Seyfarth Synopsis: New York employers are facing a host of changes in wage and hour regulations for 2017: an increase to the minimum salary amounts for exempt status; increases in the minimum wage; and changes in the amount of tip, meal and lodgings credits allowed to be taken as an offset to employee wages as well as uniform allowances.

As we previously informed our loyal blog subscribers, the New Year has brought a host of changes for New York employers on the wage and hour front: an increase to the minimum salary amounts for exempt status; increases in the minimum wage; and changes in the amount of tip, meal and lodgings credits allowed to be taken as an offset to employee wages as well as uniform allowances.

If these changes were not scary enough for employers, Governor Cuomo announced on January 2 the launch of a 200-member multi-agency Minimum Wage Enforcement and Outreach Unit charged with ensuring that all minimum wage workers are paid the proper rate. The Unit will include specially trained staff from a number of state agencies, including the Department of Labor, Department of Taxation, Workers Compensation Board and the Department of State. The staff will educate both workers and businesses on specific requirements included under the new minimum wage rates. According to Governor Cuomo, "This new enforcement unit will ensure that workers are being paid what they earned, and employers who flaunt the law will be held accountable."

As a reminder, below is a summary of these recent changes:

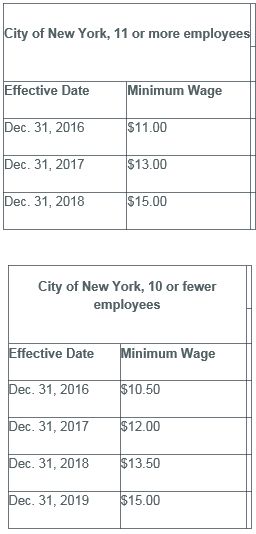

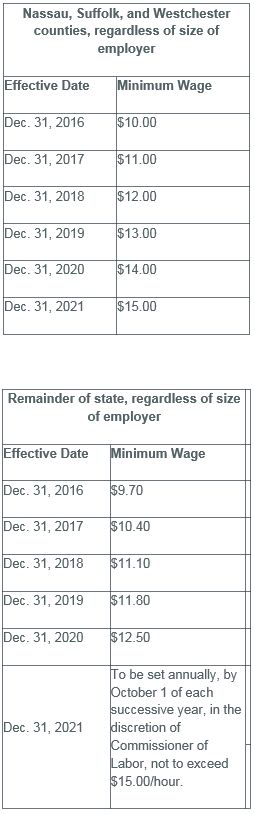

Minimum Wage

The new "tiered" minimum wage for New York employers is as follows:

The Department of Labor recently issued FAQs in connection with the minimum wage increase that address questions posed by the employer community since the announcement of this new "tiered" minimum wage system in New York, including the definitions of "large" and "small" employers in New York City and what rate(s) should be paid for employees who work at multiple job sites.

With respect to employer size, the FAQs state that a "large" New York City employer includes "any business that (1) employs one or more employees in New York City, and (2) has employed more than 10 employees at any time during the current or prior calendar year and among all worksites." Conversely, a small New York City employer includes "any business that (1) employs one or more employees in New York City and (2) has not employed more than 10 employees at any time during the current or prior calendar year and among all worksites." Notably, the FAQs make clear that "large" employers in New York City do not have to pay employees who work at a non-New York City location the New York City large employer minimum wage rate.

With respect to employees who work at multiple job sites, "an employer may pay the highest rate for all hours worked, or pay each hour worked in each region at the applicable minimum wage rate for that region." With respect to the overtime rate of pay for employees who work at multiple job sites, the FAQs note that, "overtime must be paid at one and a half times the employee's regular rate of pay. If an employee is paid at different rates for different hours, those rates may be blended in calculating the regular rate of pay."

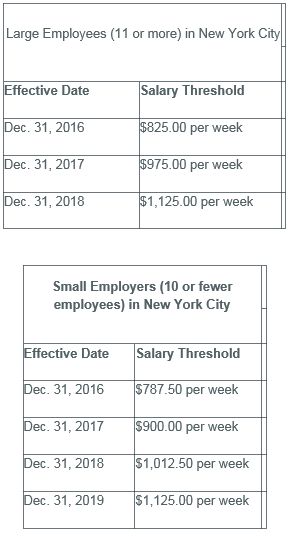

Salary Threshold for Exempt Employees

In keeping with the gradual increase in the State's minimum wage levels, the new tiered salary thresholds across the state, effective December 31, 2016, are now:

Contrary the hopes and expectations of many employers, the increase in the New York exempt-status salary levels went forward notwithstanding the injunction against the increase under the FLSA.

Tip Credits/Uniform Allowance and Meal/Lodging Credits

The new Wage Orders also adjust the amounts that employers can deduct for uniforms, meals and lodging and claim as a tip credit.

The Department of Labor has summarized the revisions applicable to hospitality employers, employers in "miscellaneous industries" and employers in the "building service industry". Employers should consult these summaries to determine how much they can deduct for a uniform allowance and claim as a meal, lodging and tip credits.

Tip Credits: Pursuant to the revised Regulations, covered employees must receive at least the applicable hourly "cash wage" (i.e., wages paid excluding tips), and tip credits may not exceed the hourly "credit" rate, so long as (i) the weekly average of tips meet the hourly "tip threshold" rate, and the actual total of tips received plus wages equal or exceed the basic minimum hourly rate in place at the time.

Uniform Maintenance Pay: The revised regulations also adjust the amount of pay employees must receive for uniform maintenance, which is required only if an employer does not maintain required uniforms for its employees. The applicable rates are based on the number of hours worked. Accordingly, employees working 30 or more hours per week will be paid at the highest rate; employees working between 20 and 30 hours per week will be paid at the medium rate; and employees working 20 or fewer hours per week will be paid at the lowest rate.

Meal and Lodging Credits: The revised regulations also adjust the amount employers can deduct from an employee's wages based on meals provided during working hours as well as lodging allowances that can be taken by employers. These changes vary depending on the industry and type of lodging, employer (for-profit or non-profit). Employers should consult the applicable wage orders to determine the revised amounts applicable to their employees.

Conclusion

Employers in New York should be on "high alert" given these recent changes to the minimum wage, permissible wage deductions/credits, and salary thresholds for exempt employees. Be careful out there!

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.