Introduction

Overview As the economic climate worsened and slid from credit crunch to global crisis over recent months, it became clear that the 2008 Pre-Budget Report (PBR) would be dominated by macro economics.

In an unprecedented departure from 'Budget Purdah', the Chancellor of the Exchequer, Alistair Darling, appeared on daytime television on 30 October and promised there would be no tax increases this time around. He indicated that his prescription for the nation would be to put more money into people's pockets to boost spending.

Mr Darling appeared on television again the day before the PBR and much of his speech was common knowledge before he finally addressed MPs. Consequently, there were no real surprises in the thrust of the report and no last minute 'rabbit out of the hat' finale as we came to expect with Mr Brown.

VAT reduction and subsequent tax increases

With all of that high-profile leaking, we had already been softened up to expect a Robin Hood type budget where the 'better off' would be squeezed to pay more income tax so that VAT could be reduced so as to encourage spending. The first income tax increases relate to the restriction of personal allowances and will impact on those with taxable incomes over £100,000. These increases will be delayed for a year to April 2010, and then a year later there will be a new higher rate of 45% on taxable incomes over £150,000. All of which could give us an interesting political situation, bearing in mind that the latest date for the next general election is early June 2010.

Small businesses

Small businesses were clearly in the Chancellor's thoughts as indicated by his decision to delay the threatened increase in the rate of corporation tax and to extend loss relief carry-back. The Chancellor also listened to our plea not to introduce the income shifting regime which, as proposed, would have required a significant amount of additional record keeping for many family businesses. Unfortunately, the formal report published today indicates that the Treasury remains intent on taking action in future so this may be just another temporary reprieve.

There are a series of measures to help small and medium-sized businesses facing credit constraints, including a rebranding and revitalisation of the existing 'Time To Pay' facility whereby businesses in difficulty may spread their tax payments on an affordable timetable.

Conclusion

Mr Darling said that his report comprised exceptional measures to reflect the exceptional times. Certainly the way in which the report was formulated via breakfast TV was wholly exceptional. It remains to be seen whether we return to Budget secrecy in future.

1 Personal tax and trust

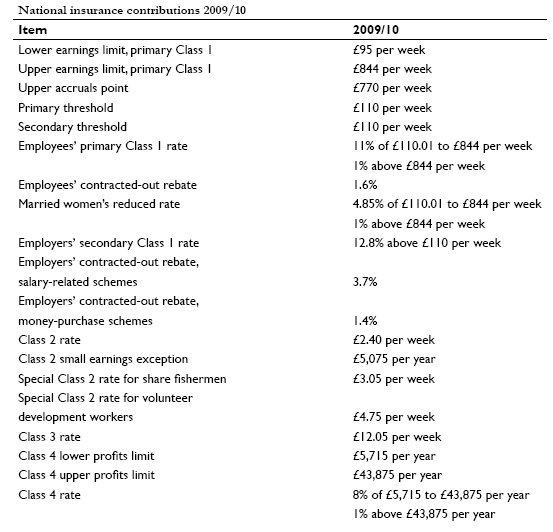

1.1 Income tax and National Insurance rates, thresholds and limits

The proposed changes to personal tax rates, allowances and limits, and National Insurance Contributions (NIC) rates and thresholds are set out in Appendix 1.

Most of the personal tax allowances will be increased as usual in line with inflation for 2009/10. However, the upper earnings limit for NICs will be aligned with the higher rate threshold for income tax.

Several significant changes have been proposed to take effect from 2010/11 and 2011/12.

From 2010/11 onward those with income exceeding £100,000 per annum will suffer a reduction to their personal allowance by £1 for every £2 in excess of £100,000, up to a maximum of half of the standard personal allowance. Those with income exceeding £140,000 per annum will suffer a further reduction to their personal allowance by £1 for every £2 in excess of £140,000, up to a maximum of the full standard personal allowance.

Further changes proposed for 2011/12 are as follows:

- a new higher rate of tax of 45% will apply to income over £150,000 per annum (37.5% on dividend income)

- the rate of tax applicable to trusts will increase to 45% (37.5% for dividend income)

- the National Insurance primary threshold will be aligned with the personal allowance for income tax, bringing all tax and National Insurance thresholds into alignment

- employers' and employees' NIC rates will increase by 0.5% as will profit-related contributions for the self-employed. The existing additional 1% contribution for those earning in excess of the upper earnings limit will increase to 1.5%.

Certain changes to the Tax Credit system in excess of inflation have been proposed to take effect from 6 April 2009.

Comment: Those earning over £150,000 will suffer a triple raid on their pockets from 2011/12. An individual with income of £200,000 will suffer approximately £6,400 more per annum in tax and NICs as a result of the combination of the two tax changes and the NIC change.

The real sting, however, is on discretionary trusts where the tax rate is increasing by 5% on all income, not just income in excess of a threshold.

Against these tax increases the enhancement of Tax Credits is to be welcomed for low to middle earners, some of whom will be up to £520 per annum better off, though the complexity of the Tax Credits system remains a concern.

