Foreword

This is a Deloitte Touche Tohmatsu (DTT) Technology, Media & Telecommunications (TMT) report. The DTT TMT group is made up of DTT member firm TMT practices around the world.

Uncertainties plague the media and entertainment sector. Which new technologies will catch on? Will any proposed solution for online piracy work? Which mergers and acquisitions (M&A) deals will win government approval?

Many executives deal with uncertainty either by making long-term commitments based on visceral hunches, or by trusting in their company’s ability to change direction rapidly in response to unforeseen changes. Hunches and agility work in some cases, but this report contends they are insufficient in today’s media and entertainment sector. Too much is at stake; the uncertainties are too great; the need to act is too pressing.

But if committing to one vision of the future is unwise and agility is impractical, how are you to formulate true strategy in the face of inescapable uncertainty?

Strategic Flexibility provides an answer. By combining scenariobased planning with real options concepts, it makes it possible for you to prepare for a future you can’t predict, and to do so in ways that increase your odds of success regardless of what tomorrow brings.

Igal Brightman

Global Managing Partner Technology, Media & Telecommunications

Introduction: When uncertainty met strategy

Corporate strategy in the media and entertainment sector is increasingly complicated by uncertainty. Key aspects of the marketplace are in flux, and even the most experienced executives disagree vigorously on the outlook. Even where there is agreement on the most likely outcome, the timetable is under debate. In the end, even the media industry – an industry that makes its living telling stories – is having difficulty figuring out the plot.

Witness the rapid changes in the scope and positioning of many leading media titans. In less than a decade’s time, organizations that first assembled a broad reach across many sectors of the industry are beginning to dismantle their own creations. Now, one view on these moves is that a decade is a long time, and that such activity represents a mere realignment in the face of changing circumstances – a defense that would have more merit if more had changed than simply the constantly evolving views of what the future will hold. In other words, at least some of this recent maneuvering wasn’t initiated in the past because of past circumstances, and isn’t being unwound today because of current circumstances. Instead, changes were largely driven by an attempt to gain position on a constantly shifting set of necessarily inaccurate predictions.

Why are the premises on which so many predicate their corporate strategy so often wrong? DTT’s view is that there are three key drivers of uncertainty: technology, intellectual property protection, and corporate structure. Consider each in turn.

Technology

Innovation in the technologies of content delivery and consumption creates both opportunities and perils. New developments range from the Internet to digital video recorders (DVRs), from 3G wireless video devices to satellite radio, and from broadband over powerline to home networking. The pace of technological advances and the rate at which consumers will adopt new technologies are major uncertainties, as is the shift in consumer behavior that we can expect to see as new technologies gain ground.

Will consumers continue their love affair with electronic gadgets that inform and entertain, or will they resist even the most innovative marketing? If they are receptive to new technology, which devices will consumers embrace, and over what time period? Will consumers prefer a TiVo next to their computer or will they want video on demand (VOD) built in to their cable or satellite system? Perhaps both? Neither? Will a new generation of smart, high-speed mobile devices further fragment media markets, thereby driving down ad rates?

Intellectual property protections

The copying of digital content has spurred raging controversy of late, as the boundary between fair use and piracy is subject to heated disagreement. It is yet unclear what response or mixture of responses industry and government will embrace. The future could be defined by government crackdowns, lawsuits, and strict legal enforcement. Alternatively, the industry could develop innovations in product design, marketing, and packaging that would make buying products and services far more attractive than stealing them.

How will the intellectual property wars turn out? Will embedded digital rights management (DRM) schemes and legitimate online sources of music and video, coupled with innovative marketing, curtail the industry’s losses to piracy? Or will lawmakers and regulatory agencies weigh in with ever more draconian sanctions? Will the recording industry’s strategy of suing downloaders prove effective? If so, at what cost, and on what schedule? Will hardware makers and content companies forge an alliance or part ways, driven by divergent market pressures? Surely, piracy is crippling to an industry that lives or dies by record sales, so to speak. But who can conceive of a future that is stifled by overregulation, in this enabling new era of information sharing? What kind of compromise, if any, will be reached?

Corporate structure

Government regulation upon ownership can either expand or contract the structural choices available to industry executives. The more that governmental policy permits companies in one segment of the industry to buy companies in others, the more companies are able to diversify and leverage the advantages of scope. If policy becomes more restrictive, companies must rely more heavily upon focus, thus emphasizing scale. Moreover, the extremes to which companies may pursue strategies of either scope or scale may be limited by ownership caps. In the end, thanks to the unpredictability of regulatory decisions, court orders, and legislation, getting a fix on what is and is not likely to be permissible is a difficult task.

