- with readers working within the Business & Consumer Services industries

On 27th July 2018, the PRA published its Consultation Paper (CP) 17/18 on Credit Risk Definition of Default (DoD). This paper sets out the PRA's proposed approach to implementing the European Banking Authority's (EBA's) three regulatory packages relating to DoD in the Capital Requirements Regulation (575/2013) (CRR) specifically:

- Regulatory Technical Standards (RTS) for the materiality threshold for credit obligations past due1;

- Guidelines (GL) on the application of the DoD2; and

- Opinion paper ('the EBA Opinion')3 on the use of the 180 days past due (DPD) criterion in the DoD.

The proposals are relevant to UK banks, building societies and PRA-designated UK investment firms. Importantly, they apply to firms using both the Standardised Approach ('SA firms') and Internal Ratings Based approaches ('IRB firms') as they affect the DoD which is fundamental to the application of supervisory risk weights within the SA, as well as to the estimation and application of IRB risk parameters.

The proposed implementation date is 31st December 2020. This is consistent with the EBA's implementation timeline of 31st December 2020 for its regulatory review of the IRB Approach4.

The key changes to highlight are:

- removal of PRA's discretion to allow firms to use 180 DPD in their default definition;

- setting a zero materiality threshold for retail exposures alongside a 1% relative and a sterling equivalent of €500 absolute materiality threshold for non-retail exposures in the application of DoD; and

- requirement to comply in full with the EBA GL on the application of DoD.

Overview of the current framework

CRR Article 178 sets out the DoD, which includes two triggers: 'unlikeliness to pay'; and 'days past due'. The latter is defined as 'the obligor is past due more than 90 days on any material credit obligation to the institution, the parent undertaking or any of its subsidiaries'. The regulation requires each national competent authority to outline how the RTS and GL should be applied. This includes:

- setting a threshold against which the materiality of a credit obligation past due shall be assessed (the 'materiality threshold'); and

- confirming whether the option to replace 90 days past due, with 180 days past due, in the DoD will be adopted (for exposures secured by residential or SME commercial real estate in the retail exposure class, as well as exposures to public sector entities).

Under the current framework, firms in the UK have been allowed to use 180 DPD in their DoD for specified exposures, subject to PRA approval, as part of their IRB permission with variable application of materiality thresholds currently across the industry.

Proposals that will change the status quo on DoD

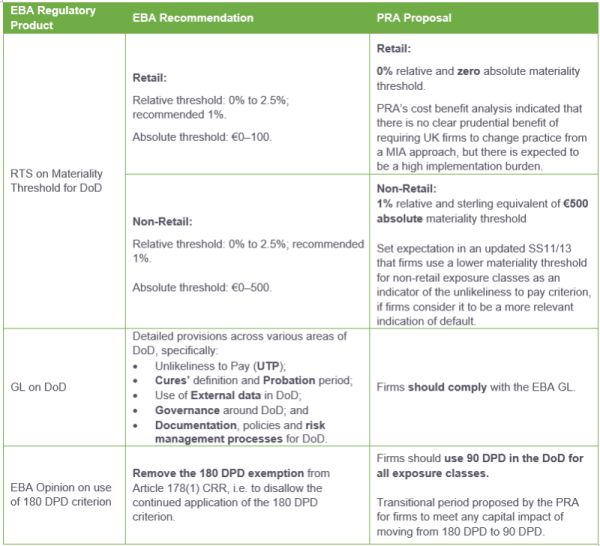

Table 1 below summarises the PRA proposals and their alignment with the EBA recommendations. Whilst the PRA proposals mostly align with the EBA recommendations, one of the major differences is the materiality threshold for retail exposures which in turn leaves room for UK firms to continue using the months in arrears (MIA) measure.

Table 1: Summary of the PRA's proposed changes compared to the EBA recommendations

N.B. The proposals relating to the RTS and GL apply to both SA firms and IRB firms, whereas the proposals relating to the EBA Opinion apply to IRB firms only.

