The potential for sweeping tax changes is greater now than in decades, but many open questions remain. Businesses and individuals are scrambling to understand when tax reform could be enacted, when it would be made effective, what is actually being proposed, how the proposals are likely to evolve, and what taxpayers can and should do before reform is completed. The following FAQs address these issues and more.

OUTLOOK

1. Is tax reform really happening?

The prospects for major tax reform increased tremendously with the Republican election sweep. There is now a very good chance significant tax legislation will be enacted, but it is not a foregone conclusion. Many obstacles still must be overcome, and many details still need to be worked out. It is possible tax reform will take longer than expected or fail altogether.

2. What are the obstacles for tax reform?

There are a variety of factors that could delay (or even derail) tax reform, or possibly force the current proposals to evolve considerably:

- Obamacare logjam: The top GOP priority is repealing and replacing the Affordable Care Act (ACA). This effort could consume lawmakers and delay tax reform, although tax reform could also leapfrog ACA repeal if ACA repeal stalls.

- Cost: President Donald Trump's campaign platform and the GOP blueprint both appear to lose significant revenue even if scored assuming economic growth and an alternative baseline. Changes to the plans may be needed to cut down on cost.

- Agreement on details: Republicans are in sole control of the legislative process right now, but they are not totally unified over tax reform. It will be both technically and politically difficult to reach a consensus on many issues, and the business community will lobby heavily against certain changes.

- Political backlash: ACA was politically costly for Democrats, and Republicans may risk a similar backlash if they lose the battle for public sentiment on tax reform. The current platforms focus largely on making the United States more competitive for investors and large corporations. Republicans may need to pivot to provide greater focus on the middle-income Americans who turned the election in rust belt states.

- Lack of 60 votes: Republicans' most significant hurdle is their slim 52-seat majority in the Senate. Because the GOP lacks 60 votes, Democrats can use procedural hurdles like filibusters to effectively block almost any legislation. The reconciliation process would allow Republicans to move tax legislation with simple 50-vote majorities, but it comes with limits. Provisions generally may not lose revenue outside of the 10-year budget window, which often requires sunsetting. Republicans may need to alter their current proposals to attract at least eight Democratic votes or meet the constraints of budget reconciliation.

3. What is the timing for tax reform?

Tax reform could take up much of 2017 and even spill into 2018. House Speaker Paul Ryan, R-Wis., has stated his intention to pass tax reform legislation in the House prior to the August recess. Senate tax writers have indicated they plan to wait for the House to finish before starting serious action. The narrowly divided Senate could make the Senate process long and difficult, and the House and Senate will also have to resolve their own differences. Tax reform could move more quickly, but the most likely scenario appears to be final enactment very late in the year or next year (if successful).

4. So when would tax reform be effective?

Tax reform effective dates are likely to be largely prospective, meaning effective beginning Jan. 1, 2018, or Jan. 1, 2019. It's possible for rate cuts to be enacted retroactively to the beginning of 2017, but unlikely. The 2001 tax cuts provided retroactive rate relief, but only in the context of a budget surplus when the goal was to deliver tax cuts, not enact revenue-neutral tax reform. Nearly all major tax reform efforts have been largely prospective. There could be transition rules that could slow effective dates even further. The tax reform discussion draft from former House Ways and Means Chair Dave Camp, R-Mich., in 2013 slowly phased in its corporate rate cut.

On the other hand, narrower individual provisions could be made retroactive to as early as the date they are first made public. This would normally be applied to changes that are viewed as closing "loopholes" or that would allow significant tax-motivated gaming if prospective.

