INTRODUCTION

On 2 November 2009, the Committee of European Insurance and Occupational Pensions Supervisors (CEIOPS) issued its third set of technical advice on implementation measures for consultation.

Following on from the last set of consultation papers (CPs) released in July 2009, this draft advice covers a range of topics across the entire Solvency II spectrum, including aspects of the Minimum Capital Requirement (MCR), Solvency Capital Requirement (SCR) Standard Formula, Internal Model, Own Funds and Repackaged Loans.

This draft advice will influence the final shape of insurance regulation across European Union member states, with final advice on these implementing measures due to be submitted to the European Commission in January 2010. This third set of papers is subject to a six week consultation period ending at 11am GMT on 11 December 2009. We welcome the opportunity that this consultation period provides for the industry to engage in the development of the detailed Solvency II regulations, and we strongly encourage firms and other stakeholders to provide constructive and practical feedback to CEIOPS in their required format by the deadline.

We have presented here a summary of each consultation paper in this wave, pulling out the main elements of the draft advice, along with our view of the key themes and impacts for the UK insurance industry. We hope that you will find it useful. Deloitte have commented on previously issued consultation papers and will continue to express our views to assist CEIOPS in its crucial rule-making activities.

CP 63 – REPACKAGED LOANS INVESTMENT

Purpose – This paper provides advice with regard to investments in repackaged loans or similar financial arrangements. The aim of the paper is to ensure cross-sectoral consistency and remove any potential misalignment of interests between the originators (the companies issuing the financial instrument) and investors in such financial instruments.

Key Messages

Fundamentally, CEIOPS's view is that, if investors understood better the quality of the loans being securitised, they could make an informed decision whether to invest in them. Consequently better transparency would make the originators' and the investors' interests more aligned and allow investors to make a more informed investment decision.

The implementing measures are high level and principles based – with specific detail to be provided at Level 3 and with the facility be amended with new market innovation in order not to stifle new developments.

|

The advice is unusual in that some of the requirements are to be met by the originator (which could be an unregulated entity) before a (re)insurance undertaking is allowed to invest in repackaged loans issued after 1 January 2011. |

(Re)insurance undertakings would be prohibited from investing in such securities unless the requirements are met rather than simply limiting the credit that can be taken for them or having an adequate capital charge.

This CP does not deal with the capital requirement implications of holding these investments.

Detailed Summary

The paper sets out seven principles.

Principle 1 – Originator's Retained Interest

Undertakings should only invest in repackaged loans or similar financial arrangements if the originator retains a net economic interest of at least 5% measured at origination and maintained on an on-going basis.

Principle 2 – Criteria For Sponsor And Originator Credit Institutions

The investing undertaking should ensure that the sponsor and originator credit institution: base credit granting (which is to be securitised) on sound and well defined criteria and on the same basis on which the originator's own exposure to credit is granted; operate effective systems to manage ongoing administration and monitoring; diversify each credit portfolio; and maintain documentation to include policy for credit risk.

Principle 3 – Transparency And Disclosure

The investing undertaking shall ensure that the sponsor and originator disclose the level of their commitment to maintain a net economic interest in the securitisation.

Principle 4 – Skill, Care And Diligence

The investing undertaking should be able to identify, measure, monitor, control and report the risks of these products and pay attention to assessing the ALM risk, concentration risk and investment risk with due regard to internal investment policy (including setting out counterparty, industry, geographical and quantitative limits).

Principle 5 – Monitoring Procedures

The investing undertaking should establish monitoring procedures commensurate with the risk profile of their investments in these securities and with appropriate relevant information.

Principle 6 – Stress Tests (Including Using Financial Models)

Where an investing undertaking holds a material value of repackaged loans, it should perform stress tests e.g. as part of its ORSA, appropriate to its securitisation positions and simultaneously taking into account the dynamic effect on the rest of the business.

Principle 7 – Formal Policies, Procedures And Reporting

The investing undertaking needs to demonstrate to its supervisory authority before investing that, for each securitisation position, it has a comprehensive and thorough understanding of, and has implemented formal policies and procedures appropriate to, the investment portfolio. There must be an adequate level of internal reporting and external reporting within supervisory reporting and public disclosure requirements.

Grandfathering

These principles shall apply from 31 December 2014 for existing securitisations where new underlying exposures are added or substituted after that date.

CP 64 – EXTENSION OF THE RECOVERY PERIOD

Purpose – This paper provides advice on the extension of the recovery period by the supervisory authority, in the event of an exceptional market fall in financial markets.

Key Messages

CEIOPS is proposing an upper limit of 30 months (i.e. 21 months in addition to the 9 month period which applies in normal market conditions) on the extension of the recovery period during exceptional falls in financial markets, in cases where the capital of the undertaking falls below the SCR.

|

The recent financial crisis shows how important it is to have guidance in this area. The drop in the FTSE combined with the widening of corporate bond spreads put significant pressure on some UK insurers' balance sheets. In some circumstances, this led to the ICA being treated as a soft rather than a hard limit. It is therefore clear that a formalised process is required going forward. |

Detailed Summary

CEIOPS has decided to keep a broad definition of financial markets as well as the definition of an exceptional fall in markets. It has also stipulated its preference to establish a consultation process before a supervisory authority considers it appropriate to extend the recovery period.

The maximum extension period supported by CEIOPS is an upper limit with the condition that the supervisory authority could ask an entity to restore the financial position over a shorter period.

