The rate of new securities class action filings appears to be stabilizing, but that does not mean 2019 has been lacking in important developments in securities law. This mid-year update highlights what you most need to know in securities litigation trends and developments for the first half of 2019:

- The Supreme Court decided Lorenzo, holding that, even though Lorenzo did not "make" statements at issue and is thus not subject to enforcement under subsection (b) of Rule 10b-5, the ordinary and dictionary definitions of the words in Rules 10b-5(a) and (c) are sufficiently broad to encompass his conduct, namely disseminating false or misleading information to prospective investors with the intent to defraud.

- Because the Supreme Court dismissed the writ of certiorari in Emulex as improvidently granted, there remains a circuit split as to whether Section 14(e) of the Exchange Act supports an implied private right of action based on negligent misrepresentations or omissions made in connection with a tender offer.

- We explain important developments in Delaware courts, including the Court of Chancery's application of C & J Energy, as well as the Delaware Supreme Court's (1) application and extension of its recent precedents in appraisal litigation to damages claims, (2) elaboration of its recent holding on MFW's "up front" requirement, and (3) rare conclusion that a Caremark claim—"possibly the most difficult theory in corporation law upon which a plaintiff might hope to win a judgment"—survived a motion to dismiss.

- Finally, we continue to monitor significant cases interpreting and applying the Supreme Court's decisions in Omnicare and Halliburton II.

I. Filing And Settlement Trends

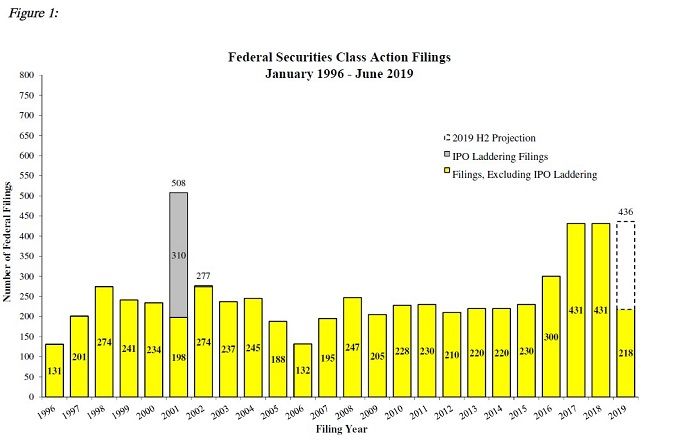

New federal securities class action filings in the first six months of 2019 indicate that annual filings are on track to be similar to the number of new cases filed in each of the prior two years. According to a newly released NERA Economic Consulting study ("NERA"), 218 cases were filed in the first half of this year. While there was a relative surge in new cases in the first quarter of the year, this higher level of new cases did not persist in the second quarter.

Filing activity in the first half of 2019 indicates a continuation of the shift in the types of cases observed in 2018—an increase in the number of Rule 10b-5, Section 11, or Section 12 cases, and a decrease in the number of merger objection cases. If the filing composition and levels observed in the first half of 2019 are indicative of the pattern for the rest of the year, we will see a 15% increase in Rule 10b-5, Section 11, and Section 12 cases compared to the approximate 1% growth in this category of filings in 2018. On the other hand, merger objection cases filed in 2019 are on pace to be more than 16% lower than similar cases filed in the prior year.

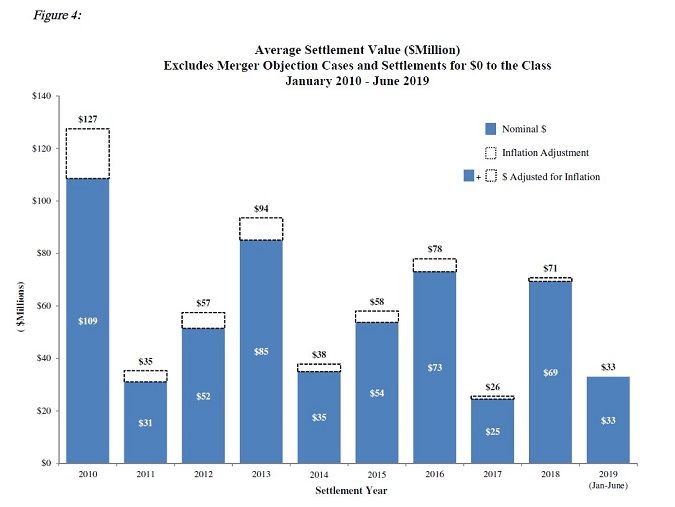

While the median settlement values for the first half of 2019 are roughly equivalent to those in 2018 (at $12.0 million, down from $12.70 million in 2018), average settlement values are down over 50% from 2018 (at $33 million, down from $71 million in 2018). That said, this discrepancy is due predominantly to one settlement in 2018 exceeding $1 billion. Excluding such outliers, we actually see a slight increase in average settlement values compared to the prior two years.

