FINRA's Reorganized and Simplified Advertising Web Pages

The FINRA Advertising Regulation Department recently reorganized and updated its webpage, which is available here: https://goo.gl/JJpfEP. The updated webpage is organized into six areas: frequently asked questions, notices by topic, education and training, how to file, what and when to file, and a section for new and pending member firms. In the frequently asked questions section, all FINRA interpretive guidance on Rule 2210 (Communications with the Public) is organized and indexed in one place. Similarly, all advertising regulation-related FINRA notices are indexed and organized together.

These indexed materials are a great improvement over the anonymous list of notices at the end of Rule 2210, providing context and order for practitioners and others seeking FINRA's view on advertising and communications.

SEC Report on Fiscal Year 2018 Enforcement Results

On November 2, 2018, the Securities and Exchange Commission's Enforcement Division (the "Division") released its annual report for fiscal year 2018. Based on the five principles laid out in the Division's FY 2017 annual report, this year's report focuses its assessment on the Division's performance relating to: (1) focusing on the Main Street investor; (2) focusing on individual accountability; (3) keeping pace with technological change; (4) imposing remedies that most effectively further enforcement goals; and (5) constantly assessing the allocation of resources. Highlighting its focus on retail investors, the Division noted it returned $794 million dollars to harmed investors. Two major initiatives were taken in FY 2018: first, the Retail Strategy

Task Force; second, the Share Class Selection Disclosure (SCSD) Initiative. The SEC brought a mix of 821 actions, including 490 standalone actions. The SEC obtained judgments and orders totaling $3.945 billion in disgorgement and penalties. It suspended trading in the securities of 280 companies, and obtained nearly 550 bars and suspensions. To read this annual report, visit https://goo.gl/PM3CCi.

OCIE Examination Initiatives Will Focus on Proprietary Indices

The Office of Compliance Inspections and Examinations ("OCIE") released a Risk Alert on November 8, 2018 that provided information regarding OCIE's risk-based examination initiatives focused on matters relevant to certain registered investment companies. When assessing Index Funds that track custom-built indexes, the staff will assess the unique risks and challenges associated with the roles of advisers and index providers as they relate to the selection and weighting of the custom-built or bespoke index components, ongoing index administration, management of mutual and exchange-traded funds and related performance advertising.

- The OCIE noted, during these examinations, they will also seek to:

- Review the manner in which the portfolios are managed compared to the funds' disclosures to investors describing their strategy;

- Understand the nature of services provided by the index providers, and the adequacy of disclosures made to mutual and exchange-traded funds' boards regarding the index providers;

- Assess whether any conflicts of interest between the index providers and advisers are appropriately addressed; and

- Review the effectiveness of mutual and exchange-traded funds' compliance programs for portfolio management and their boards' oversight of such programs.

The OCIE encourages registrants to reflect upon their own practices, policies, and procedures, as applicable, and to consider improvements in their supervisory, oversight, and compliance programs. The Risk Alert can be found in full here.

New Jersey to Propose a Uniform Fiduciary Standard for Financial Professionals

In a recent notice of pre-proposal, the New Jersey Bureau of Securities (NJBOS) is contemplating a uniform fiduciary standard for financial professionals, including broker-dealers and investment advisers. While a formal rule has not been proposed, the NJBOS intends to make it a dishonest or unethical business practice to fail to act in accordance with a fiduciary duty when recommending to a customer an investment strategy or the purchase, sale, or exchange of any security or securities, or when providing investment advisory services to a customer. The NJBOS cites a comprehensive study by the SEC in 2011, which was mandated by the Dodd-Frank Act (the "913 Study"), in support of the uniform fiduciary standard. For example, the NJBOS highlighted the finding of the 913 Study that many retail investors do not understand the differences between investment advisers and broker-dealers or the standards of care applicable to investment advisers and broker-dealers. The uncertainty of the rule making process at the federal level is another factor that led the NJBOS to issue the pre-proposal. (One might question whether this viewpoint has been overtaken by events, given proposed SEC Regulation Best Interest.) The NJBOS concluded that investors are without adequate protection under the varying fiduciary standards imposed on different investment professionals.

Regarding the rule text, some have predicted that NBBOS's proposed fiduciary rule would be similar to the fiduciary rule adopted by the Department of Labor, which was vacated by the Fifth Circuit in March 2018.

The NJBOS is soliciting comments on the pre-proposal. The American Retirement Association (the "ARA") submitted a comment letter asking that services provided to ERISA plans be exempted from the proposed fiduciary rule. The ARA reasoned that the state rule would be pre-empted by ERISA statutes.

