- in Asia

1. EXECUTIVE SUMMARY

A Financial Reporting Council report, published in October 2009, contains the following:

"Addressing the requirements of the FRSSE, UK GAAP, IFRS, CA2006 and the Listing Rules that apply to a company may lead it to address going concern and liquidity risk in different sections of its annual report and financial statements. This may create difficulties ... in seeking to obtain a clear, comprehensive and cohesive understanding of the issues facing the company".

The main adjectives therein probably represent an unintended alliteration by the FRC and it is regrettable that overused adjective "dysfunctional" is missing. That's because dysfunctional is a good way to describe the competing disclosure regimes applying to the front half of companies' annual reports.

Despite this, companies have performed better in 2009 than in 2008 in meeting the disclosure demands. That's the main message from this 2009 annual Deloitte survey looking at what companies report in the narrative sections, that is the parts outwith the audited financial statements, of their annual reports. As with 2008, the population of listed companies is split into two categories, being investment trusts which make up 40% of listed companies (38% in 2008) and other companies. The findings on investment trusts are reported in section 13 while the results for other companies are reported in sections 4 to 12.

The main findings for companies other than investment trusts are:

- the length of the annual report has increased by 3% compared with 2008 and by 41% compared with 2005. There are no signs of recession here. The hope that 2008 was a plateau has been proven unfounded. While some companies have taken the option to publish some information on their websites rather than in the annual report, this has not compensated for the need to say more to meet the disclosure requirements and to tell how companies have performed in the choppy economic conditions in 2008/9;

- 62% of those companies, which reported after the November 2008 FRC Update on going concern and liquidity risk was published, clearly took on board voluntarily the guidance therein. They provided on average 253 words on going concern matters;

- nine companies (2008: five) had received modified audit reports, seven (2008: four) of which related to group going concern. Another one related to a subsidiary going into administration post year-end;

- three areas saw dramatic increases compared with 2008: 83% (2008: 47%) discussed their capital structure and financing; 68% (2008: 48%) discussed treasury policies and 47% (2008: 22%) discussed their current and prospective liquidity. In some cases companies were merely reassuring the market about the strength of their financial position. For about a third of companies, relative weaknesses or uncertainties related to their going concern and liquidity positions were discussed;

- 96% of companies (2008: 89%) clearly described their principal risks and uncertainties. Companies disclosed eight risks on average, with one FTSE 350 company identifying 30. The state of the economy was the most commonly noted risk;

- 84% of companies (2008: 77%) identified clearly their key performance indicators. The average number of KPIs per company was eight, of which five were financial in nature and three were non-financial. While these statistics are strong, companies' performance in explaining the KPIs selected and their link with strategy was relatively poor, with less than half doing so;

- 35% (2008: 30%) of companies complied fully with the provisions of the Combined Code on corporate governance, the remainder using the facility to explain the areas in which they had not complied. The results demonstrated the relative burden of the Code on smaller listed companies, with only 18% complying in full; and

- only four out of 100 companies (2008: five) claimed that they had complied with the ASB's Reporting Statement on operating and financial reviews.

The ASB has announced that it is carrying out a survey of narrative reporting in 2009, following up on the survey which it did a couple of years ago. The results of this Deloitte survey suggest that the ASB needs to take action to withdraw its Reporting Statement and to consider issuing a document which tackles the dysfunctional disclosures and provides companies with a complete and logically ordered guide to narrative reporting.

2. REGULATORY OVERVIEW

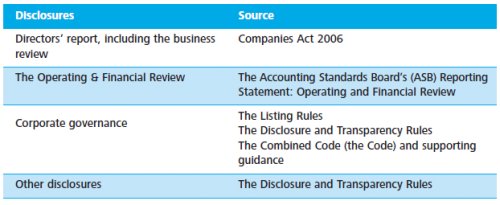

Narrative reporting by UK listed companies is subject to a complex tapestry of requirements, which has evolved significantly over the last couple of years and will continue to do so for the foreseeable future. This section provides an overview of the regulations and guidance which shape some of the "front half" of annual reports, being:

Also discussed here are directors' liability and changes that may be made to the narrative disclosure regime in the foreseeable future. It excludes the directors' remuneration report, the regulatory requirements for which are covered in the separate Deloitte publication, 'Know the ropes – the remuneration committee knowledge'.

Directors' Report, Including The Business Review

The general requirement to produce a directors' report is contained in section 415 of the Companies Act 2006.

All quoted and unquoted companies (except those qualifying as small) are required to include a business review in their directors' report. This includes subsidiary companies which do not qualify as small, even if they are wholly-owned. The purpose of the business review is to inform members of the company and help them assess how the directors have performed their duty to promote the success of the company.

Under section 417, a business review should include a fair review of the company's business and a description of the principal risks and uncertainties facing the company. The review required is a balanced and comprehensive analysis, consistent with the size and complexity of the business, of:

- the development and performance of the business of the company during the financial year; and

- the position of the company at the end of the year.

The requirements include, to the extent necessary for an understanding of the development, performance or position of the business of the company:

- an analysis using financial key performance indicators (KPIs); and

- where appropriate, analysis using other KPIs, including information relating to environmental matters and employee matters.

In practice the interpretation of "necessary" and "appropriate" varies greatly depending on the size and nature of the company's business.

