WINDS OF CHANGE - GEORGE OSBORNE'S FIRST BUDGET AS THE CHANCELLOR OF A CONSERVATIVE GOVERNMENT BROUGHT SEVERAL SIGNIFICANT ANNOUNCEMENTS.

By Mark Wingate

Taking a leaf from the Labour Party's election manifesto, there will be a further tightening of the rules for non-doms. In an attempt to provide a more level playing field for those receiving remuneration from companies by salary or dividend, there is a revision to the way dividends are taxed. But one of the consequences of the withdrawal of the notional tax credit is greater taxation for higher rate and additional rate taxpayers with substantial dividend income.

Landlords will also see changes over the coming years, particularly concerning entitlement to tax relief for interest on borrowings on buy-to-lets. Amid so much change, there are pockets and windows during which you could maximise relief. There is currently such a window for contributions to pension schemes between now and 5 April 2016.

If you are the trustee of a charity you should be aware of changes to the definition of a fit and proper person included in the Charities Bill that is passing through Parliament. The Charities Commission will be able to disqualify unfit trustees and HMRC has a view on who is not fit and proper for this purpose.

CHANGES TO THE TAXATION OF DIVIDENDS - ONE OF THE MAJOR ANNOUNCEMENTS MADE IN THE SUMMER BUDGET CONCERNED THE TAXATION OF DIVIDENDS.

By Angela Hughes

Currently, UK dividends are notionally grossed up by 10% in the tax computation of an individual or trust, with this 10% tax credit deducted from the overall tax liability. From April 2016, this system will be replaced with a £5,000 tax-free dividend allowance per year, with any dividends received over this amount taxed gross (without the 10% notional credit).

Below are calculations showing the effect of the changes.

The new policy is expected to exclude the vast majority of ordinary investors from tax on their dividend income, with many others paying less tax. The Chancellor predicts that 85% of those who receive dividends will be better off. For any dividends received over the £5,000 limit, taxpayers will essentially pay an additional 7.5% of tax.

Who will and won't benefit?

As can be seen from the graph, certain investors will pay more: basic rate taxpayers receiving over £5,000 of dividend income will face an increased tax liability, as will higher rate taxpayers with dividend income over £21,667 and additional rate taxpayers with dividend income over £25,265. Under these levels, higher and additional rate taxpayers will be slightly better off.

Incorporated businesses: dividend v salary?

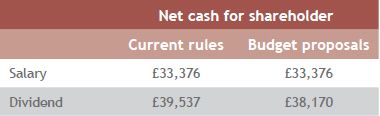

The new rules will make it less attractive for individuals to run their business through a limited company and take remuneration via dividends. Individuals who take low salaries and high dividends will be hit particularly hard. Although there will still be savings from taking dividends rather than a salary, even after the planned reduction in corporation tax rates to 18%, individuals drawing large dividends will be worse off.

A comparison of extracting £50,000 of profit by salary or dividend based on 2015/16 rates and allowances results in the following after-tax amounts.

What can I do?

Couples should contemplate reorganising their investments to ensure they use both tax-free allowances and dividends received over this level are covered where possible by lower rate bands rather than higher.

With increasing updates to the taxation of income, it could be worth using yearly ISA allowances to protect savings from any future changes.

In the short term, business owners may wish to consider accelerating dividend payments from 2016/17 to 2015/16 in order to take advantage of the lower effective tax rates (subject to levels of distributable reserves and expected marginal tax rates for each individual).

ALL CHANGE - NEW MEASURES FOR NON-DOMS AND OVERSEAS OWNERS OF UK RESIDENTIAL PROPERTY

By Susan Roller

The Government is making rapid reductions to the favourable tax regime for longer-term UK residents domiciled overseas (also known as non-doms). The increase to the remittance basis charge (RBC) to £90,000 for non-doms resident in the UK for 17 out of the previous 20 tax years will only be in point for the 2015/16 and 2016/17 tax years because the Chancellor announced more fundamental changes.