1.2 Simplification of anti-avoidance rules: employment-related securities

With effect from Royal Assent to the Finance Bill 2009, one of the mistakes in the anti-avoidance legislation for employment-related securities will finally be corrected.

The amendment concerns the taxation of certain share acquisitions where the employee acquires, at an undervalue, shares not otherwise taxed to employment income tax.

Pre-Budget Report 2008 The most common examples are where the shares are acquired partly-paid or where payment is made in instalments. In these circumstances, the employee is treated as receiving an interest-free loan by reference to the outstanding amounts. These charges are generally brought to an end only when the shares are sold.

If the employee sells before paying all instalments, there can be tax due even when there is no profit. Similarly, if partly-paid shares are sold, the employee will be taxed on a profit he/she never makes. In both situations the treatment is to be corrected.

Similarly, where there is a scrip or bonus issue, the employee may technically be caught under these provisions even though he/she is effectively no better off because his/her other shares have correspondingly fallen in value.

Comment: These amendments are long overdue. The interesting question will be how HMRC will now treat possible occasions when the charges arise before Royal Assent. At present, there has been an unofficial pragmatic acceptance by HMRC that the charges concerned are anomalous. It is just possible that its sensible sympathetic approach may be jeopardized by the impending change.

1.3 Assistance for disabled company car drivers

From April 2009, the tax charge for a company car with automatic transmission provided for private use to a disabled employee (someone entitled to a blue badge) will be based on the manufacturer's list price and the carbon dioxide (CO2) emissions rating of the equivalent manual transmission model.

Comment: The amount of the benefit of a company provided car is calculated by applying a percentage derived from its CO2 emissions rating to the manufacturer's list price for the vehicle. This measure will extend the current minor tax advantage enjoyed by disabled company car drivers who have their taxable benefit measured according to the CO2 emissions rating of the equivalent manual model car if they are provided with an automatic. The emissions level is likely to be lower for the manual version, as is the list price. This change will have limited impact.

1.4 Leasing avoidance by film partnerships

A measure has been introduced, effective following the issue of a technical note on 13 November 2008, to counter avoidance involving businesses leasing films on long-funding leases.

Under current law, certain income streams were outside the charge to income tax, if reliefs aimed at long-funding leases of plant and machinery were exploited.

The new measure will counter such avoidance by classifying all rental receipts as taxable.

Comment: A largely technical and narrowly targeted clampdown further highlights HMRC's intolerance of aggressive tax avoidance arrangements. This also further highlights the recurring theme of reliefs being introduced only to be gradually withdrawn as and when loopholes arising from their complexity are discovered. (See also the commentary at 2.11 on long-funding leases generally.)

1.5 Tax relief for travel by temporary workers

It has been decided not to make changes to the legislation concerning relief for employee travel and subsistence expenses by reference to temporary workers and those covered by overarching employment contracts on which the Government had been consulting. However, HMRC will be refocusing its efforts to ensure that the current regime is correctly applied.

Comment: The Government had been concerned that particular groups of workers were in a position, because of the nature of their employment, to take much greater advantage of the legislation concerning employee travel and subsistence expenditure than had been intended when the regime was relaxed in 1998. The consultation process has led the Government to believe that the legislation should not be disturbed, however compliance in this field is poor. It intends to tackle abuse through more vigilant compliance inspections, presumably targeted at employment agencies and other similar providers of temporary workers. If the intelligence does not indicate an improvement in compliance, the Government may be expected to come back to this at a later date.

1.6 Offshore disclosure facility

HMRC will be giving offshore account holders a fresh opportunity to make voluntary disclosures of unpaid tax liabilities on the interest received or otherwise on the source of the invested funds.

Comment: HMRC offered the first offshore disclosure facility in 2007 (known colloquially as an amnesty). Taxpayers who gave a full disclosure were entitled to suffer only a fixed 10% penalty on undeclared liabilities. It appears that HMRC holds information that suggests that a large number of individuals did not come forward. The objective is to encourage them to do so now in return for the promise of a capped penalty lower than would otherwise be the case, therefore reducing the manpower that would be needed if HMRC were to investigate every undeclared liability.

2 Business

2.1 Small companies rate of corporation tax

The increase from 21% to 22% in small companies corporation tax rate planned from 1 April 2009 has been deferred to 1 April 2010. The lower and upper limits for marginal relief calculations remain at £300,000 and £1,500,000 respectively, and the fraction used in calculating marginal relief for nonring fence companies for the period to 31 March 2010 is 1/40.

Comment: The phased increase in small companies corporation tax rate (apart from North Sea ring fence profits) was announced in Budget 2007, increasing to 21% on 1 April 2008 with a planned increase to 22% on 1 April 2009. The deferral of the introduction of the increase on 1 April 2009 was widely predicted in the lead up to the PBR. It is of relatively small assistance to small companies, being a maximum one-off cash benefit of £3,000 to companies with taxable profits of £300,000 (less for those with lower profits), clawed back in full where profits reach or exceed the £1.5m limit.

