Even with the growth of streaming, a future model to replace the highly profitable Pay TV structure has yet to take shape in a way that satisfies both industry players and consumers. But while the future model remains uncertain, wholesale distribution deals are bringing operators and streaming services together—a strategy that diverges from the "emulate Netflix" trend of the late 2010s.

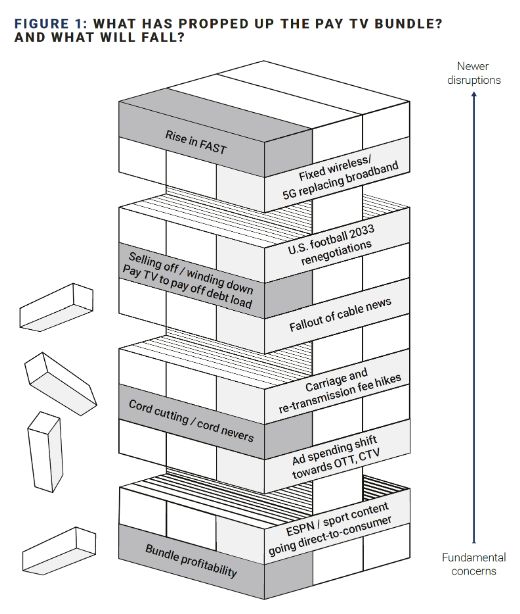

In July, we wrote about how the decline of the Pay TV bundle operates like a game of Jenga. Each new disruption is like pulling another block out of the tower. Unless Pay TV operators pivot, it's only a matter of time before the whole tower topples over. In August, the tower started to shake with the Charter-Disney carriage dispute. Stock prices in the ecosystem plunged as TV industry players and investors waited to see if the tower would topple. The negotiated agreement served as a block pulled out without collapsing the tower.

In the wake of the Charter and Disney agreement, it's evident that traditional Pay TV providers are not ready to go down without a fight. Cable providers know higher carriage fees will not continue to offset lost revenues from a declining subscriber base, especially as programmers move more premium content exclusively to direct-to-consumer (DTC).

In Charter's case, its weakness acted as a strength. Through preemptive diversification away from Pay TV as a main source of revenue, the company claims to have "reached the point of economic indifference" with its Pay TV business model. Calling attention to DTC vulnerabilities demonstrated that programmers have more to lose in this evolving landscape, and the proof is in the bottom line. Disney could have lost $4 billion in yearly free cash flow (FCF) without the new agreement, according to Oppenheimer estimates.

A pivotal aspect of the Charter-Disney deal was its DTC wholesale distribution agreement. Disney+ (the ad-supported tier) and ESPN+ will be provided to an estimated 9-10 million premium Spectrum cable subscribers, sold to Charter on a discounted wholesale basis.

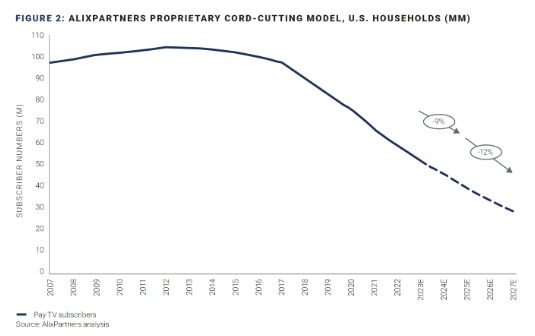

Over the next year, Pay TV providers will follow a similar framework when executing distribution deals with other DTC providers that maintain linear assets. With that said, this will not restore Pay TV to its peak-profit glory days—we anticipate cord-cutting will accelerate in 2024 (see Figure 2 below).