5. What would tax reform look like?

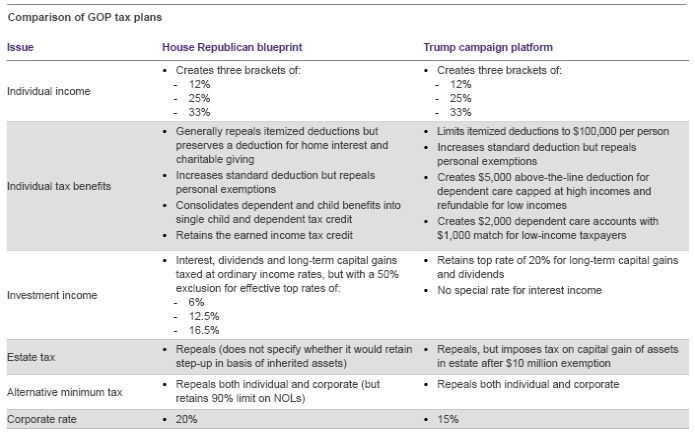

Republicans are committed to comprehensive tax reform, but there are policy differences among their plans. House Republicans released a tax reform blueprint last year, and they are currently writing a full bill based on it. Trump released his own tax reform platform during the campaign. Senate tax writers have not yet unveiled an independent plan. The House GOP blueprint will likely be the starting point. It would generally repeal targeted tax benefits in exchange for rate cuts, but unlike past reform efforts, also seeks to make structural changes. The idea is to convert the business income tax system to a more cashflow-based system that mimics the economic impact of a consumption tax like a value-added tax (VAT). The major provisions would:

- Cut the top individual rate to 33%

- Cut the top corporate rate to 20% (Trump has proposed 15%)

- Create a special 25% rate for active business income from a pass-through

- Repeal most business and individual benefits except for the mortgage interest and charitable deductions and the R&D credit

- Provide for full expensing of business equipment (including buildings), but limit interest expense

- Make business taxes border adjustable

- Move to a territorial tax system with a 100% dividend deduction

- Provide a one-time tax on unrepatriated earnings of 8.75% for cash (and cash equivalents) and 3.5% for everything else with the tax to be paid over an 8-year period

Many of these proposals are discussed in more detail below, and we have a full side-by-side comparison of the Trump and House GOP plans.

INDIVIDUAL TAXES

6. Would my individual tax benefits go away?

Yes, many targeted individual tax benefits would need to be sacrificed for a rate cut. Neither Trump nor House Republicans have offered a list of everything that will be repealed, but they have explicitly promised to retain only a few incentives. Both the Trump and House GOP blueprint would generally consolidate personal exemptions and the standard deduction into one large standard deduction. The House GOP plan would also consolidate tax-preferred retirement accounts, retain certain child tax benefits and the earned income tax credit, and preserve deductions for home mortgage interest and charitable giving.

7. Would there be limits on my itemized deductions?

Trump's campaign proposed a cap of $100,000 on itemized deductions for single taxpayers and $200,000 for joint filers. The House GOP plan does not include a limit but would eliminate most itemized deductions altogether. The House plan does retain the deductions for mortgage interest and charitable giving, but these incentives could be weakened for many taxpayers by an increase in the standard deduction. A higher standard deduction means fewer taxpayers who itemize deduction. Taxpayers who don't itemize don't get any tax benefit from these activities.

8. What is proposed for the individual AMT?

Alternative minimum tax (AMT) repeal has long been a key component of Republican tax reform plans and is very likely to be included in any plan that is ultimately enacted.

9. What is proposed for the estate tax?

Trump proposed repealing the estate tax, but imposing a tax on the built-in capital gain of assets in the estate. No details were provided, but presumably the tax would be paid by the estate, and the heirs would then receive a step-up in basis in any inherited assets. There would be an exemption for first $10 million in gains, and for small businesses and family farms.

The GOP House blueprint would also repeal the estate tax. It does not discuss whether the step-up in basis at death would be repealed, but this is typically considered the sacrifice for full estate tax repeal (the step-up in basis was repealed during the one-year estate tax repeal in 2010). Neither Trump nor the House GOP blueprint specify whether the gift tax would also be repealed. See question No. 27 for a discussion of how these proposals should affect current estate planning.