The industry sectors most frequently sued thus far in 2019 continue to be healthcare (22% of all cases filed), tech (20%), and finance (15%). Cases filed against healthcare companies in the first half of 2019 are showing the continuation of a downward trend from a spike in 2016, while cases filed against tech and finance companies are on pace with 2018.

A. Filing Trends

Figure 1 below reflects filing rates for the first half of 2019 (all charts courtesy of NERA). So far this year, 218 cases have been filed in federal court, annualizing to 436 cases, which is on pace with the number of filings in 2017 and 2018, and significantly higher than the numbers seen in years prior to 2017. Note that this figure does not include the many class suits filed in state courts or the rising number of state court derivative suits, including many such suits filed in the Delaware Court of Chancery.

B. Mix Of Cases Filed In First Half Of 2019

1. Filings By Industry Sector

As seen in Figure 2 below, the split of non-merger objection class actions filed in the first half of 2019 across industry sectors is fairly consistent with the distribution observed in 2018, with few indications of significant shifts or increases in particular sectors. As in 2018, the Health Technology and Services and the Electronic Technology and Technology Services sectors accounted for over 40% of filings. The two sectors reflecting the largest changes from 2018 thus far are Consumer Durables and Non-Durables (at 9%, up from 6% in 2018) and Consumer and Distribution Services (at 5%, down from 9% in 2018). See Figure 2, infra.

2. Merger Cases

As shown in Figure 3, 83 "merger objection" cases have been filed in federal court in the first half of 2019 —below the pace of 109 cases at this point in 2018. If the 2019 trend continues, the 166 merger objection cases projected to be filed in 2019 will be about 16% fewer than the 198 merger objection cases filed in the prior year.

C. Settlement Trends

As Figure 4 shows below, during the first half of 2019, the average settlement declined to $33 million, more than 50% lower than the average in 2018 but higher than the average in 2017. This phenomenon is primarily driven by one settlement in 2018 exceeding $1 billion, heavily skewing the average for that year. If we limit our analysis to cases with settlements under $1 billion, there is actually a slight increase in the average settlement value in 2019 compared to the prior years.

Finally, as Figure 5 shows, the median settlement value for cases was $12 million, which is in line with the median in 2018 and almost double the median value in 2017.

II. What To Watch For In The Supreme Court

A. Lorenzo Affirms That Disseminators Of False Statements May Be Held Liable Under Rules 10b-5(a) And 10b-5(c) Even If Janus Shields Them From Liability Under Rule 10b-5(b)

We discussed the Supreme Court's decision to grant review of Lorenzo v. Securities and Exchange Commission, No. 17-1077, in our 2018 Mid-Year Securities Litigation Update, and our 2018 Year-End Securities Litigation Update. Readers will recall that the question presented in Lorenzo was whether a securities fraud claim premised on a false statement that was not "made" by the defendant can be actionable as a "fraudulent scheme" under Section 17(a)(1) of the Securities Act and Exchange Act Rules 10b-5(a) and 10b-5(c), even though it would not support a claim under Rule 10b-5(b) pursuant to the Court's ruling in Janus Capital Group, Inc. v. First Derivative Traders, 564 U.S. 135 (2011).

On March 27, 2019, the Supreme Court affirmed the D.C. Circuit in a 6–2 opinion by Justice Breyer (Justice Kavanaugh took no part in the decision because he participated in the panel decision while a judge on the court of appeals). The Court held that the ordinary and dictionary definitions of the words in Rules 10b-5(a) and 10b-5(c) are sufficiently broad to encompass Lorenzo's conduct, namely disseminating false or misleading information to prospective investors with the intent to defraud, even if the disseminator did not "make" the statements and is thus not subject to enforcement under subsection (b) of the Rule. Lorenzo v. SEC, 587 U.S. ___ (2019), slip op. at 5–7.

Underlying the Court's opinion is the principle that the securities laws and regulations work together as a whole. The Court rejected Lorenzo's argument that Rule 10b-5 should be read to mean that each provision of the Rule governs different, mutually exclusive spheres of conduct. Under Lorenzo's reading, he could be liable for false statements only if his conduct violated provisions that specifically refer to such statements, such as Rule 10b-5(b), and could therefore not be liable under other provisions of the Rule, which do not specifically mention misstatements. The Court noted, however, that it has "long recognized considerable overlap among the subsections of the Rule" and related statutory provisions. Id. at 7–8. The opinion further noted that Lorenzo's conduct "would seem a paradigmatic example of securities fraud," making it difficult for the majority to reconcile Lorenzo's argument with the basic purpose and congressional intent behind the securities laws. Id. at 9.