In addition, a quoted company's business review must disclose:

- the main trends and factors likely to affect the future development, performance and position of the company's business;

- information about:

-

- environmental matters (including the impact of the company's business on the environment);

- the company's employees; and

- social and community issues,

- including information about any policies of the company in relation to those matters and the effectiveness of those policies; and

- information about persons with whom the company has contractual or other arrangements which are essential to the business of the company. Disclosure about a person is not required if the disclosure would, in the opinion of the directors, be seriously prejudicial to that person and contrary to the public interest.

Although the above disclosures need to be included only "to the extent necessary" for an understanding of the business, a company not discussing each of the specific areas in the second and third bullets above has to state expressly that it has not done so.

Companies are not required to disclose information about impending developments or matters in the course of negotiation if the disclosure would, in the opinion of the directors, be seriously prejudicial to the interests of the company.

The exemption from disclosing information about persons with whom the company has contractual arrangements is somewhat different – disclosure of information about such a person may only be omitted if it would be seriously prejudicial to that person and contrary to the public interest. Non-disclosure is not permitted simply because it would be prejudicial to the company.

Compliance with the statutory requirements of the business review is analysed in sections 6, 7 and 8 of this publication.

The Operating And Financial Review

The ASB's 'Reporting Statement: Operating and Financial Review' (RS) sets out best practice principles and guidelines, for a narrative report on operating and financial matters.

The statement was originally issued in 1993 and subsequently revised in 2003 and 2006. While the Government had been planning to make compliance with the ASB statement mandatory in 2005, this did not happen and thus adherence to the ASB Statement has remained voluntary throughout its existence.

If a narrative report is called an 'Operating and Financial Review' (OFR) there is an expectation that directors will have followed the ASB's guidance and if this is not the case it would be useful to give the narrative report a different name, such as a 'Business Review'. In practice, as discussed in section 12 of this publication, only a handful of companies included in the survey called their narrative report an OFR or stated compliance with the RS. This publication refers to 'OFR-style information' which includes both formal OFRs and where companies have covered many of the items recommended by the RS within their chairman's and/or chief executive's statement, business review and financial review.

Corporate Governance Disclosures

Corporate Governance Statements – The Combined Code And Listing Rules

Listed companies are required by the Listing Rules to make certain disclosures about corporate governance in their annual reports. At the heart of this requirement is the Code. A listed company incorporated in the UK is required to make a statement about how it has applied the main principles in the Code and a statement of compliance with the Code. The Code is supported by additional guidance on internal controls (the 'Turnbull Guidance') and audit committees (the 'Smith Guidance').

In addition, the Listing Rules state that there should be a statement by the directors that the business is a going concern with supporting assumptions or qualifications as necessary. These requirements are discussed in more detail in sections 9 to 11 of this publication.

An updated Combined Code was issued in June 2008 which applies to accounting periods beginning on or after 29 June 2008. In practice this means that most companies will begin to apply the 2008 Code in 2009 and will report against its requirements for the first time in 2010.

The updated version includes two amendments to the 2006 Code:

- to remove the restriction on an individual chairing more than one FTSE 100 company; and

- to allow the chairman of a smaller listed company (outside the FTSE 350) to be a member of the audit committee where he or she was considered independent on appointment.

Corporate Governance Statements – The DTR

Following amendments to the EU Fourth, Seventh and Eighth Directives, the Financial Services Authority (FSA) has introduced new rules into the Disclosure and Transparency Rules (DTR) on corporate governance statements and audit committees. These rules apply to all UK companies, which have shares and/or debt admitted to trading on a regulated market in the EU, for periods commencing on or after 29 June 2008.

Listed companies will have to include a corporate governance statement in their directors' report referring to:

- the corporate governance code that the company has decided to apply or is subject to under the law of the Member State in which it is incorporated (the Combined Code in the UK);

- an explanation as to whether, and to what extent the company complies with that code. To the extent that a company departs from the code, the company should explain the parts of the code from which it has departed and the reasons for doing so;

- a description of the main features of the company's internal control and risk management systems in relation to the financial reporting process;

- major shareholdings and related matters already required by the Takeover Directive; and

- a description of the composition and operation of the company's administrative, management and supervisory bodies and their committees.

For companies complying in full with the relevant provisions of the 2008 Code, many of these disclosures will already be in place. What is new are the requirements to provide the information in a dedicated 'corporate governance statement' and to provide a description of the main features of the company's internal control and risk management systems.

A company may elect that, instead of including its corporate governance statement in its directors' report, the information required may be set out:

- in a separate report published together with and in the same manner as its annual report; or

- by means of a reference in its directors' report to where such a document is publicly available on the company's website.

Audit Committees

Under the new DTR 7.2, companies whose securities are traded on a regulated market in the EU are also required to have a body, such as an audit committee, which is responsible for performing the functions detailed below. At least one member of that body must be independent and at least one member must have competence in accounting and/or auditing. The requirements may be satisfied by the same member or by different members of the relevant body.

The company must ensure that, as a minimum, the relevant body should:

- monitor the financial reporting process;

- review and monitor the independence of the statutory auditor and in particular the provision of additional services to the company;

- monitor the effectiveness of the company's internal control, internal audit function where applicable and risk management systems; and

- monitor the statutory audit of the annual and consolidated accounts.