BUSINESS TAXES

10. Will my business tax benefits be repealed?

Yes, the idea is that most targeted business tax benefits will be exchanged for rate cuts. Both the Trump platform and the House GOP plan simply state that nearly all business benefits will be repealed, but without providing a list. Lobbying to protect various benefits will be fierce, and some provisions will undoubtedly survive. Both Trump and House Republicans have specifically promised to retain a research credit, while House Republicans have also proposed keeping the last-in, first-out method of accounting.

11. What about carried interest?

Trump proposed taxing carried interest as ordinary income during the campaign, but did not provide details on his proposal. The House GOP blueprint does not mention it one way or the other, but staff is reportedly considering retaining the current treatment. Regardless, carried interest will remain a target throughout the tax reform process, both due to its potential revenue impact and public visibility.

12. What is proposed for the corporate AMT?

The House GOP blueprint would repeal the corporate AMT, but would impose a limit on net operating losses (NOLs) similar to the AMT rule.

13. How would NOLs be treated?

The House GOP blueprint would not allow any NOL carrybacks, but would allow indefinite carryforwards. NOLs could not offset more than 90% of taxable income in any year.

14. What would 'full expensing' mean?

The House GOP plan proposes allowing taxpayers to deduct the full cost of all property in the year it is placed in service. This would include all tangible and intangible property (including real property) except land, and would basically end the practice of depreciation for tax purposes. The price for this benefit would be new limits on interest deductions (see next question). Trump offers more narrow provisions to allow full expensing only for certain manufacturers or manufacturing equipment. The treatment of property already in service is not known.

15. What would happen to my interest expense?

The House GOP plan would no longer allow a deduction for interest expense in excess of interest income. Trump would more narrowly target the taxpayers enjoying his more limited expensing proposal. House Republicans have said their proposal would provide exceptions for financial industries like banking, insurance and leasing. Net interest expense could be carried forward indefinitely to offset future interest income. House Republicans are also discussing possible transition rules that would grandfather in certain pre-existing debt as of as early as the day legislative language is released. The limit on interest deductions is proposed only in the context of a shift to full expensing, and would be very unlikely to be proposed as a standalone revenue raiser.

16. What does 'border adjustable' in the House GOP plan mean?

The House GOP blueprint offers few details on border adjustability, but discussions by committee staff and economists have revealed that the proposal is meant to mimic a value-added tax by exempting export receipts from income while disallowing deductions for imports. So the cost basis of any imported item would be zero. For example, a taxpayer that pays $100 to import a good and then sells it in the U.S. for $110, would normally have $10 of income after deducting the $100 cost of goods sold. Under the proposal, the $100 cost would not be deductible so that the income would be the full $110, even though the margin is only $10. On the other hand, any gross receipts from an exported product would not be included in income.

17. Is border adjustability likely to be part of final bill?

This is an open question and the most pressing issue for lawmakers to resolve. The proposal is controversial and will sharply divide the business community. Already, the Trump administration has criticized it, and important constituencies like retailers are rising in opposition. The opposition maintains that the proposal will create a regressive consumption tax that will sharply raise prices, while economists who support it say that currency adjustments will hold down domestic prices on imported products.

There are two other important complications. First, border adjustability is expected to be the largest revenue raiser in the bill. Without it, many of the rate cuts and other provisions in the bill may not be possible under current cost constraints. Second, it could be ruled an illegal export subsidy by the World Trade Organization (WTO).

18. How would a WTO challenge work?

The WTO is an international organization created to facilitate trade. The WTO settles trade disputes among members and can levy sanctions or allow retaliatory tariffs against countries that do not abide by WTO rules. The threat of these penalties has forced changes in U.S. tax law before (the repeal of the FSC-ETI regime in favor of Section 199 in 2004), and could make border adjustability untenable.

The WTO has traditionally allowed indirect taxes like VATs to be adjusted at the border (applied to imports but not exports). The WTO has generally maintained that border adjustments for direct taxes like income taxes are an impermissible export subsidy. House Republicans have argued that because their tax system would mimic a VAT from an economic perspective in many ways, it should be considered an indirect tax by the WTO. This is far from clear. Typically, a complaint would not be lodged until after a law is passed and could take years to litigate, but it would be possible for the WTO to provide guidance while the debate is ongoing.

