- within Government, Public Sector, Coronavirus (COVID-19) and Strategy topic(s)

Overview

2018 was another exciting year for M&A activity in the automotive sector. Accelerated growth in U.S. and global economies from the last quarter of 2017 through most of 2018 provided added munitions in the continuing arms-race for emerging automotive technology supremacy and the industry's expansion into new verticals like ride-sharing and other mobility apps. We saw deal volumes in the automotive sector remain strong and deal values at or near all-time highs despite a number of emerging factors that traditionally could be seen as having material dampening effects on M&A activity in the sector, including rising interest rates and geopolitical uncertainties relating to the imposition of tariffs and opening up longstanding trade agreements. While some of these headwinds, and the recent GM announcement and anticipated Ford announcement of cutbacks, have the potential to reduce capital necessary for investments or otherwise risk encouraging some to take a "wait and see" approach, short of the bottom unexpectedly falling out from the economy, there appears to be continuing inertia in the automotive M&A deal-space in 2019 for another good year for deal activity. OEMs, suppliers, technology companies and other investors of all kinds (from traditional private equity, to venture capital funds to sovereign wealth funds) appreciate that there is no time to wait in order seize lucrative opportunities in order to position themselves for long-term success in an industry that is so quickly evolving.

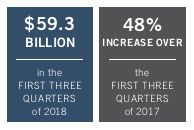

Though we await final numbers for Q4 of 2018, we know that M&A activity through the first three quarters was very strong. PwC reported that the aggregate value of M&A deals in the automotive sector through the end of quarter three of 2018 was $59.3 billion, on pace to be the highest in the last 10 years and which represented a 48% increase over the first three quarters of 2017. Some of the more notable larger-value deals include Tenneco's acquisition of supplier Federal Mogul for $5.4 billion and Novelis, Inc.'s announced acquisition of Aleris Corp., a producer of aluminum rolled products for the industry for over $2.6 billion. Market watchers have also continued to see high purchase price multiples for automotive transactions, especially in the software and certain parts and components manufacturing categories. A clear example of this is Cars.com's acquisition of Deal Inspire, an automotive advertising software and services provider, for healthy EBITDA (earnings before interest, taxes, depreciation and amortization) multiple of 41x. Overall, PwC saw average EBITDA transaction multiples through the first half of 2018 hold steady at 8.4x from 8.3x in 2017.

While 2018 was a great year for M&A activity in the automotive sector some reasonably question whether this trend can continue into and through 2019 given a number concerning macroeconomic developments and market uncertainties. Several of these factors have the potential to dampen deal activity, including rising interest rates, tariffs and trade disputes and certain regulatory developments. In addition, as we enter the 9th year of automotive market expansion coming out of the Great Recession, many are forecasting a cyclical recession on the near term horizon (by 2020), which would hinder some M&A activity while providing opportunities as well.

First is the continual ratcheting up of interest rates. The U.S. Federal Reserve Board of Governors raised interest rates four times in 2018 and is expected to continue to raise rates at least twice in 2019, although recent comments and market volatility may dictate a more "wait and see" approach. Rising interest rates always have the potential to slow deal activity as buyers who typically rely on debt to facilitate deal making, such as private equity investors, as more cash flow is devoted to debt amortization vs. paying equity value.

A second factor which of course has the whole of the automotive industry worried are the imposition of tariffs that do and would necessarily lead to increased vehicle prices, lower sales and therefore less capital available for investment and transaction activity. According to an October 2018 report conducted by the Center for Automotive Research, a 25% tariff on U.S. imports of light vehicles and parts, which remains a possibility at the time this article is being written, would drop U.S. light vehicle sales by 12%, reduce U.S. light vehicle export by 357,000 units and lead to increased light vehicle prices for consumers of at least 10%. Since President Trump's executive order in March 2018 to impose tariffs of 10% on imported aluminum and 25% on imported steel under Section 232 of the Trade Expansion Act of 1962, we have seen a back and forth of reprisals and threats to and from other countries, China in particular, that threaten to have a material impact on the industry. Relatedly, most Free Trade Agreements (such as NAFTA) are in some stage of renegotiation and recently the U.S., Canada and Mexico have agreed in principle to change and rebrand NAFTA, which has now been named the U.S.-Mexico-Canada Agreement (USMCA). Changes to long-standing trade agreements have the potential to disrupt the status quo and otherwise generate uncertainty in the marketplace, which can be bad for deal-making as it has the potential can drag down or delay decision-making and make business due diligence more troublesome. The impacts of any trade policy changes will continue to be watched closely as we enter 2019.