The company must make a statement available to the public disclosing which body carries out the functions above and how it is composed. This statement can be included in any corporate governance statement.

The Smith Guidance

In October 2008 the Financial Reporting Council (FRC) issued a new edition of the Smith Guidance on audit committees. The report includes the following new recommendations that the audit committee:

- explains to shareholders in the audit committee report how it reached its recommendation to the board on the appointment, re-appointment or removal of the external auditors;

- considers whether there might be any benefit in using firms from more than one network; and

- considers the need to include the risk of the withdrawal of their auditor from the market in their risk evaluation and planning.

The explanation to shareholders on how the audit committee reached its recommendation to the board on the appointment, re-appointment or removal of the external auditors should normally include supporting information on tendering frequency, the tenure of the incumbent auditor, and any contractual obligations that acted to restrict the audit committee's choice of external auditors.

Companies were invited to adopt the best practice guidance with immediate effect, but the recommendations on disclosure are only intended to apply to reports covering operating periods ending on or after 30 June 2009. This means that they take effect at the same time as new disclosure requirements contained in the revised Code and the DTR corporate governance rules discussed above.

Other Disclosures

UK companies with shares and/or debt admitted to trading on a regulated market also have to comply with the requirements on periodic financial reporting in the DTR issued by the FSA. These rules replace some of the Listing Rules for such periods and are derived from the EU Transparency Obligations Directive. The DTR require most listed companies to prepare an annual management report. With one minor exception, these requirements duplicate the existing requirements within UK law for the directors' report.

The requirements of DTR 4.1 for the annual report include a 'responsibility statement'. This is in force for annual periods beginning on or after 20 January 2007. ISA (UK and Ireland) 700 (revised), which is applicable for periods commencing on or after 6 April 2008 and ending on or after 5 April 2009, requires that the audit report contain a 'statement that those charged with governance are responsible for the preparation of the financial statements'. Whilst this is not as strict as the previous ISA, which required that either the annual report or the audit report contain a description of those responsibilities, all of APB's examples refer to a separate Directors' Responsibilities Statement. The APB has not provided an example of a statement for a public company, but market practice has generally been to continue preparing a similar statement to that used in previous years, combined with the statement required by DTR 4.1. This is presumably driven by a concern that removing the statement required under the old ISA could imply that directors were taking less responsibility for the accounts and reports.

The responsibility statement required by the DTR must be made by the person(s) responsible within the company. This is usually the directors, but it is up to each company to decide which person(s) is (are) considered responsible. The responsibility statement must include the name and function of the person making the statement. Only one person is required physically to sign the responsibility statement.

Each person making a responsibility statement must confirm that to the best of his or her knowledge:

- the financial statements, prepared in accordance with the applicable set of accounting standards, give a true and fair view of the assets, liabilities, financial position and profit or loss of the company and the undertakings included in the consolidation taken as a whole; and

- the management report (the DTR term to describe the narrative part of the annual report) includes a fair review of the development and performance of the business and of the position of the company and the undertakings included in the consolidation taken as a whole, together with a description of the principal risks and uncertainties that they face.

The responsibility statement is discussed in more detail in section 6 of this publication.

Directors' Liability For Disclosures

Section 463 of the Companies Act 2006 provides a level of protection for directors in respect of certain statements. It was introduced to encourage directors to provide more meaningful disclosures, particularly relating to the future. Under section 463, a director may be held liable only to the company itself (although existing civil or criminal offences are unchanged) and not to individual shareholders or third parties. Such liability to the company would exist only if the director knowingly made a statement that was untrue or misleading, or was reckless as to whether this was the case. For an omission from the directors' report, liability would arise only if he or she knew that the omission was 'dishonest concealment of a material fact'.

This protection extends only to the directors' report and directors' remuneration report and any summary financial statement derived from those reports. Statements made outside these reports, such as within an OFR or corporate governance statement (whether under the Listing Rules or DTR 7.2), are not protected unless the OFR or other relevant statement has been scoped into the directors' report by means of a clear cross reference.

On The Horizon

This section provides an overview of the latest developments which will impact narrative reporting next year and beyond.

Review Of The Combined Code

At the beginning of 2009 the FRC announced another review of the impact of the 2008 Combined Code on Corporate Governance. Views were invited on the following questions:

- Which parts of the Code have worked well? Do any of them need further reinforcement?

- Have any parts of the Code inadvertently reduced the effectiveness of the board?

- Are there any aspects of good governance practice not currently addressed by the Code or its related guidance that should be?

- Is the 'comply or explain' mechanism operating effectively and, if not, how might its operation be improved?

In addition Sir David Walker was asked by the Chancellor of the Exchequer to review the corporate governance arrangements of the UK banking industry. The terms of reference for this review included consideration of the following areas:

- the effectiveness of risk management at board level including the incentive in remuneration policy to manage risk effectively;

- the balance of skills, experience and independence required on the boards of UK banking institutions;

- the effectiveness of board practices and the performance of audit, risk, remuneration and nomination committees; and

- whether the UK approach is consistent with international practice and how national and international best practice can be promulgated.

Sir David published his proposed recommendations in July 2009 and invited comment on these by 1 October. These will seek to address weaknesses in risk management, board quality and practice, control of remuneration and the exercise of ownership rights. Sir David's intention is to issue final recommendations in November 2009.

