Overview

Exposure to foreign exchange rate risk is often hedged with forward foreign exchange ("FX") contracts, which fix an exchange rate now for settlement at a future date. The parties to an FX forward agree to buy or sell a currency at a specified exchange rate, at a specified quantity and on a specified future date. On the specified future date, the two parties exchange the currency amounts to settle their claims under the contract.

Some countries' monetary authorities impose restrictions on their currency's convertibility in order to regulate the currency's inflow and outflow. As a consequence, offshore parties can face difficulty hedging their exposure with forward contracts as such transactions might not be allowed under the currency restrictions. As a result, markets for non-deliverable forwards, which do not require the exchange of the non-convertible currency, have developed.

A non-deliverable forward foreign exchange contract ("NDF") is similar to a regular forward FX contract but does not require physical delivery of the designated currencies at maturity. Instead, the NDF specifies an exchange rate ("contracted forward exchange rate" or simply "forward rate") against a convertible currency, typically the US dollar (USD), a notional amount of the non-convertible currency and a settlement date. On the settlement date, the spot market exchange rate is compared to the forward rate and the contract is net-settled in the convertible currency based on the notional amount. The manner in which the spot rate is determined is agreed upon at the initiation of the contract and varies by currency and jurisdiction. This might be the daily rate published by the central bank of the non-convertible currency or an industry group reference benchmark which is typically an average of rates from several banks and FX dealers. NDFs are traded primarily in over-the-counter markets and are cash-settled in the convertible currency. Since March 2012, NDFs can also be cleared through several exchanges such as the CME, the ICE, and ForexClear.

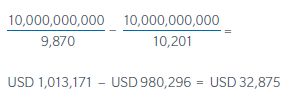

As an example, suppose that an American company, Company A, will receive IDR 10,000,000,000 (Indonesian Rupiah) three months from today as a result of an investment in Indonesia. Upon receipt, Company A is planning to convert the payment into USD at the then available spot rate; Indonesian authorities permit this spot market transaction because of the underlying investment. In contrast, no deliverable forward FX contracts are available for IDR, so in order to hedge the exchange rate risk between IDR and USD, Company A enters into an NDF with a bank in Singapore. The NDF contract specifies a notional of IDR 10,000,000,000, a maturity of three months, and the agreed upon forward rate of 9,870 which equals the current spot rate (IDR 9,870 = USD 1). The spot rate for IDR is set by the Associations of Banks in Singapore ("ABS"), which calculates the rate based on data submitted by banks (using a process similar to the one used to calculate LIBOR and other global reference benchmarks). Suppose that three months later, at maturity, this spot rate is 10,201. The close-out payment of the NDF is calculated as:

History

The NDF market began to grow in the early 1990s, focused mostly on emerging market currencies in Latin America. Because NDF trading was primarily used as a means to hedge exchange rate risk for non-convertible currencies, market growth has been greatest for currencies of countries with increasingly active investors (portfolio and/or foreign direct investment) and countries with uncertain exchange rate regimes. NDF markets in currencies that were becoming increasingly convertible have dissipated or disappeared. Throughout the 1990s, increasing investments in emerging markets in Asia and Eastern Europe further expanded the NDF market. By 1997 the International Swaps and Derivatives Association added provisions for NDF transactions to its definitions.

Risks of NDFs

A party to an NDF is exposed to various risks, most importantly the risk that the spot rate moves above or below the forward rate in the contract. Parties using NDFs to speculate or to hedge another asset willingly assume this risk; their exposure to spot rate movements is the purpose of entering an NDF. Major financial institutions are primarily involved in the NDF markets through their market-maker activities. They frequently offset the risk assumed through the broker market, with other banks and onshore market participants and exchanges. This implies that these market-making firms are exposed to basis riskâ€"the risk that offsetting contracts might settle at different rates in the event of a disruption. Finally, NDFs are not considered to have emerging market country risk or sovereign risk, but are subject to counterparty risk if not centrally cleared through an exchange.

NDFs, when used as a hedging instrument, have additional risks which need to be considered. The main risk concerns the spot rate at which the contract settles. As explained above, this rate is often a rate posted by onshore authorities or offshore organizations and there is no guarantee that NDF parties will actually be able to convert their onshore currency at that rate. In particular, in times of market crisis or when a change in exchange rate regime is increasingly likely, the likelihood that the NDF fixing rate is an indication of where the spot market is trading may be significantly diminished. This may affect the usefulness of NDFs as a hedging product because protection from the contracts would be most desired during episodes of market distress.

Recent Developments

As mentioned above, the process for determining the spot rate varies by currency and jurisdiction. For some currencies, the market exchange rate is determined using a similar process to that which determines LIBOR. For example, the reference rates for the Indonesian rupiah, Malaysian ringgit, Singapore dollar, and Thai baht are overseen by the ABS. For these currencies the ABS collects quotes from a panel of participating banks, excludes a proportion of the highest and lowest bids, and averages the remaining values to determine the spot rate.

Probes into the recent LIBOR rigging scandal have raised concerns that spot rates on NDF contracts might also have been manipulated for some currencies, including the Malaysian ringgit and the Indonesian rupiah. The concerns are that traders could have attempted to move spot rates in order to profit when settling NDFs carried on their books. In the summer of 2012 the Monetary Authority of Singapore ("MAS") instructed banks to review their processes to set foreign-exchange rates used to settle certain currency forward contracts. As of November 2012, both UBS and RBS had suspended Singapore-based FX traders following internal probes into the manipulation of NDF rates and pending an investigation into the manipulation of the NDF spot rates by the MAS. Citigroup is also being investigated.1 In January 2013, a Reuters news article cited an unnamed source with knowledge of the inquiries and reports and stated that the probes found evidence showing that traders from several banks colluded to fix NDF rates in order to benefit their trading books.

Footnotes

1. BusinessWeek, "Citigroup Says Singapore Monetary Authority Probes Rates," 6 November 2012.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.