Introduction

On 22 August 2018, the European Securities and Markets Authority ("ESMA") published its Final Report on the technical standards on disclosure requirements under the EU Securitisation Regulation1 (the "Final Report")2. This annexed final draft technical standards on the disclosure requirements under the Securitisation Regulation (the "draft Disclosure Technical Standards") (consisting of draft Disclosure RTS3 and draft Disclosure ITS4).

The December 2017 Consultation

The draft Disclosure Technical Standards follow on from ESMA's consultation paper dated 19 December 2017 and the draft technical standards annexed to that consultation (the "December Consultation Paper"). They incorporate comments made in feedback to the December Consultation Paper and arising from a public hearing on the proposed technical standards in February 2018.

ESMA has noted that the second part of its December Consultation Paper, relating to operational standards and access conditions for information made available to securitisation repositories, will now be included in a second batch of documents that will deal with ESMA's mandates regarding securitisation repositories.

Legislative Background

The Securitisation Regulation was published in the Official Journal of the European Union on 28 December 2017 and entered into force on 17 January 2018. The Securitisation Regulation will be directly applicable law across the EU and will apply to securitisations, the securities of which are issued (or where no securities are issued, the securitisation positions of which are created), from 1 January 2019. We commented on the obligations that will arise under the Securitisation Regulation in our Clients and Friends Memorandum dated 26 October 20175.

Other Technical Standards prepared under the Securitisation Regulation

ESMA's draft Disclosure Technical Standards are part of the various technical standards prepared by ESMA and the European Banking Authority ("EBA") pursuant to mandates contained in the Securitisation Regulation. We commented on the draft Regulatory Technical Standards ("RTS") published by the EBA in respect of the Securitisation Regulation's risk retention requirements in our Clients and Friends Memoranda dated 21 December 20176 and 31 July 2018.

Transparency Obligations in the Securitisation Regulation

Transparency Obligations in the Securitisation Regulation – reporting entity

Article 7 of the Securitisation Regulation contains the transparency requirements and directs the originator, sponsor and Securitisation Special Purpose Entity ("SSPE") (i.e. the special purpose vehicle) of a securitisation to make certain prescribed information relating to the securitisation available to investors, national regulators and, upon request, to potential investors. These entities must designate one of them to fulfil the disclosure requirements (the "reporting entity").

Transparency Obligations in the Securitisation Regulation – Information to be Provided Before Pricing

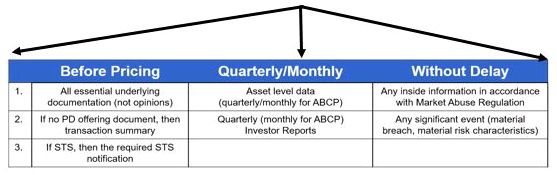

Under Article 7 the information to be made available includes: (i) documentation disclosure (i.e. prescribed transaction documentation); (ii) a transaction summary for "private securitisations"7 (please see below); and (iii) in the case of STS8 securitisations, the STS notification.

This information is to be made available before pricing9. The timing of the transaction documentation disclosure obligation will potentially be problematic given that documents are typically still in draft form, and often incomplete, at the time of pricing. Furthermore, Article 22(5) of the Securitisation Regulation, which relates to STS securitisations only, requires the information to be made "available before pricing at least in draft or initial form". There does not seem to a clear basis for this apparently less onerous obligation for STS securitisations. In its Final Report, ESMA acknowledges this issue and has said that, although it falls outside ESMA's technical mandates, it has ensured that this issue has been passed on to the responsible legislative bodies.

Transparency Obligations in the Securitisation Regulation – Ongoing Reporting Obligations

The ongoing reporting obligations include: (i) quarterly10 asset level disclosure (i.e. information on the underlying exposures) (the "Underlying Exposures") (ii) quarterly11 investor reports containing prescribed information ("Investor Reports"); (iii) any inside information relating to the securitisation that the reporting entity12 is obliged to make public under the Market Abuse Regulation13 ("Inside Information"); and (iv) even where it is not inside information, any material breach of the obligations laid down in the documents, any material change in the structural features or risk characteristic of the securitisation, or any material amendment to transaction documents ("Significant Events").