19. How would tax reform treat pass-throughs?

Final rates will be subject to some negotiating and compromises, but the expectation is that the top corporate rate will be significantly lower than the top individual rate. To help alleviate this difference, both Trump and the House GOP plan propose a reduced rate on the active business income from a pass-through. In the House GOP plan, the 25% pass-through rate is between the 20% corporate rate and 33% top individual rate. Trump proposed making certain pass-throughs eligible for his 15% corporate rate.

20. How would a reduced rate on pass-through business income work?

The special rates would apply when the qualified pass-through income is taxed on an individual's return. Trump's campaign surrogates released conflicting information on how his plan would work, but, in general, he proposed to only allow "small" pass-throughs to qualify for the 15% rate while enjoying full pass-through treatment. He provided no information on the threshold, but indicated large pass-throughs could not use the 15% rate while enjoying pass-through treatment. This could be interpreted to mean that only retained earnings would be eligible for the 15% rate, or that pass-throughs would need to elect to be taxed as C corporations for the lower rate.

The House GOP blueprint would provide its 25% rate only on active business income and would create rules to ensure a proper amount of income is characterized as compensation and taxed at ordinary individual rates. Staff is discussing various ways to designate income as compensation and subject to normal individual rate, including:

- Applying a standard split such as 70% compensation and 30% business earnings

- Strengthening current reasonable compensation principles, perhaps with a pre-certification process

- Providing the reduced rate only for retained earnings while taxing any distributions at the same rate as compensation

- Providing the reduced rate only for what could be considered a return on invested capital, calculated using a set rate of return on an individual's amount of capital in the business

More than one of these options could be used as safe harbors, but the rules are still under discussion.

21. So pass-throughs have to give up the same business benefits as C corporations for a smaller rate cut?

Potentially, yes, pass-through businesses could be forced to give up the same business benefits as C corporations but get a much shallower rate cut. Grant Thornton has long advocated for fairness for pass-throughs during tax reform. See the latest information on this topic from our website.

INTERNATIONAL TAXES

22. What would tax reform do for offshore income?

The House GOP blueprint and the Trump campaign platform split over international taxes. House Republicans would generally move toward a territorial tax system that would exempt foreign income from U.S. tax with a 100% dividend deduction. They would also repeal the bulk of Subpart F, including the foreign base company income rules (retaining the foreign personal holding company rules).

Trump proposes to not only retain the worldwide tax system, but to end deferral so that all income is subject to U.S. tax immediately. However, this is proposed within the context of a 15% corporate rate. Because foreign tax credits would be allowed, his system would function more like a global minimum tax applying to offshore earnings taxed at a rate lower than 15%. To transition to either system (and to raise revenue for tax reform) both plans would impose a one-time mandatory tax on unrepatriated earnings.

23. How would mandatory repatriation work?

The idea is to impose a one-time tax on all pre-existing foreign earnings that have not been repatriated as of the effective date. The tax would apply even if the money is not repatriated, but the earnings could then be brought back tax-free if desired. Trump proposed using a 10% rate during the campaign, while the House GOP blueprint would apply an 8.75% rate to cash and cash equivalents and a 3.5% rate for everything else. The tax could be paid over a period of time (eight years in the blueprint).

24. Are these international changes likely?

Yes, if tax reform is successful, the international changes are among the most likely to be enacted. There is broad agreement that the U.S. must shift to a territorial tax system, even among many Democrats. In fact, before the election, Democrats and Republicans discussed the possibility of bipartisan legislation that would pair international tax reform with infrastructure spending. Nearly every reform plan over the past several years has proposed similar international changes, although the details have differed and will still be subject to negotiation.

