In This Issue:

- The Fed Tries a Twist

- Chilly Reception for Disclosure Bill

- Obama's Jobs Bill Prompts Disclosure for New Issues

- Bond Market Snapshot

The Fed Tries a Twist

The Federal Reserve recently initiated a "sell short, buy long" bond strategy in an effort to stimulate the current stagnant economy. Under this strategy, dubbed "Operation Twist," the Fed will sell $400 billion of maturing short-term bonds (6-month to 2-year maturities) and use the proceeds to buy long-term bonds (5-, 10-, 30-year maturities). President Kennedy tried a similar strategy in 1961, partly to discourage investors from selling dollars for gold and then selling the gold in Europe for a profit, and partly to provide stimulus by keeping long-term rates lower. The program was originally thought to be a failure, but some economists think that it was effective after isolating certain statistics.

Operation Twist sparked a massive sell-off in stocks and continued an unprecedented bond market rally, driving the 10-year Treasury yield down to 1.71%, the lowest yield since the 1950s. It is difficult to predict, however, how much real stimulus will result from this strategy. Interest rates have been at historic lows for an extended period and the economy has remained unexpectedly unresponsive to traditional stimulus. Will lowering interest rates prompt consumers and businesses to spend on houses, cars, and hiring? Or is the fear of an uncertain future at the heart of our stagnant economy?

Chilly Reception for Disclosure Bill

U.S. Representative Mike Quigley (D-IL) has drafted a bill designed to expand the authority of the Securities and Exchange Commission to regulate disclosure for municipal bonds. The bill, called the "Municipal Securities Transparency Act of 2011," is currently being circulated to market participants and regulators for review and comment.

Under current disclosure law, municipal bond underwriters are generally required to ensure that adequate disclosure is available to investors. If adopted in its current form, Quigley's bill would amend the Securities and Exchange Act of 1934 (the "1934 Act") to give the SEC the authority to directly require bond issuers to provide official statements and other disclosure documents, including financial statements, to investors. The bill would also authorize the SEC to establish the frequency with which such documents must be provided.

Many market participants, including several bond issuers, have voiced their disapproval of the bill. The draft bill does not require issuers to file documents directly with the SEC. The bill does, however, authorize the SEC to require issuers to provide disclosure to investors. Opponents of the bill argue that such a provision violates the intent of the Tower Amendment, a 1975 amendment to the 1934 Act that prohibits the SEC from directly or indirectly requiring municipal bond issuers to file disclosure documents with the SEC or the Municipal Securities Rulemaking Board prior to the sale of municipal securities.

Obama's Jobs Bill Prompts Disclosure for New Issues

President Obama recently submitted his jobs bill to Congress. The bill, called the "American Jobs Act of 2011," provides an array of solutions to the current economic crisis, including closing tax loopholes and reducing the funding for several federal programs such as Medicare and certain farm subsidies. One of the bill's provisions that has unnerved the municipal bond industry is Obama's proposal to limit the deduction of tax-exempt interest on municipal securities for higher income taxpayers.

Notwithstanding several predictions by pundits that the chances of the bill's passage are slim, disclosure regarding its potential impact on municipal bonds began to appear in official statements within days of the bill's introduction.

"Bond lawyers generally agree that the potential impact warrants a mention," says Lewis Feldman, head of the Public Finance Practice at Goodwin Procter LLP. "If the bill were to pass with even a modified form of the provision, it could significantly reduce the value of the securities for an investor."

In its present form, the bill would limit the deduction of certain income and expenditures, including tax-exempt interest from municipal bonds, to 28% for individuals with $200,000 or more of taxable income ($250,000 for married couples). The provision would apply to taxable years beginning on or after January 1, 2013, and there would be no grandfathering for tax-exempt bonds currently held by tax payers.

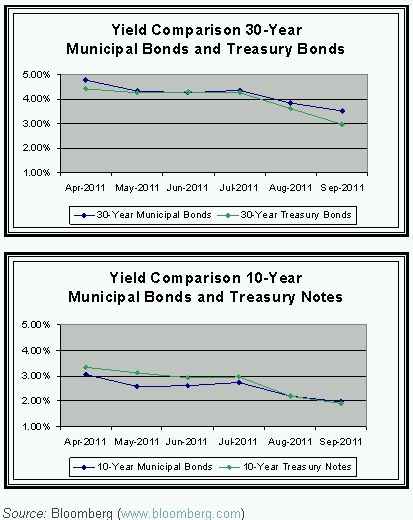

Bond Market Snapshot

In September 2011, yields on both municipal bonds and Treasuries continued to drop to record lows. 10-year munis dropped from 2.20% to 1.99%, falling as low as 1.71% following the Fed's announcement of its "Twist" policy (see "The Fed Tries a Twist" in this issue). Yields on 10-year Treasury notes also dropped from 2.19 to 1.90%. Yields on 30-year securities dropped from 3.85% to 3.51% for municipal bonds and from 3.60% to 2.98% for Treasuries.

Goodwin Procter LLP is one of the nation's leading law firms, with a team of 700 attorneys and offices in Boston, Los Angeles, New York, San Diego, San Francisco and Washington, D.C. The firm combines in-depth legal knowledge with practical business experience to deliver innovative solutions to complex legal problems. We provide litigation, corporate law and real estate services to clients ranging from start-up companies to Fortune 500 multinationals, with a focus on matters involving private equity, technology companies, real estate capital markets, financial services, intellectual property and products liability.

This article, which may be considered advertising under the ethical rules of certain jurisdictions, is provided with the understanding that it does not constitute the rendering of legal advice or other professional advice by Goodwin Procter LLP or its attorneys. © 2011 Goodwin Procter LLP. All rights reserved.