The quarterly Investor Reports must contain: (i) all materially relevant data on the credit quality and performance of underlying exposures; (ii) information on events which trigger changes in the priority of payments or the replacement of any counterparties, and data on the cash flows generated by the underlying exposures and by the liabilities of the securitisation14; and (iii) risk retention compliance information.

The information on Underlying Exposures and in the Investor Reports is to be made available simultaneously each quarter at the latest one month after the due date for the payment of interest15.

The annex to this memorandum summarises these reporting obligations in diagrammatic form.

Transparency Obligations – Securitisation Repositories

Securitisation repositories are to be established to which prescribed information relating to the securitisation is to be provided by the reporting entity. Those repositories, which are to be registered with ESMA, will collect details of the securitisation and will provide direct and immediate access free of charge to the EU supervisory authorities, to investors and to potential investors. Where no securitisation repository is registered, the reporting entity shall make the information available by means of a website that meets certain prescribed conditions.

Reporting Obligations and Private Securitisations

There is an exemption from reporting to the repository (but not from the rest of the reporting requirements) for "private securitisations" (i.e., those where a Prospectus Directive compliant prospectus has not been drawn up). Recital 13 to the Securitisation Regulation, explains that, in light of the possibility for sensitive commercial information being present in the transaction, private securitisations should be exempted from the requirement to notify information to a securitisation repository. A Prospectus Directive compliant prospectus does not have to be drawn up for admission to trading on markets such as the Irish Global Exchange Market.

In its Final Report ESMA said that it had conducted additional legal analysis and that its interpretation of the Securitisation Regulation was that the technical standards covering the Underlying Exposures and Investor Reports "appear to apply" to all securitisations (i.e. both public and private securitisations). At the same time, ESMA understands that its Article 17 mandates (see below) appear to apply only to public securitisations (which are required to report information to a securitisation repository).

The Draft Disclosure Technical Standards

Legislative Basis of the Disclosure Technical Standards

Article 7(3) of the Securitisation Regulation directs ESMA to develop draft RTS and Implementing Technical Standards ("ITS")16 to specify the information that the reporting entity shall provide in order to comply with their reporting obligations.

In addition, Article 17 mandates ESMA to draft technical standards specifying the information and standardised templates that should be provided by the reporting entity to comply with the information requirements of Article 7.

The Securitisation Regulation directed ESMA to submit these draft Disclosure Technical Standards to the European Commission by 18 January 2019. The finalised technical standards are then to be adopted by the Commission by way of a delegated regulation. However, ESMA has recognised that the technical standards need to be adopted by the Commission prior to the date of application of the Securitisation Regulation on 1 January 2019 and has brought this to the Commission's attention (see also below)17.

Securitisations subject to the Disclosure Technical Standards

In its December 2017 Consultation Paper, ESMA identified three categories of transactions: (a) securitisations with any securities issued from 1 January 2019 onwards ("new securitisations"); (b) securitisations with all securities issued on or before 31 December 2018, that seek to obtain STS status ("legacy STS securitisations'); and (c) securitisations with all securities issued on or before 31 December 2018, that do not seek to obtain STS status ('legacy non-STS securitisations'). New securitisations and legacy STS securitisations must comply with the Disclosure Technical Standards18. However, in its December 2017 Consultation Paper, ESMA notes that legacy non-STS securitisations "appear" to be exempt from disclosure requirements19.

Concerns Raised in Feedback to the December Consultation Paper

ESMA has highlighted some of the concerns raised in responses to the December Consultation Paper. Respondents raised the jurisdiction issue (discussed below) and the requirement to provide documentation prior to pricing (discussed above). ESMA has made clear that both of these issues are outside the scope of its mandate in preparing the draft Disclosure Technical Standards.

Other points raised in the feedback to the December Consultation Paper related to: (i) the suitability of the templates to non-bank/non-original lender originators; (ii) the potential impact of the transitional provisions; (iii) the need for templates appropriate for CLOs; and (iv) the "no data" options. These points are discussed below.

ESMA's Draft Disclosure Technical Standards and the Templates

ESMA's Draft Disclosure Technical Standards consist mainly of extensive reporting templates reflecting the categories of information in the Securitisation Regulations ongoing reporting obligations. There are therefore templates for: (a) Underlying Exposures; (b) Investor Reports; (c) Inside Information; and (d) Significant Events.