The majority also adopted the SEC's argument that Janus concerned only Rule 10b-5(b), and thus does not operate to shield those who disseminate false or misleading information from scheme liability, even if they do not "make" the statement. In response to Lorenzo's contention that imposing primary liability here would weaken the distinction between primary and secondary liability, the Court drew what it characterized as a clear line: "Those who disseminate false statements with intent to defraud may be held primarily liable under Rules 10b-5(a) and (c)," as well as Section 10(b) of the Exchange Act and Section 17(a)(1) of the Securities Act, "even if they are secondarily liable under Rule 10b-5(b)." Id. at 10–11. Finally, the Court identified a flaw in Lorenzo's suggestion that he should only be held secondarily liable. Under that theory, someone who disseminated false statements (even if knowingly engaged in fraud) could not be held to have aided and abetted a "maker" of a false statement if the maker did not violate Rule 10b-5(b). That is because the aiding and abetting statute requires that there be a violator to whom the secondary violator provides "substantial assistance." Id. at 12. And if, under Lorenzo's theory, the disseminator did not primarily violate other subsections (perhaps because the disseminator lacked the necessary intent), the fraud might go unpunished altogether. Id. at 12–13.

We noted in our 2018 Year-End Securities Litigation Update that Justice Gorsuch appeared accepting of Lorenzo's positions during the oral argument, and he did join Justice Thomas (the author of Janus) in dissent. The dissent contended that the majority "eviscerate[d]" the distinction drawn in Janus between primary and secondary liability by holding that a person who did not "make" a fraudulent misstatement "can nevertheless be primarily liable for it." Id. at 1 (Thomas, J., dissenting). The dissent faulted the Court for holding, in essence, that the more general provisions of other securities laws each "completely subsumes" the provisions that specifically govern false statements, such as Rule 10b-5(b). Id. at 3. Instead, the dissenters argued that these specific provisions must be operative in false-statement cases, and that the more general provisions should be applied only to cases that do not fall within the purview of these more specific provisions.

B. Pending Certiorari Petitions

Regular readers of these updates will recall that we wrote about the Supreme Court's pending decision in Emulex Corp. v. Varjabedian, No. 18-459, in the 2018 Year-End Securities Litigation Update. In April, the Supreme Court heard oral argument and then dismissed the writ of certiorari as improvidently granted. Emulex Corp. v. Varjabedian, 587 U.S. ___ (2019), slip op. at 1. As is common in such dismissals, the Justices offered no explanation of why they dismissed the case. Therefore, there remains a circuit split as to whether Section 14(e) of the Exchange Act supports an implied private right of action based on negligent misrepresentations or omissions made in connection with a tender offer.

There is also at least one notable securities case in which a petition for certiorari is pending. Putnam Investments, LLC v. Brotherston, No. 18-926, an ERISA case, presents the question whether the plaintiff or defendant must prove that an alleged fiduciary breach related to investment option selection caused a loss to participants or the plan. The case also raises the issue of whether the First Circuit correctly held that showing that particular investment options did not perform as well as a set of index funds, selected by the plaintiffs with the benefit of hindsight, suffices as a matter of law to establish "losses to the plan." The Supreme Court has entered an order requesting the Solicitor General file a brief expressing the views of the United States. The government has not yet filed its brief in this case. We will continue to monitor the petition and provide an update if the Supreme Court grants certiorari.

III. Delaware Developments

A. Delaware Supreme Court Affirms Deal Price Is Best Evidence Of Fair Value In Appraisal, And Of Damages In Entire Fairness