How will UK-domiciled status be applied?

The Summer Budget measures provide that from April 2017, anyone resident in the UK for more than 15 out of the previous 20 years will be treated as UK-domiciled for all UK taxes and the remittance basis will no longer be available to them. This significant change will mean that once an individual has been deemed to have UK-domiciled status, they will be taxed on worldwide income and gains while UK resident, with their worldwide estate subject to UK inheritance tax (IHT). The Government proposes to consult on the best way to deliver the reforms with a view to including legislation in the Finance Bill 2016.

Non-UK domiciled status to stay

For those resident in the UK for 15 or fewer years, the availability of the remittance basis and amount of RBC will be unchanged. The new rules will not abolish the non-UK domiciled status, but rather bring in a new deemed UK-domiciled status, which can be lost once an individual has been non-UK resident for more than five tax years.

Further measures will apply from the same date to those who have a UK 'domicile of origin' but have since acquired an overseas domicile of choice. Even if a person emigrated from the UK as a child and acquired a long-term domicile of choice abroad, this will be ignored for UK tax purposes if they resume UK residence. It will be essential to monitor the implications of the Statutory Residence Test introduced in April 2013 in order to ensure there are no unintended outcomes.

Bringing UK residential property under UK taxation

The Chancellor also proposed new rules from 6 April 2017 that will bring all UK residential property held directly or indirectly by non-UK domiciled individuals within the scope of UK IHT. This will include those residential properties typically held in overseas registered companies, often below an excluded property trust. This measure will be the final step in bringing UK residential property held by non-residents fully within the scope of UK taxation after already extending the charge to capital gains tax where a property sold after 6 April 2015 is held by a non-UK resident. Individuals who have not yet unwound their UK property-owning overseas structures should review this in light of these changes and the exposure to the increasing cost of the annual tax on enveloped dwellings.

THE GOOD, THE BAD AND THE REPLACEMENT - IMPACT ON LANDLORDS

By Toby Tallon

George Osborne announced a number of surprises for landlords in his July 2015 Budget.

The good: rent-a-room relief

For landlords renting a room to a lodger, there was good news as 'rent-a-room relief', the flat rate allowance that can be deducted from rental income from lodgers, will be increased from £4,250 to £7,500 from April 2016.

The bad: restriction on relief of finance costs

From April 2017, landlords liable to income tax will start to face a restriction on the effective tax relief they can claim on allowable finance costs. Instead of a straight deduction for such costs from rental, income from residential properties relief will be by way of a credit applied at the basic rate of income tax.

The mechanics to achieve this are more complicated than intimated in the Budget speech. In addition to the increased tax liability expected for higher rate (40%) and additional rate (45%) taxpayers the disallowance of a deduction against profits will mean some individuals will see their tax bills increase by more than the difference between their current marginal tax rate and the credit at 20%.

- The increase in income could mean crossing tax banding thresholds. For example, basic rate taxpayers could become higher rate taxpayers, higher rate taxpayers could stray above the £100,000 of income and see their personal allowance restricted or move into the additional rate band with the associated tapering of their annual allowance for pension relief.

- As well as the marginal rate of tax on the adjusted residential profits being higher, savings and dividend income could become taxed at higher tax rates than before.

- The relief will apply at the basic rate of tax but, for Scottish taxpayers, the Scottish basic rate applied to their income may not be 20% by April 2017.

Other important points to note from the proposals are as follows.

- The change will be phased in, starting from April 2017 with the disallowance and credit applying to 25% of the costs for 2017/18, increasing by a further 25% each tax year so that for 2020/21 it will apply in full.

- It will apply to individuals renting out residential properties. It will not apply to qualifying furnished holiday lets, corporate landlords or commercial properties.

- It will apply to partners in respect of finance costs within the partnership and for external borrowings used to fund a partnership residential property activity.