CEIOPS has stated that extensions will need to be made on a case by case basis and no formula can be applied to derive the extension. The external and internal factors to be taken into account include:

- External Factors: Financial market stability (including systemic risk), in particular the pro-cyclical impact of distressed sales of assets on the financial markets; the ability of financial markets to provide extra capital at a reasonable price; the availability in financial markets of adequate financial mitigation instruments at a reasonable price; the capacity of the reinsurance market to provide reinsurance cover at a reasonable price; and

- Internal factors: Causes leading to the noncompliance with the SCR; degree of non-compliance with the SCR; composition of own funds held by the (re)insurer; composition of the undertaking's assets; nature and duration of technical provisions and other liabilities; solutions effectively available to the undertaking; potential availability of support from other group entities; the size or significance of the undertaking relative to the market; steps taken by the undertaking to limit the outflow of capital and the deterioration of its solvency situation.

When an entity is granted an extension period it would have to report every 3 months on the progress towards SCR compliance. Any extension granted could be removed if no significant progress was achieved against the entity's own recovery plan. Following the withdrawal of an extension period, the supervisory authority would have the power to take the measures deemed appropriate in order to close the gap between the own funds and the SCR.

Any extension withdrawal would be publicly disclosed in the Solvency and Financial Condition Report. In addition CEIOPS suggests that the supervisory authority should also disclose the number, range and average duration of these extensions.

CP 65 – PARTIAL INTERNAL MODELS

Purpose – This paper provides advice in respect of partial internal models covering: the scope of partial internal models; specific provisions for the approval of partial internal models, and in particular how results of partial internal models may be integrated into the results of the standard formula; the concept of a major business unit; the integration of risks not covered in the standard formula; and the changes to be made to the standards set out in Articles 118 to 123.

Key Messages

Partial internal models give firms flexibility to choose which risks and which business units will be covered in their internal models. The supervisory authority will require a proper justification of the limitation of scope in order to prevent "cherry picking", and they can also request a transition plan to extend the scope of the internal model.

|

We believe that scoping a partial internal model will be a significant task, and that (re)insurers should give due attention to this in order to minimise the risk of their partial internal model being rejected, or having to extend the scope of the internal model. |

|

The selection of the technique to integrate results from the partial internal model with results from the standard formula should be carefully considered. CEIOPS's preferred approach, which is to use the standard formula correlation matrix or a technique chosen from a list to be provided in Level 3 text, could be onerous. (Re)insurers will have to provide evidence that the standard formula correlation matrix approach and the techniques suggested in the Level 3 text are either not feasible or not appropriate before they can apply any internally developed technique. Although CEIOPS advises that the Level 3 list should be regularly updated, we believe that there is a risk that the use of new techniques could be restricted. |

Detailed Summary

Scope

The scope of a partial internal model can include:

- one or more risk modules for the whole business or for one or more major business units;

- one or more risk sub-modules for the whole business or for one or more major business units;

- the adjustment for the loss absorbency capacity of technical provisions and deferred taxes for the whole business or for one or more major business units; and

- operational risk for the whole business or for one or more major business units.

In addition, (re)insurers could model risks not covered by the standard formula.

(Re)insurers are required to demonstrate that the limitations in scope have been properly justified, and there should be no ambiguity as to which risks, assets and/or liabilities are included in the scope and those which are excluded. The supervisory authority retains the right to disagree with the proposed scope and reject the model; approve it with conditions; or require the (re)insurer to submit a transition plan to extend the scope of the model.

CEIOPS also sets out advice on the definition of a major business unit. It must be a functional unit which is managed with independence and with dedicated governance processes. It must also make sense to calculate both profit and losses and capital charges for that business unit. The term major implies that the business unit must be materially significant for the SCR calculation.

CP 66 – SUPERVISION OF GROUPS WITH CENTRALISED RISK MANAGEMENT

Purpose – This paper provides advice in respect of the conditions that must be satisfied for the supervision of a group where risk management is centralised within the organisation. These conditions are in addition to the need for the group supervisor to agree to a single ORSA at the solo and group level and a single solvency and financial condition report for the whole group.

Key Messages

Within any group there needs to be consistently applied group wide risk management (GWRM) operating at both the group level and the subsidiary. A group may elect to satisfy the GWRM requirements through centralised risk management (CRM) where the risk management and internal control mechanisms are performed centrally. CRM ordinarily involves the risk management arrangements of the parent covering the subsidiary, but the centralisation can be undertaken anywhere within the group. Supervisory approval needs to be obtained where a group wants to adopt CRM. Each application is evaluated on a case-by-case basis and the impact upon policyholders and adherence to regulatory requirements will be key considerations.

Detailed Summary

Group Wide Risk Management (GWRM)

We note the following:

- the governance requirements applicable to a solo undertaking apply equally to the extent relevant at the group level;

- there is a need to have in place an effective system of governance at the group level which provides for sound and prudent management of the group business. This includes for example a risk management function, compliance function and internal audit function as well as a group wide risk management strategy, policies, processes and procedures;

- within this arrangement special focus needs to be given to group specific risks, interdependencies and concentrations;

- risk management and internal control mechanisms need to be implemented consistently across the group. A primary objective of GWRM is to foster a common understanding of the functioning and reporting of risk management and aid the quality and comparability of results; and

- whilst the solo undertaking has responsibility for ensuring adequate risk management at a solo level, the parent is charged with ensuring consistent implementation and constant monitoring of all relevant processes within all individual subsidiaries, and maintaining adequate tools and expertise to oversee and steer the functioning of risk management.