2.2 Income shifting

In January 2008, the Government introduced draft legislation to counteract cases where company distributions and partnership profits had been shifted from one individual to another who paid tax at a lower rate. After fierce opposition from trade and professional bodies it was announced in the March 2008 Budget that the legislation would be delayed until 2009 to allow further debate. The Government has now announced that in light of the current economic challenges, it is deferring action once more and no legislation will be included in the 2009 Finance Bill. However, the matter will be kept under review.

Comment: The draft legislation was issued in response to the Arctic Systems Ltd case. The company's profits derived from computer consultancy services provided by Mr Jones, but a large part of those profits were then distributed equally to Mr and Mrs Jones as shareholders. The House of Lords ruled that HM Revenue & Customs (HMRC) had no right to reallocate the dividend received by Mrs Jones to her husband. The draft legislation would have required many family businesses to keep additional records to justify the respective contributions of the various individuals involved and could have been the final straw for many struggling businesses. Although it is good that the Government has deferred tackling the issue, it has not gone away and it appears the Government is still intent on taking action. The real problem is that the system for taxing small businesses has evolved in a piecemeal way and what is needed is a fundamental root and branch review.

2.3 Extension of trading loss carry-back rules for business

To help businesses of all sizes with cashflow in respect of tax losses, the Chancellor has announced an extension to the carry-back rules for trade losses. The rules for companies and unincorporated businesses are slightly different.

Companies For losses incurred in accounting periods ending in the period 24 November 2008 to 23 November 2009, it will be possible for companies to elect to carry-back up to £50,000 of unrelieved trade losses against profits of the preceding three years with losses being set against later years first. The £50,000 limit will be adjusted pro-rata for accounting periods ending within the above dates that are less than 12 months. This will also limit the total loss relief for all accounting periods ending in the above period to £50,000.

The existing loss reliefs (carry-back against any profits of the previous 12 months, or unrestricted carry-forward against future losses from the same trade) will continue. In addition to normal businesses, the extension applies to losses incurred in the oil and gas ring fence regime and losses incurred in a furnished holiday lettings business.

The new loss relief is referred to as an 'extended' loss relief. The guidance, therefore, implies that where the loss can be fully utilised in the immediately preceding year there will be no option to carry back £50,000 to the two years preceding that. It appears the £50,000 limit is a restriction per company rather than a restriction per group.

Unincorporated businesses

For losses incurred in the 2008/09 tax year, it will be possible to carry back up to £50,000 of unrelieved trade loss against profits of the same trade, profession or vocation, or the same furnished holiday business, for the three years before 2008/09.

The guidance in the technical note indicates the new extended loss relief rule applies only where a claim for relief is made under ITA2007 s64 (relief for loss against general income of the loss-making year or the previous tax year or both). Indeed, it will be available where no claim is made due to the absence of other profits in the loss making or previous year, if it would otherwise be possible to make a claim. The new loss relief will be available against profits of a later year before an earlier year. There will also be relief for NICs from the loss.

Repayments

Although claims for loss relief will be accepted when they can be made under the existing rules for claiming relief, as the relief is to be formally introduced in Budget 2009, any repayment of tax will only be possible after Budget day.

Comment: The new corporate loss relief is referred to as an 'extended' loss relief, and it will be available for offset against any type of profit of previous years. The guidance, therefore, implies that where the loss can be fully utilised in the immediate preceding year there will be no option to carry back £50,000 to the two years preceding that. It appears the £50,000 limit is a restriction per company rather than a restriction per group, and that the loss period will coincide with the current period of economic downturn (accounting periods ending on or after 24 November 2009 and on or before 23 November 2009).

For unincorporated businesses, however, relief is only available against previous profits from the same trade. In addition, a business with a 30 April year end may only be able to obtain relief for a loss incurred in the year ended 30 April 2008, whereas it may have a more significant loss in the year ended 30 April 2009 (assessable in 2009/10). Thus, in some instances it may be appropriate to consider the change of accounting date rules.

2.4 Taxation of foreign profits

The long-running and high-profile discussions about reforming the way overseas profits of UK-based multinational companies are taxed has continued in the PBR. This time however, the UK Government has announced its intention to bring forward its comprehensive package of reform for inclusion in Finance Bill 2009. With businesses threatening to leave the UK for more favourable tax regimes, the Chancellor has sought to make the UK corporate tax regime more attractive to international companies.

The package of reform includes:

- introducing in Finance Bill 2009, the foreign dividend exemption for large and medium-sized businesses supported by a worldwide debt cap on interest, and an extension of the unallowable purpose rule for loan relationships (to include schemes and arrangements)

- committing to consult further on modernising the controlled foreign company regime (CFC), together with a removal of the exempt activities test for holding companies in Finance Bill 2009

- removing Treasury consent rules and notification requirements, and replacing them with a quarterly reporting requirement for high-risk transactions (a deminimis limit of £100m is proposed, on which details are awaited).

Draft legislation is expected in December 2008.

The earlier proposals for reform of the CFC rules were roundly condemned by businesses. Recognising this, while still acknowledging the need to protect UK tax revenues from artificial diversion of profits from the UK, the Government is proposing further consultation. The Government does not anticipate finalising CFC reform in time for Finance Bill 2010. In view of this, the Government is offering a 24-month transitional period to allow companies to reorganise their holding company structures to deal with the proposed Finance Bill 2009 removal of the exempt activities test for holding companies.