ESMA's Draft Templates for Underlying Exposures

Of these templates, those for Underlying Exposures20 are likely to have the most significant impact for market participants.

The templates are based on previous work in this area. In 2014 ESMA prepared draft RTS (subsequently adopted) containing loan-level requirements for specified ABS21 pursuant to the CRA3 Regulation22. The European Central Bank ("ECB") has also already prepared templates as part of it ABS loan-level initiative23. These existing ECB templates were used as a starting point for ESMA's templates.

The Underlying Exposures templates distinguish between ABCP and non-ABCP securitisations. For the latter, ESMA's Underlying Exposure templates cover the following underlying exposure types: (a) residential mortgages; (b) commercial real estate; (c) corporate exposures (including loans to SMEs as well as large corporates); (d) auto loans/leases; (e) consumer loans; (f) credit card receivables; and (g) leasing. ESMA has developed a further template for "esoteric" underlying exposures that do not fall within any of these categories. ESMA has also developed an additional add-on template for non-performing exposure ("NPE") securitisations. Another template exists for ABCP securitisations.

Reporting for CLOs

Many respondents to the December Consultation Paper proposed that a separate reporting template be prepared for CLOs24, or that the Corporate Underlying Exposures template be modified so as to make it appropriate for CLOs. It was pointed out that the templates should be appropriate for non-bank originators, as well as for bank originators, and that the templates should be suitable for reporting entities who are not original lenders (please see below). ESMA has taken this feedback on board and has taken the view that the Corporate Underlying Exposures template should be adapted for CLOs.

ESMA commented on respondents' concerns that some information would not be available to CLO managers, as it would only be held by the original lender such as the jurisdiction of the originator/original lender, origination channel of a loan, its origination date, and its original principal balance. ESMA is of the view that such information25 is important for potential investors to perform their due diligence, as well as for investors and public authorities to meet their monitoring tasks and, therefore, should always be available. ESMA said that "although such information may be challenging to retrieve at first, then by the time that the reporting requirements fully apply, it appears that this information would be able to be made available in a sufficiently broad manner".

In its Final Report, ESMA explained that it had set out the following arrangements in its draft Disclosure Technical Standards regarding CLO securitisations:

(a) CLO securitisations should complete the applicable Underlying Exposure template for each underlying exposure in the pool (this would normally be the Corporate Underlying Exposures template);

(b) CLO securitisations should also complete an additional securitisation information section, which contains fields of particular relevance for due diligence and monitoring of CLO securitisations. These include information on the type of CLO, on the current stage of the CLO securitisation (e.g. warehousing, ramp-up, reinvestment, post-reinvestment/wind-down), as well as numerous fields to capture in a standardised manner key possible restrictions on the CLO manager's actions.

(c) CLO securitisations should also complete an additional CLO manager information template, for each CLO manager, including information on the size of the CLO manager in terms of assets under management, capital, employees, as well as its operational arrangements (e.g. pricing frequency and time needed for settlement) and the performance of its CLO securitisation-related investments in recent years.

There is not a separate template for CLOs, but the draft template for Significant Events annexed to the draft Disclosure Technical Standards contains a "CLO Securitisation information section" and a "CLO Manager information section".

ESMA's Draft Templates for Investor Reports

Separate Investor Report templates have been created for ABCP and for non-ABCP securitisations.

ESMA's Draft Templates for Inside Information and Significant Events

As part of the information to be made available for all "public securitisations" (as opposed to that for "all securitisations") under the draft Disclosure RTS, reference is made to templates for the Inside Information that the reporting entity has made public and for the information on Significant Events that the reporting entity is to make available under the Securitisation Regulation26. It therefore appears that these reporting templates do not apply to private securitisations. For the Significant Event templates, ESMA has stated that it has placed particular emphasis on the need to report further details regarding a change in the structural features of the securitisation, or a change in its risk characteristics or its underlying exposures.

Concerns Raised in Feedback Regarding Non-Bank/Non-Original Lender Originators

An important concern raised by respondents to the Consultation was that many of the data fields in the templates annexed to the December Consultation Paper were written in terms that assumed that the originator is a bank. This will not always be the case. Originators may also be entities that have purchased loans on the secondary market and have then securitised them (known as "limb (b) originators" in the context of the risk retention obligation). It was pointed out that compliance with the reporting obligations in the templates should be practicable for reporting entities who are not original lenders and that the templates should be designed so that all types of originator can comply, and not solely bank originators.

