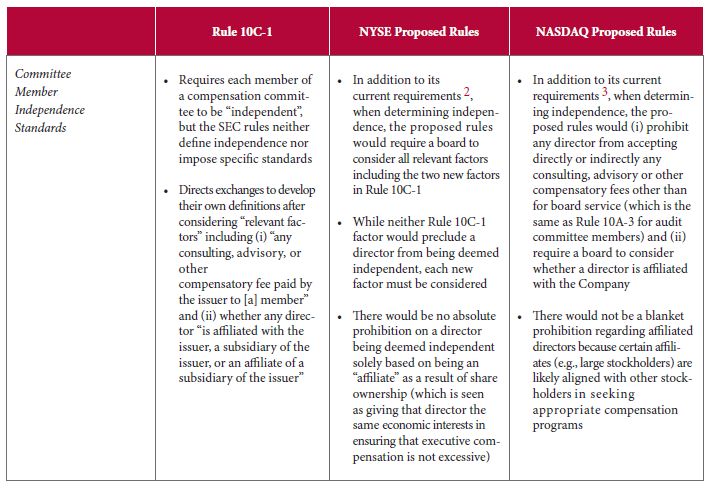

On June 20, 2012, in furtherance of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Securities and Exchange Commission adopted new Rule 10C-1 under the Securities Exchange Act of 1934 and amendments to Item 407 of Regulation S-K1 that, among other things, focused on ensuring the independence of compensation committee members by directing the national securities exchanges to "establish listings standards that ... require each member of a listed issuer's compensation committee to be ... 'independent' as defined in the listing standards of the exchange." In response to this SEC release, each national securities exchange in late September proposed rule change submissions to comply with new Rule 10C-1.

The requirements of Rule 10C-1 and the proposed new listing standards of each of the NYSE and NASDAQ are summarized below. Once the exchanges' final listing standards are approved, we will disseminate a comprehensive review updating this Client Alert.

Footnotes

1 For a further discussion on the SEC's adopting release for Rule 10C-1 and amendments to Item 407 of Regulation S-K, please see our Client Alerts entitled " SEC Adopts New Rules Requiring Stock Exchange Listing Standards For Compensation Committees" (June 27, 2012).

2 When determining "independence" under its current listing standards, the NYSE rules (a) require a board to affirmatively determine that a director has no material relationship to the company and (b) provide that a director may not be independent if a relationship exists that would violate five "bright line" tests.

3 When determining "independence" under its current standards, the NASDAQ rules (a) require a board to affirmatively determine that a director does not have a relationship that would interfere with the exercise of independent judgment in carrying out that director's responsibilities and (b) provide that certain categories of director, based on certain identified relationships, cannot be independent.

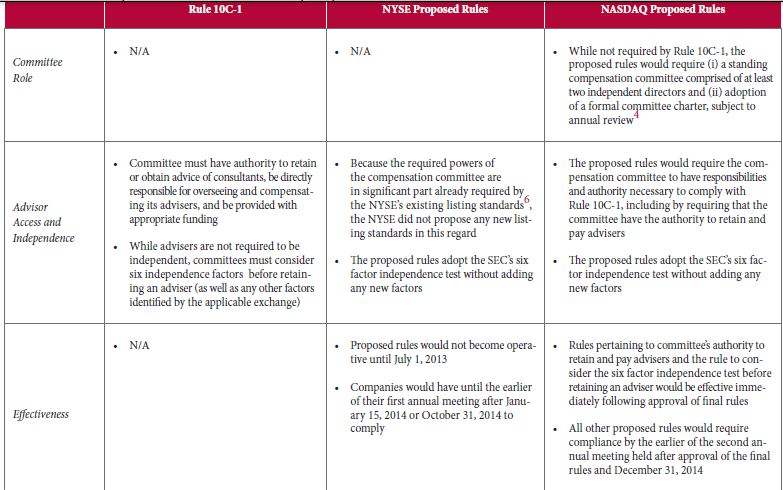

4 In adopting this approach under the proposed rules, NASDAQ is proposing to eliminate its alternative rule that permits a majority of independent directors, in lieu of having a standing compensation committee, determine executive compensation.

5 The six factors set forth in Rule 10C-1 include (i) the provision of other services to the company by the compensation committee adviser, (ii) the percentage of the adviser's total revenue that is represented by the fees received from the company, (iii) the policies and procedures of the adviser that are designed to prevent conflicts of interest, (iv) any business or personal relationship of the adviser with an executive officer, (v) any business or personal relationship of the adviser with a member of the compensation committee and (vi) any stock of the company owned by the adviser.

6 Significantly all of Rule 10C-1's requirements in this regard exist in the NYSE's compensation committee charter listing standards.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.