Centralised Risk Management (CRM)

We note the following:

- the principal condition for obtaining the permission for centralised risk management is that risk management processes and internal control mechanisms of the parent cover the subsidiary and this is generally deemed to be met if material tasks in this regard are substantially transferred from the subsidiary to the parent;

- although CRM may be achieved through outsourcing or other group arrangements, neither option absolves the (re)insurance undertaking from its ultimate responsibilities with regard to the transferred function and activities;

- whilst it is envisaged that outsourcing of risk management would be to the parent, it can be outsourced to another provider within the group;

- the parent needs to be able to demonstrate that the subsidiary has an effective governance system in place, even if certain functions are outsourced within the group; and

- all requirements must be adhered to both on application and on a continuous basis, with significant changes being immediately reported to the relevant supervisory authority – solo and group.

CP 67 – TREATMENT OF PARTICIPATIONS

Purpose – This paper provides advice on the solo treatment of participations in credit and financial institutions for the determination of own funds and advice on the approach to the calculation of the SCR and in particular the equity risk sub-module with respect to related undertakings.

Key Messages

CEIOPS is of the view that the same method should apply regardless of whether the related undertaking is a subsidiary or participation. However CEIOPS distinguishes between whether the participation or subsidiary is included or excluded from the scope of group supervision.

A distinction is also made between unregulated entities related to the financial sector and unregulated entities not related to the financial sector.

The Level 1 text refers only to holdings in subordinated claims and instruments for credit and financial institutions – however CEIOPS is of the opinion that, for all regulated undertakings, investment in all types of own funds should be considered.

|

CEIOPS considered different approaches supported by a minority of members which are also summarised below. In addition, CEIOPS considers that participation in non-regulated entities in the financial sector and within the scope of group supervision should not be recognised for the purpose of the MCR and SCR. CEIOPS considers that own funds from participations in financial and credit institutions should not be recognised for the purpose of the SCR and MCR. The look-through method was not considered an option for the treatment of participations because supervisors would be unable to identify which own funds reside in the solo entity (as it is a line-by-line aggregation). |

Detailed Summary

Financial And Credit Institutions – In Scope Of Group Supervision

Own funds arising from participations in subentities should not be recognised as eligible own funds for the purpose of the SCR and MCR. Any holdings of subordinated claims and other instruments should be excluded. In effect the investment is fully derecognised.

Or – Minority view – Value on a market consistent basis and then apply an equity risk charge with a 50% reduction of the equity risk shock. The counterparty default risk module would apply to subordinated claims and instruments.

(Re)Insurers – In Scope Of Group Supervision

The excess of assets over liabilities which is used to meet the (re)insurer's own SCR cannot be used to meet the capital requirements in the participating entity and should be treated as a restricted item and excluded from the participating entity's eligible own funds (i.e. exclude the SCR of the participation).

Any holdings of subordinated claims and other instruments which meet Tier 2 or Tier 3 for the (re)insurer's own SCR would be excluded from the participating entity's own funds.

Any inherent goodwill in the valuation should be excluded from own funds of the participating undertaking.

The remaining portion of the participating undertaking's share of the participation's excess of own funds over its SCR (the excess) needs to be tested as to whether it provides the required capacity to absorb losses – and a judgment needs to be made on whether it should be restricted or, if included, on the tier in which it should fall.

The Commission considers that the approach recommended would not comply with Level 1 text. But CEIOPS reiterates its view on the grounds of cross sectoral consistency. Otherwise, if there is no scope for the exclusion of the own funds used to meet the participation's own SCR, CEIOPS's advice would be that the risk should be addressed by an equity capital requirement taking into account the particular risk profile of the participation.

Or – Minority view – as above.

Financial Non Regulated Undertakings – In Scope Of Group Supervision

Same approach as financial and credit institutions, i.e. own funds arising from participations should not be recognised as eligible own funds for the purpose of SCR and MCR. Any holdings of subordinated claims and other instruments should be excluded.

Or – Minority view – as above.

Non Financial Non Regulated Undertakings – In Scope Of Group Supervision

Unanimous view – Standard equity risk charge. No explicit statement about the recognition of subordinated claims and instruments.

Financial And Credit Institutions And (Re)Insurers – Excluded From Scope Of Group Supervision

Unanimous view – The solo supervisory authority should consider whether the circumstances leading to the exclusion from group supervision also apply to the assessment of the solo position.

If they do not apply (so needs to be included within the solo calculation), then treat as the same as in-scope above.

If they do apply (so excluded) and that the loss absorbency of the own funds derived from the participation is affected, then the amount should not be recognised as eligible own funds. Exclude holdings in subordinated claims and other instruments.

Non Financial Entities – Excluded From Scope Of Group Supervision

Unanimous view – Standard equity risk charge (depending on whether it should ever be considered a strategic investment).

CP 68 – RING-FENCED FUNDS

Purpose – This paper provides advice on adjustments to reduce own funds to reflect the lack of transferability of own funds and reduced scope for SCR risk diversification relating to Ring-Fenced Funds.

Key Messages

Own funds in Ring-Fenced Funds in excess of notional SCR for the Ring-Fenced Funds are to be excluded from own funds.

Diversification credit in SCR is reduced where there are Ring-Fenced Funds. The adjustment is made by reducing own funds rather than increasing SCR.