Key implications for UK firms

These proposals will have implications both in terms of operational costs and, more importantly, potential additional capital requirements for firms. Specifically, we see the following key implications which will need to be considered:

- Continued use of MIA as a proxy for DPD with zero materiality threshold may create inconsistency.

The CP leaves room for UK firms to continue to apply a MIA-driven measure of DPD within the DoD. On the face of it, this is an appealing option for firms already using MIA given that legacy systems and processes would need to be overhauled to accommodate a mandatory change. However, it is important to recognise that this remains inconsistent with the CRR definition (and associated technical standards) and may ultimately not be sufficiently conservative or consistent with other uses. For example, the definition of 'credit impaired' (used in IFRS 9), which emphasises the importance of counting material DPD by applying 90 DPD as a Stage 3 backstop trigger.

It may of course be possible to demonstrate that the continuing use of MIA does not generate material differences in capital impacts across the credit cycle relative to the DPD counting approach. The broader questions are about RWA comparability across CRR firms and the extent to which the use of MIA could distort this picture, creating unintended impacts for the retail market, particularly in relation to mortgages. UK firms should challenge themselves as to whether they wish to align themselves with the dwindling number of MIA reporters, or the growing number of European reporters which have adopted compliant DPD counting whilst addressing IFRS 9 expectations

- Capital requirements are likely to rise for firms currently using 180 DPD.

For IRB firms currently using 180 DPD, the proposal to use 90 DPD will accelerate the recognition of defaults. The EBA Assessment3 for UK and French firms noted that this will likely lead to higher PD estimates and lower LGD estimates, driven by a reallocation of exposures that are currently non-defaulted into a default status, and the resulting change in risk parameter calibrations. The absolute impact on capital requirements, however, is less clear and will depend on the extent to which a potential decrease in LGD offsets the increase in PD, if it does at all. For example, some firms may not be able to realise the full decrease in LGD due to the CRR's current 10% portfolio-level LGD floor for retail exposures secured by residential property and the 15% portfolio-level LGD floor for retail exposures secured by commercial immovable property.

The materiality threshold proposal is also likely to affect the number of defaults and therefore the PD and LGD estimates. For IRB firms, the RWA and EL treatment for the increased default population will be directly affected. For SA firms the proposals on materiality threshold will result in a direct impact from a change in the stock of defaulted accounts which attract higher risk weights. Firms will therefore need to assess the impact of these proposals on their capital position and engage with the PRA to agree an appropriate transitional period which in some cases, may need to extend beyond the implementation date to meet the capital impact.

-

Internal systems and controls will need to be upgraded.

Both IRB and SA firms will incur implementation costs from introducing non-zero relative and absolute materiality thresholds in their systems. IRB firms currently using 180 DPD will face an implementation burden to change their systems, controls and default database to a 90 DPD measure.

Model monitoring will need to be enhanced to incorporate the proposals in addition to the GL provisions for monitoring the effectiveness of 'unlikeliness to pay' indicators and 'criteria for return to non-defaulted status'.

- Model landscape and infrastructure will need to be refreshed.

For IRB firms, the proposals regarding materiality threshold and removal of 180 DPD in the DoD would at a minimum require a reassessment of the models' performance with the revised DoD across PD, LGD and EAD/CF models. Where this results in a need to recalibrate or redevelop the models, it will require a programme of work with close coordination across the related implications for controls, capital and compliance as well as other regulations.

- Compliance assessment will need to be conducted to identify any gaps.

The PRA has not proposed to deviate from any chapter / article of the EBA GL on DoD and proposes that firms should comply with the GL fully. The onus will therefore be on firms to undertake a thorough assessment of the GL and request clarifications where required.

For example, the minimum probation period of 3 months for defaults meeting the DPD criterion is an area we believe firms will seek to clarify. Any choice of probation period requires careful consideration given its effect on the portfolio cure rate and the resulting effects on PD and LGD estimates. Further, the GL will add to the ongoing requirement to attest to compliance with the CRR, probably as part of the enhanced annual self-assessment process that should exist currently.

- Policies and processes will need to be subsequently updated.