In public hearings, representatives of the Securities Industry and Financial Markets Association (SIFMA) and other financial industry participants testified against the pre-proposal. SIFMA urged NJBOS to wait until the SEC finalizes its Regulation Best Interest. SIFMA's testimony is consistent with its position that there should be federal, not state, governance in this area, as reiterated by SIFMA's president and CEO Kenneth E. Bentsen Jr. in a recent briefing on SIFMA's 2019 policy outlook. On the other hand, advisers and planners, such as the Financial Planning Association, supported NJBOS's rulemaking proposal, and generally agree with NJBOS's position that Regulation Best Interest provides insufficient protection for investors.

SEC Investor Advisory Committee's Recommendations Regarding Proposed Regulation Best Interest

The SEC Investment Advisory Committee (IAC) recommended1 the following enhancements to proposed Regulation Best Interest ("Proposed Regulation BI") in furtherance of its underlying goals:

- Clarify the best interest standard without abandoning the principles-based approach. Proposed Regulation BI, as presently worded, requires brokers and advisers to act in their customers' best interests without specifying how to do so. The IAC recommends clarifying the meaning of this obligation by "requiring broker-dealers, investment advisers and their associated persons to recommend the investments, investment strategies, accounts or services, from among those they have reasonably available to recommend, that they reasonably believe to be the best options for the investor."2 The IAC believes that the exact meaning of the best interest standard remains vague, and the IAC's recommendation may address the ambiguity while avoiding a "one size fits all" approach.

Recommending the best option for the investor requires analysis of each investor's needs and goals, the relationship between the investor and broker or adviser, the available investment options and all other facts and circumstances relevant to the investor's risk appetite.

- Expand the scope of the best interest obligation to cover rollover recommendations and recommendations by dual registrant firms about account types. The IAC believes that the advice given on account types and rollover recommendations, among others, made at the outset of the BD/IA relationship is crucially important (often even more so than advice regarding specific transactions), and should also be subject to the best interest standard.

- Proposed Regulation BI should explicitly state that the best interest standard is a fiduciary duty. According to the IAC, clarifying that the best interest standard is a principles-based fiduciary obligation is important. The IAC notes that investors would be best protected in a regulatory environment that requires investment advisers and broker-dealers to place the interest of clients ahead of their own, and that investors reasonably expect this from the phrase "best interest." However, the present regulatory environment does not meet this standard because an adviser's duties can be satisfied through mere disclosure. Once advisers have made the required disclosures, they can and do engage in practices that put their interests ahead of those of clients, such as recommending higher-cost funds. The IAC views this mismatch as a regulatory gap and believes that declaring characterizing the best interest standard as a fiduciary standard will address this.

- The SEC should test Form CRS disclosures for effectiveness prior to adoption. Proposed Regulation BI requires that a summary disclosure describing the relationship with clients be given to prospective clients (Form CRS). The IAC is concerned that Form CRS will not likely achieve its intended purpose of reducing investor confusion and supporting informed decision-making. Hence, the IAC suggests that the disclosures should undergo usability testing. If usability testing reveals that these disclosures are not effective, the IAC recommends that the SEC should work with a disclosure design expert before finalizing the Form CRS.

More details on IAC's recommendation may be viewed here: https://goo.gl/Yk4E3Z.

Daily Redeemable Notes versus Exchange Traded Notes: Fraternal Twin, Kissing Cousin or Lonely Stepchild?

Since 2006, investors have been able to choose among exchange traded notes ("ETNs") in many different variations. Under the listing rules of the relevant national securities exchange, ETNs may reference the performance of equity indices, commodities, currencies, fixed income securities, futures or any combination of two or more of these underlying reference assets. ETNs have evolved from their original form of referencing the performance of an index more or less on a delta-one basis to more complicated, leveraged, daily reset structures perhaps better suited for professional investors. ETNs have certain common features:

- A listing on a national securities exchange, which generally ensures liquidity for popular ETNs;

- A daily investor fee, which accrues and is charged against the investor at maturity or early redemption or acceleration of the ETN;

- A redemption fee, charged against the investor if the investor redeems the ETN with the issuer;

- An intraday indicative value, published in real time and calculated by the issuer pursuant to a preset formula set forth in the prospectus, which generally reflects the value of the ETN based on the performance of the underlying reference asset and takes into account the accrued daily investor fee;

- The ETN issuer's affiliated broker-dealer acts as a market maker in the ETNs; and

- A continuous issuance process, meaning that the issuer is constantly "creating" new ETNs and issuing these to meet investor demand.