Detailed Summary

QIS4

At QIS4, most Ring-Fenced Funds were identified as with profit funds but there are also other examples. There was general agreement among QIS4 participants and supervisors on the principle of excluding own funds in excess of notional Ring-Fenced Funds SCR but there was no agreement on the basis of determining notional SCR and treatment of diversification.

Identification Of Ring-Fenced Funds

CEIOPS proposes two alternative principle-based definitions of Ring Fenced Funds and asks for comments on each definition.

Alternative A requires either a barrier to the sharing of profits with other parts of the firm's business and/or legal, constitutional or regulatory restrictions on the use of assets or capital for other parts of the firm's business.

Alternative B requires contractual or legal isolation of the funds both in a going concern and in a winding up situation. A barrier to the sharing of profits or restrictions on the use of assets or capital would not meet this definition of Ring Fenced Funds if the funds would become transferable in a winding up situation.

|

UK with-profits funds have a barrier to the sharing of profits and losses with other parts of the business and they have restrictions on the use of with-profits assets or capital for other parts of the firm's business. Therefore UK with-profits funds would fall within CEIOPS's alternative A for identification of Ring-Fenced Funds. CEIOPS's alternative B also requires a barrier to the transferability of assets or capital on a winding-up situation. UK firms that have a with-profits fund may need to consider whether there are any circumstances under which the surplus available to shareholders (or policyholders outside the with-profits fund) could exceed the shareholders' attributable share of any surplus in the with-profits fund in a winding up situation. If so, the with-profits fund may not meet the CEIOPS's alternative B for identification of Ring-Fenced Funds. If alternative B is adopted and certain UK with-profits funds are outside this definition then those firms would not be subject to the Ring-Fenced Funds reduction in eligible own funds at the level of the firm. |

Detailed Adjustment Calculation

The CEIOPS proposal is more prudent than the principle applied in CP 60 for insurance groups.

CP 68 excludes all diversification credit arising from the Ring-Fenced Funds – CP 60 excludes the proportionate share (based on the ring-fenced funds SCR reduced by the diversification ratio) attributable to the Ring-Fenced Funds.

|

Will the CP 60 insurance groups diversification adjustment principle change to match that set out in CP 68? If so, will the principle change for other examples of non-transferable funds? If UK with-profits funds are within the chosen definition of Ring-Fenced Funds then firms will face a twofold adjustment to own funds. Firstly a reduction for SCR diversification credit and secondly a deduction for surplus within a withprofits fund. Surplus within a with-profits fund in excess of the shareholder's attributable share of that surplus that is not being used to meet the notional SCR of the with-profits fund is not available to the entity to meet losses outside the with-profits fund. Therefore any such surplus would be included in the Ring-Fenced Funds deduction in determining own funds at the level of the firm. |

CP 69 – EQUITY RISK SUB-MODULE

Purpose – This paper provides advice with regard to the design and calibration of the equity risk sub-module including the symmetric adjustment mechanism and the duration damper.

Key Messages

The proposed equity stress is now stronger than in QIS4, due to re-calibration following the recent financial crisis. In addition, the implied volatility stresses are now applied simultaneously with the equity stress.

|

We believe that a combined stress for a drop in equities and an increase in equity volatility could be very onerous for UK with-profits funds. Although (re)insurers have typically included these stresses in their ICA, they are considered individually and aggregated using a correlation assumption. The proposed approach is likely to give a stress that is more onerous then a 1-in-200 year event. |

Detailed Summary

Stress For Equity Level

The majority of CEIOPS members support the equity stress being 45% for "global equity" (whereas in QIS4 it was 32%) and 60% for other equity, for example, hedge funds (whereas in QIS4 it was 45%).

|

We believe the industry is unlikely to welcome this strengthening, but it was largely inevitable given the Level 1 commitment to 1-in-200 failure rates and the recent financial crisis. We note that CEIOPS used world indices for calibration purposes which give greater diversification than the country/European specific indices used in most other studies. This means that insurers which allow in their internal models for any divergence between their own equity portfolios and the world index, may get even higher stresses. |

The stress is measured relative to a 12 month average instead of current market value as specified in Level 1 text, subject to a plus or minus 10% band (i.e. this means the stress cannot be less onerous than 35% but may be as onerous as 55%). The average is based on an index, which avoids data issues such as constructing historic prices for equities issued within the past year.

Stress Level For Equity Implied Volatilities

Whilst there was no volatility stress in QIS4, CEIOPS proposes an increase of volatilities as the current volatility multiplied by 1.6 and a decrease of volatilities as the current volatility multiplied by 0.85.

Applied Stress – Combination Of The Two

The stress is the combination of the above equity level stress and the volatility stress and not two individual stresses. The volatility stress is applied simultaneously with the equity stress, and the worst case of volatility increase or decrease is taken.

|

We believe it would be more appropiate to apply two separate stresses, one for equity and one for volatilities. These could have been combined within an enlarged correlation matrix, as is the case for most UK ICA submissions. We would welcome co-ordination between this CP and CP74 on this point. |

CP 70 – CALIBRATION OF MARKET RISK MODULE

Purpose – This paper provides advice on market risk stresses, other than equity stresses.

Key Messages

There is little change compared to QIS4 on interest rates but a slight strengthening of the property test. The new implied volatility test for interest rates is applied simultaneously with the interest rate stress tests.