Firms will be required to update their policies and processes to implement the materiality threshold, removal of 180 DPD and meet the GL regarding identification, application and monitoring of 'unlikeliness to pay' indicators. The provisions to meet the documentation standards set out, as well as how it is consistent with IFRS 9. Firms will also need to look at the implications for stress testing and Pillar 2 as well as the recently published standards in this space. The business will then have to be trained to use the updated model suite to enable continued compliance with the use test. This will apply to all levels of the organisation up to the Board, depending on the relevant governance framework.

- Governance will need to be refreshed to align to the GL.

The GL ask for effective internal governance arrangements for correct and consistent application of definition of default. Firms should reassess the internal governance arrangements for compliance with the GL, including the scope of internal audit.

In addition to the above, firms in the process of seeking IRB permission ('IRB Aspirants'), especially those in the early stages of this process, will need to carefully consider the proposed changes in conjunction with all the other in-flight regulatory changes from the PRA, EBA and BCBS to optimise delivery timescales and avoid 'regret spend'.

Regulatory programme of work interactions

The DoD PRA changes add to the significant number of regulatory requirements and proposals relating to credit risk capital requirements which have recently been finalised by the PRA, EBA and BCBS. The over-arching objective of the proposals is to reduce RWA variability under the IRB approach and to increase risk sensitivity under the SA.

Figure 1: Key regulatory requirements and proposals affecting credit risk capital requirements

The proposed changes to DoD create a fundamental dependency in firms' implementation plans as they affect both the application of supervisory risk weights under Basel III final reforms6 and the recalibration / redevelopment of IRB models to meet the new and upcoming PRA and EBA requirements. For example, UK firms will need to understand the impact of these proposed changes alongside the PRA-imposed requirements for the IRB approach for residential mortgage portfolios5 which also need to be implemented by 31st December 2020. Firms undertaking financial and business impact assessments, in order to understand how credit risk capital requirements will change following these reforms will need to adapt them for the proposed changes to DoD. This will make developing (or updating) the implementation plan for Basel III final reforms, to capture inter-dependencies between regulations and ensure the overlapping timelines can be met, an immediate priority.

How firms are getting ahead on this new requirement

Sophisticated firms are seeking an accurate assessment of the impact of these proposals on capital, even where they do not expect to be affected. Once they have further clarity on the range and sources of potential impacts, we expect these firms will apprise their stakeholders (not least given the level of market interest in this paper on the day it was released) and are well advanced with plans to engage with the PRA, to agree an appropriate transitional period to meet any capital impact. This is the case for both SA and IRB firms.

Those firms transitioning to IRB have typically incorporated assumptions relating to DoD within existing quantitative impact studies. They will also have completed an assessment of the GL to understand whether there will be broader operational changes. The changes proposed will either reinforce or build on the expected impacts, which may require time and budget to be revised, redesigned and then implemented, including technology updates. This is particularly important given we are operating in a time when data regulation such as BCBS239 is hugely topical7

We anticipate that those firms looking at the emerging regulation holistically will already be working with their partners to reassess already full regulatory books of work in an effort to update their implementation plans to ensure overlapping timelines are met without incurring 'regret' spend.

Conclusion

The CP provides clarity around the PRA's approach to the implementation of the EBA's roadmap and offers some flexibility for UK firms. It also increases the number of prudential regulatory changes that we expect to see in the near future, implementation of which will need to be carefully coordinated.

The proposals in this CP are part of the jigsaw of several inter-connected regulatory products arising from the reforms developed by the PRA, EBA and BCBS.

The challenge for firms is to complete the jigsaw by mapping out the requirements, timelines and impact on individual credit risk components and to avoid multiple cycles of extended implementation effort and significant cost.

Footnotes

1 http://data.europa.eu/eli/reg_del/2018/171/oj

4 www.eba.europa.eu/documents/10180/1359456/EBA-Op-2016-01+Opinion+on+IRB+implementation.pdf.

6 For a detailed understanding of the emerging implications of the Basel III final reforms, refer to our publication: Basel III – The calm before the reform

7 https://www.bis.org/bcbs/publ/d443.pdf

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]