On 15 November 2014, Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014, amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups, was published in the Official Journal of the European Union. The Member States must transpose this new Directive into national law by 6 December 2016 and its provisions are to apply as from the financial years beginning on 1 January 2017 or during the calendar year 2017.

The Accounting Directive

As a reminder, Directive 2013/34/EU of the European Parliament and of the Council of 26 June 2013 on the annual financial statements, consolidated financial statements and related reports of certain types of undertakings (the Accounting Directive) repeals the old Directives 78/660/EEC and 83/349/EEC. The Member States are required to transpose it into national law by 20 July 2015, but may provide that its provisions shall apply only to financial statements for financial years beginning on 1 January 2016 or during the calendar year 2016.

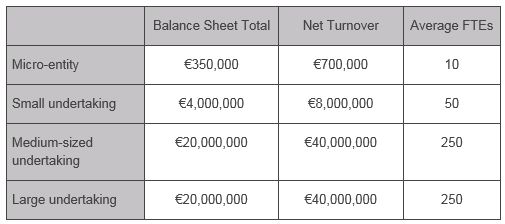

In short, the main purpose of the Accounting Directive is to encourage Member States to provide for different accounting and disclosure requirements, and reporting obligations, including with respect to the contents of the management report and the inclusion of a 'corporate governance statement', for so-called micro-entities, small and medium-sized companies, and large undertakings in accordance with the "think small first" principle. In order to qualify as 'micro, small or medium sized', the relevant entity may not exceed the limits of at least two of the three following criteria. 'Large' undertakings are those that exceed at least two of the three following criteria.

A fifth category of undertakings, the so-called public-interest entities (PIEs), includes listed companies, credit institutions, insurance undertakings or other entities so designated by Member States because of the nature of their business, their size or the number of their employees.

Mining and Other Extractive Activities

The Accounting Directive also introduced specific reporting requirements for large undertakings and all PIEs that are active in the ' extractive industry 1' or the logging of primary forests, as a result of which a report on payments made to governments is to be made public on an annual basis, it being understood that any payment, whether made as a single payment or as a series of related payments, need not to be taken into account in the report if it is below €100,000 within a financial year.

Additional Non-Financial Reporting

Non-Financial Statement

The new Directive 2014/95/EU introduces further corporate social responsibility reporting obligations for all large PIEs (employing, on a consolidated basis, an average of 500 employees during the financial year).Such entities are required to include, in the annual management report, an additional non-financial statement containing information to the extent necessary for an understanding of the undertaking's development, performance, position and impact of its activity, relating to, as a minimum: environmental, social and employee matters; respect for human rights; anti-corruption and bribery matters, including:

- a brief description of an undertaking's business model;

- a description of the policies pursued by the undertaking in relation to those matters, including due diligence processes implemented;

- the outcome of those policies;

- the principal risks related to those matters linked to the undertaking's operations including, where relevant and proportionate, its business relationships, products or services which are likely to cause adverse impacts in those areas, and how to manage those risks; and

- non-financial key performance indicators relevant to the particular business.

The reporting is based on a "comply or explain principle" meaning that when an undertaking does not pursue policies in relation to one or more of those matters, the non-financial statement must provide a clear and reasoned explanation for not doing so.

The commission shall prepare non-binding guidelines on methodology for reporting non-financial information, including non-financial key performance indicators, general and sectoral, with a view to facilitating relevant, useful and comparable disclosure of non-financial information. These guidelines are expected by 6 December 2016 and the commission shall first consult relevant stakeholders.

Diversity Policy

Directive 2014/95/EU also introduces a new section to be included in the 'corporate governance statement' to be prepared in accordance with the Accounting Directive, whereby a description is to be given of the diversity policy applied in relation to the undertaking's administrative, management and supervisory bodies with regard to aspects such as age, gender, or education and professional backgrounds; the objective of that diversity policy; how it has been implemented; and the results in the reporting period. If no such policy is applied, the statement shall contain an explanation as to why this is the case ('comply or explain').

Footnote

1. Defined as undertakings with any activity involving the exploration, prospection, discovery, development, and extraction of inter alia minerals, oil, natural gas deposits, etc.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.