ESMA's response in its Final Report noted the need to ensure that the securitisation disclosure requirements sufficiently catered for the features of non-bank originators. ESMA made certain adjustments to take this into account. ESMA also noted its view that securitisation disclosure requirements should preserve a level playing field between non-bank originators (particularly those having purchased loan portfolios from original lenders) and bank originators.

"No Data" Options in the Templates

Several respondents to the December Consultation Paper suggested additional "no data" options for the templates. ESMA rejected these suggestions and confirmed that there are five "no data" options in the templates:

(a) ND1: data not collected as not required by the lending or underwriting criteria;

(b) ND2: data collected on underlying exposure application but not loaded into the originator's reporting system;

(c) ND3: data collected on underlying exposure application but loaded onto a separate system from the originator's reporting system;

(d) ND4: data collected but will only be available from specified date; and

(e) ND5: "not applicable".

ESMA has clarified that the use of the "no data" options should be limited to certain fields in the templates. It has said that the ND1 to ND4 "no data" options should only be used in legitimate cases of information not being available. ESMA has said that the use of these options in reporting underlying exposures information in a securitisation "is expected to be extremely limited" and that under no circumstance should they be used as an exemption from the reporting requirements. "No data" options ND1 to ND4 could potentially be used in certain fields in the Underlying Exposure templates, but not in the remaining templates (i.e., the Investor Reports, Inside Information, and Significant Events templates). ESMA has said that greater flexibility is given on the use of the ND5 "no data" option (i.e. "not applicable") throughout all of the templates27, although there are also specific fields where there appears to be no reasonable case for the required information to be "not applicable".

As regards information not being available because it has been transferred from the original lender to the originator, ESMA considers it important that original lenders make sufficient efforts to collect similar information on loans to avoid risks of circumvention of these reporting requirements via the use of original lenders.

Similarly, ESMA considers that allowing loans originated prior to the entry into force of the Disclosure Technical Standards to avoid reporting certain fields would also not be sufficient to capture the requirements in the Securitisation Regulation. As regards "new securitisations"28, ESMA considers that the draft Disclosure Technical Standards are being published with a sufficient lead time to allow originating banks to begin collecting the necessary information with a view to issuing securitisation transactions from 1 January 2019 and that, consequently, the case for a "no data" option in this situation is not strong.

Transitional Issues

Concerns on the Securitisation Regulation's Transitional Provisions

The Final Report said that respondents had highlighted that the draft Disclosure Technical Standards need to be adopted prior to the 1 January 2019 application date of the Securitisation Regulation so as to reduce the possibility of the Securitisation Regulation's transitional provisions29 applying, which would result in market participants having to implement two sets of templates: i.e., those under the Disclosure Technical Standards and those under Article 8b of the CRA3 Regulation. As noted above, ESMA has already alerted the Commission to this issue.

ESMA's Proposed Transitional Period for Implementation

ESMA has noted that respondents have emphasised the need for sufficient time to adapt to the proposed reporting requirements. ESMA has said that it does not have a legal mandate to propose a transitional period for the implementation of the Disclosure Technical Standards. However, ESMA understands that compliance with the Disclosure Technical Standards may require substantial time and effort. Although ESMA makes clear that is a matter for the Commission, it proposes a transition period for the implementation of the Disclosure Technical Standards so that they could apply in a gradually increasing manner. ESMA considers that 15-18 months appear to be necessary as a transition period. This is a welcome proposal for market participants who would otherwise have very little time to develop the reporting systems necessary to comply with these requirements. We will need to see if the Commission acts on ESMA's proposal.

The Jurisdictional Scope of the Transparency Obligations

The Jurisdictional Scope of the Obligations in the Securitisation Regulation

The transparency obligations are not expressly stated to be restricted to EU-established originators, sponsors and SSPEs and so appear to have a potential extra-territorial effect (in that they could apply to non-EU established originators, sponsors and SSPEs). Furthermore, these obligations may apply on a consolidated basis to non-EU subsidiaries as a result of the consolidation provisions in the Capital Requirements Regulation30 ("CRR") (please see below).