Over the course of the earlier consultation, businesses had expressed concern over the scope of these new anti-avoidance rules; the PBR has sought to reassure them by confirming that any measures being contemplated would seek to enhance UK competitiveness.

There are no further details regarding the worldwide debt cap on interest; however, interest claimed by UK members of a multinational group would be restricted by reference to the group's consolidated external finance costs.

Comment: Overall, the proposals set out in the PBR will be welcomed by many businesses with overseas connections. It should go some way to making the UK an attractive location for multinational companies. Given that there is little in the way of detail on the measures proposed, a cautious note should be struck as we will need to see the draft legislation and consultation documents to evaluate the success of these proposals.

2.5 Foreign exchange accounting changes

Changes in the practice of accounting for financial instruments enacted in 2004 introduced measures which recognised the changes for corporation tax purposes over a period of ten years.

However, an anomaly in the legislation has been identified in respect of the reversal of the foreign exchange differences on certain foreign denominated instruments. In particular, where such instruments were used to hedge the company's economic risk under the old matching rules, the foreign exchange difference was not taxed.

Under the Change of Accounting Practice (COAP) regulations for financial instruments it is possible for the reversal of the exchange differences to be taxed twice.

Measures are to be introduced with effect from 1 January 2009 to prevent double taxation or relief for the exchange differences by disregarding transitional arrangements under the COAP regulations.

2.6 Loan relationship rules: connected companies

The current loan relationship rules for loans between connected parties can create a situation where on a release of a trade debt, the creditor is denied relief for the debit on writing off its asset, while the debtor is taxed on the credit from the release of its liability. With effect for accounting periods beginning on or after 1 April 2009, the release of a trade debt between connected parties in such circumstances will no longer result in a taxable amount for the debtor.

In addition, there is currently a restriction on the availability of a tax deduction for interest accrued and due to a connected party, but not paid within 12 months of the end of the accounting period, and where the creditor is not required to account for the interest under the loan relationship rules. The restriction applies to deny the debtor relief for the interest until it is paid. This has been held to be contrary to EU rules on freedom of establishment, as it discriminates against borrowing from a connected lender located outside the UK. Changes to eliminate this potential discrimination are announced for accounting periods beginning on or after 1 April 2009.

Draft legislation is expected on both the above points before 31 December 2008.

Comment: It is currently possible to avoid the taxation of release of a connected party trade debt by circulating cash to turn the trade debt into a 'loan relationship'. The proposed change is a welcome simplification to the current rules which can trap the unwary or ill-advised.

The options being considered for change with respect to timing of deduction for loan interest on connected party debt are (i) to require restriction of relief until paid in all cases or (ii) to introduce an anti-avoidance rule. A change to reduce discrimination against overseas connected party debt will be welcomed by most businesses.

2.7 Tax on chargeable gains, stamp duty and stamp duty reserve tax: stock lending arrangements

Transfers of securities under stock lending arrangements are generally disregarded for capital gains purposes. Where it becomes apparent that the borrower is insolvent and unable to return securities under a stock lending arrangement, the lender is deemed to have sold the securities for market value consideration.

Where the borrower becomes insolvent on or after 24 November and, provided the lender uses collateral provided by the borrower to acquire replacement securities of the same kind, the lender will not be treated as making a disposal for capital gains purposes. It will be possible to elect for the changes to take effect from 1 September 2008.

Similar changes to the capital gains treatment of securities sold under sale and repurchase agreements ('repos') are being considered.

New rules will remove stamp duty or stamp duty reserve tax on the acquisition by the lender of replacement securities of the same kind using collateral from an insolvent borrower from 1 September 2008.

These rules also remove a stamp duty reserve charge on the borrower under stock lending and repo arrangements where the borrower has defaulted due to insolvency.

Comment: These are helpful concessions which permit effective gross investment of collateral by the lender where the borrower becomes insolvent, and provide relief to parties from stamp taxes.

2.8 Business expenditure on cars

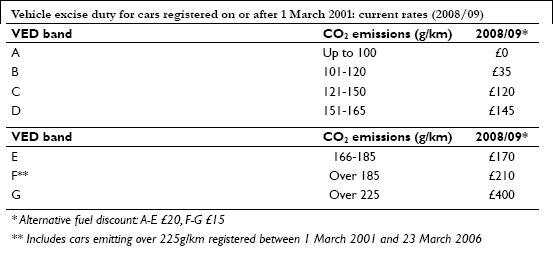

From April 2009, the Government will abolish the current rules for 'expensive cars' replacing them with a new pooling system where the rate of writing-down allowance will be based on the CO2 emissions of the car.

The restriction on allowable lease rentals for businesses will also be based on the CO2 emissions of the car.

The current capital allowances rules for cars are as follows.

- Expenditure on cars with CO2 emissions up to 10g/km can qualify for 1 00% first-year allowances.

- Expenditure on cars costing £12,000 or less is eligible to go into the main pool and writing-down allowances are given at 20% per annum on the reducing balance.