Regular readers of these updates will recall that, since our 2017 Year-End Securities Litigation Update, we have been reporting on the significant shift in Delaware appraisal law resulting from the Delaware Supreme Court's landmark decision in Dell, Inc. v. Magnetar Global Event Driven Master Fund Ltd., 177 A.3d 1 (Del. 2017), where it directed the Court of Chancery to use market factors to determine the fair value of a company's stock. In our 2018 Mid-Year Securities Litigation Update, we wrote about the Delaware Court of Chancery's decision in Verition Partners Master Fund v. Aruba Networks, Inc., where the trial court interpreted Dell as endorsing a company's unaffected market price and deal price as reliable indicators of fair value under certain circumstances. 2018 WL 2315943, at *1 (Del. Ch. May 21, 2018). In April, however, the Delaware Supreme Court reversed the trial court, clarifying that, although the "unaffected market price" of a seller's stock "in an efficient market is an important indicator of its economic value that should be given weight" under appropriate circumstances, Dell "did not imply that the market price of a stock was necessarily the best estimate of the stock's so-called fundamental value at any particular time." Verition Partners Master Fund v. Aruba Networks, Inc., 210 A.3d 128, 2019 WL 1614026, at *6 (Del. Apr. 16, 2019). Eschewing remand, the Supreme Court instead ordered the trial court to enter judgment awarding deal price less synergies as the company's "fair value." Id. at *8–9.

Then, in May, the Delaware Supreme Court extended the same market-based deference from the appraisal context to damages claims in its affirmance of In re PLX Technology Inc. Stockholders Litigation, 2018 WL 5018535 (Del. Ch. Oct. 16, 2018), aff'd, 2019 WL 2144476, at *1 (Del. May 16, 2019) (TABLE). Late last year, the Delaware Court of Chancery determined in a post-trial opinion that an activist hedge fund aided and abetted a breach of fiduciary duties by directors in connection with their sale of the target company. 2018 WL 5018535, at *1. This was a pyrrhic victory, however, as the Court of Chancery concluded that the plaintiffs failed to prove their allegation that, had the company remained a stand-alone entity, its value would have exceeded the deal price by more than 50%. Id. at *2. Instead, the Court of Chancery found that "[a] far more persuasive source of valuation evidence is the deal price that resulted from the Company's sale process." Id. at *54; see also id. & n.605 (citing Dell, 177 A.3d at 30). In affirming the Court of Chancery's decision on appeal, the Delaware Supreme Court rejected the plaintiffs' argument that "the Court of Chancery erred . . . by importing principles from . . . appraisal jurisprudence to give deference to the deal price." In re PLX Tech. Inc. Stockholders Litig., 2019 WL 2144476, at *1 (Del. May 16, 2019) (TABLE).

B. Joint Valuation Exercise Constitutes Substantive Economic Negotiations Under Flood, Fails MFW's "Up Front" Requirement

In our 2018 Year-End Securities Litigation Update, we reported on the Delaware Supreme Court's decision in Flood v. Synutra International, Inc., where it held that the element of Kahn v. M & F Worldwide Corp. ("MFW"), 88 A.3d 635, 644 (Del. 2014) that requires a transaction to be conditioned "ab initio" or "up front" on the approval of both a special committee and a majority of the minority stockholders, in turn "require[s] the controller to self-disable before the start of substantive economic negotiations, and to have both the controller and Special Committee bargain under the pressures exerted on both of them by these protections." Flood v. Synutra Int'l, Inc., 195 A.3d 754, 763 (Del. 2018).

In Olenik v. Lodzinski, 208 A.3d 704 (Del. 2019), the Delaware Supreme Court added color to its holding in Flood that "up front" means "before the start of substantive economic negotiations," Flood, 195 A.3d at 763. In the decision underlying Olenik, the Court of Chancery found that, although the parties to the merger had "worked on the transaction for months" before implementing MFW's "up front" conditions, those "preliminary discussions" were "entirely exploratory in nature" and "never rose to the level of bargaining." Olenik, 208 A.3d at 706, 716–17. Disagreeing with and reversing the Court of Chancery, the Delaware Supreme Court held that "preliminary discussions transitioned to substantive economic negotiations when the parties engaged in a joint exercise to value" the merging entities. Id. at 717. In particular, the Delaware Supreme Court found it reasonable to infer that two presentations valuing the target "set the field of play for the economic negotiations to come by fixing the range in which offers and counteroffers might be made." Id. Thus, the parties could not invoke MFW's protections because they did not condition the transaction on approval of both a special committee and a majority of the minority stockholders until after these "substantive economic negotiations." Id.

C. Under C & J Energy, Curative Shopping Process "Cannot Be Granted" To Remedy Deal Subject To Entire Fairness

Recently, the Court of Chancery declined to "blue-pencil" a merger agreement resulting from a flawed process based on the Delaware Supreme Court's decision in C & J Energy Services v. City of Miami General Employees' & Sanitation Employees' Retirement Trust, 107 A.3d 1049 (Del. 2014). See FrontFour Capital Grp. LLC v. Traube, 2019 WL 1313408, at *33 (Del. Ch. Mar. 22, 2019). Recall that, in C & J Energy, the Delaware Supreme Court cautioned the Court of Chancery against depriving "adequately informed" stockholders of the "chance to vote on whether to accept the benefits and risks that come with [a flawed] transaction, or to reject the deal," 107 A.3d at 1070, where (1) "no rival bidder has emerged to complain that it was not given a fair opportunity to bid," id. at 1073, and (2) a preliminary injunction would "strip an innocent third party [buyer] of its contractual rights while simultaneously binding that party to consummate the transaction," id. at 1054.