The FRC issued in July 2009 a progress report on its review of the Combined Code, which summarised the responses to the initial consultation paper, of which there were over 100, identified the areas of the Code the FRC may consider updating and cross-referred those areas to the relevant recommendations contained in the Walker Review consultation document. In particular the FRC is seeking views during the same period to October 2009 on whether the Walker Review recommendations should extend to all non-financial listed companies or some sub-set of those. The FRC aims to publish its final report, and begin consultation on whatever changes may be proposed to the Combined Code, before the end of the year. Subject to the outcome of that consultation, a revised Code would take effect in mid-2010.

Going Concern

In November 2008 the FRC published an Update for directors of listed companies: going concern and liquidity risk. The Update brought together the requirements on directors to comment on going concern and liquidity in annual reports and accounts, in the light of the significant economic difficulties that were being experienced in the latter half of 2008.

However, its status was that of guidance and it did not replace the formal 1994 Guidance on going concern to which reference is currently made in the Listing Rules. Section 11 of this publication considers how companies have adopted the Update's recommendations.

In October 2009 the FRC published updated guidance for directors of UK companies for implementation for periods ending on or after 31 December 2009. It is expected that the FSA will take the necessary steps to replace the 1994 Guidance with the 2009 Guidance to meet this timetable.

The updated guidance brings together the Update published in November 2008 and the 1994 Guidance and draws on the experience gained in the first half of 2009. The format and style of the updated guidance is significantly different to the 1994 guidance. It follows the same practical approach to making a going concern assessment but seeks more disclosures. The FRC believes that its impact will be to support directors making high quality assessments of going concern and providing effective disclosures without increasing the costs for companies or users of financial statements.

IASB Exposure Draft 'Management Commentary' And The ASB's Review Of Narrative Reporting

This exposure draft presents the International Accounting Standards Board's (IASB) proposals for a broad framework for the preparation and presentation of management commentary to accompany financial statements in accordance with International Financial Reporting Standards (IFRSs). The IASB makes it clear that it is for the management of an entity to decide how best to apply this framework in the particular circumstances of its business. The Board's proposals are intended to provide a basis for the development of good management commentary. It offers a non-binding framework which could be adapted to the legal and economic circumstances of individual jurisdictions. The guidance has been developed to apply to publicly traded entities.

The IASB's ED is similar in content and proposed status to the ASB's RS. The ASB carried out a review of narrative reporting in 2007 and is planning to issue a further report in 2009.

3. SURVEY OBJECTIVES

The main objectives of the survey were to discover:

- what narrative reporting listed companies have provided in their annual reports;

- how disclosures varied depending on the size of the company;

- how companies met the requirements of the Companies Act 2006 to provide a business review within the directors' report;

- to what extent companies have adopted the recommendations in the ASB's best practice RS; and

- how the results compared with similar surveys performed in previous years.

The annual reports of 130 listed companies were surveyed to determine current practice. Consistent with the approach adopted in Deloitte's 2008 survey, the companies were split into two groups being 30 investment trusts and 100 other companies. Investment trusts are those companies classified by the London Stock Exchange as non-equity or equity investment instruments (this excludes real estate investment trusts). They have been treated as a separate population due to their specialised nature and the particular needs of their investors.

The sample is, as far as possible, consistent with that used in last year's survey. As a result of takeovers and mergers over the last twelve months, the sample could not be identical. Replacements and additional reports were selected evenly and at random from three categories being those within the top 350 companies by market capitalisation at 30 June 2009, those in the smallest 350 by market capitalisation, and those that fall in between those categories (the 'middle' group).

The annual reports used were those most recently available and published in the period from 1 August 2008 to 31 July 2009.

Consistent with last year, the scope of the survey included a review of corporate governance statements in annual reports against the provisions of the 2006 Code. It seemed timely to understand in more detail how companies are performing in this area as the new regulatory requirements under the DTR came into force for periods commencing on or after 29 June 2008.

As noted above the findings for investment trusts are analysed separately within this publication. Sections 4 to 12 summarise the results for the 100 companies excluding investment trusts and section 13 reviews the 30 investment trusts.

The disclosures in the directors' remuneration report are not covered in this publication but are studied in the Deloitte publication Executive directors' remuneration published in September 2009.

4. OVERVIEW OF THE ANNUAL REPORT*

|

Length Of Annual Report

The trend noted over recent years has continued in 2009, with the overall length of annual reports increasing to an average of 99 pages (2008: 96), an increase of 3%. The largest increase is seen in the top 350 companies (up 5% on prior year) whereas the length of the smallest companies' annual reports has remained flat at 64 pages. It is perhaps surprising that annual reports have increased in length given that some companies have sought to make the reports shorter or at least less glossy to save costs and that some are now opting to put information on their websites e.g. environmental information which might hitherto have been included in their annual reports. On the other hand, there have been some additional disclosure requirements in 2008 and 2009 and the current economic climate and its effect on companies' results will have warranted further explanations.

Over the four year period since the 2005 survey, the average length of reports has grown by 41% from 70 to 99 pages. The most significant increases in length are seen in the middle group of companies whose reports have increased by 46% since 2005, from an average of 57 to 83 pages. Length of reports for the smallest 350 companies has increased from 47 to 64 pages and the top 350 companies from 108 to 147 pages.