- Expenditure on cars costing over £12,000 must be dealt with separately with each car being allocated to a single asset pool and the writing-down allowance restricted to £3,000 per annum.

The proposed changes to the capital allowances rules for purchased cars are as follows.

- The restriction of capital allowances on cars costing more than £12,000 will be abolished and qualifying expenditure will be allocated to one of the two general plant and machinery pools, based on the car's CO2 emissions. Cars with CO2 emission over 160g/km will be dealt with in a special rate pool receiving writing-down allowances at 10%. Cars with CO2 emissions of less than 160g/km will be dealt with in the general pool receiving capital allowances at 20%.

- A single asset pool will continue to be used for cars which have an element of non-business use, but capital allowances will be based on the car's CO2 emissions.

- A transitional period of five years will operate for expenditure incurred prior to April 2009, which will be subject to the old rules.

As noted, the rules regarding lease rental payments on expensive cars (cars costing over £12,000) have been amended. The current restriction will be changed and a flat rate disallowance of 15% will apply to the relevant payments for cars with CO2 emissions above 160g/km. Leases that commence prior to April 2009 will be subject to the old rules.

Certain hire cars (taxis, daily hire cars, cars leased to disabled people) are exempt from the 'expensive car rules' under current legislation but in future will be subject to the CO2 emission rules. The rules regarding expenditure on cars leased to those in receipt of certain disability allowances are still under review.

Motorcycles are excluded from the definition of cars and will not be subject to the above rules. Expenditure on motorcycles after April 2009 should qualify for the annual investment allowance.

Comment: The Government is following through on its intention to link capital allowances with environmental issues by choosing to focus on CO2 emissions.

Companies due to replace motor vehicles (including leased vehicles) in the coming year have an opportunity for tax planning. In order to receive the maximum amount of capital allowances, companies must ensure that motor vehicles purchased (or leased) after April 2009 have emissions below 160g/km.

Depending on costings and emissions rates, companies may wish to time their motor vehicle acquisitions to take place after April 2009 as expenditure prior to that date will be subject to the old rules for a transitional period of five years.

2.9 Land remediation relief

Legislation will be introduced to extend land remediation relief to expenditure on remediating longterm derelict land incurred on or after 1 April 2009.

Subject to secondary legislation, derelict land will be 'long-term' if derelict since 1 April 1998 and the relief will be available on specified removal, below-ground demolition and relevant preparatory activity costs only.

The Finance Bill 2009 will also give greater clarity over what expenditure qualifies for existing relief for the removal or mitigation of the effects of contamination – in general, expenditure on naturally occurring contamination will not qualify, although specifically included are the costs of treating land effected by Japanese knotweed, radon and arsenic.

However, in line with the Government's ambition to encourage environmentally sustainable tax incentives, relief will only be available for methods of remediation that are considered appropriate. In particular, costs of removing Japanese knotweed to landfill sites will not qualify for relief from 1 April 2009.

Comment: Land remediation relief gives bodies liable to corporation tax a deduction of 150% for qualifying expenditure, or a tax credit for losses surrendered.

The relief has previously been criticised as too narrow for its exclusion of sole traders, individuals operating in partnership and non-UK resident property owners. These changes do nothing to widen the scope in this respect.

While the reforms may be positive extensions to the existing legislation, the specific exclusion of most naturally occurring contaminants is not welcome.

2.10 Sale of lessor companies: intermediate lessors

This measure counteracts a tax avoidance scheme involving a sale and leaseback arrangement. The arrangement transforms a lessor into an intermediate lessor with no legal title to plant and machinery but the lessor is still entitled to claim capital allowances. On the sale of the lessor there was no charge imposed to recapture the timing benefits derived from a claim to capital allowances from the selling group.

This measure has effect where a lessor company is sold on or after 13 November 2008 and imposes a charge in the above circumstances. Relief equalling the charge returns the benefit to the purchasing group.

Comment: These rules specifically target avoidance schemes seeking to exploit an anomaly in the legislation and have limited application.

2.11 Long-funding leases of plant or machinery

The Chancellor reiterated the Government's intention to amend the long-funding leasing rules to correct deficiencies and close down avoidance schemes with effect for transactions entered into on or after 13 November 2008. A long-funding lease is an operating lease that is five years or more, or a finance lease exceeding either five or seven years in length depending on the terms and accounting of the lease.

The legislative changes to take effect from 13 November are as follows.

- The disposal value for lessees under long-funding leases has been amended so that it will be the higher of (i) the full lease rentals less finance costs and (ii) market value.

- The opportunity to claim capital allowances (or even first year allowances) on the current market value of plant or machinery on which allowances have already been claimed, using a combination of long-funding finance and long-funding operating leases has been blocked.

Comment: Although detailed rules assist taxpayers with certainty, the regular changes to correct weaknesses in the legislation show that greater thought needs to be given to designing effective targeted legislation. The long-funding leasing rules were introduced with the intention of removing the tax distortion for a decision on financing the purchase of plant or machinery (P&M) between using a bank loan or capital or alternatively using lease finance. These rules seek to transfer the right to capital allowances from the lessor (legal owner of the P&M) to the lessee, in the case of a long-funding lease. Prior to these rules, a business which was unable to make immediate use of the tax allowances arising from P&M could access these tax benefits using lease finance.

