As you probably are well-aware by now, the U.S. Congress recently passed H.R. 1 (commonly referred to as the Tax Cuts and Jobs Act of 2017) (the "Act"), and the President signed the Act on December 22, 2017. The Act embodies the most significant and sweeping changes in U.S. tax law since 1986. For individual taxpayers, the Act dramatically alters the tax landscape through 2025, establishing new income tax rates and brackets, increasing the standard deduction, eliminating personal exemption deductions, limiting application of the alternative minimum tax, limiting state and local tax deductions, changing the way inflation adjustments are calculated, reducing the impact of estate, gift and generation-skipping transfer taxes, providing a new deduction for non-corporate taxpayers having so-called "qualified business income" from pass-through businesses (partnerships, LLCs, S corporations and sole proprietorships) and instituting many other changes. For businesses, the Act implements a wide array of changes, including a permanent reduction of the top corporate tax rate to 21%, repeal of the corporate alternative minimum tax, new limits on business interest deductions and new rules for expensing and depreciation. The Act also significantly modifies a number of tax rules applicable to foreign income and taxpayers (including the exemption from U.S. tax for certain foreign income and the deemed repatriation of foreign income), tax-exempt organizations, executive compensation, retirement plans, payments for education, insurance companies and energy, rehabilitation and other credits.

This Client Alert summarizes those key provisions of the Act affecting individuals and businesses which we believe may be of particular relevance to many of our clients.

Tax Changes Affecting Individuals

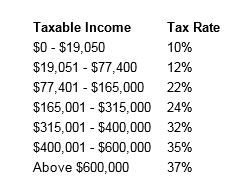

- Tax Rates. The Act

retains a seven tax bracket structure, but with slightly lower

marginal rates on slightly wider brackets. The 37% top marginal

rate is lower than the pre-Act top marginal rate of 39.6% and

applies to income over $600,000 for married taxpayers filing

jointly, as opposed to the $470,700 pre-Act threshold. Similar

changes have been made to the tax rate bracket structures

applicable to married taxpayers filing separately, heads of

households and single individuals. These reduced rates, like most

of the Act's provisions affecting individuals, will sunset

after 2025. Notably, the Act retains the maximum 20% tax rate

applicable to net capital gains and qualified dividends, as well as

the additional 3.8% tax on net investment income applicable to

certain high-income taxpayers. Married couples filing jointly are

subject to the following new tax rates:

- Standard Deduction and Personal Exemptions. The standard deduction is doubled, such that the first $12,000 of income for an individual is tax-free ($24,000 for married couples), but the deduction for personal exemptions is eliminated.

- Itemized Deductions. The limitation on total itemized deductions for high-income taxpayers (known as the "Pease" limitation) is repealed, and all "miscellaneous itemized deductions" (formerly deductible to the extent they exceeded 2% of adjusted gross income) are eliminated.

- Deduction of State and Local Taxes. Through 2025,an individual generally will be allowed to claim an itemized deduction of no more than $10,000 ($5,000 if married and filing a separate return) for the aggregate of (i) state and local property taxes not paid or accrued in carrying on a trade or business (or in an income-producing activity), and (ii) state and local income (or sales taxes) paid or accrued in any tax year. Foreign real property taxes will be deductible only when paid or accrued in carrying on a trade or business (or for the production of income).

- Mortgage Interest Deduction. The mortgage interest deduction for existing mortgages (and refinancings of existing mortgages) is preserved, but interest is deductible on mortgages with respect to homes purchased after December 15, 2017 only to the extent such mortgages do not exceed $750,000 (reduced from the pre-Act limit of $1,000,000). The Act also eliminates deductions for interest on home equity indebtedness after December 31, 2017.

- Excess Business Losses Disallowed. The Act contains a significant change in the tax treatment of a non-corporate taxpayer's losses incurred in a non-passive activity (i.e., one in which the taxpayer "materially participates" within the meaning of IRS rules). Under the Act, such taxpayer's "excess business loss" (more than $500,000 for married individuals filing jointly or $250,000 for other individuals) for any tax year would not be deductible. Such "excess business loss" must be treated as a net operating loss ("NOL") and carried forward to subsequent tax years, with such NOL carry forwards being deductible in such subsequent tax years to the extent of 90% of taxable income (determined without regard to the NOL deduction) in such subsequent tax years.

- Modified Alternative Minimum Tax. The Act retains the individual alternative minimum tax ("AMT"), although with increased exemption amounts. For taxable years 2018 through 2025, the AMT exemption amount is increased to $109,400 for married taxpayers filing a joint return and $73,000 for all other individual taxpayers. The phase-out thresholds are increased to $1,000,000 for married taxpayers filing a joint return and $500,000 for all other individual taxpayers.With the limitations on the deductibility of state and local taxes, the individual AMT is expected to apply to fewer taxpayers.