The longest report was 469 pages (2008: 473) and the shortest was 32 pages in length (2008: 30).

Figure 1. What Is The Overall Length Of The Annual Report?

Balance Of Narrative And Financial Reporting

For the purposes of this survey the 'narrative' section or 'front half' of the annual report is defined as all the pages in the annual report excluding the audited financial statements. The 'narrative' reporting typically includes some or all of the following sections:

- Chairman's statement.

- Chief executive's statement.

- Business review.

- Financial review.

- Corporate social responsibility statement (CSR).

- Directors' report.

- Corporate governance statement.

- Directors' remuneration report.

- Statement of directors' responsibilities.

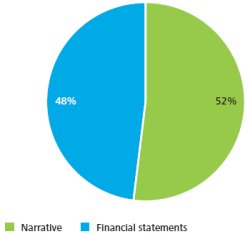

The balance of narrative versus financial statements as a proportion of the total annual report has shifted slightly from the prior year. As shown in figure 2, below, financial statements now represent on average 2% more of the total report than last year at 48% (2008: 46%). The overall shift is to an increase in length of the financial statements. The larger companies continue to devote more of the report to narrative information than the middle and smaller companies, with total narrative of 56%, 50% and 45% respectively (2008: 59%, 51% and 47% respectively). The relative decline between 2008 and 2009 may be due to the factors referred to above regarding information being moved to company websites or separate reports.

Figure 2. What Is The Balance Of Narrative And Financial Reporting In The Annual Report?

Speed Of Reporting

The DTR require that the annual report, which includes the audited financial statements, a management report and the responsibility statement, is published within four months of the end of the financial year. This is a significantly shorter deadline than the six months allowed under the previous Listing Rules.

All companies included in the survey are required to comply with the DTR requirement to publish their annual report within four months of their year-end. The potential impact of not complying with this rule is the suspension of shares.

Overall compliance with this requirement was good, with 99 companies meeting the deadline. The company which missed the deadline announced its preliminary, unaudited results within four months, but took 141 days to approve its financial statements.

During this period administrators were appointed to two of its subsidiaries and a company voluntary arrangement was entered into.

Of the 99 companies, 59 approved their financial statements within 75 days, 21 within 76 to 90 days and the remaining 19 companies over 90 days. Despite fewer companies reporting within 75 days (2008: 61 companies), there was an overall improvement in speed of reporting on prior year with only 20% of companies reporting after 90 days (2008: 25%) and the average number of days falling from 78 to 75.

Figure 3. How Quickly Was The Annual Report Approved In 2009?

The largest companies were the quickest reporters, with 91% reporting within 75 days and the remaining 9% within 90 days, which is consistent with last year. Middle-sized companies were quicker than last year with only 12% reporting after 90 days (2008: 18%). The smallest companies remain the slowest reporters, with 48% reporting after 90 days, albeit an improvement on 2008 where 58% reported in that timeframe.

Presentation

Many companies invested in producing glossy annual reports. 89% of companies presented their annual reports in a manner which was visually interesting. The appeal of a report is a subjective assessment. However some of the criteria used to determine whether a report was well presented were structure of report, clear headings and use of colour, pictures, tables and charts.

5. SUMMARY INFORMATION*

|

As the disclosure requirements within narrative reporting increase and the length of annual reports follow suit, it is no surprise that so many companies include a summary page at the front of the annual report. The inclusion of a summary page is optional and not a regulatory requirement.

Overall 89% of companies (2008: 85%) presented a summary page at the front of their annual report. All of the top 350 companies included a summary page (2008: 94%) compared to 94% of middle-sized companies (2008: 97%) and only 73% of the smallest companies (2008: 64%). The smaller companies tended to have simpler structures and shorter reports, indicating that there is less need for a summary report.

Figure 4. How Many Annual Reports Include A Summary Information Page?

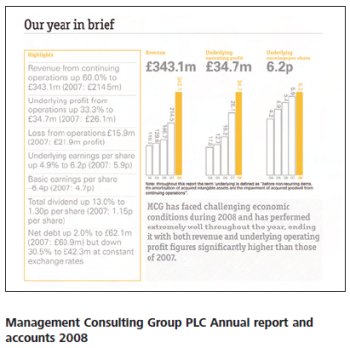

The benefits of providing a summary page include being able to draw to the user's attention the key statistics and developments in the period to support the narrative discussion that follows. A good example of this is Management Consulting Group PLC which presents key financial information in tabular format, alongside graphs with several years of comparatives and a summary performance statement.

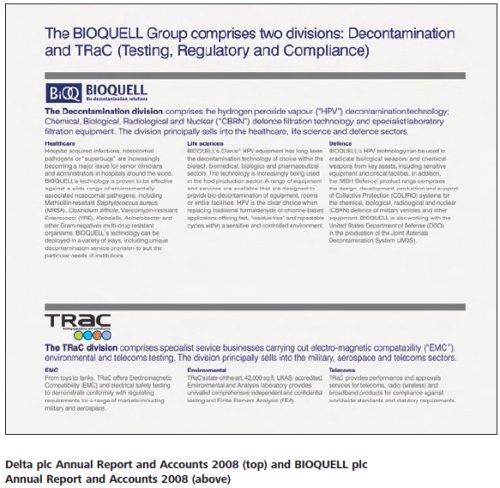

Some companies also use the summary page to provide information about the structure and business of the organisation, thus portraying either graphically or simply in summary what would otherwise occupy further discussion in the business review. Good examples of these are Delta plc and BIOQUELL plc which present information about their divisions in alternative ways.