2.12 Empty property rates relief

The Government has temporarily increased the threshold at which an empty property becomes liable for business rates. For the financial year 2009/10 only, empty properties with a rateable value of less than £15,000 will be exempt from business rates.

Comment: The change will be welcomed by the property industry which has lobbied the Government on this issue since the abolition of the empty property relief for vacant commercial and industrial properties was announced in the 2007 Budget.

However, the move is not completely satisfactory and will not prevent the forced demolition of some empty properties and the delay of developments.

The Chancellor announced that the increase will exempt an estimated 70% of empty properties but, as it is thought the rateable value threshold equates to a property value of around just £250,000, it is only likely to apply to small properties.

The fact that the relief is temporary, postponed and restricted will lead many to conclude that the Treasury has not gone far enough.

3 VAT and other indirect taxes

3.1 Temporary change in rate

In view of the current economic climate and in an attempt to boost the economy and encourage spending, the Chancellor has introduced a temporary decrease in the standard rate of VAT from 17.5% to 15%. The reduced rate of VAT will come into effect from 1 December 2008 and will last until 31 December 2009.

It should be noted that this decrease of 2.5% is likely to reduce revenues to the Government by around £12.5bn, which is a significant loss that is likely to be offset by future increases in income tax and National Insurance as well as current increases in excise duties.

Anti-forestalling legislation will be introduced to prevent the creation of artificial arrangements to avoid the reintroduction of the 17.5% rate on 1 January 2010.

Comment: The change in the VAT rate is likely to cause many businesses some administrative issues as the rate of VAT has not changed since the early 1990s. There are special rules dealing with tax points for supplies that cover both periods where contracts have been signed and agreed with the previous standard rate of VAT. This is something all businesses will have to review before next week.

This will directly benefit businesses that make exempt supplies, including banks and insurers for whom irrecoverable VAT represents a significant cost. This change will also be welcomed by charities and not-for-profit bodies which incur irrecoverable VAT.

At the household level, however, with many retailers already offering 20% off prices in the run up to Christmas, the effect on consumer spending may be difficult to notice, especially if retailers choose not to pass on the benefits to consumers.

3.2 More time to pay

The Chancellor has announced that more support will be available for businesses that are worried about being able to meet their VAT payments to HMRC. A new business payment support service has been launched from today to provide a helpline service, options to pay over a longer period of time and to offer some flexibility in paying.

Comment: In the past, HMRC has typically taken a hard line on businesses that fail to pay the VAT due to HMRC on time, on the basis that customers have paid the VAT over to the business in good faith. This is a welcome measure in today's economic climate and this should provide further support for businesses suffering cashflow difficulties. (For further comment, see 5.1.)

3.3 Flat-rate scheme simplification

The entry and leaving tests for the VAT flat-rate scheme are to be simplified. The entry test based on total business income will be removed, so that the only requirement for entry to the scheme will be that the annual taxable turnover is less than £150,000. The test for leaving the scheme will be amended, so that when the annual income exceeds £225,000 the business will have to leave the scheme. In the past there had been confusion as to how to calculate this income. This has now been clarified and businesses are required to use the method of accounting used by the business while in the scheme (i.e. cash basis for cash accounting).

Comment: This is a welcome change for businesses that are eligible for the scheme. The previous entry and leaving tests often caused confusion and this simplification should make it easier for businesses considering joining the scheme.

3.4 Bespoke retail scheme changes

The turnover limit to use the five published retail schemes available to retailers will increase to £130m with effect from 1 April 2009. Previously, retailers with a turnover of over £100m had to agree a bespoke retail scheme with HMRC or use the normal VAT rules.

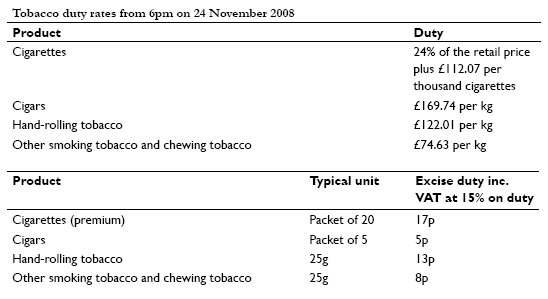

3.5 Excise duty increases

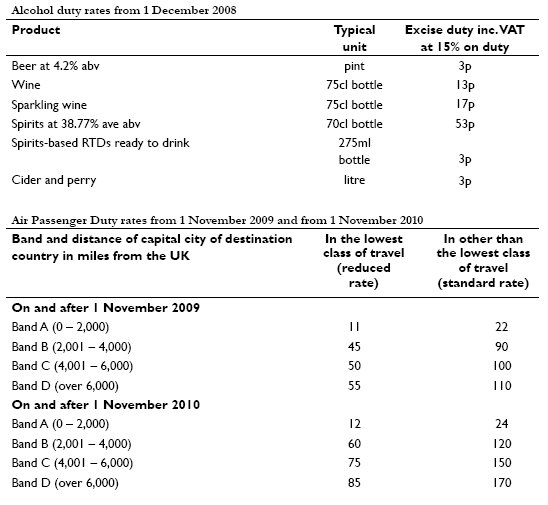

The duty on alcoholic drinks will be increased by 8% across all alcoholic drinks with effect from 1 December 2008.