At present there is little reason to believe that government policy is on a steady path. In the US, for example, the Federal Communications Commission’s (FCC) attempt at revising rules on industry cross-ownership has set off an as-yet unresolved controversy involving the courts, Congress, and the Administration. When a compromise finally emerges, how long will it last before the issue explodes once more? Will the US relax antitrust restrictions to encourage new investment in media properties? Or will they grow more stringent, based on concerns that two decades of consolidation across all media segments have already curbed competition? Will governments be receptive or resistant to additional mergers and acquisitions involving content providers and hardware makers? The outcome will certainly dictate the size and shape of the industry to come.

What does it all mean?

These and other uncertainties have led to divergent conclusions about how tomorrow’s marketplace will look. For, though no two companies would be expected to hold exactly the same expectations for the future, or to respond in exactly the same way, the sheer degree of divergence in the strategies being pursued by leading companies indicates similar divergence when it comes to expectations about tomorrow’s competitive landscape.

For example, some major industry players are pursuing vertical integration while others are focusing on one link in the value chain, implying conflicting assumptions regarding future governmental policy on ownership and the sources of competitive advantage. Certain new entrants have built their strategies around as-yet immature technologies, suggesting bold assumptions about their potential for overthrowing established content delivery models, regardless of scale and scope strategies embraced by industry leaders.

Some executives lack the time or the money to commit to a new corporate strategy. Still others believe that their companies can deal with any unexpected marketplace developments simply by being agile. Yet, even when this works, it tends to place stress on important relationships. After all, stakeholders such as customers, employees, suppliers, regulators, lenders, and investors base their relationships with a company on continuity, not on repeated and sudden change. In the real world, media and entertainment companies need to make long-term investments in infrastructure, technologies, relationships, and markets.

Alas, uncertainty is the natural enemy of strategy. But if uncertainty is the unavoidable context for many important decisions, is it hopeless to approach those decisions in a strategic way? The answer, of course, is ‘no.’ For those decisions that require commitment in the face of uncertainty, it’s important to find a way to ‘square the circle’ – to combine the strategic commitments that must be made with the flexibility made necessary by an unknowable future.

Strategic Flexibility: A paradox resolved

Strategic Flexibility makes it possible for companies to embrace uncertainty as part of the planning process without abandoning the benefits of commitment. Strategic Flexibility permits executives to prepare for a range of plausible, albeit unpredictable, tomorrows rather than being forced to commit to one specific version of the future.

Strategic Flexibility offers a rational alternative to agility. It empowers executives to realize the benefits of commitment without relinquishing the ability to respond to change. It involves choosing commitments that can be nurtured, adjusted, or abandoned. In this manner, a company no longer need presume an unknowable future. Instead, it may position itself to compete successfully no matter what the future holds.

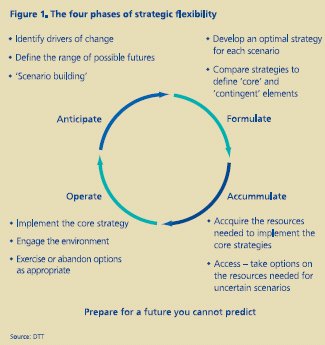

A company adopting the Strategic Flexibility approach develops and executes its strategy in four phases (see Figure 1):

Anticipate

The company first defines a set of scenarios that captures the range of plausible alternative future business environments. Scenario building provides a means to think logically and systematically about the future without either becoming paralyzed by the dizzying array of possibilities or deciding to bank on just one vision of what lies ahead.

Formulate

Next, the company devises an optimal strategy that addresses each plausible scenario. This requires thinking through all the resources necessary for the company to succeed, along with detailed assessments of the economic consequences of pursuing each optimal strategy. An optimal strategy can be thought of as a list of activities to be undertaken or resources to be acquired under a given scenario. The lists for the different scenarios are then compared so to identify which elements are common across multiple scenarios, as well as those elements that are unique to one scenario.1 The common items are core elements that figure in any strategy the company might pursue, whereas the unique items are considered contingent elements, essential for dealing with only a particular scenario, should it materialize.

Accumulate

During the third phase, the company makes whatever investments are required to prepare for the common elements among scenarios. In addition to these safe bets, it also must invest in contingent elements. Even though they satisfy conditions that may never materialize, deploying only core elements isn’t enough to fully implement any strategy. To be successful under any likely scenario, a company should first deploy both the core elements and the contingent elements demanded under those conditions.It is obvious that no organization could afford the effort and expense that would be required to fully arm itself for each and every scenario. Accordingly, the company makes use of ‘real options.’ These are small, initial investments that create the right, but not the obligation, to make further investments in the future.2 Real options offer a way to allocate resources that both respect current competitive pressures and copes with future uncertainty. This report will offer insights into how real options can be a powerful strategic tool in addressing the operational complexities that so often prove difficult when companies attempt to translate theory into practice.