There is an argument that Article (5)(1)(e) of the Securitisation Regulation, which requires investors to verify compliance with the transparency obligations, does not apply where there is no EU originator, sponsor, original lender or SSPE ("non-EU Securitisation") because arguably such originator, sponsor, original lender and SSPE do not have an obligation to provide such information pursuant to Article 7 of the Securitisation Regulation. However, even if the market view is that Article 5(1)(e) of the Securitisation Regulation does not apply to an EU institutional investor investing in a non-EU securitisation, EU institutional investors are still required to carry out a due diligence assessment under Article 5(3) of the Securitisation Regulation and to satisfy their continuing obligations under Article 5(4) of Securitisation Regulation. The receipt of information corresponding to that to be provided under Article 7 of the Securitisation Regulation is something that an EU institutional investor may look for in that regard. Effectively, the increased reporting required by Article 7 of the Securitisation Regulation in respect of EU securitisations will likely increase the level of information that EU institutional investors need to consider prior to investing in a non-EU securitisation.

Jurisdictional Consequences of the Consolidated Application of the CRR

We mentioned in our Clients and Friends Memoranda dated 26 October 2017 and 31 July 2018 that an issue that has caused widespread concern in the industry is the extent of the applicability of certain obligations (including the transparency requirements) in the Securitisation Regulation as a result of changes to the CRR. Article 14 of the CRR as amended by Article 1(11) of the CRR Amendment Regulation31 applies the transparency requirements (as well as the risk retention, due diligence, the "criteria for credit-granting" obligations, and the ban on re-securitisation) under the Securitisation Regulation to EU institutions subject to the CRR, on a consolidated basis. As a result of this amendment to Article 14 of the CRR, the transparency requirements could therefore apply on a consolidated basis to a non-EU subsidiary of an EU bank. Such a subsidiary would have to comply both with the EU transparency requirements and with any locally applicable rules. Those requirements could have significant implications for EU banks operating in third countries through subsidiaries.

It appears that the application of such requirements to non-EU subsidiaries of EU banks was an unforeseen consequence of the changes to the CRR. It looks likely that further amendments will be made to the CRR, the effect of which would be that Article 14 of the CRR would only apply the Securitisation Regulation's due diligence requirements (and not its transparency requirements or other obligations) on a consolidated basis. However, these further changes to Article 14 of the CRR would be made as part of the overall package to amend the CRR known as "CRR II", and it is currently not clear that these further amendments would apply from the application date of the Securitisation Regulation, 1 January 2019.

ESMA's Comments on the Jurisdictional Issues in its Final Report

In its Final Report, ESMA referred to these jurisdictional points having been raised in the feedback to its December Consultation Paper. ESMA is aware of the issues concerning the geographical scope of the disclosure requirements, where the originator, sponsor, and/or original lender32 is located outside of the EU and the application of disclosure requirements to consolidated entities outside of the EU as a result of the amendments to Article 14 of the CRR. ESMA has said that, although these points fall outside its technical mandates, it has ensured that these issues have been passed on to the responsible legislative bodies.

Next Steps and Conclusion

The draft Disclosure Technical Standards will now be submitted to the Commission, who will adopt the Disclosure Technical Standards by way of delegated EU legislation.

ESMA has listened to the concerns of market participants as regards the contents of the draft Disclosure Technical Standards. Nevertheless, the practical difficulties of complying with these new reporting obligations are likely to be significant and the relevant reporting entities will have to start preparing both their back-office function and their advisors to address those reporting changes. Some market participants have questioned whether the benefits to be gained from the collection of this vast amount of data (a net increase of 516 reporting fields compared with current ECB templates33) will justify the resulting compliance costs and will indeed be used by investors.

As noted above, ESMA has highlighted the need for the technical standards to be adopted by the Commission as soon as possible, in view of the transitional provisions of the Securitisation Regulation, to avoid market participants having to implement two sets of templates34. ESMA has also proposed a 15-18 month transition period for implementation. It is to be hoped that the Commission will follow ESMA's advice on these points.

Cadwalader has assisted the Loan Market Association in engaging with ESMA as regards issues arising from the December draft of the Disclosure Technical Standards and will continue to engage with ESMA and the EU legislative institutions as regards concerns with the Securitisation Regulation's transparency regime.

