of European venture capital and

so-called social entrepreneurship funds. The requirements set by

EVCFR to the fund managers relate e.g. to investment portfolio,

investment techniques and other undertakings of the fund. These

rules are, however, significantly lighter than the burdensome

regulation brought by the AIFM Directive and, most importantly, a

voluntary framework for managers that would not be required to be

licensed under the AIFM Directive. This framework comes with a EU

passport: fund managers may, after domestic registration process,

market the qualified funds covered by EVCFR in all EU member states

without a need to separately register and obtain approval from

market authorities of each of the relevant member state. Thus,

EVCFR will make the EU-wide marketing of qualified venture capital

and social entrepreneurship funds considerably less

cumbersome.

In a nutshell, a qualifying venture capital fund would, based on

EVCFR, be a collective investment undertaking (anything save for a

UCITS fund) which intends to invest directly at least 70 percent of

its aggregate capital contributions (after deduction of all

relevant costs) to companies which qualify as small and

medium-sized companies at the moment of investment. The definition

refers to companies that are unlisted, employ fewer than 250

persons and have either an annual turnover not exceeding EUR 50

million or annual balance sheet not exceeding EUR 43 million.

Further, EVCFR would not apply to funds covered by AIFMD.

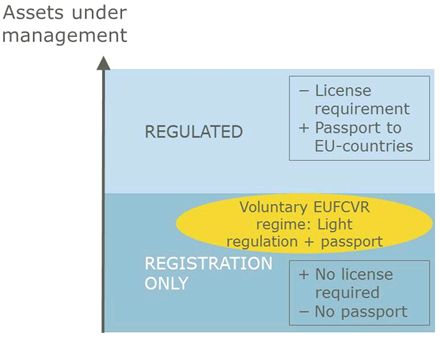

The AIFMD (blue) and EVCFR (yellow) regulations may be roughly

illustrated as follows:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.