- We are awaiting clarification on the position for trustees and the trust's underlying beneficiaries, as this is not entirely clear.

- It applies to financing costs, not just mortgage interest. Hence if allowable refinancing costs are in prospect, taxpayers may wish to consider advancing them.

- Unused relievable finance costs can be carried forward against rental profits in future tax years. These will be usable, again subject to another calculation, after carried forward rental losses.

- The £50,000 cap on reliefs will not apply to unused finance costs relief.

The replacement: wear and tear allowance and replacement furniture relief

Another proposed change that is expected to take effect from April 2016 is the ability for residential landlords to claim 'replacement furniture relief'.

At first blush this could be seen as miserly and anti-simplification, as it will replace the relatively generous and straightforward 'wear and tear' annual allowance for furnished properties. However, the new relief will apply to landlords of unfurnished and part-furnished properties, as well as furnished properties, and also brings welcome clarity, for example, confirming relief for free-standing fridges.

Furnished holiday lets will continue unaffected and landlords remain able to claim capital allowances.

GREATER RELIEF FOR THE HOME - IHT NIL-RATE BAND EXTENSION

By Julia Rosenbloom

Chancellor announces an increased nil-rate band where a person's residence is passed on death to direct descendants. This will apply to deaths on or after 6 April 2017.

The increased nil-rate band will be in addition to the current nil rate band of £325,000 (which has remained unchanged since 2009/10 and will be frozen until 2021/22) and is to be phased in as follows.

After that, both the basic and additional nil-rate band will increase in line with the consumer price index. Any unused nil-rate band can be transferred to the surviving spouse or civil partner as with the basic nil-rate band.

IHT payable as a result of lifetime transfers will not benefit from this relief and the relief will be limited to one residential property. However, the personal representatives will be able to nominate which property qualifies if there is more than one in the estate, provided it was used as a person's residence at some point.

Restrictions to the relief

Not everyone, however, will be able to benefit, as estates with a net value over £2m will see this additional nil-rate band tapered away at a rate of £1 for every £2 over the threshold. In addition, it may prove difficult for unmarried couples to fully benefit from the change.

Measures are also proposed to preserve the relief where the individual has downsized or ceased to own a residence after 8 July 2015. The additional nil-rate band will then be applied to the value of the former home for assets of an equivalent value passed to descendants. This will be subject to consultation, which will be published in September 2015.

This is generally seen as a welcome measure, particularly for those living in areas of the country where house prices have pushed those with even moderate wealth into the IHT net. For those with greater wealth though, the changes may not provide any benefit at all.

As before, it's advisable to review your affairs carefully to ensure that you are taking maximum advantage of all reliefs.

CHARITY TRUSTEES - ARE YOU A FIT AND PROPER PERSON?

By Wilson Cotton

The Charities (Protection and Social Investment) Bill is going through the House of Lords and is on course to give the Charity Commission, the regulator of charities in England and Wales, the power to disqualify trustees.

The Charities Commission requires trustees to meet three tests and in its policy paper at: http://tinyurl.com/CCdisqual the Commission emphasises that it cannot exercise the power of disqualification simply because one of these conditions applied.

While most of the grounds for removal are to be expected, including misconduct or mismanagement of a charity, concern has been expressed at the role that HMRC may have in the process.

The origin of this lies in events surrounding the Cup Trust, an aggressive tax avoidance scheme that made use of charitable tax reliefs. The Charity Commission was heavily criticised for a failure of oversight by the public accounts committee of the House of Commons.

The tests

Test 1 includes "a person has been found by HMRC not to be a fit and proper person to be a manager of a body or trust". In its published guidance http://tinyurl.com/CharityF-P HMRC states, "it doesn't necessarily follow that individuals who are considered by a charity regulator to be suitable to act as trustees of charities will always be considered to be fit and proper persons for the purposes of the management condition... Factors that may lead to HMRC deciding that a manager (or trustee) isn't a fit and proper person include, but aren't limited to, where individuals....