Operate

The final stage in achieving Strategic Flexibility is to implement the core elements of the company’s strategy while also managing the contingent investments as a portfolio of options. The company exercises, abandons, or preserves the options as unfolding events provide clues as to which scenarios are actually materializing, and therefore which assets and capabilities will be needed for an appropriate strategic response. The entire process is repeated when new conditions emerge and existing scenarios and real options must be modified or replaced. After all, the future never really arrives; nor does preparing for it.

Overview

This report begins by defining five scenarios that capture plausible future business environments that might be in store for the industry. In DTT TMT group’s experience with scenario planning, it has been found that it is useful to assign a name to each scenario. As such, in the example that follows, each scenario has been labelled with a movie name that (wryly) describes the situation: Basic Instinct, Necessary Roughness, Almost Famous, The Quick and the Dead, and The Wizard of Oz. Five scenarios will be defined that capture plausible future business environments that may be in store for the industry.

Referring back to the drivers of uncertainty, three variables shall form the basis for the scenarios: (1) whether consumers will embrace or resist new technologies for content distribution and consumption; (2) whether online piracy will abate due to government sanctions or market-based innovations, and (3) whether government authorities will tend to permit or reject M&A transactions in the media and entertainment sector.

This report will show how scenarios may be validated by identifying real-world corporate strategies that match a company’s likely response if it believed that a particular scenario was, in fact, imminent.

Finally, this report will describe how each of the companies in the example could equip itself to deal with scenarios other than the one it seems to be banking on by making limited, incremental investments that may ratcheted up or down as new developments unfold.

The notion of contingent investments, a portfolio of financial options, is one of the key aspects of the Strategic Flexibility approach. Such investments, though reflecting a minimal expense, position a company to deal with a particular set of opportunities and challenges while also providing the ability to exit if the right conditions do not materialize.

Using the movie metaphor, this report ultimately will illustrate how media companies can reduce dependence upon the elements of any one ‘future’ by concurrently arming themselves for other plausible scenarios. This report shows how Strategic Flexibility permits you to be strategic and flexible at the same time: You position your company to deal with a whole range of possible futures, but then hone in on only what you need for the future that actually arrives. By the time your competitors start preparing for a new tomorrow, you’re already there.

Phase I: Anticipate

Thinking about an unpredictable future in an ordered, clear way requires that the introduction of some terminology for talking about the future, and about the relative probability that different futures will actually occur.

The term imaginable is used to designate the least constrained ideas about what tomorrow might bring. Only logical contradictions are off-limits. Wild-eyed hand waving is encouraged, as it helps to ensure that nothing is missed. Include every uncertainty that comes to mind: ad rates, technical standards for home networking, government policy, global unrest, and so on.

From this starting point, it is crucial to reduce all imaginable outcomes of a wide variety of specific issues to a reasonable number of possible, i.e. specific and coherent, scenarios. This process begins by identifying uncertainties that demand commitment to specific courses of action in advance of being able to resolve them. It is crucial to differentiate between those uncertainties for which alternative, and less onerous, responses are possible. For example, an organization can typically respond to labor unrest in real-time, because contract negotiations begin long in advance of a strike threat. Barring wildcat action, it is reasonable simply to sense and respond to this particular uncertainty as it unfolds.

With a shortened list of high uncertainty/high commitment unknowns, the second tactic for whittling a universe of uncertainties down to digestible bites is to identify common threads running throughout the shortened list. These commonalities allow the identification of ‘drivers of change’ that capture a range of related uncertainties.

There is no single right way to reduce multiple uncertainties to a few drivers of change. In the end, it is a judgment call that must first be considered very carefully, if only because getting it wrong may evoke enormous penalties. More specific techniques for scenario building are available in a number of good how-to guides.4

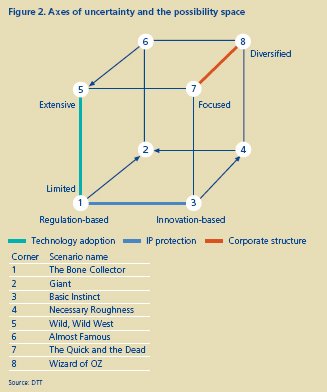

For example, this report has settled upon three drivers of change that represent a small sampling of the many possible key uncertainties facing media and entertainment companies: technology, IP protections, and corporate structure (see Figure 2). These drivers, or axes of uncertainty, will form the basis of this report’s illustrative set of plausible scenarios.

Each of these drivers will be considered largely in isolation, and the ‘extremes’ identified. With respect to the three drivers showcased in this report, the DTT TMT group has defined the extremes as depicted (as vertices) in Figure 2 and addressed in the ensuing discussions..