The credit spread stress tests are substantially strengthened and the new formula has some awkward discontinuities at maturity bucket boundaries.

Detailed Summary

Interest Rates

Overall there is a slight strengthening on the upward stress and no change on the downward stress for interest rates. For example, the 10 year stress test (and similarly other tests) are similar for an interest rate increase. The current rate is multiplied by 1.51 (QIS4 by 1.42); and, for an interest rate decrease the current rate is multiplied by 0.66 (QIS4 by 0.66).

New interest rate volatility stress tests are applied to the Black volatility of swaptions whereby, for a volatility increase, the current volatility is multiplied by 1.95 (no QIS4 test); and, for a volatility decrease, the current volatility is multiplied by 0.80 (no QIS4 test).

The interest rate and volatility stresses are applied simultaneously. The worst of the four cases is taken

|

As with our comment in CP69, we believe the interest rate and volatility stresses should have been done separately, and then aggregated via a correlation matrix. As an alternative, the stresses for volatility (equity, volatility etc) could be performed in a combined stress. |

Currency

The currency stress is 25% (for non euro including GBP/EUR, QIS4 20%)

Property

The property stress for city offices, retail or warehouses is 30%, otherwise 25% (QIS4 20%).

|

Given the inclusion of implied volatility tests for equity and interest rates, we query why there is no similar requirement for property. |

Credit Spreads

Credit spread tests have substantially strengthened compared to QIS4. However, the new structure is expressed in terms of market value stresses in maturity buckets rather than spread changes. Thus, the 3-5 year bond stress is now a 7.1% market value fall, corresponding to a 237bp widening in 3 year spreads or a 142bp widening in 5 year spreads (QIS4: 25bp). Stresses are defined discontinuously within maturity buckets.

|

The present analysis focuses on bond market value movements, some of which are due to movements in risk free rates rather than spreads. As a result, interest rate risk is double-counted in the current calibration, to the extent that the changes in the risk-free curve will impact the corporate bond prices under the proposed methodology. |

CP 71 – SCR STANDARD FORMULA – CALIBRATION OF NON-LIFE UNDERWRITING RISK

Purpose – This paper provides advice on the calibration of the non-life underwriting risk sub-module and follows on from CP48. In particular, it addresses:

- the calibration of standard deviations for the premium and reserve risk sub module of the non-life underwriting risk module; and

- the calibration of the factors required under the "Factor Method" for the catastrophe risk sub-module.

Key Messages

Premium And Reserve Risk

The analysis carried out for this CP suggests that some of the volatility factors in QIS4 may have been under-calibrated for at least some lines of business and so, in CP71, the standard deviations for all lines of business have increased for premium and reserve risk which is expected to increase the underwriting risk capital charge by 35%.

|

The analysis conducted by CEIOPS was based on data provided by six member states and has been assumed to be a proxy for a European representative undertaking. However, the standard deviations are weighted by volume so this is likely to be appropriate for only the larger firms. Furthermore the portfolio of risks written by different member states can vary widely and so a larger data set would have provided a more accurate calibration. |

In relation to data, the requirements for use of data for firms adopting partial models to determine the volatility factors appears to be more onerous than those set out for the standard formula calibration.

|

The premium standard deviations are based on loss ratios which do cover volatility of claims but do not address expenses. We consider the use of combined ratios would address volatility better. |

Calibration Of The CAT Risk

The factors for the CAT risk capital charges are applied to gross data, and allow insurers to make an adjustment for their own reinsurance. In addition the capital charges for some lines of business are determined at a more granular level. Key concerns relating to these factors are:

- the factors are based on limited data and may underestimate the factors used for the calibration;

- the estimation and usage of a universal factor for all undertakings across all EU states is unrepresentative of reality since there will be significant differences between the risk profiles across undertakings;

- the factors are unlikely to represent a 1-in-200 year loss for all undertakings. A more granular factor based method could be more appropriate but will increase complexity; and

undertakings will need to calculate the net of reinsurance capital charges individually which will put strain on resources.

Separate factors are given for captives following concerns by local supervisors.

Detailed Summary

1) Calibration Of The Premium And Reserve Risk

The proposed factors for the Premium and Reserve risk factors have increased for all classes by between 10% and 100%. Factors for the Reinsurance and MAT classes have increased the most. The proposed increases would result in an average increase of around 35% on the Premium and Reserve risk sub-module. The more comprehensive analysis that CEIOPS has carried out supports the increase in the factors compared to QIS4.

The key limitations CEIOPS has highlighted in its analysis are:

- the factors at a line of business (LOB) level are intended to represent the average European insurer but may not be appropriate for all undertakings;

- the analysis is based on a small sample of data of insurance undertakings and may not capture all features of the European insurance market;

- the design of the standard formula implicitly allows for geographical diversification and risk mitigating effects of non-proportional reinsurance; and

- no explicit allowance for inflation has been made other than what is implicit.

pi>In calibrating the standard deviations the key assumptions used in the analysis of the data are:

- expenses do not impact volatility as they are considered as a deterministic percentage of premiums;

- no explicit allowance for inflation was made;

- average levels of geographical diversification and non proportional reinsurance levels were made;

- in some cases net data was not available so it is assumed that gross and net volatility are the same; and

- the risk margin does not change after stressed conditions.

For premium risk, data from six member states was applied to four different methods to estimate four different sets of results. In addition an analysis on the loss ratios time series from the QIS4 feedback was also summarised. This gave a total of five results to assist in determining the standard deviation for Premiums.