ANNEX

SUMMARY OF SECURITISATION REGULATION DISCLOSURE REQUIREMENTS

The originator, sponsor and SSPE of a securitisation are required to make the following disclosures to holders of a securitisation position, competent authorities and, upon request, to potential investors.

Originator, sponsor and SSPE are to designate one of them to fulfil the disclosure requirements.

Disclosure obligations are satisfied by submitting information to a registered "securitisation repository" the identity of which must be disclosed in the securitisation documentation (save for "private securitisations" i.e. where no Prospectus Directive compliant prospectus is required).

Disclosure obligations are to comply with national and EU law governing the protection of confidentiality (but competent authorities may request such information). Obligations also take account of contractual confidentiality requirements.

ESMA has developed draft technical standards for asset level disclosure, quarterly/monthly reporting, inside information and significant events.

Footnotes

1 Regulation (EU) 2017/2402 of the European Parliament and of the Council of 12 December 2017 laying down a general framework for securitisation and creating a specific framework for simple, transparent and standardised securitisation, and amending Directives 2009/65/EC, 2009/138/EC and 2011/61/EU and Regulations (EC) No 1060/2009 and (EU) No 648/2012.

3 Draft regulatory technical standards specifying the information and the details of a securitisation to be made available by the originator, sponsor and SSPE.

4 Draft implementing technical standards with regard to the format and standardised templates for making available information and details of a securitisation by the originator, sponsor and SSPE.

5 https://www.cadwalader.com/uploads/cfmemos/38ea3c254ddf2413acc355485d187ead.pdf

6 https://www.cadwalader.com/uploads/cfmemos/6611b2cb78b3f7d724fe820e5dd7acfc.pdf

7 Also known as "private transactions"

8 "Simple, transparent and standardised"

9 Although please see below for STS securitisations

10 Monthly for asset-backed commercial paper (ABCP).

11 Monthly for ABCP

12 The originator, sponsor or SSPE.

13 Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC.

14 For non-ABCP securitisations.

15 In the case of ABCP transactions, at the latest one month after the end of the period the report covers.

16 The RTS supplement the Securitisation Regulation, while ITS specify how the details are to be implemented (eg through standard templates).

17 In the letter from Steven Maijoor of ESMA to the Commission dated 24 April 2018.

18 Article 43 of the Securitisation Regulation

19 ESMA explains that this is because the Securitisation Regulation stipulates that, until the Commission adopts ESMA's draft RTS on disclosure, the reporting templates set out in the RTS adopted as per Article 8b of the CRA3 Regulation (Regulation (EU) No 462/2013) will apply. At the same time, the Securitisation Regulation states elsewhere that Article 8b of the CRA3 Regulation is "deleted".

20 As noted in the Recitals to the draft Disclosure RTS, the term "underlying exposure" is generally understood to refer to any loan, lease, debt, credit, or other cash-flow generating receivable.

21 Asset-Backed Securities

22 Regulation (EU) No 462/2013 of the European Parliament and of the Council of 21 May 2013 amending Regulation (EC) No 1060/2009 on credit rating agencies

23 The ECB ABS loan-level initiative established loan-by-loan information requirements for ABS accepted as collateral in Eurosystem credit operations.

24 Collateralised Loan Obligations

25 Such as the jurisdiction of the originator/original lender, origination channel of a loan, its origination date, and its original principal balance

26 There are separate templates for ABCP and non-ABCP securitisations

27 ESMA has said that it considers that the ND5 'No data' option (i.e. 'not applicable') appears to remain valid and necessary to allow in fields in each of the templates, given the heterogeneity of securitisations, the variety of various underlying exposure products that may still be classified under the same type (e.g. 'residential mortgages') and also the prevalence of different originator and jurisdictional practices.

28 Securitisations the securities of which are issued on or after 1 January 2019 – please see above.

29 Article 43(8) of the Securitisation Regulation

30 Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012.

31 Regulation (EU) 2017/2401 of the European Parliament and of the Council of 12 December 2017 amending Regulation (EU) No 575/2013 on prudential requirements for credit institutions and investment firms.

32 "Original lender" inadvertently omitted from the Final Report

33 An extra 959 mandatory fields being offset by a reduction of 443 unnecessary optional fields.

34 i.e. both the present technical standards as well as the templates developed under Article 8b of the CRA3 Regulation.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.