The Senate voted yesterday to begin formal negotiations with the House of Representatives to reconcile their two versions of the Tax Cuts and Jobs Act, a bill that seeks to make sweeping changes to federal tax law. Republicans are racing to enact a final bill before Christmas. Under both versions of the bill, tax-exempt organizations would face new burdens and taxes in order to pay for tax cuts elsewhere. In particular, the proposed changes would:

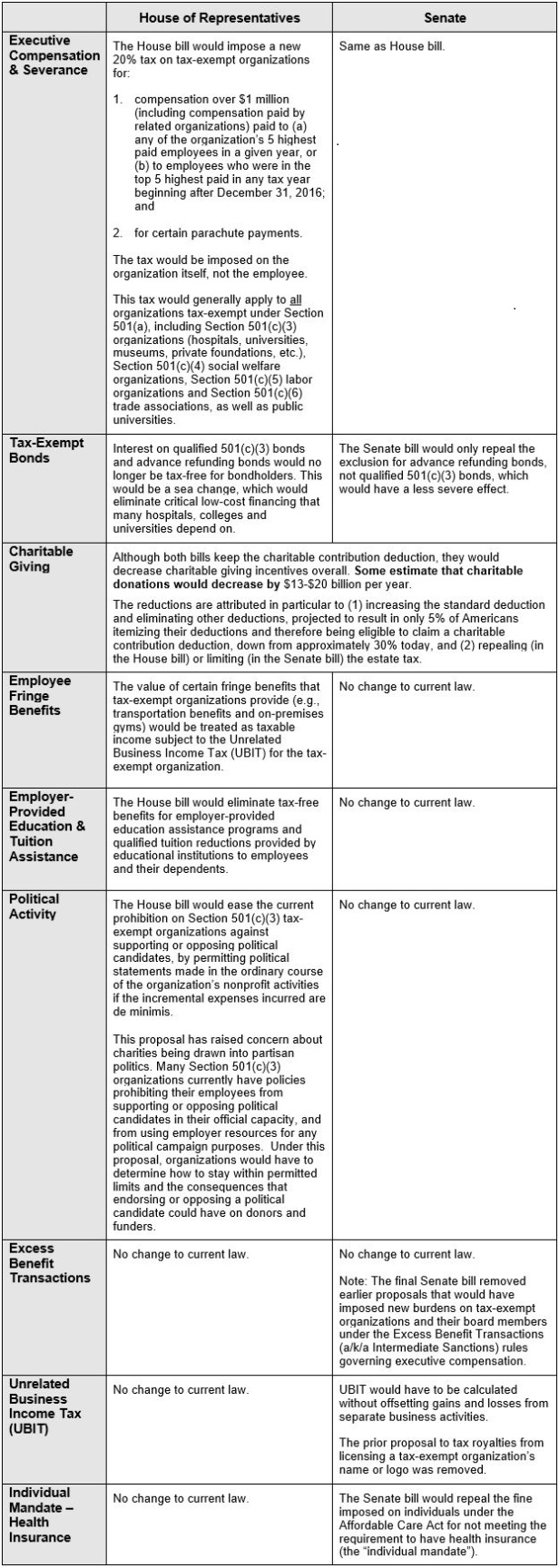

- make it harder for larger tax-exempt organizations to attract and retain top talent, by imposing a new 20% tax on annual compensation of over $1 million per year paid to any of their top 5 highest paid employees (including certain severance payments);

- reduce revenues, by eliminating certain tax incentives to make charitable donations;

- eliminate critical low-cost financing for hospitals and universities from tax-exempt bonds;

- make certain employee benefits more expensive, by taxing organizations that pay certain fringe benefits and taxing employees on certain employer-provided education and tuition assistance; and

- add new pressures on Section 501(c)(3) organizations to support or oppose political candidates, by loosening the current absolute prohibition against political activity.

Current Status. The House passed their version of the Tax Cuts and Jobs Act on November 16, 2017, and the Senate passed a similar bill this past weekend, in the early hours of Saturday, December 2, 2017. There are a few notable differences between the two bills, which are outlined below. The compromise bill would need to be approved by both houses of Congress, but Republicans are pushing hard to enact a final bill before Christmas, and it is widely expected that they will succeed.

What's at Stake?

- For All Tax-Exempt Organizations: The chart below highlights how the House and Senate's bills would impact tax-exempt organizations, with certain key differences between the two bills. Many proposed changes would take effect for tax years beginning in 2018.

- Hospitals and Healthcare Organizations: The financial stresses from tax reform could be particularly acute for hospitals and other healthcare organizations when combining the effects of: (1) decreased revenue from charitable donations; (2) loss of low-cost financing from tax-exempt bonds; (3) increased costs to paying executive and physician compensation that may be necessary to attract and retain top talent; (4) repeal of the "individual mandate" under the Affordable Care Act (which requires most Americans to have health insurance or pay a fine), which would result in more uninsured people unable to pay for healthcare; and (5) mandatory cuts to Medicare and possibly other government programs that could result under pay-as-you-go rules, unless Congress separately acts to prevent such cuts.

- Colleges and Universities: There would be significant impact on colleges and universities under tax reform, including from (1) the loss of low-cost financing from tax-exempt bonds, (2) decreased revenue from charitable donations, (3) increased costs to paying competitive compensation for senior executives and top faculty, (4) eliminating tax-free benefits for employer-provided education assistance programs and qualified tuition reductions provided by educational institutions to employees and their dependents, (5) repealing the personal income tax deductions for interest paid on education loans and for qualified tuition and related expenses, and (6) a new 1.4% tax on net investment income earned by certain larger college and university endowments.

- Private Foundations: The tax on private foundation's net investment income would be streamlined from a two-tier 1% or 2% tax to a flat 1.4% tax.

Comparison of Senate and House Bills:

The Big Picture:

New tax burdens on tax-exempt organizations are among the ways in which the bills would raise revenue to pay for proposed tax cuts for businesses and individuals. Significant concern has been expressed in the nonprofit sector about the anticipated adverse consequences of the proposals, particularly about decreasing charitable giving incentives and politicizing charities and eliminating tax-exempt bonds.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.