In the latest of our series of post-employment protection blog posts, we consider the compliance and regulatory issues that need to be thought through when drafting an effective post-employment restraint in Australia.

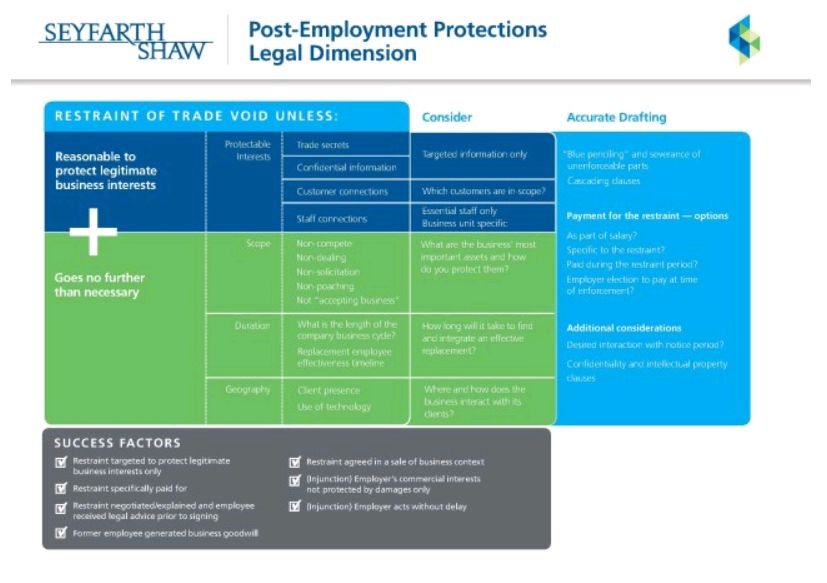

How will any restraint payment be structured?

The threshold question is what kind of payment (if any) to make in return for the agreement of an employee not to engage in particular activities, such as working for a competitor, soliciting business from clients, etc.

The best option will depend on the particular circumstances.

Payment could be part of normal salary. There could be a separate lump sum payment which is paid when the agreement is made or at the time the restraint is called on. Alternatively, an employer might wish to drip feed monthly payments during the restraint period. There are a number of ways to structure the arrangements that best suit the business and the employee concerned.

It is also possible for no specific payment to be made in return for the restraint. However, at a practical level, paying an individual not to engage in certain activities such as working for a competitor or poaching staff might mean the obligations are more likely to be complied with. For example, an executive who is not "out of pocket" during the restraint period is less likely to need to take the risk of working for a competitor.

From a purely legal perspective payment does not guarantee enforceability. When the payment is made and the quantum are discretionary matters to be taken into account by a court asked to enforce a restraint. In our experience, it is very helpful to be able to point to payment in return for agreement to be restrained.

Payment for a restraint will, of course, raise a number of regulatory disclosure, approval and tax issues.

"Gardening leave" compared to a post-employment restraint

At the outset it's important to distinguish between:

- payment of salary during a period of notice of termination where the employee is not required to work, which is referred to commonly as "gardening leave" because the employee cannot commence working for another employer but can engage in leisure activities such as gardening (Notice Payments); and

- additional payment/s made after termination of employment in return for the former employee's agreement to be prevented from engaging in certain activities such as working for a competitor or approaching their former clients, suppliers or colleagues (Restraint Payments).

Notice Payments will not raise the same issues as Restraint Payments. However, neither payment will guarantee the legal enforceability of the restrictions but will merely be a factor that a court may consider in deciding whether the restrictions are reasonable. The argument is that the payment will go some way to addressing the public policy concern about restraints to the effect that they should not deprive a person of their ability to earn a living.

Termination benefits requiring shareholder approval

In the case of certain executives (broadly "Key Management Personnel" as defined in the Corporations Act 2001 and directors) Restraint Payments may also require the approval of shareholders in general meeting if they are in connection with termination of employment or the transfer of any undertaking or property of the company. This is because the corporations legislation in Australia specifically deems a payment that is made as part of "a restrictive covenant, restraint-of-trade clause or non-compete clause" a benefit that requires shareholder approval.

Whether such approval is required must be determined on a case by case analysis. Generally, Notice Payments will not be caught by this requirement.

Board determination of "reasonableness" of the payment

For some executives a company's board of directors may also have to determine whether a Restraint Payment is "reasonable" in the context of the limits on payments to related parties under the corporations legislation. This is an issue that should be considered at the time a restraint provision is drafted and agreed. If a benefit is not considered reasonable then it will require shareholder approval. External advice may need to be taken by a board to assist its determination of whether a proposed payment is reasonable.

Disclosure

Corporations legislation and the Listing Rules of the Australian Securities Exchange impose obligations on companies to make disclosures about executive pay, including Restraint Payments and Notice Payments, in certain circumstances. Whether a payment is ultimately disclosed publicly may be a relevant consideration in deciding whether the payment is commercially acceptable to both the executive or employee and the company. On this basis any potential disclosure obligations should be considered at the time of drafting and agreeing payment obligations for restraints.

Taxation

Finally, the tax treatment of a Restraint Payment may be different to the tax treatment of a Notice Payment, depending on whether the Restraint Payment is categorised as an employment termination payment or a capital payment. Specific consideration of this issue will also be required.

Well drafted restraints of trade are a necessary and reasonable business tool and can be highly effective to protect business interests. To be enforceable, and to prevent side issues becoming a problem, the above matters need to be carefully thought through at the time the restraint is drafted and agreed.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.