Another regulatory development in the U.S. worth noting is the recent codification of foreign investment restrictions imposed by the Committee on Foreign Investment in the United States ("CFIUS"), which is an interagency committee that conducts national security reviews of foreign investments in U.S. businesses, following the August 2018 passage of the Foreign Investment Risk Review Modernization Act ("FIRRMA"). Under FIRMMA, which in part codified existing CFIUS practice, CFIUS is empowered to block or even unwind cross-border investment transactions that it views as a potential threat to U.S. national security (which concept increasingly is being merged with "U.S. economic security"). CFIUS review has been more recently focused on critical infrastructure and access to sensitive technology and has been intently focused on investments from China and certain other geographies in U.S. companies that are developing technologies related to electric and autonomous vehicles. Even if transactions may eventually pass CFIUS muster the process to obtain clearance from CFIUS is time-consuming and expensive, as application of the "Foreign Ownership, Control and Influence" rules take some time to diligence in almost all transactions. Given these increased risks it is no wonder that we have already seen a decrease in investments in U.S. companies from China, based on figures from Thomson Reuters and research group Dealroom. In addition, over 75% of bankers, lawyers and consultants interviewed on the topic by Reuters, said their Chinese clients were increasingly choosing Europe over the United States because of growing difficulties with CFIUS. This has the potential to have a direct impact on automotive deal activity as, according to Reuters, in the last five years alone Chinese companies have funded at least 80 U.S. transportation startups with a combined valuation of more than $80 billion.

Finally, as mentioned, the automotive expansion cycle is entering its ninth year in North America, and production and sales numbers all indicate a market that is plateaued, post-peak and starting to decline. General Motors recent announcement of planned production cuts to align with sales and to focus on autonomous and other investments, is an early harbinger that automotive suppliers with an unhealthy product or platform mix, combined with leverage, may face challenges in adapting to market and production changes and create distressed M&A opportunities for some buyers.

All of the factors noted above have the potential to have some measurable negative impact investment on deal activity in the automotive sector in 2019. Nevertheless, the overall outlook for automotive M&A remains positive on balance due to the continued fervor surrounding investment in ride sharing/mobility, autonomous/connected vehicle, online vehicle dealerships/trading platforms and other technological vehicle features and platforms. The automotive industry is transforming at an ever-accelerating pace. As Lisa Joy Rosner, CMO of Otonomo conveyed to her interview at Flex, car manufacturers are transitioning from being hardware to software manufactures and now find themselves in a position where it is necessary to "continually update their software and provide service far beyond the initial transaction." This paradigm shift is leading manufacturers, suppliers, equity/venture funds and technology companies to continue to invest heavily in automotive technologies, bringing with it changes to business models and product offerings. And, because of the significant capital requirements and uncertainties, we will continue to see collaborations like Honda's investment in GM/Cruise Automation and Ford's reported current talks with Volkswagen, especially among OEMs that have "complementary" (read: non-overlapping) strengths and geographies.

One of the most interesting developments of the last few years has been that strategic investors are increasingly becoming active in early stage venture investing opportunities. Seventy-five of the Fortune 100 are active in corporate venturing and over 40 have dedicated corporate venture capital teams. The automotive sector is at the center of much of this strategic investment with General Motors, Honda, Ford, BMW, Toyota, Daimler AG, Volkswagen, among others, all making sizable investments. For founders/ sellers of early-stage automotive technology companies these corporate venture capital groups can offer several advantages over "traditional" venture capital funds, including dedicated marketing and research/development groups, built-in customers and distribution channels and have a perception that they will generally play a more passive role in management than your average traditional venture capital fund. However, strategic venture capital funds are also frequently perceived by potential targets as generally slower to make decisions, less familiar with the needs of venture capital-backed companies and more focused on strategic objectives that may not always be consistent with the target's objectives. On balance in 2019, CVCs are expected to continue to provide a helpful influx of capital in critical segments of the evolving automotive and mobility industries.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]