Most ETNs are callable by the issuer after six months from their initial issuance. Because of the availability of a trading price for the ETN, the level of the underlying reference asset and also the ETN's intraday indicative value, ETN investors have sufficient pricing information upon which to base an investment decision, sell in the secondary market, redeem or hold.

DAILY REDEEMABLE NOTES

At least one issuer has come out with a variation on the ETN theme, issuing a "daily redeemable note" ("DRN"). We are aware of one registered DRN and understand that there are several versions issued in exempt offerings or as exempt securities. What is a DRN, and how does it differ from an ETN?

DRNs are not listed on a national securities exchange. Consequently, a DRN could reference the performance of an underlying reference asset that is not within the permissible categories allowed by the exchanges. DRNs have some similarities to ETNs:

- A daily investor fee, which accrues and is charged against the investor at maturity or early redemption or acceleration of the DRN;

- A redemption fee, charged against the investor if the investor redeems the DRN with the issuer;

- An issuer call option; and

- A continuous issuance, with the issuer constantly creating new DRNs and issuing notes subject to investor demand.

Why would an issuer choose to issue a DRN instead of an ETN? ETNs come with a certain amount of fixed costs for the issuer. The exchange has an annual listing fee, which will have to be paid whether or not a sufficient number of ETNs are outstanding or actively trading in order to justify the listing fees. The issuer must stand ready to buy back ETNs from investors who do not use the redemption feature. For an issuer whose securities are exempt from registration under the Securities Act of 1933 (the "Securities Act") under Section 3(a)(2) thereof (a bank), even if that issuer could list its securities on a national securities exchange in compliance with Section 12(i) of the Securities Exchange Act of 1934 (the "Exchange Act"), it may not want to become subject to the corporate governance and other rules of an exchange.

REGULATION M ISSUES

The continuous creation feature of DRNs leads to some interesting differences from ETNs. Issuers of ETNs and DRNs are constantly issuing, or creating, new securities. For example, a typical ETN prospectus supplement will state that it relates to at least $50,000,000 of ETNs, but will disclose that at least $4,000,000 of ETNs were issued on the original issuance date at par and that the rest of the stated amount will be sold at market or negotiated prices from time to time. DRN prospectus supplements make a similar statement, but they are not bound by the requirements of an exchange to issue at least $4,000,000 of the DRNs on the original issuance date. A DRN prospectus will generally indicate a smaller amount sold on the original issue date. This continuous issuance results in recurring "restricted periods" for purposes of Regulation M. The restricted period for ETNs and DRNs continues until the securities are called or mature or until the issuer ceases new creations.

During the applicable restricted period, an ETN or DRN issuer could not redeem existing securities, or have its affiliated broker-dealer maintain a secondary market in the securities, without violating Regulation M, absent an exemption or no-action relief. For ETN issuers, the SEC's Division of Trading and Markets provided that exemptive relief in the Barclays Bank PLC Staff No-Action Letter (July 27, 2006) (the "iPath Letter"). Under the iPath letter, broker-dealer affiliates of ETN issuers could bid for or purchase ETNs in market-making transactions during their distribution of the ETNs without violating Rule 101 of Regulation M. The iPath Letter also permitted ETN issuers and their affiliates to redeem ETNs during the restricted period, without violating Rule 102 of Regulation M.

Because DRNs are not listed, DRN issuers may not rely on the iPath Letter. The lack of a listing and real-time availability of the DRNs' public trading price removes both the liquidity and pricing transparency elements present in the iPath Letter. In granting relief from the prohibitions of Regulation M, the Staff of the Division of Trading and Markets stated in the iPath Letter that it based its position "particularly [on the representations that the ETNs] are redeemable at the option of the holder on a weekly basis ... and that the secondary market price [of the ETNs] should not vary substantially from the value of the relevant underlying index." Although DRNs are redeemable on a daily basis, the absence of a real-time public trading price and a published intraday indicative value would likely make it difficult for a DRN issuer to make any representations about the DRNs' secondary market price as compared to the value of the relevant underlying index. This limitation may be exacerbated by a lack of a secondary market, as opposed to a listed security, such as an ETN.

Consequently, DRN issuers must look elsewhere for relief from Regulation M for issuer redemptions and any potential market making activities by their affiliated broker-dealers. How do they do this?