In FrontFour, the plaintiff proved that the deal at issue was not entirely fair because conflicted insiders tainted the sale process; the special committee failed to inform itself adequately; standstill agreements prevented third parties from coming forward; and other deal protections prevented an effective post-signing market check, among other things. 2019 WL 1313408, at *32. Nevertheless, the Court of Chancery declined to grant "the most equitable relief" available—"a curative shopping process, devoid of [management] influence, free of any deal protections, plus full disclosures." Id. at *33. The Court of Chancery reasoned that it had "no discretion" to do so under C & J Energy because the injunction sought would "strip an innocent third party of its contractual rights" under the merger agreement. Id.

D. Delaware Supreme Court Holds Caremark Claim Adequately Pleaded

As we reported in our 2017 Year-End Securities Litigation Update, a Caremark claim generally seeks to hold directors personally accountable for damages to a company arising from their failure to properly monitor or oversee the company's major business activities and compliance programs. On June 19, 2019, the Delaware Supreme Court reversed the Court of Chancery's dismissal of a derivative suit against key executives and the board of directors of Blue Bell USA, carrying implications for both determinations of director independence and fiduciary duties under Caremark. See Marchand v. Barnhill, 2019 WL 2509617 (Del. June 19, 2019). In its demand futility analysis, the Court held that a combination of a "longstanding business affiliation" and "deep . . . personal ties" cast reasonable doubt on a director's ability to act impartially. Id. at *2. Notably, the reversal turned on the length and depth of one director's relationship with the CEO of Blue Bell and his family. Although being "social acquaintances who occasionally have dinner or go to common events" does not per se preclude one's independence, the current CEO's father and predecessor had hired, mentored, and quickly promoted the director in question to senior management. Id. at *11. The director maintained a close relationship with the CEO's family that spanned more than three decades and the family even spearheaded a campaign to name a college building after the director. Id. at *10. This combination of facts persuaded the Court that this director was not independent for demand futility purposes. Id. at *10–11.

The Court also held that a board's failure to implement oversight systems related to a "compliance issue intrinsically critical to the business operation" gives rise to a duty of loyalty claim under Caremark. Id. at *13. The Court concluded that because food safety compliance was critical to the operation of a "single-product food company," id at *4, neither the Company's nominal compliance with some applicable regulations, nor management's discussion of general compliance matters with the board were sufficient to satisfy the board's oversight responsibilities, id. at *13–14.

IV. Loss Causation Developments

The first half of 2019 saw several notable developments regarding loss causation, including continued developments relating to Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014), discussed below in Section VI.

Separately, on June 24, 2019, the Supreme Court rejected a petition for a writ of certiorari filed in First Solar, Inc. v. Mineworkers' Pension Scheme, which we discussed in the 2018 Mid-Year Securities Litigation Update. First Solar involved a perceived ambiguity in prior precedent regarding the correct test for loss causation under the Securities Exchange Act of 1934 (the "Exchange Act"). Readers will recall that the Ninth Circuit held in First Solar that loss causation can be established even when the corrective disclosure did not reveal the alleged fraud on which the securities fraud claim is based. Mineworkers' Pension Scheme v. First Solar, Inc., 881 F.3d 750, 754 (9th Cir. 2018), cert. denied, No. 18-164, 2019 WL 2570667 (U.S. June 24, 2019). First Solar filed its petition for writ of certiorari in August 2018, arguing that loss causation can be proven only if the market learns of, and reacts to, the underlying fraud. In May 2019, the Solicitor General filed an amicus brief recommending that certiorari be denied, arguing that the Ninth Circuit correctly rejected a "revelation-of-the-fraud" requirement for loss causation, pursuant to which a stock-price drop comes immediately after the revelation of a defendant's fraud.

Following the Ninth Circuit's decision in First Solar, some courts have found that a plaintiff adequately pleaded loss causation for the purposes of stating a claim under the Exchange Act when the revelation that caused the decline in a company's stock price could be tracked back to the facts allegedly concealed, thus establishing proximate cause at the pleadings phase. See, e.g., In re Silver Wheaton Corp. Sec. Litig., 2019 WL 1512269, at *14 (C.D. Cal. Mar. 25, 2019) (denying motion to dismiss); Maverick Fund, L.D.C. v. First Solar, Inc., 2018 WL 6181241, at *8–10 (D. Ariz. Nov. 27, 2018) (denying motion to dismiss and finding that plaintiffs had adequately pleaded facts that, if proven, would establish that disclosures related to misstatements were "casually related" to fraudulent scheme).