Other companies use the summary page as a way of setting the scene by explaining who the company is, what they do, what their strategy is and the key highlights from the financial year. A good example of this is Zotefoams plc.

Information Shown On The Summary Page

As demonstrated in the examples above, the different approaches to a summary page result in a variety of information being given prominence at the start of the report. Of the companies including a summary page, 90% included narrative on the page (2008: 80%). Such narrative covered various topics, including strategic mission statements, an overview of the group's business, and highlights of performance and developments during the period.

89% of companies provided financial information (2008: 91%). 79% of companies with a summary page provided both narrative and financial information.

Figure 5. What Type Of Information Is Shown On The Summary Page?

6. THE BUSINESS REVIEW*

|

Since 1 April 2005, all quoted and unquoted companies (except those qualifying as small) have been required by section 417 of the 2006 Companies Act to include a business review in their directors' report. The review should include a fair review of the business and a description of the principal risks and uncertainties facing the company and contain a balanced and comprehensive analysis of:

- the development and performance of the business of the company during the financial year; and

- the position of the company at the end of that year.

Other requirements are discussed further below.

All companies except one identified the narrative which met the definition of a business review. The one exception had clearly complied with all the business review requirements within a very extensive directors' report but had not clearly identified any particular sections as fulfilling the business review criteria.

Figure 6. Where Is The Business Review Positioned?

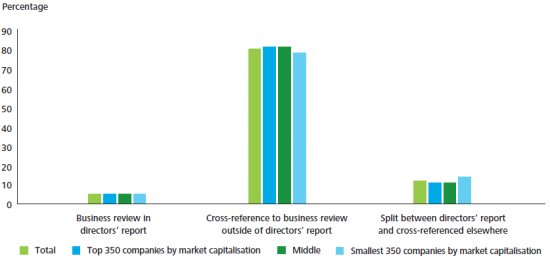

Location Of Business Review

The law requires the business review to be part of the directors' report. The most common way of fulfilling this obligation across all sizes of companies was to prepare a separate business review outside the directors' report and then scope it clearly into the directors' report via a cross reference. 81% of companies did this. The reference to the business review in the directors' report was often cross-referenced to the individual reviews of the chairman, chief executive and other financial and operating reviews.

13% of companies both cross-referenced to narrative outside the directors' report and also included some of the business review requirements within the directors' report. Only 6% of companies across all size groups presented their complete business review within the directors' report.

An example of a clear cross-reference in the directors' report is shown below in an extract from the Annual Report of PayPoint plc.

The inclusion of a formal OFR remains voluntary. 11 companies provided a narrative section titled "Operating and Financial Review", a surprising increase on last year where only nine companies did so. In 2009, nine companies included the OFR within their business review, which consisted of the OFR and other narrative statements cross-referenced from the directors' report. One company defined their business review through cross-reference in the directors' report to the OFR and the financial statements. The remaining company chose to label the majority of the narrative (including the OFR) as the directors' report without specifically defining any text as the business review. All requirements of the business review were met by this company. OFR-style information is discussed further in section 12.

Principal Risks And Uncertainties

96 companies clearly disclosed their principal risks and uncertainties. Principal risks and uncertainties are discussed further in section 7.

Key Performance Indicators

The Companies Act requires a business review to include, if considered necessary, an analysis using financial and non-financial KPIs. 84 companies identified KPIs with the majority of companies locating the discussion of KPIs in their business review presented separately from the directors' report but scoped into it via a cross-reference. KPIs are discussed further in section 8.

Development And Performance Of The Business

99% of companies provided a review of the business within the narrative identified as the business review. One company had included a cross-reference from the directors' report to both the financial statements and the OFR to fulfil the business review requirements. However the brevity of the OFR, being only four sentences in length, and lack of discussion in the financial statements resulted in the conclusion that a review of the business had not been provided.

Of those companies providing a review of the business, 99% provided a fair review. The one company which was considered not to provide a fair review had failed to mention the group's overall significant loss for the period, driven by discontinued operations. Instead, the review concentrated solely on the profitable continuing operations. Similarly, the business review made a fleeting mention of the large negative retained earnings when it confirmed no dividends would be proposed, but did not expand on this when discussing the year end position of the company or future strategy.

93% of companies included an analysis of the development and performance of the company during the year. All of the seven companies which did not clearly discuss performance during the year were within the smallest 350 companies. These companies focused solely on the year end position without commenting on factors during the year.

The 2006 Act strengthened the requirements regarding both non-financial and forward-looking information in the business review. In addition to the existing provisions, a quoted company's review must disclose the main trends and factors likely to affect the future development, performance and position of the company's business.

93% of companies included information on the trends and factors likely to affect the future development, performance and position of the business within the business review. Of the seven companies which did not, three had this information in the chairman's statement which had not been cross-referenced into the defined business review. The four remaining companies did not clearly discuss future trends and factors that would affect the business at all.