DRN issuers state in their prospectus supplements or other offering document that their broker-dealer affiliates will not make a secondary market in the DRNs. That leaves issuer redemptions in need of an exemption. The most likely exemption that a DRN issuer would rely upon for issuer redemptions during the applicable restricted period is the exemption under Regulation M for offerings of investment grade nonconvertible securities. Rule 102(d)(2) of Regulation M requires that securities be rated investment grade by at least one nationally recognized statistical rating organization. Market practice has been that, and practitioners read, this requirement to be broad enough to encompass securities, such as DRNs, that are of the same class and ranking as investment grade rated debt securities of the same issuer.

What if a bank were to list a DRN on a national securities exchange in compliance with Section 12(i) of the Exchange Act?3 Could it then rely on the iPath Letter enabling it to make a market in the DRNs and redeem the DRNs, even if the issuer did not have other pari passu investment grade rated debt securities? Likely not. The iPath Letter, arguably, assumes a Form S-3 or Form F-3 issuer filing reports under the Exchange Act. Although a theoretical Section 3(a)(2) DRN issuer using Section 12(i) of the Exchange Act to list a class of its securities on a national securities exchange would file reports with its principal bank regulator substantially in the form required if the issuer were to be subject to the Exchange Act reporting requirements, it may be too big a leap to assume that the iPath Letter would apply to such an issuer without confirmation from the Staff of the Division of Trading and Markets.

CONCLUSION

DRNs may be attractive to some issuers due to, among other things, the potential to harvest fees. DRNs may also be attractive to some investors due to the potential to redeem the DRNs when the underlying reference asset is higher than when they purchased the DRNs. Both sides should be aware that they cannot replicate the characteristics and advantages of ETNs in a DRN wrapper.

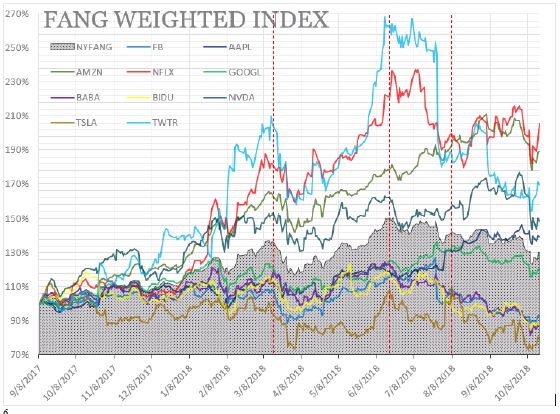

The FANG Index and its Significant Constituents

The NYSE® FANG+" Index (Ticker: NYFANG) ("Index") is an equal-dollar weighted index designed to represent a segment of the technology and consumer discretionary sectors consisting of actively traded growth stocks of technology and tech-enabled companies.4 ICE Data Indices, LLC is its Index sponsor, administrator and calculation agent. On September 26, 2017, the Index was launched with only 10 underlying stocks, comprising the minimum number of index constituents.5 The Index constituents are the common stocks of Apple Inc. (Ticker: AAPL), Amazon.Com, Inc. (Ticker: AMZN), Alibaba Group Holding Limited (Ticker: BABA), Baidu, Inc. (Ticker: BIDU), Facebook, Inc. (Ticker: FB), Alphabet Inc. (Ticker: GOOGL), Netflix, Inc. (Ticker: NFLX), Nvidia Corporation (Ticker: NVDA), Tesla, Inc. (Ticker: TSLA), and Twitter, Inc. (Ticker: TWTR).

From the time the Index was launched until today, the Index has had the same constituents with equal weightings. Each Index constituent represents 10 percent of the weight of the Index, and any reduction in the market price of any constituent will likely affect the value of the Index negatively and substantially. Since there are only 10 constituents, the Index may not necessarily reflect the actual price movements of the entire technology and consumer discretionary industries. Negative changes in a constituent's performance may be magnified and may materially affect the value of the Index, even if common stock prices of other companies in the same industry increase in value.

This graph shows the historical performances of the Index and its constituents and underscores, by way of example, three recent milestones where the volatility of each of, or of some of, the constituents had a material effect on the Index.