NEXT STEPS

25. Will the extenders provisions that expired at the end of 2016 be reinstated for 2017?

This remains unclear. More than 30 provisions expired at the end of 2016, including:

- Mortgage insurance deduction

- Exclusion for home debt forgiveness

- Accelerated depreciation for racehorses and motorsport tracks

- Empowerment zone incentives

- Alternative fuel and biofuel and biodiesel credits

- Energy-efficient new homes credit

- Energy-efficient home improvement credit

- Section 179D deduction for energy-efficient commercial buildings

- Credits for nonwind and nonsolar energy property under Sections 45 and 48

Taxpayers have learned to expect these provisions to be retroactively reinstated, and lawmakers may be reluctant to punish them for making investments based on that assumption. Extending them would also maintain the status quo while lawmakers work to complete tax reform. On the other hand, if tax reform is nearing completion by the end of the year and most of these provisions are not included, lawmakers may see no point in extending them. In addition, many of the most popular temporary provisions, such as the R&D credit, are now permanent. The remaining temporary provisions will not be treated with the same urgency by lawmakers.

26. Is there anything I should be doing before tax reform is effective?

Yes, the possibility of a rate cut effective beginning in 2018 or 2019 opens up many planning opportunities for 2017. If a rate cut is eventually enacted, it can turn normal deferral strategies into permanent benefits. Accelerating deductions into 2017 allows them to be used against today's higher rates, while deferring income allows it to be recognized against potentially lower rates.

For individuals, this can mean accelerating itemized deductions, but be careful. Many individual deductions, like for charitable giving, can run into AGI limits or phaseouts. On the business side, the opportunities are better. Most businesses employ dozens of separate accounting methods on everything from inventory and rebates to software development and advanced payments. Identifying a more favorable method of accounting often results in a favorable adjustment that can be taken fully in the year a change is made. Common opportunities include:

- Deferral of income related to advanced payments

- Deferral of recognition of disputed income

- Acceleration of the deduction for

liabilities and expenses related to the following:

- Computer software development expenses

- Self-insured medical expenses

- Prepaid expenses

- Real and personal property taxes

- Payroll taxes

- Rebates

- Reduction of amounts capitalized to inventory

Other opportunities include capital expenditures and the recovery period for fixed assets. A cost segregation study can often identify scores of building components that can be segregated and depreciated more quickly. As always, there are important reasons to be cautious. Method changes will have an ongoing impact. Tax reform could also retroactively take away the tax benefits for 2017. And it's always possible tax reform doesn't happen at all, or that rate changes are made effective early or late so that there is no rate difference between 2017 and 2018. The good news is that deferring tax is typically a good strategy if only for the cash flow benefits and the time-value of money.

Businesses with international operations should consider the changes very carefully. The possibility of a reduced rate for previously unrepatriated earnings could discourage repatriations now at the full rate. On the other hand, the mandatory repatriation and potential loss of foreign tax credits could be very painful for taxpayers who have reinvested earnings abroad.

Taxpayers with debt can also consider their borrowing and the possible loss of interest deductions on new debt as of as early as the date legislative language is introduced.

27. Should I stop estate planning?

It would be premature to abandon estate planning. Estate tax repeal has long been a staple of the Republican platform, but will remain difficult despite their election victory. Tax reform faces serious cost constraints, and Republicans will be under pressure to provide benefits for middle-income taxpayers. Now that the exemption has reached $5.49 million (almost $11 million per couple), repeal would benefit only a narrow group of individuals. Repeal could also hurt taxpayers below this threshold if it comes with the repeal of step-up in basis of inherited assets at death. The GOP House blueprint does not specifically address this issue, but it is the typical trade-off for repeal (Trump has proposed assessing tax on realized capital gains at death after a $10 million exemption).

The reconciliation process could also hamper repeal efforts. Republicans controlled Congress and the White House in 2001 in much the same way they do now (they lacked 60 votes in the Senate). They made estate tax repeal a top priority, but were only able to achieve a single year of repeal in 2010 before it sunsetted due to reconciliation. Stopping estate planning now could be just as big of a mistake as it would have been 10 years ago. It may, however, be prudent to avoid estate planning techniques that involve paying gift tax.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.