The fuel duty rates for 2008 introduced in the Finance Act 2008 will be reinstated with effect from 1 December 2008 increasing the fuel duty by 2p per litre on leaded petrol, unleaded petrol and diesel. There are further stepped increases that will take effect from 1 April 2009. It was also announced that the current duty differential of 20p per litre for biofuels for road use will cease from 2010.

The duty rate for cigarettes is to increase from 22% to 24% and will take immediate effect (other tobacco products will increase by 4%).

3.6 Air Passenger Duty changes

With effect from 1 November 2009, Air Passenger Duty will be reformed to be based on four geographical bands based on distance from London to the capital city of the country of destination. Each band will have two rates, one for standard class of travel and one for other classes of travel.

Comment: This should make Air Passenger Duty fairer in the sense that the further you fly, the higher tax will be due.

4 Pensions and investment

4.1 Statutory Lifetime Allowance The Statutory Lifetime Allowance (SLA), the amount which individuals can accumulate in tax-efficient pension funds during their working life, is to be frozen at £1.8m as of 2011/2012 until 2015/2016. As well as freezing the SLA, the Chancellor has also chosen to freeze the annual allowance or the amount that can be paid in the way of tax relievable pensions contributions. This will remain at £255,000 for the five years commencing 2011/2012.

Comment: Since the introduction of the SLA in 2006/2007, when it was £1.5m, it has increased by approximately £75,000 per annum. By freezing increases for a period of five years the Chancellor is potentially raising taxes of between 40% and 55% on this amount, being the tax relief that will be forgone on pension contributions and the possible lifetime allowance charge which could become due on those who will now breach the limits. This is, therefore, a significant measure.

The freezing of the annual allowance is again seen as a significant measure which will further limit the amount that high-earning individuals can receive in the way of tax relief on pension contributions.

The NIC changes in 2011/2012 will, in general, place much more focus on pensions planning as employers can improve benefit packages to reduce NIC while boosting pension provision.

Employer contributions into pension schemes are not subject to employer or employee NIC and the proposed rises will place more emphasis on the use on pension funds as a way of providing tax-efficient remuneration.

It is also arguable that those paying tax at 45% as well as those that could potentially lose their personal tax allowances, or a part of them, may well also look to use pension contributions to reduce their tax burden and improve their retirement provision.

4.2 Changes to Authorised Investment Funds

As part of the Government's commitment to increasing the attractiveness of the UK authorised funds regime over those of competitor countries, a number of previously highlighted changes have been confirmed in the PBR.

- Qualified investor schemes (QIS) – since creation by the Financial Services Authority (FSA) in 2004, investors in these funds have been subject to an annual tax charge on profits where their interest is 10% or more. This has had the practical effect of making the regime unattractive, and few QIS funds have been launched. With effect from 1 January 2009, the 10% test will be abolished, and investors in these funds will be treated as if they held shares in an ordinary Authorised Investment Fund (AIF). Transitional rules will apply for existing QIS.

However, the 10% rule will continue to apply if the fund does not meet the 'genuine diversity of ownership rule', which applies in the case of existing property authorised funds. The aim of this rule is to prevent QIS being used by small groups of connected individuals or companies.

- Property Authorised Investment Funds (PAIF) – property feeder funds being set up to take advantage of the new PAIF regime will be assisted by two technical changes to ensure the tax efficiency of these funds. The first change will ensure that Stamp Duty Reserve Tax is not levied at both the feeder fund and PAIF level on the creation of shares to avoid a double charge to tax. The second change will allow PAIFs to pay net distributions to feeder funds to reduce the administration on onward payments to the ultimate shareholders.

Finally, the tax treatment of manufactured payments representing PAIF distributions will be brought in line with the existing manufactured payment provisions.

The Government is also creating a targeted anti-avoidance rule to tackle an existing arrangement that has been brought to light by the disclosure rules. The scheme involved trading companies being able to use the corporate streaming rules that apply to AIF distributions to convert taxable dividends into non-taxable dividends. This measure will take effect from 1 January 2009.

Comment: The UK's fund industry has been under severe competition from other jurisdictions, and any changes to increase the willingness of fund managers to set up UK based investment funds is very welcome. These changes are part of a wider Government programme to provide flexibility in the UK's authorised investment fund regime, and convince fund managers that the UK is the best place to set up an investment fund. The anti-avoidance changes are part of the continuing campaign against the use of funds for tax avoidance.

4.3 Individual saving accounts (ISAs)

Technical amendments will be made to increase the types of investments that are eligible under these tax-efficient savings schemes to include bonds issued by multilateral institutions such as the World Bank, the International Monetary Fund, the United Nations and regional development banks.