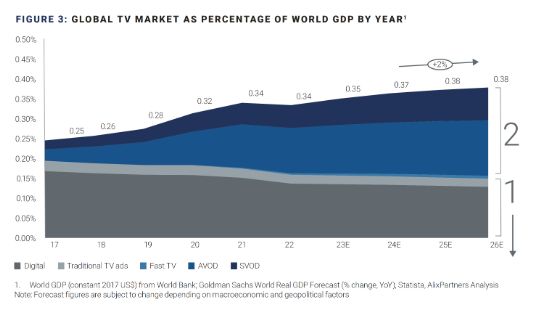

Global TV market growth will begin to level off as Pay TV revenues continue to shrink and the streaming market continues to mature.

As a result of a tapering CAGR, it is unlikely the market will support the 80+ streaming players that exist today globally, leading to streaming consolidation in 2024. In the U.S., we foresee streaming as a "winner-take-most" market with 4-5 winners.

We see three key signs that the global TV market is approaching a critical inflection point:

- Diminishing revenue pool

within Pay TV

Combined Pay TV subscription and ad revenues will fall to 0.16% world GDP in 2024 (falling at a negative -3% CAGR since 2017). - Deceleration in streaming growth as the market

reaches maturity

OTT revenues will reach 0.21% world GDP in 2024. However, high-double-digit growth of 22% CAGR since 2017 will slow to a 5% CAGR from 2024 to 2026, demonstrating platform maturity. - Approaching the maximum consumers are willing to spend

on premium subscription tiers

With rising premium subscription prices, consumers have started seeking alternative OTT offerings.

The tides will turn back in favor of bundled offerings

DTC providers will need to tap into wholesale licensing and distribution to unlock incremental value in streaming markets. According to Omdia, bundles that include Pay TV, broadband, or wireless plans alongside a streaming subscription will generate 70% of OTT video net sub adds.

At the same time, consumers are increasingly overwhelmed by the proliferation of platforms, rising prices, and disparate billing sources for multiple subscriptions. Demand for bundles is growing as consumers crave a simplified experience—more content with fewer apps to flip between—and better value, as they save 20-50% with bundled services vs. subscribing à la carte.

Global estimates forecast that bundles will constitute one-fourth of global subscriptions by 2028. We believe the opportunity for streaming bundles in the U.S. could be even higher than global estimates—with the potential to surpass 50% of total subscription video on demand (SVOD) purchases through telco or aggregator bundles.

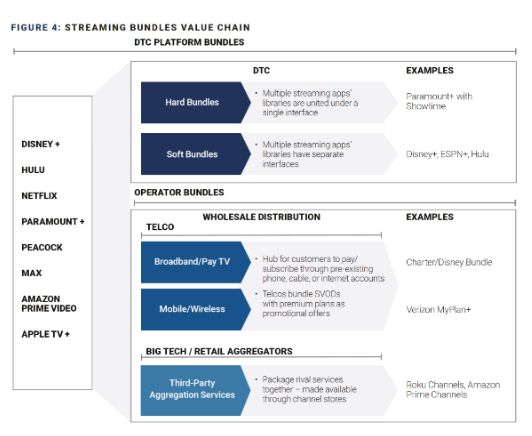

The current streaming bundle value chain is a complex ecosystem with more than 1,200 documented partnerships between streaming services and wholesale distributors such as telcos and cable providers.

Is the new "streaming war" becoming the "streaming bundles war"?

It remains to be seen whether telcos, big tech companies, or streaming providers themselves will dominate in a world that leans wholesale. Can traditional multichannel video programming distributors (MVPDs) remain the wholesalers of choice in a world without Pay TV if they pivot to provide bundled streaming offerings with virtual MVPD and SVOD?

The pendulum will swing back toward bundled offerings, but to what extent? Different operator bundles encompass varying levels of "invasiveness" to streaming businesses, and DTC providers will want to weigh the trade-offs. Do the upsides of bundles—greater net new subscribers, lower customer acquisition cost, and reduced churn—outweigh the downsides of lower average revenue per unit (APRU) for DTC and a requirement for providers to share more data?

This article is an excerpt from our 2024 Media and Entertainment Predictions Report. You can view the full report here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.