- Estate, Gift, and Generation-Skipping Transfer Taxes. The Act doubles the estate, gift, and generation-skipping transfer tax exemption amount to roughly $11.2 million per person (or $22.4 million for a married couple) in 2018, adjusted annually for inflation. Please refer to our firm's separate Client Alert for a more detailed explanation of these changes.

- Alimony. Under pre-Act law, payments of alimony were deductible to the payor and includible in the income of the recipient. The Act eliminates the deduction for alimony payments and the requirement that such payment be included in the income of recipients. These changes apply only to agreements executed after December 31, 2018.

Tax Changes Affecting Businesses

- Tax Rates. The top corporate tax rate is reduced from 35% to 21%, effective for tax years beginning after December 31, 2017, and with no sunset provision.

- Deduction for"Qualified Business Income" from Pass-Through Businesses. The Act generally allows a non-corporate taxpayer to deduct the lesser of (i) 20% of such taxpayer's share of any domestic "qualified business income" ("QBI") of a pass-thru business (e.g., partnership, LLC, S corporation or sole proprietorship), and (ii) the greater of (a) 50% of such taxpayer's share of the domestic wages paid with respect to the trade or business and (b) such taxpayer's share of the sum of 25% of such wages and 2.5% of the unadjusted basis of all qualified property used in such trade or business. If the full 20% deduction is applicable, the effective marginal tax rate on the taxpayer's QBI (assuming he is subject to the maximum 37% tax rate) is 29.6%. QBI generally is defined as the net amount of income, gain, deduction and loss (with the exception of investment-related income, gain, deduction and loss, other than certain dividends from REITs) with respect to any trade or business other than a "specified service business," which, in turn, is defined as a profession in the field of health, law, accounting, consulting, athletics, financial services, brokerage services or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees or owners, or which involves the performance of services that consist of investing and investmentmanagement and trading, or dealing in securities, partnership interests or commodities. Engineering and architecture are specifically excluded from the definition of a "specified service business." Individuals who derive business income from a "specified service business" are permitted to treat such income as QBI if their taxable income is less than $315,000 (for married taxpayers filing a joint return) or $157,500 (for individuals). If such an individual's income exceeds the applicable threshold amount, the benefit of the deduction is phased out over up to $100,000 of such excess (for married individuals filing jointly; $50,000 for other individuals).

- Reduced Dividends-Received Deduction. To preserve the effective tax rates on dividends received from domestic corporations, a corporation is able to deduct only 65% (down from 80%) of the amount of such dividends, if the receiving corporation owns 20% or more of the stock of the dividend-paying corporation, and only 50% (down from 70%) of the amount of such dividends if the receiving corporation owns less than 20% of the stock of the dividend-paying corporation.

- Immediate Expensing of Capital Expenditures. The Act allows temporary 100% expensing for property (other than real estate) acquired and placed in service after September 27, 2017 and before January 1, 2023, with the expensing percentage decreasing by 20% every year thereafter. Property acquired before September 28, 2017, but placed in service after September 28, 2017, will remain subject to pre-Act bonus depreciation rules.

- Interest Deduction Limitation. The deductibility of net business interest is effectively capped at 30% of EBITDA through 2021, and then at 30% of EBIT thereafter. Any disallowed amounts generally may be carried forward indefinitely. There is no grandfathering for preexisting debt.Small businesses ($25 million or less of gross receipts) are exempt from this limitation, and real estate businesses can elect out of this limitation, but upon such an election, are required to use a slightly less favorable depreciation recovery period.

- Net Operating Losses. NOLs arising in tax years beginning after December 31, 2017 are deductible only up to 80% of taxable income and can be carried forward indefinitely, but generally cannot be carried back.

- Elimination of Corporate AMT. The AMT applicable to corporations is eliminated.

- Like-Kind Exchanges. Before the Act, taxpayers were permitted to defer gain upon an exchange of real estate, tangible personal property and certain types of intangible property (other than goodwill) held for productive use in a trade or business or for investment for "like-kind" property that also is held for productive use in a trade or business or for investment. The Act limits nonrecognition treatment to like-kind exchanges of real property (other than real property held primarily for sale), effective for exchanges after December 31, 2017, but grandfathers any deferred exchange of otherwise qualifying property disposed of or received prior to December 31, 2017.

The foregoing is only a summary of certain key provisions of the Act.

This alert provides general coverage of its subject area. We provide it with the understanding that Frankfurt Kurnit Klein & Selz is not engaged herein in rendering legal advice, and shall not be liable for any damages resulting from any error, inaccuracy, or omission. Our attorneys practice law only in jurisdictions in which they are properly authorized to do so. We do not seek to represent clients in other jurisdictions.