Following a flurry of interest in "liquid alt" funds (also known as alternative mutual funds), Interval Alts are becoming increasingly popular. In 2015 alone, there have been ten filings for new Interval Alts. Interval Alts are non-traded closed-end funds registered under the Investment Company Act of 1940 (the Investment Company Act), but they function very much like traditional hedge funds. In addition to employing alternative strategies, they have terms similar to those of hedge funds, such as monthly subscriptions and quarterly or semi-annual liquidity. Because of the commonality in offering terms, many Interval Alts also charge fees similar to their sister hedge funds managed by the same manager (e.g., fees of 2 and 20, or some variation thereof). Unlike hedge funds, however, they may be publicly offered and therefore may be offered in a variety of distribution channels.

In a guest article, George M. Silfen and Ronald M. Feiman of Kramer Levin Naftalis & Frankel examine the regulatory basis for Interval Alts; explore the differences between such structures and liquid alternative funds; and address the marketing advantages of Interval Alts versus traditional hedge funds. The authors also provide an extensive chart comparing Interval Alts to alternative mutual funds and traditional hedge funds. For additional insight from Silfen, see "Kramer Levin Partner George Silfen Discusses Challenges Faced by Hedge Fund Managers in Operating and Distributing Alternative Mutual Funds," The Hedge Fund Law Report, Vol. 6, No. 16 (Apr. 18, 2013); and "How to Mitigate Conflicts Arising Out of Simultaneous Management of Hedge Funds and Alternative Mutual Funds Following the Same Strategy (Part Three of Three),"The Hedge Fund Law Report, Vol. 8, No. 15 (Apr. 16, 2015). For more from Kramer Levin partners, see "OTC Derivatives Clearing: How Does It Work and What Will Change?," The Hedge Fund Law Report, Vol. 4, No. 24 (Jul. 14, 2011).

Regulatory Basis for Interval Alts

Interval Alts derive their name from the fact that these funds provide liquidity within Rule 23c-3 under the Investment Company Act (the Interval Fund Rule), which allows closed-end funds to make annual, semi-annual or quarterly repurchase offers. Alternatively, Interval Alts may provide liquidity through repurchase offers made under Rule 13e-4 under the Securities Exchange Act of 1934 (the Tender Offer Rule) in lieu of the Interval Fund Rule.

Managers offering Interval Alts often opt to operate outside of the Interval Fund Rule because that rule does not provide for monthly liquidity, whereas the Tender Offer Rule allows monthly repurchase offers. Also, the Interval Fund Rule has stricter provisions dictating the timing of the valuation of the portfolio, which renders it impractical for certain funds with illiquid assets — such as funds of hedge funds — to operate within the Interval Fund Rule. By contrast, the Tender Offer Rule does not have similar restrictive pricing provisions. As a result, many Interval Alt managers operate under the Tender Offer Rule rather than under the Interval Fund Rule.

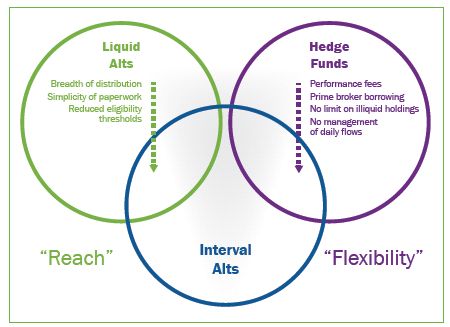

Advantages over Liquid Alts

Interval Alts, like liquid alts, are subject to regulation under the Investment Company Act, including affiliated transaction restrictions, leverage limitations, governance by an independent board of directors and quarterly reporting of portfolio holdings (at least until adoption of a newly proposed SEC rule that would require monthly portfolio disclosure). The foregoing requirements need to be considered carefully by fund managers before moving forward with any registered fund. The intricate regulations governing how leverage may or may not be obtained, including through derivatives, may require some degree of re-engineering from what is customary for hedge funds. In addition, policies and procedures, especially governing potential conflicts such as trade allocation procedures, need to be formalized in anticipation of launching any public fund, whether an Interval Alt or a liquid alt. See "Eight Important Regulatory and Operational Differences Between Managing Hedge Funds and Alternative Mutual Funds," The Hedge Fund Law Report, Vol. 7, No. 44 (Nov. 20, 2014).

However, Interval Alts offer a number of key advantages over liquid alts. First, there are no liquidity restrictions, whereas liquid alts may only hold up to 15% of their assets in illiquid securities. Thus, certain, more illiquid hedge fund strategies are better suited as an Interval Alt as they cannot employ the same strategy in a liquid alt.

In addition, liquid alts are subject to daily fluctuations in assets (which sometimes can be significant) due to daily subscriptions and redemptions, potentially disrupting the manager's ability to employ its investment strategy in a consistent manner. Interval Alts (which are not subject to daily flow activity) allow the manager greater ability to align the fund's strategy to the sister hedge fund.

Also, like hedge funds, Interval Alts are permitted to effect margin borrowings directly from their prime brokers (subject to Investment Company Act limitations on leverage), whereas liquid alts may only borrow from banks.

In short, Interval Alts afford managers greater flexibility to mimic their hedge fund products, while also allowing them to access broader distribution channels than pure hedge funds, as discussed below.

Marketing Advantages over Hedge Funds

As publicly offered products, Interval Alts inherently offer increased marketing flexibility through: (1) greater freedom to advertise/market broadly (e.g., without the requirement for a pre-existing relationship); (2) allowance for an unlimited number of investors; and (3) the lack of any requirement that investors satisfy "Qualified Purchaser" eligibility standards (generally, investors with $5 million of net investments); however, if the Interval Alt pays a performance fee on gains, the fund may only be sold to "Qualified Clients" (generally, investors with $2 million of net worth, excluding their primary residence).

While the above features can be important, experience with managers reveals that the recent wave of Interval Alt popularity is driven more by the following "marketing" advantages Interval Alts have over hedge funds:

1. Simple Sale Process for Brokers — Unlike the cumbersome hedge fund subscription process, intermediaries selling Interval Alts can complete a sale quickly with little "red tape." Interval Alts can be sold through National Securities Clearing Corporation or electronic networking transactions with the investor completing, at most, a one-page certificate. (Despite the simpler process, Interval Alt brokers also enjoy sales compensation that often exceeds hedge fund placement fees.);

2. 1099 Reporting — Interval Alts can generate 1099s for clients, which is a far more attractive tax reporting result for investors than the inherently complex K-1 reporting of hedge funds. (Brokers also prefer 1099 reporting, as it fosters a simpler, less time-consuming client relationship.); and

3. ERISA and IRA investors — Interval Alts, unlike hedge funds, can take in an unlimited number of ERISA and IRA investors — all in the same vehicle (without altering investment strategies or interposing any complex master/feeder or offshore fund structure).

Although Interval Alts are more simple products for end users (clients and brokers), they require careful structuring considerations concerning pricing/fees, multiple distribution channel availability, prime brokerage arrangements and taxation, among other areas. More importantly, the fund must fit well within the hedge fund manager's existing suite of funds, without disruption to its business or cannibalization of its other products.

Interval Alts strike a useful balance, successfully marrying the interests of managers, clients and brokers. We thus expect the current filing wave to continue.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.