- On March 19, 2018, Facebook's stock fell to $172.69, 6.77% down from its previous close of $185.09, while Nasdaq Tech 100 went down by 1.93% at closing. The Index experienced a 2.9% drop in price at closing, a disproportionate drop compared to the overall technology sector.6

- On June 19, 2018, the United States threatened to impose tariffs on $200 billion worth of Chinese goods. China's Commerce Ministry warned that it would retaliate, leading the United States to threaten tariffs against another $450 billion worth of Chinese goods. Trade wars are generally a negative for the short term outlook of stocks across the board, so it was no surprise that the technology sector fell overall (the NASDAQ Tech 100 fell by 0.82%). Two Index constituents are Chinese companies and therefore were particularly affected. BABA was down 1.98%, while BIDU was down by 2.52%, causing the Index to fall 1.17%.7 Because Chinese companies are over-represented in the Index relative to the overall U.S. technology sector, the Index may have experience a stronger negative response to rising trade tensions.

- On August 7, 2018, TSLA closed at a 10.99% increase compared to its closing price on the previous day (i.e., $379.57 versus $341.99 the previous day). While there was no significant movement in the technology industry, the Index went up by 1.05%, driven by the increase in TSLA stock price.8

Because the Index places such a heavy weight on each constituent, short-term changes in the Index may sometimes be largely attributable to events affecting a single company or group of companies rather than the industry as a whole.

FINRA's 2018 Report on Examination Findings and Structured Products

Financial Industry Regulatory Authority, Inc. ("FINRA") recently released its annual report highlighting key observations from its recent examinations. This year's report included several observations of particular relevance to the structured products industry, including:

SUITABILITY

FINRA observed failures among member firms in discharging their suitability obligation. For example, FINRA noted instances in which registered representatives failed to consider adequately the customer's financial situation and needs, investment experience, risk tolerance, time horizon and other factors when making their recommendations. In other cases, FINRA noted that some registered representatives failed to take into account when making their recommendations the cumulative fess, sales charges or commissions. A number of the problematic practices related to recommendations of complex products. FINRA also pointed to concerns regarding overconcentration of illiquid securities in customer accounts, including overconcentration of structured products. Specifically, the report notes that some recommendations involving illiquid securities with limited price transparency were made without customers fully understanding that their investments would fluctuate in value. FINRA noted that registered representations must fully understand specific features and terms of products recommended to clients. The report also cites challenges with supervisory systems and operational issues encountered that impaired the member firms from discharging their quantitative suitability obligation. The report notes that some firms developed parameters for trading volume and cost to identify and prevent excessive trading, and imposed restrictions on frequency or patterns of clustered or single product exchanges. On quantitative suitability, FINRA further noted that some member firms maintained inadequate written supervisory procedures that identified indicators of excessive trading but failed to establish related specific threshold values or parameters.

VOLATILITY-LINKED PRODUCTS

During its recent sweep of volatility-linked products, FINRA observed unsuitable recommendations, inadequate due diligence and insufficient systems and controls. FINRA specifically notes inappropriate marketing to retail customers and recommendations that were inconsistent with customers' risk tolerances and investment time horizons, despite explicit warnings in the related prospectuses. In addition, FINRA noted a lack of sufficient due diligence in light of the heightened risks posed by volatility-linked products, particularly with respect to the potential for accelerated losses. FINRA noted, seemingly as a good practice, that some firms had controls in place that enforced net worth conditions or other pre-qualification criteria for recommendations of such products, and required written certifications attesting to the customers' product knowledge prior to allocating such products. FINRA also noted instances in which firms failed to recognize under their new product approval processes when a new product on the platform was a volatility-linked product.

MARK-UP DISCLOSURES ON CONFIRMATIONS

In connection with revised FINRA Rule 2232 (Customer Confirmations) relating to disclosure of mark-ups, FINRA observed compliance failures related to structured notes where firms were unaware that the structured notes were subject to FINRA Rule 2232 and where distributors failed to provide required information to clearing firms.

FINRA's 2018 report on examination findings reflects its ongoing focus on suitability in connection with

structured notes and complex products. The full report is available here.

Footnotes

1 Recommendation of the Investor as Purchaser Subcommittee Regarding Proposed Regulation Best Interest, Form CRS, and Investment Advisers Act Fiduciary Guidance, available at https://goo.gl/2JVZT4.

2 Id.

3 Several banks have a class of securities listed on the NYSE or the Nasdaq in reliance on this exemption and are not subject to the Exchange Act's reporting requirements.

4 Index Methodology ("Methodology"), at 2, available at https://goo.gl/HPYmgq.

5 Id.

6 See https://goo.gl/a9HX63.

7 The Dow Erases its 2018 gains as Trump moves Closer to All Out Trade War can be found at https://goo.gl/w9i8VK.

8 See https://goo.gl/Z3r6U8.

Originally published in REVERSEinquiries: Volume 1, Issue

8.

Visit us at mayerbrown.com

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2018. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.