We will continue to monitor these and other developments regarding loss causation.

V. Falsity Of Opinions – Omnicare Update

In the first half of 2019, courts continued to define the boundaries of Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund, 135 S. Ct. 1318 (2015), the case in which the Supreme Court addressed the scope of liability for false opinion statements under Section 11 of the Securities Act. In Omnicare, the Court held that "a sincere statement of pure opinion is not an 'untrue statement of material fact,' regardless whether an investor can ultimately prove the belief wrong." Id. at 1327. Under that standard, opinion statements give rise to liability under only three circumstances: (1) when the speaker does not "actually hold[] the stated belief;" (2) when the statement contains false "embedded statements of fact;" and (3) when the omitted facts "conflict with what a reasonable investor would take from the statement itself." Id. at 1326–27, 1329.

Consistent with past years, Omnicare remains a high bar to pleading the falsity of opinion statements. See, e.g, Plaisance v. Schiller, 2019 WL 1205628, at *11 (S.D. Tex. Mar. 14, 2019) (dismissing complaint that was "[m]issing . . . allegations of fact capable of proving that [the company] did not subjectively believe its audit opinions when they were issued"); Teamsters Local 210 Affiliated Pension Tr. Fund v. Neustar, Inc., 2019 WL 693276, at *5 (E.D. Va. Feb. 19, 2019) (finding that plaintiffs did not "allege facts that create a strong inference that at the time they [made the alleged misstatement], the Defendants could not have reasonably held the opinion" proffered). For example, in Neustar, plaintiffs alleged that defendants' opinion that a certain transition "would occur by September 30, 2018" was false or misleading. 2019 WL 693276, at *5. Even though defendants were in possession of a "Transition Report, which warned that the transition might not occur" by that date, the court found that "[t]hese statements were far from definitive pronouncements that the transition date would occur later than September 2018." Id.

In addition, courts have continued to flesh out the contours of when a plaintiff has alleged that a company is in possession of sufficient information cutting against its statements to render it liable for an omission. In In re Ocular Therapeutix, Inc. Securities Litigation, the court found that a CEO's statement that the company "think[s]" it had remedied deficiencies leading to the FDA's denial of its New Drug Application was inactionable, even where the FDA later rejected the resubmitted application. 2019 WL 1950399, at *8 (D. Mass. Apr. 30, 2019). Not only did the CEO's language "signal[] to investors that his statement was an opinion and not a guarantee," but he also cautioned that it was up to the FDA to determine whether or not those deficiencies were corrected. Id. In Securities & Exchange Commission v. Rio Tinto plc, the SEC alleged that Rio Tinto violated securities laws by overstating the valuation of its newly acquired coal business when there had been certain adverse developments concerning the ability to transport coal and the quality of coal in the ground. 2019 WL 1244933, at *9 (S.D.N.Y. Mar. 18, 2019). The court dismissed the claim based on early valuation statements because those statements were opinions that "'fairly align[ed] with'" information known at the time: namely, the main transportation option had not been entirely rejected, and the SEC did not "allege that Rio Tinto had come to fully appreciate the difficulties" concerning other transportation options and coal reserves by the time of those statements. Id. The SEC has moved to amend its complaint. Gibson Dunn represents Rio Tinto in this and other litigation.

This year, courts also weighed in on the question of whether Omnicare applies to claims other than those brought under Section 11. Specifically, a Northern District of California court found that "[t]he Ninth Circuit has only extended Omnicare to Section 10(b) and Rule 10b-5 claims, not to Section 14 claims," and therefore "decline[d] to extend Omnicare past the Ninth Circuit's guidance." Golub v. Gigamon Inc., 372 F. Supp. 3d 1033, 1049 (N.D. Cal. 2019) (citing City of Dearborn Heights Act 345 Police & Fire Ret. Sys. v. Align Tech., Inc., 856 F.3d 605, 616 (9th Cir. 2017)). Gibson Dunn represents several defendants in that matter. In contrast, the Fourth Circuit applied Omnicare to dismiss a Section 14 claim without any discussion about Omnicare's limitations, determining that a forward-looking statement was still actionable as an omission. Paradise Wire & Cable Defined Benefit Pension Plan v. Weil, 918 F.3d 312, 322–23 (4th Cir. 2019). Rather, the court emphasized the importance of context when evaluating opinion statements, noting that "words matter" and, as in Paradise Wire, can "render the claim for relief implausible." Id. at 323. "When the words of a proxy statement, like the ones in this case, . . . contain tailored and specific warnings about the very omissions that are the subject of the allegations, those words render the claim for relief implausible." Id.