4.4 UK Real Estate Investment Trusts: dealing with group owner-occupied property

Real Estate Investment Trusts (REITs) are tax-efficient structures for holding property investments compared to traditional companies, as they avoid a potential double tax charge on the shareholders – firstly through tax on company profits and then on the shareholder through tax on company distributions. In order to come within the REIT regime, certain conditions have to be met, including the fact that 75% or more of the assets must be qualifying properties used in a qualifying property rental business, which must generate at least 75% of the REIT's profits. Qualifying properties and rental businesses do not include the rental of properties to group companies. A REIT group is defined on the lines of a capital gains group which relates to the amount of share capital held.

Some groups have been looking at ways of re-organising their structure to form two or more REITs within a group, each REIT being a qualifying capital gains group. There could then be rental of REIT qualifying properties in one group to the other group, thus circumventing the intended requirement for the whole REIT entity to meet the 75% tests described above.

Changes will be introduced with draft legislation subject to consultation in the New Year, to ensure the required tests for the regime apply to the whole economic business.

Comment: Previous changes to the REIT regulations have been deemed to apply from commencement of the regime. Thus, there would seem to be little or no opportunity to take advantage of the current weakness in the legislation. The corresponding tax exempt property asset and business requirements for a PAIF are 60% compared to 75% for REITs. However, the meaning of property rental business to which the asset and business tests apply are more all encompassing than for the REIT regime, although it may be possible for a PAIF to invest in REITs which lease properties to each other.

5 Miscellaneous

5.1 Business payment support service HMRC has introduced a new business payment support service to help firms facing difficulties to spread their tax on an affordable timetable. The service covers all business taxes, namely VAT, corporation tax, income tax and NIC.

Comment: HMRC already offered 'time to pay' arrangements, but these were not well publicised. This new service is backed by a dedicated telephone call centre and is designed to help businesses affected by the current economic conditions.

5.2 The 'Taxpayers' Charter'

HMRC does not have a single document that clearly sets out the rights of taxpayers and the recipients of tax credits. There was an Inland Revenue Charter dating back to 1986, but this had no statutory backing and faded virtually without a trace. As part of the HMRC Review of Powers, Deterrents and Safeguards in January 2008, the Government announced that HMRC would work with interested parties to begin the process of developing a charter. There was a further comment on the charter in Budget 2008 and a formal consultation document was issued in June 2008. HMRC has reviewed the various responses received and, amongst the various supplementary materials released with the PBR 2008 documentation, there was a response document setting down the next steps for the charter.

The key point is that, in response to strong representations calling for the charter to have legal status HMRC has agreed that Finance Act 2009 will include a clause giving the charter explicit legislative authority. Other decisions on the charter are that:

- there should be a single charter (rather than several aimed at different 'customer' segments)

- the charter should be a high-level principles document with a link to HMRC standards of service to help customers measure performance

- the charter should be short, simple to understand and easily accessible

- the charter should cover customer rights and obligations but there should be no inference that they are mutually dependent

- the charter should clearly signpost where taxpayers and tax credit recipients can find information with respect to their rights to appeal against and obtain redress with respect to unreasonable behaviour by HMRC officials.

Given the wide ranging issues HMRC deals with, it has been decided that it would be inappropriate to refer to the final document as 'The Taxpayers' Charter'. Apparently 50 titles were suggested during the consultation process. HMRC has stated that it will continue to consider the title and take steps to ensure the eventual title is as representative as possible.

HMRC has invited stakeholders and staff members to be involved in the initial drafting of the charter. It is anticipated that the first draft will be released for public consultation early in the New Year.

Comment: We believe that the charter is a vitally important document which, if drafted correctly and with appropriate statutory underpinning could provide taxpayers with important safeguards. Accordingly, we welcome the announcement that the charter will have statutory authority. However, we cannot comment substantively until we have a draft of the charter and the proposed legislation. We believe that it is important that there should be independent oversight of the charter and would endorse the comments made by the Tax Faculty of the Institute of Chartered Accountants in England and Wales that there should be a regular review process 'which could be carried out under the aegis of a Parliamentary Select Committee'.

5.3 Anti-avoidance

The Government has previously consulted on the possible introduction of principles-based legislation to counter avoidance in connection with financial products. This consultation was seeking to establish whether a principles-based approach – rather than the continual introduction of detailed rules – may be a more appropriate way of countering avoidance in the area of financial products. It now plans to publish a further consultation document that includes draft legislation on disguised interest and transfers of income streams.

Comment: The recent change to capital gains tax (CGT) has produced a 22% differential between the higher rate of income tax and the flat rate of CGT. The proposal to introduce a new 45% income tax rate would increase the differential to 27%. This differential will undoubtedly cause the financial industry to seek ways to convert income returns into capital, hence the Government's determination to put a strong anti-avoidance system in place.

5.4. Offshore financial centres

The Government has announced an independent review of British offshore financial centres.

Comment: In his speech, the Chancellor referred specifically to the extent of compensation schemes for lost bank deposits, but it is possible that any review might also consider the lower tax rates available in offshore centres such as the Isle of Man and the Channel Islands.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.