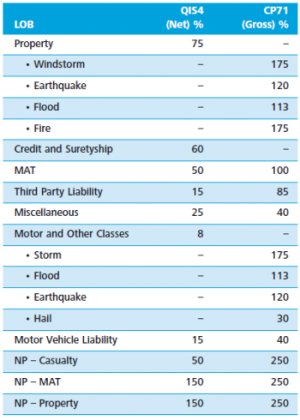

Table 1.1 – Selected CAT Factors By Class (QIS4 And CP71)

For reserve risk six methods that were used to estimate the reserve risk standard deviations to assist in the standard deviation calibration level.

Correlations

The correlation matrices to estimate the combined standard deviation factors are unchanged as CEIOPS considers these to be appropriate. Similarly, the correlation factor between the Premium and Reserve risk is unchanged from 50%.

2) CAT Risk – Calibration Of The Factor Method

CP71 provides information on CEIOPS's approach to calibrating the factors for CAT exposures for the "Factor Method". CEIOPS has calculated factors for each of the standard CATS for each LOB and they are based on various analyses CEIOPS has carried out and other benchmarks. The key changes compared to the QIS4 calibration are:

- The factors have been calculated on a gross of reinsurance basis so that insurers can allow for their own reinsurance.

- In QIS4, the factors were given for each LOB. In CP71 the factor has been calibrated by peril for Property and "Other Motor" lines of business.

Captives

The standard factors in QIS4 were considered by supervisors to be too low for captives and consequently separate factors for captives have been given in CP71 which are much higher.

CP 72 – SCR STANDARD FORMULA – FURTHER ADVICE ON HEALTH UNDERWRITING RISK

Purpose – This paper provides advice on the calibration of the health underwriting risk module (premium and reserve sub-modules).

Key Messages

Following a more comprehensive analysis by CEIOPS, the calibrations for the Premium and Reserve risk in the non- Similar to Life insurance Techniques module have increased significantly. CEIOPS carried out a preliminary high level impact assessment on the QIS4 exercise and concluded – "the proposed increases would result on average in an increase of 34% on the Premium and Reserve risk sub module".

|

We consider the higher calibration factors would increase the health SCR significantly and insurers who previously anticipated small changes could now have a much higher capital requirement under Solvency II. Consequently, insurers may be encouraged to use (partial) internal models. |

CP50 set out three options for the definition of lines of business for the assessment of the premium and reserve risk calibration. Following this, only one option has been defined in CP72 – the lines of business are split into three: accident, sickness and worker's compensation and calibrations have been defined for each.

Insurers that consider parameters to be inappropriate may apply for the approval of a (partial) internal model or make use of undertaking specific parameters.

Detailed Summary

As with CP50, the health underwriting capital requirement should be calculated as a combination of two sub modules:

- Similar to Life insurance Techniques (SLT) health – health insurance obligations pursued on a similar technical basis to life insurance; and

- non- Similar to Life insurance Techniques (NSLT) health

– health insurance obligations not pursued on a similar

technical basis to life insurance.

|

Data from six member states were used when determining the calibration factors for premium and reserve risk in the non-Similar to Life insurance Techniques health module. There is a risk that these calibrations do not reflect the risk profiles of smaller undertakings; especially given smaller undertakings are less likely to build approved (partial) internal models reflecting more realistic risk profile. |

Consistent with CP50, the risk elements under the Similar to Life insurance Techniques health module at a high level are the same as under the life module, though the underlying detail of the calculations and the scenarios considered continue to be different for some risks (in particular disability risk for medical insurance).

The correlations between the different risks in the Similar to Life insurance Techniques health module have been set equal to those for the life underwriting risk module. This follows from CP50 where the calibration provided had only been for illustrative purposes and there was an indication that the correlations should eventually be the same as those on the life underwriting risk module.

The calibration of the health catastrophe (CAT) risk for both Similar to Life insurance Techniques and non- Similar to Life insurance Techniques sub modules will be discussed in the CEIOPS Task Force on CAT risk and will be provided in June 2010.

No further clarity has been provided of how products should be classified into the different lines of business.

CP 73 – CALIBRATION OF THE MCR

Purpose – This paper provides a refinement of the QIS4 calibration of the MCR as well as post-QIS4 changes of the MCR and the SCR.

Key Messages

The calculation of the MCR remains relatively unchanged compared to QIS4 except for the already known change in the corridor (now fixed in the Level 1 text at 25%-45%) and the recalibration of the factors in the linear formula of the MCR.

QIS5 may provide further clarity on whether this new calibration will be appropriate.

Detailed Summary

The paper keeps to the linear formula in the calculation of the MCR. It builds on the definitions and notations in CP 55. The Level 1 text requires the MCR linear formula to be calibrated to an 85% Value-at-Risk confidence level over a one-year time horizon. As the linear formula is not expected to reflect accurately the prescribed level of confidence, CEIOPS calibrated the MCR linear formula relative to the SCR standard formula. Hence if there were significant changes to the SCR standard formula, the MCR linear formula would also need to be recalibrated.

CEIOPS notes that following the change to the cap and floor from 50% and 20% respectively in QIS4 to 45% and 25%, a larger percentage of the linear formula results will fall outside this corridor than was observed in QIS4 despite the effort put into finding the correct linear factors.