Additionally, a District of Delaware court recently declined to apply Omnicare to Section 10(b) claims: "Because the Third Circuit has twice declined to decide that Omnicare applies to Exchange Act claims, the Court is reluctant to decide that issue of first impression in connection with a motion to dismiss." Lord Abbett Affiliated Fund, Inc. v. Navient Corp., 363 F. Supp. 3d 476, 496 (D. Del. 2019) (citing Jaroslawicz v. M & T Bank Corp., 912 F.3d 96 (3d Cir. 2018); In re Amarin Corp. PLC Sec. Litig., 689 F. App'x 124, 132 n.12 (3d Cir. 2017)).

The Southern District of New York also considered whether Omnicare required broad disclosure of attorney-client privileged communications that might bear on whether omitted information rendered an opinion misleading. Pearlstein v. BlackBerry Ltd., 2019 WL 1259382, at *16 (S.D.N.Y. Mar. 19, 2019). In Pearlstein, plaintiffs argued that under Omnicare, a company's "decision to include a legal opinion in [a] press release waived all attorney-client communications" related to the issuance of that release. Id. at *15. The court noted that Omnicare did not mandate a wholesale waiver, but "[a]t best . . . suggest[ed] that communications specific to a particular subject allegedly omitted or misrepresented within a securities filing may be subject to disclosure and, if the communications happen to be privileged, those communications may be subject to a finding of waiver." Id. at *16. Accordingly, the company could not insulate itself with the privilege—documents containing relevant factual information were discoverable. However, privilege was not waived over the "side issue" of the company's legal exposure, including as to documents on the strength and likelihood of any legal claims and "communications conducted solely for purposes of document preservation in connection with anticipated legal claims." Id.

VI. Courts Continue To Define "Price Impact" Analysis At The Class Certification Stage

We are continuing to monitor significant decisions interpreting Halliburton Co. v. Erica P. John Fund, Inc., 573 U.S. 258 (2014) ("Halliburton II"), but the one federal circuit court of appeal decision issued in the first half of 2019 did little to resolve outstanding questions regarding what it will mean for securities litigants. Recall that in Halliburton II, the Supreme Court preserved the "fraud-on-the-market" presumption, permitting plaintiffs to maintain the common proof of reliance that is required for class certification in a Rule 10b-5 case, but also permitting defendants to rebut the presumption at the class certification stage with evidence that the alleged misrepresentation did not impact the issuer's stock price. There are three key questions we have been following in the wake of Halliburton II. First, how should courts reconcile the Supreme Court's explicit ruling in Halliburton II that direct and indirect evidence of price impact must be considered at the class certification stage, Halliburton II, 573 U.S. at 283, with the Supreme Court's previous decisions holding that plaintiffs need not prove loss causation or materiality until the merits stage? See Erica P. John Fund, Inc. v. Halliburton Co., 563 U.S. 804, 815 (2011); Amgen Inc. v. Conn. Ret. Plans & Trust Funds, 568 U.S. 455 (2013). Second, what standard of proof must defendants meet to rebut the presumption with evidence of no price impact? Third, what evidence is required to successfully rebut the presumption?

As noted in our 2018 Year-End Securities Litigation Update, the Second Circuit addressed the first two questions in Waggoner v. Barclays PLC, 875 F.3d 79 (2d Cir. 2017) ("Barclays") and Arkansas Teachers Retirement System v. Goldman Sachs Group, Inc., 879 F.3d 474 (2d Cir. 2018) ("Goldman Sachs"). Those decisions remain the most substantive interpretations of Halliburton II. Barclays addressed the standard of proof necessary to rebut the presumption of reliance and held that after a plaintiff establishes the presumption of reliance applies, the defendant bears the burden of persuasion to rebut the presumption by a preponderance of the evidence. This puts the Second Circuit at odds with the Eighth Circuit, which cited Rule 301 of the Federal Rules of Evidence when reversing a trial court's certification order on price impact grounds, see IBEW Local 98 Pension Fund v. Best Buy Co., 818 F.3d 775, 782 (8th Cir. 2016), because Rule 301 assigns only the burden of production—i.e., producing some evidence—to the party seeking to rebut a presumption, but "does not shift the burden of persuasion, which remains on the party who had it originally." Fed. R. Evid. 301. Nonetheless, that inconsistency was not enough to persuade the Supreme Court to review the Second Circuit's decision. Barclays PLC v. Waggoner, 138 S. Ct. 1702 (Mem.) (2018) (denying writ of certiorari).

