In March 2023, we wrote about the evolving challenges affecting the advertising market, shedding light on ad spend headwinds during economic downturns. Our research indicated that the advertising market often faces a prolonged recovery period, spanning an estimated 8 to 19 quarters after the broader economy.

Thus far, the recovery has been volatile. According to Standard Media Index, the U.S. ad market experienced an average monthly decline of -3.8% in the first half of 2023. However, Q3 saw a noteworthy turning point with 6.2% year-over-year growth in July, followed by 1.2% year-over-year growth in August—the first consecutive months of growth since early 2022.

While there are promising signs for the ad market in 2024—the presidential election will provide a $10+ billion boost in the U.S.—it's unlikely digital growth will return to high-double-digit rates seen pre-pandemic. Our prediction for a FY 2024 recovery is in line with industry forecasts, indicating a moderate rebound and mid-single-digit growth for overall ad spend. However, this hinges on broader economic conditions, which remain unclear.

Inflation is a significant factor in this uncertainty. According to AlixPartners' 2023 U.S. Retail Holiday-Outlook Survey, 44% of consumers think the economy is doing worse now than a year ago, and 34% think the economy will be worse in a year.

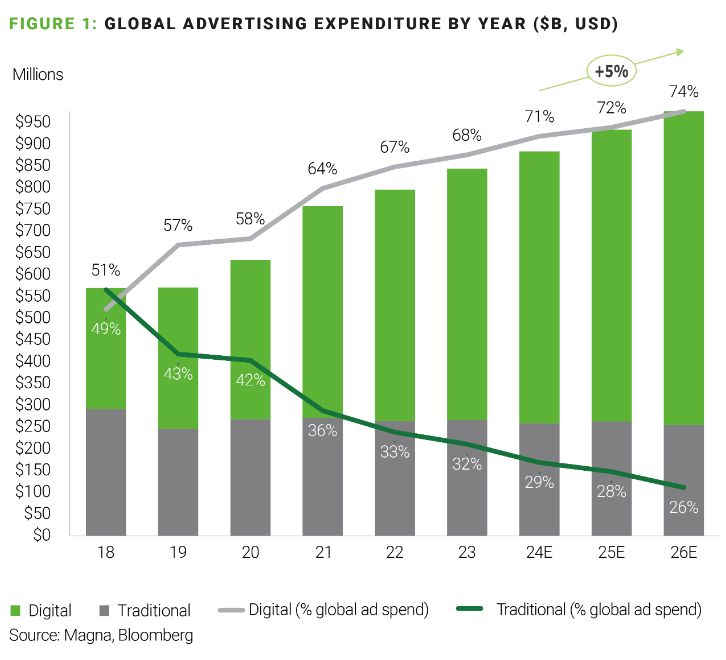

Over the next three years, the global ad market is expected to stabilize at a 5% CAGR, but budget shifts across the advertising value chain are poised to create an uneven recovery across channels and platforms.

Traditional channel spend will not fully recover to pre-pandemic levels as advertisers will further reallocate budgets to digital platforms.

A recent media agency survey by Digiday found that 49% of advertisers expect budgets to increase in 2024; 43% expect budgets to remain the same and only 8% expect budgets to decrease. But advertisers will allocate budget increases toward digital channels—such as social media, search marketing, digital displays, streaming video, connected TV (CTV), and retail media.

We expect reallocation of traditional channel ad spend from linear TV, print, and radio to total roughly $10-20 billion in 2024. This is in line with a 1-2% global spending reallocation to digital in 2022 and 2023 but demonstrates a leveling off compared to previous years, which saw reallocation rates of 5-7% over the total market.

In times of economic uncertainty, digital advertising platforms provide a valuable benefit. They allow advertisers to swiftly move funds across various platforms like CTV, retail media networks, search, and social media. This flexibility enhances advertisers' ability to adapt to changing circumstances.

CTV is rapidly approaching Pay TV. CTV is on an upward trajectory, on track to capture 39% of total TV ad spend by 2026—posing an imminent threat to Pay TV's dominance over TV advertising. Over the next year, we anticipate market dynamics will accelerate the flow of ad dollars to CTV, potentially hastening a point of inflection.

- Pay TV has been a trusted and reliable platform for advertisers

for decades, but its weakening stronghold hinges on tentpole

programming like elections, live news, and sports—which will

continue to shift toward live-streaming models (more on this

later).

- More SVOD price hikes will come in 2024 as providers attempt to draw more subscribers to ad-supported tiers. We anticipate Disney and Netflix advertising video on demand (AVOD) tiers will steadily gain more traction with advertisers this year, but at a slower rate than Amazon. Given the strength of its well-established ad network, demand for ads on Prime Video will be significantly higher than that of other players.

As the ad market rebounds, we expect to see scrutiny over digital-dollar allocation in budgets. Instead of an "everything but the kitchen sink" approach, advertisers will funnel a larger portion of their budgets into fewer digital channels that drive higher engagement with their target audiences.

We expect to see divergence in ad revenue growth across social media platforms. Intensifying competition and user growth saturation—approaching 230 million users in the U.S. (67% of the population) with less than 2% user CAGR through 2025—will drive uneven performance for players over the next year. For instance, legacy platforms like Facebook and X (formerly Twitter) will face challenges in retaining users according to forecasts, suppressing advertiser ROI.

Second-tier platforms, such as Snapchat and Pinterest, will find it increasingly difficult to compete with larger rivals even if they serve a niche or offer a differentiated experience in a specific category, such as shopping or online communities.

Fragmentation and saturation are driving large players, namely Meta and TikTok, to expand into new functional areas to retain user engagement, which will create greater convergence.

Platforms moving to innovate with new GenAI tools and advertising services could win greater share. To do so, they must offer a compelling value proposition to attract and retain users and creators, while providing differentiated ad solutions for brands and creators.

2024 will be a pivotal year for advertisers to evolve data & technology strategies to mitigate unforeseen costs and ROI damages.

Amid the evolving landscape for global data privacy regulations, marketers face a growing checklist to comply with the proliferation of policies. Four more U.S. state laws will take effect in 2024, along with talks of federal law for AI and data privacy and tighter EU general data protection regulation (GDPR) enforcement (including the Digital Markets Act and Digital Services Act).

Companies will need to be particularly diligent in maintaining robust data standards and governance practices as the role of AI in marketing and advertising evolves. This will expose new blind spot risks for marketers—who are already required to disclose how they use personal data to power AI tools under GDPR.

This article is an excerpt from our 2024 Media and Entertainment Predictions Report. You can view the full report here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.