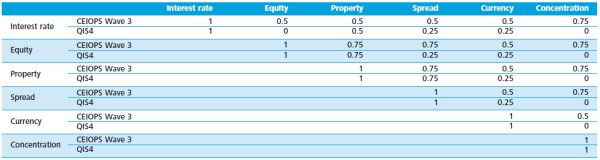

CP 74 – SCR STANDARD FORMULA – CORRELATIONS

Purpose – This paper provides advice regarding the regulatory power to impose capital add-ons in the context of setting correlation assumptions.

Key Messages

We note a major strengthening of interest rate/equity correlations.

|

This is likely to have a major impact on the capital requirement for UK with profit funds. We note, however, that a high correlation between interest rate and equity risk is not supported by historical evidence. We believe further consideration should be given to not strengthening the correlation assumptions in this regard. |

Detailed Summary

The old and new market correlations are shown in the table below (i.e. QIS4 and CEIOPS wave 3) (see Table 1.2 – Market Correlations).

|

The equity-interest rate correlation is now set at 50% (QIS4: 0%). This is a major consideration which will have an adverse effect on UK with profit funds. We note that the proposed approach is not sensitive to the direction of the interest rate exposure whereby firms exposed to an interest rate fall assume 50% correlation and firms exposed to an interest rate rise assume minus 50% correlation. This appears to be inconsistent as the correlation between interest rates and equities cannot simultaneously be both -50% and +50%. Indeed historical data supports values close to zero. |

Concentration risks are now 75% correlated with most other risks. There are further small changes made to underwriting risk correlations.

|

We would welcome further analysis and clarity over the appropriate method to allow for tail dependency and non-symmetric distribution. For example, the examples provided by CEIOPS in its discussion of tail correlations are based on independent random variables which, by definition, show no tail correlation. Their conclusion is to make most assumptions more prudent to reflect tail effects. We consider this likely overstates the necessary adjustment. |

Table 1.2 – Market Correlations

CP 75 – SCR STANDARD FORMULA – UNDERTAKING-SPECIFIC PARAMETERS

Purpose – This paper provides advice with regard to:

- the subset of standard parameters in the life, non-life and health underwriting risk modules that may be replaced with undertaking-specific parameters;

- the standardised methods to be used by a (re)insurance undertaking to calculate those undertaking-specific parameters; and

- the criteria with respect to the completeness, accuracy and appropriateness of the data utilised for that purpose in order for supervisory approval to be given.

Detailed Summary

The standard parameters that may be replaced with undertaking-specific parameters are the non-life premium risk and non-life reserve risk; the NSLT premium and reserve risk (health risk); the SLT health revision risk; and the revision shock for revision risk.

The paper outlines the criteria for the data used to calculate undertaking specific parameters. Data used may be internal or external but must be relevant and must also be consistent with the underlying assumptions of the standard methodology. It should be noted that the proportionality principle is not applicable due to the optional nature of the undertaking-specific parameters.

Supervisory approval is required to switch between the standard parameters and undertaking-specific parameters and back again. Supervisory approval will be based on the data provided. The undertaking must be able to demonstrate why the assumptions underlying standard parameters are appropriate for their risk profile and that the standard formula parameters are not a good representation of their particular risk profile.

The paper proposes a number of approaches for the standardised method for the calculation of the undertaking specific parameters for non-life premium risk and non-life reserve risk.

Non-life premium risk covers the risk of loss arising because the premium provision at the start of the year proves inadequate as well as the risk of loss on new contracts written during the year.

Non-life reserve risk covers the risk of loss arising because the absolute level of claims provision may have been mis-estimated as well as the stochastic nature of future claims payouts, the actual claims will fluctuate around their statistical mean value.

The final parameter used in the standard formula is derived by taking a credibility weighted average of the undertaking specific parameter and the CEIOPS standard factor; performed for each line of business for Premium and Reserve risk separately.

The paper also suggests the credibility weighting to be given to the undertaking specific parameter which is dependent on the number of years of historical data used in the undertaking specific parameter calculation and also whether internal or external data is used.

Revision risk is intended to capture the risk of adverse variation of an annuity arising from an unexpected change to the claims process. CEIOPS proposes a standardised method for calculating company-specific parameters as a shock to revision risk. (Re)insurers are expected to derive their own specific parameters by looking at their data of individual annuities in payment for consecutive years during the period they are subject to revision risk.

CEIOPS has specified statistical estimates to be calculated from this data and used as inputs to the calculations procedure. The prescribed calculation procedure applies statistical fitting techniques to the data and (re)insurers are expected to validate the quality of the fit. Failure to provide satisfactory results in this validation would be sufficient to reject the company-specific parameter request. We believe it would be beneficial for CEIOPS to clarify how it will perform its assessment in this regard.

The calculation of the revision shock (subject to a satisfactory data fit) is carried out using prescribed statistical distributions and multiple simulations to produce a company-specific estimate of the appropriate revision shock.

CP 76 – TECHNICAL PROVISIONS – SIMPLIFIED METHODS AND TECHNIQUES TO CALCULATE TECHNICAL PROVISIONS

Purpose – This paper provides advice on simplified methods and techniques to calculate technical provisions to ensure that actuarial and statistical methodologies are proportionate to the nature, scale and complexity of the risks. The paper follows CP45 which provided guidance on when using simplified methods might be appropriate.