Balanced Review

8% of companies did not contain any negative comments within their business review, bringing into question whether the review met the criteria of being balanced. Three quarters of these were in the top 350 companies. Most acknowledged the troubled economic environment but failed to specify what, if any, effect this had had on the company. This is a key feature of the business review that the Financial Reporting Review Panel (FRRP) has said it will be taking into account when reviewing annual reports and deciding whether to raise a question on the business review.

Corporate And Social Responsibility

The Companies Act 2006 requires companies to discuss additional information about:

- environmental matters (including the impact of the company's business on the environment);

- the company's employees; and

- social and community issues,

including information about any policies of the company in relation to those matters and the effectiveness of those policies to the extent necessary for an understanding of the business. A company not discussing each of the specific areas above has to state expressly that it has not done so.

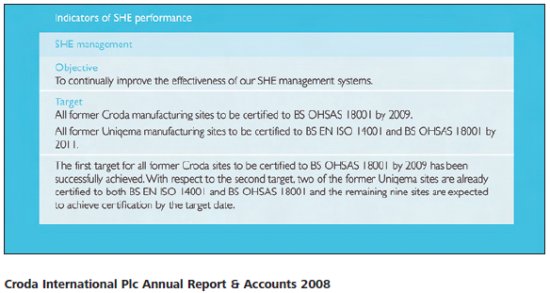

Overall the disclosure around the environment, employees and social and community issues has not improved significantly on last year. The most helpful information provided in any area was by companies who clearly identified and set out their policies and discussed future targets or related non-financial KPIs alongside the policies. An example of clearly set out key principles underpinning the company's policy, complemented by corresponding KPIs is from Croda International Plc, right.

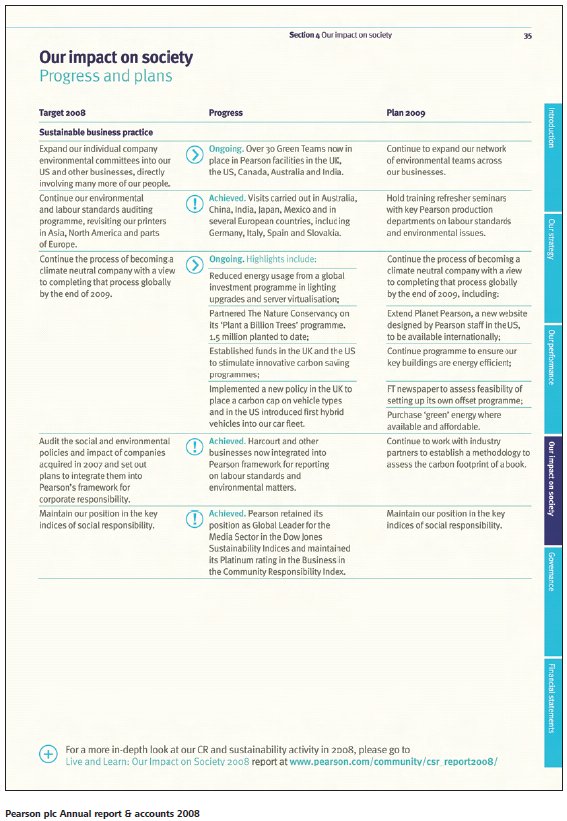

Other useful ways to present policies and their effectiveness is in tabular format, an approach adopted by Pearson plc, shown below.

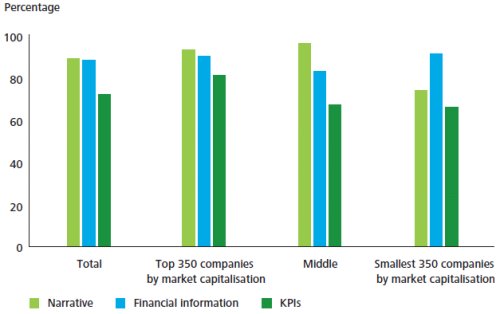

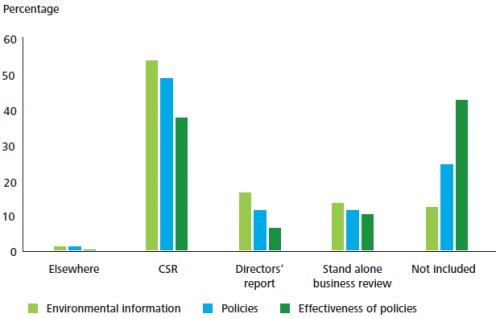

Environment

Overall 87 companies included some information on their response to environmental matters. The most common location for the discussion of environmental factors across all sizes of company is the corporate and social responsibility (CSR) statement, with 54 companies including information therein. Over a third of these companies included their CSR statement within the business review. 17 companies provided detail directly in the directors' report and 14 incorporated these comments in their stand alone business review without titling them 'CSR'. Many companies produce separate CSR reports, in addition to their annual reports, which tend to be available on the companies' websites; these have not been taken into account for the purposes of this survey.

Companies were less clear about specific environmental policies, with only 75 companies disclosing details around such policies. Of these, only 57 went on to provide details about the effectiveness of such policies. Common policies related to the ISO 14001 accreditation which is internationally recognised. Other popular environmental policies adopted include reduction in energy usage and waste output.

The smallest companies within the sample were noticeably weaker at disclosing information around environmental issues than their larger counterparts. While 73% of the smallest 350 companies provided some information, only 45% described their policies and 27% disclosed the effectiveness of such policies.