In Goldman Sachs, the Second Circuit vacated the trial court's ruling certifying a class and remanded the action, directing that price impact evidence must be analyzed prior to certification, even if price impact "touches" on the issue of materiality. Goldman Sachs, 879 F.3d at 486. On remand, the district court again certified the class. In re Goldman Sachs Grp. Sec. Litig., 2018 WL 3854757, at *1–2 (S.D.N.Y. Aug. 14, 2018). Plaintiffs argued on remand that because the company's stock price declined following the announcement of three regulatory actions related to the company's conflicts of interest, previous misstatements about its conflicts had inflated the company's stock price. See id. at *2. Defendants' experts testified that correction of the alleged misstatements could not have caused the stock price drops, both because thirty-six similar announcements had not impacted the company's stock price and because alternative news (i.e., news of regulatory investigations), in fact, caused the price drop. Id. at *3. The court found the plaintiffs' expert's "link between the news of [the company]'s conflicts and the subsequent stock price declines . . . sufficient," and defendants' expert testimony insufficient to "sever" that link. Id. at *4–6.

In January, however, the Second Circuit agreed to review Goldman Sachs for a second time. See Order, Ark. Teachers Ret. Sys. v. Goldman Sachs, Case No. 18-3667 (2d Cir. Jan. 31, 2019) ("Goldman Sachs II"). In Goldman Sachs II, the Second Circuit is poised to address what evidence is sufficient to rebut the presumption and how the analysis is affected by plaintiffs' assertion that the alleged misstatements' price impact is evidenced not by a price increase when the alleged misstatement is made, but by a price drop when the alleged misstatements are corrected, known as "price maintenance theory."

Defendants-appellants challenged the district court's finding in two primary ways. First, they argued that the district court impermissibly extended price maintenance theory. See Brief for Defendants-Appellants, Goldman Sachs II, at 28–52 (2d Cir. Feb. 15, 2019). They reasoned that a price maintenance theory is unsupportable where the alleged corrective disclosures revealed no concrete financial or operational information that had been hidden from the market for the purpose of maintaining the stock price, see id. at 28–40, and where the challenged statements are too general to have induced reliance (and thus impacted the stock's price), see id. at 40–50. Second, defendants-appellants argued that the district court misapplied the preponderance of the evidence standard by considering plaintiffs-appellees' allegations as evidence and misconstruing defendants-appellants' evidence of no price impact. See id. at 53–67.

Plaintiffs-appellees responded that defendants-appellants' price-maintenance arguments are not supported by law and that such arguments regarding the general nature of the statements are, in essence, a materiality challenge in disguise and thus not appropriate at the class certification stage. Brief for Plaintiffs-Appellees, Goldman Sachs II, at 20–30 (2d Cir. Feb. Apr. 19, 2019). Plaintiffs-appellees further argued that the district court did not abuse its discretion in weighing the evidence. Id. at 36–61.

Defendants-appellants submitted their reply brief in May, Reply Brief for Defendants-Appellants, Goldman Sachs II (2d Cir. May 3, 2019), and the Second Circuit heard the case in June. Seven amicus briefs were filed in this case, including by the United States Chamber of Commerce and a number of securities law experts supporting defendants-appellants, and by the National Conference on Public Employee Retirement Systems supporting plaintiffs-appellees.

Our 2018 Year-End Securities Litigation Update also noted that the Third Circuit was poised to address price impact analysis in Li v. Aeterna Zentaris, Inc. in the coming months. Briefing there invited the Third Circuit to clarify the type of evidence defendants must present, including the burden of proof they must meet, to rebut the presumption of reliance at the class certification stage and whether statistical evidence regarding price impact must meet a 95% confidence threshold. The district court had rejected defendants' argument that plaintiff's event study rebutted the presumption, and criticized defendants for not offering their own event study. See Li v. Aeterna Zentaris, Inc., 324 F.R.D. 331, 345 (D.N.J. 2018). With limited analysis, the Third Circuit affirmed, finding that the district court did not abuse its discretion in its consideration of conflicting expert testimony. Vizirgianakis v. Aeterna Zentaris, Inc., 2019 WL 2305491, at *2–3 (3d Cir. May 30, 2019).

We will continue to monitor developments in Goldman Sachs II and other cases.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.