Key Messages

CEIOPS has incorporated some changes suggested by the insurance industry as part of the feedback provided to CP45.

|

We believe that (re)insurers should be able to apply simplified methods even if a full method has been developed, in particular for interim reporting. Full methods could be time-consuming to run as the associated process could be complex. If CEIOPS was to allow this, it is clearly important that a framework be put in place to avoid "cherry-picking", i.e. selecting simplified methods in order to minimise capital rerequirements. |

Detailed Summary

Some changes have been made in line with the responses to CP45, for example, agreeing that there should be no absolute threshold for accepting or rejecting a method, and that in selecting a method, assessment of the proportionality of the method is more appropriate than assessment of model error.

The paper considers in detail those parts of the valuation of technical provisions where the use of simplified methods is particularly relevant. CEIOPS's view is that simplifications should only be used if the amounts involved are immaterial, or there is not sufficient data to do a more accurate calculation, or if performing the full calculations is disproportionately complex and time consuming.

Where data is the issue, (re)insurers should work towards collecting sufficient data so that more accurate methods can be used in future. However, the issue still remains of how to justify that a more accurate method would be disproportionately complex and time consuming – although the paper recognises that for quarterly calculations this might often be the case.

CEIOPS also discusses different areas where simplified methods might be developed in calculating best estimate technical provisions. Many of the suggested simplifications are widely used currently and many (re)insurers would not even deem them to be simplifications.

The simplifications suggested for the calculation of the risk margin are mostly in line with those in QIS4. The paper raises the possibility of an even simpler method, percentage of best estimate, but most (re)insurers are unlikely to be able to justify use of this method.

|

We consider it to be important that all the simplified approaches are re-tested in QIS5 to ensure that they are fit for purpose. |

CP 77 – SCR STANDARD FORMULA – SIMPLIFIED CALCULATIONS IN THE STANDARD FORMULA

Purpose – This paper provides advice for the use of simplified methodologies for the calculation of the SCR standard formula in order to ensure actuarial and statistical methodologies are proportionate to the nature, scale and complexity of the risks. The paper also considers how an assessment of proportionality should be carried out with regards to the calculation of the SCR using the standard formula.

Key Messages

There have been slight changes to the simplifications considered in QIS4 to reflect the new structure or calibration of some risks suggesting that CEIOPS is relatively satisfied with the results produced in QIS4. For some modules CEIOPS considers that simplifications are not required as the approaches set out in the standard formula for these risks should be relatively simple to implement.

|

As for CP76, we consider it important for these approaches to be re-tested in QIS5 to ensure that they are fit for purpose. |

Detailed Summary

Assessment Of Proportionality

This paper primarily focuses on the role of proportionality in the valuation of the SCR standard formula. The main concepts used to assess the nature, scale and complexity of the risks are the same as for the calculation of technical provisions but they should be adapted according to the purpose of the calculation and the scope of the risks i.e. technical provisions are based on an average situation whereas the SCR captures extreme outcomes of the future.

Two steps are given for the process by which to evaluate proportionality in respect of simplified SCR calculations.

1. Assessing The Nature, Scale And Complexity Of The Risks

The assessment of proportionality should be performed on a sub-module by sub-module basis and repeated each time the undertaking would consider another simplified calculation for another sub-module/module.

With increasing complexity and less predictability of risks comes more sophisticated and elaborate tools and this will be a means to assess whether to apply a simplification.

This paper recognises that there are various measures of scale which can be assigned to distinguish between risks in order to identify where the use of a simplified calculation is likely to be appropriate. Undertakings would be expected to use an interpretation of scale which is best suited to their specific circumstances and to their risk profile. CEIOPS supports the idea that the assessment of proportionality should ideally be more qualitative than quantitative.

2. Assessment Of Whether The Application Of A Particular Simplification Is Proportionate

In this step the insurer should assess whether a specific simplification can be regarded as proportionate to the nature, scale and complexity of the risks analysed in the first step. Further, the insurer should assess the degree of model error that results from the use of a given simplification. The simplification should be regarded as proportionate if the model error is expected to be immaterial.

CEIOPS proposes using, as a reference, the definition of materiality used in International Accounting Standards (IAS), i.e. "information is material if its omission or misstatement could influence the economic decisions of users...".

CEIOPS recognises that a practical assessment of the model error will not be easy and comments that undertakings should not be required to quantify the degree of model error in precise quantitative terms but instead demonstrate with reasonable assurance that the model error implied by the application of the simplified method is immaterial.

|

If both the standard formula and the simplified calculation turn out to be proportionate, the standard formula should be chosen. Likewise, where several simplifications turn out to be proportionate, the insurer should generally apply the simplification which is likely to include the smallest degree of model error. |

Simplification In QIS4 Under The Standard Formula

The Level 1 text does not envisage an approval process for the use of simplifications to the standard formula. In addition to the general definition of proportionality, the implementing measures could state proportionality requirements specific to certain simplifications.

CEIOPS provides a definition of the simplification methods to be used taking into account the approach used for QIS4. We note:

- no simplification calculations are foreseen for the interest rate, equity, currency, spread (with the exception of bond risk), property and concentration risk modules;

- QIS4 simplifications could be used for life underwriting risks but recalibrated to consider the proposed levels for the different stresses given in CP49;

- new simplifications have been introduced for health underwriting risks since the structure of this module has been changed compared to QIS4; and

- we expect CEIOPS to provide advice on the standardised scenarios for non-life catastrophe risk at a later date while no simplification is foreseen for premium and reserve risk.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.