- are known by HMRC to have involvement in attacks against, or abuse of, tax repayment systems

- have used a tax avoidance scheme featuring charitable tax reliefs or using a charity to facilitate the avoidance

- have been involved in designing and/or promoting tax avoidance schemes..."

A person who is dissatisfied with HMRC's decision can ask for it to be reviewed by a senior manager in the HMRC charities department, after which an appeal is made to the head of HMRC charities and ultimately to the adjudicator.

The Charity Commission then has to consider test 2 unfitness to act as a result of a failure in one or more of the following broad categories.

- Honesty and integrity

- Competence

- Credibility

Concerns about competence can include a failure to discharge certain duties in their personal or business affairs, while concerns about credibility include:

- negligence and repeated failure to comply with legal requirements on tax matters that has been penalised by HMRC

- support for and participation in discredited tax schemes.

This appears to set the bar to fall over quite low. It may be uneconomical for a taxpayer to appeal a penalty imposed by HMRC on the basis of negligence where in reality there has been a simple mistake. The phrase "discredited tax schemes" also needs explanation. Does discredited mean 'something likely to cause public outrage' or merely 'tested in the courts and held not to succeed'?

Test 3 is only relevant if the others are met and requires the commission to determine that the disqualification must be desirable in the public interest to protect public trust and confidence. In reaching such a decision, the commission must consider the nature and seriousness of the conduct and the extent of the unfitness and whether it might be temporary or time-specific.

Protections in place

Certain protections are built in. In exercising discretion the commission must ensure that any action taken reflects the principles of best regulatory practice under Charities Act 2011 s.16 and is proportionate, accountable, consistent, transparent and targeted only at cases where action is needed. Further, as a public authority it has obligations in terms of human rights and equality, and must consider the impact any order has on the person's rights. Appeal against an order is to the First-tier Tribunal (Charity).

A finding by either HMRC or the Charity Commission that someone is not a fit and proper person could cause significant reputational and professional damage to the individual concerned, as well as to the charity. It is therefore essential that the ground rules for its use are clear and unambiguous and that as a sanction, it is used sparingly.

TECHNICAL CORNER - BUDGET CHANGES TO THE PIP RULES

By Roger Perry

A small but important change to the pension rules was announced in the recent Budget, which allows for additional pension contributions (made between now and 5 April) over and above the current £40,000 annual allowance and benefit from tax relief.

The rules for calculating pension relief uses the concept of a 'pension input period' (PIP), i.e. the period over which pension contributions are made when considering the annual allowance.

Previously, the complicating factor was that PIPs did not have to match the tax year-end. So this meant calculations could get complex, especially in the case of someone with more than one pension and differing PIPs.

The Government has recognised the confusion this is causing, so from 8 July 2015, all PIPs were deemed to have closed. From this date PIPs will match the tax year (6 April to 5 April), which should make it more straightforward.

There are transitional rules that may allow for additional contributions to be made in excess of the annual £40,000 for 2015/16. In some circumstances, this could mean an additional amount of up to £40,000 of contributions (tax relieved), which can be made on top of the annual allowance amount.

For PIPs ending between 6 April 2015 and 8 July 2015 the annual allowance (ignoring carry forward amounts) is £80,000. Any of this £80,000 that is unused can be carried forward to the second part of the tax year (i.e. 9 July to 5 April), but up to a maximum of £40,000.

This is an unexpected bonus for those looking to maximise their pension contributions, particularly those additional rate taxpayers who will have their annual allowance reduced from April 2016. While these rules should make it more straightforward, for the transitional period it is important that these changes have been considered in full to ensure the maximum relief available is used.

We have taken great care to ensure the accuracy of this newsletter. However, the newsletter is written in general terms and you are strongly recommended to seek specific advice before taking any action based on the information it contains. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. © Smith & Williamson Holdings Limited 2015. code NTD264 31/12/15.