Figure 7. Where Is Information On The Environment Shown In The Annual Report?

Wm Morrison Supermarkets PLC is a good example of clear disclosure in this area. An extract from the Annual report and financial statements 2009 highlighting environmental policies and the effectiveness of such policies, shown right.

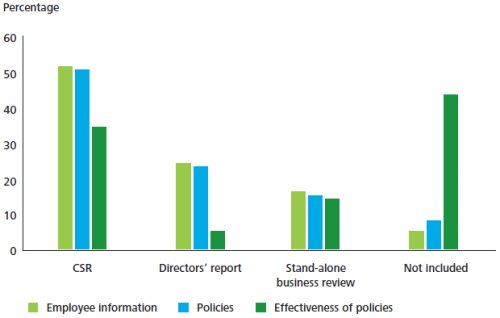

Employees

Five companies in the sample do not have any employees. All of these companies' principal activity is investment in either property or mortgage-backed securities, although they do not meet the definition of an Investment Trust (Investment Trusts are discussed in section 13). Of the remaining 95 companies, 94% provided some information around employees. Again, it was most common to include such information in the CSR statement (52%) with 25% choosing to disclose relevant information directly in the directors' report and 17% in the stand-alone business review.

Companies were strong at including discussion around employee policies, with 91% of companies with employees doing so. However, detail of the effectiveness of such policies was lacking with only 56% of companies providing this information. Any information provided under the Companies Act requirement to disclose detail concerning disabled employees was not taken into account for the purpose of these questions.

Again it was the smallest companies who were weakest at providing details of policies (77% of the smallest 350) and the effectiveness of policies (26%).

Figure 8. Where Is Employee Information Shown In The Annual Report?

Compass Group PLC is a good example of describing clearly the importance of employees and relevant policies in place.

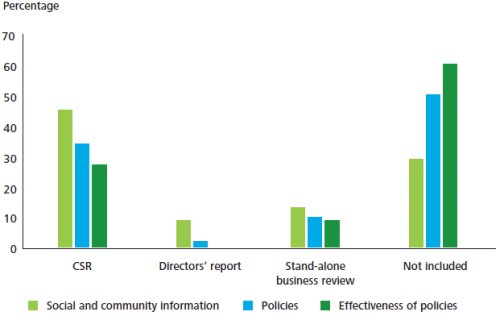

Social And Community Issues

This was the weakest area of disclosure across all companies. All of the top 350 companies provided information around social and community issues, but the middle group and smallest 350 companies struggled, with only 67% and 42% complying respectively. Overall compliance with providing general information was 70%, an improvement on 64% from 2008.

As with the other disclosures, it was most common to include this information in the CSR statement with 46% of companies doing so. 14% disclosed information within the stand-alone business review and 10% directly within the directors' report.

Less than half of the total sample detailed policies in this area, with 51% of companies not providing any detail at all (2008: 46%). Similarly, only 39% of companies (2008: 48%) discussed the effectiveness of policies in place.

Again it was the smallest companies whose disclosure in this area was considerably weaker than other companies. Only 42% provided any information at all, 15% disclosed their policies but only 12% discussed the effectiveness of such policies. Clearly these areas are proving burdensome for the smallest companies.

Figure 9. Where Are Social And Community Issues Discussed In The Annual Report?

A good example of furthering the reader's understanding of the business through describing relevant social and community activities is Punch Taverns plc.

There were 31 companies which did not disclose any detail about one or more of the above three issues. Of these, only two companies stated that they had not done so.

Contractual Arrangements

A further stipulation of the Companies Act 2006 is to include information about persons with whom the company has contractual or other arrangements which are essential to the business of the company.

Thirteen companies disclosed persons with whom the company has contractual or other arrangements which are essential to the business of the company and ten confirmed that there were none to disclose. Of the total 23, ten were from the top 350 companies, nine from the middle group and the remaining four from the smallest 350. Although this is an increase on 2008 where only 15 companies disclosed specific information about contractual and other arrangements, the level of compliance with this legal requirement seems very low. A possible reason for non-compliance is that the Companies Act caveats the requirement, stating that disclosure should only be made to the extent necessary for an understanding of the business and where such disclosure would not be seriously prejudicial to the interests of the person and contrary to the public interest. However, if a company does not make the disclosure, the Companies Act requires the company to state expressly that it has not done so.

A good example of clear disclosure in this area is taken from Goldshield Group plc's Annual Report 2009.

Section 12 of this report discusses the dependency disclosure set out in the RS which is a broader but not necessarily overlapping disclosure with the specific Companies Act requirement discussed above.

DTR Responsibility Statement

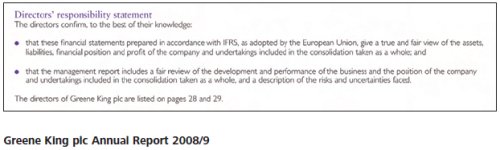

The DTR requirement for directors to provide a responsibility statement is now effective for all companies within the sample. It was met by 86% of companies, a significant increase on 2008 (54% of eligible companies). Two non-compliant companies were in the top 350 group, six were from the middle group and six from the smallest 350 companies. An example of the responsibility statement taken from Greene King plc's Annual Report is shown left.

* This section analyses the findings for all companies other than investment trusts

To read this Report in full please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.