IP protection (blue x-axis)

The ways in which companies capture the value of their IP is bounded by a ‘regulation-based’ extreme in which governments protects big media and entertainment companies from the millions of ‘pirates’ who have no qualms about illegally downloading or otherwise capturing print, audio, or video content for their own use. Criminal prosecutions and costly civil suits are the primary enforcement tools. Companies focus their initiatives on legislatures and courtrooms.

At the other extreme, IP protection is achieved through ‘innovationbased’ solutions. These are technological, packaging, delivery, and/or marketing innovations that increase demand for legal access to content – thus quelling the appeal of piracy. At this end of the IP protection axis, companies focus their efforts on the laboratory – where they develop appealing interfaces and ways to make copying increasingly difficult, and on the marketplace – where they add value to their products in ways that render piracy prohibitively difficult or uneconomical.

Technology (green y-axis)

One extreme of the technology driver is ‘limited adoption,’ a future marketplace in which there has been little change from today’s conditions, in which content is delivered via free-standing devices such as stereos, TVs, and portable content delivery technologies such as iPods and PSPs (PlayStation Portable). Widespread at-home broadband access stalls, and in-home networks remain the province of technophiles.

The other extreme of ‘extensive adoption’ represents a world in which consumers are highly adaptive and allow technology into their lives with an accepting attitude rivaled only by TV’s Jetsons. Ubiquitous broadband networks deliver vast amounts of digitized content to the home, where it is distributed, stored, and accessed via smart devices linked through a dynamic home network.

Corporate structure (red z-axis)

Here the extremes are ‘diversified’ and ‘focused.’ In a future world in which a diversified approach prevails, the most successful media and entertainment companies are those that have adopted an integrated structure, collecting under one corporate roof an assortment of businesses that collectively own all or many of the stages in the value chain, from content creation through delivery.

At the opposite extreme, the value chain would be modular. In this scenario, companies seek to identify the point in the value chain that represents the key to success given consumer demand, and they focus on doing that activity well while also building scale.

Considering all eight possible futures as viable candidates for the Formulate phase is still unworkable. There’s simply too much to do and too much operational complexity involved in driving eight or more scenarios through the Accumulate and Operate phases.5 Hence, there is one more step – that is, getting from ‘possible’ to ‘plausible.’ That is, of all possible futures, certain scenarios are sufficiently plausible to merit the kind of preparatory investment required by Strategic Flexibility. Likewise, there are scenarios that are probably ‘implausible’ – scenarios that involve intersections of the three example drivers that yield an unrealistic theoretical environment. As you might suspect, such an environment would not warrant extensive planning.

As this report moves through discussions of plausible and implausible scenarios within the context of this example, this report will further illustrate and discuss scenarios and the logic behind the labels that have been bestowed.

Building scenarios

Taken all together, the drivers of change yield a three-dimensional ‘possibility space’ within which the actual future may fall. Such an analysis allows the move from ‘imaginable’ futures to ‘possible’ ones by reducing a budding, buzzing confusion to a manageable foundation for strategy making.

To bring the three axes of uncertainty to life, each of the eight corners has been given a movie title name – to help conger up the nature of reality that could emerge.

Plausible scenarios

One way to gain insight into the plausibility of scenarios is to look to companies that appear to have adopted strategies corresponding to actions an organization would take if it believed in a given scenario. That is, if a major company’s strategy seems aligned with the assumptions underlying a particular scenario, this supports the assumption that the scenario itself is sufficiently plausible to merit serious consideration.

Of course, this test is merely suggestive, not definitive. After all, the company may be building a strategy based on flawed assumptions about the future, thereby lending false credibility to an unrealistic scenario. Alternatively, it is entirely possible that a scenario warranting careful consideration could be overlooked by all industry players. For present purposes, however, this approach serves as a valuable ‘reality test’ for the generic scenarios developed here.

The test has been applied, summarized in Table 1 and the text below, by identifying actual (though disguised) companies pursuing strategies that appear to be most appropriate to conditions defined by particular scenarios bounding the ‘possibility space’ of Figure 2.

Basic Instinct (Corner 3, see figure 2)

The scenario represented by Corner 3 is a future marked by limited technology adoption, innovation-based IP protections, and restrictive government policy on corporate structure. This report has dubbed the Basic Instinct scenario. What real-world corporate strategy would validate this as a realistic scenario? One example is a freestanding record company that appears intent upon growing within that segment of the value chain while making its content available through a variety of online distribution channels (See Table 1).

Necessary Roughness (Corner 4)

The Necessary Roughness scenario resembles Basic Instinct in that there is limited technology adoption and IP protection is achieved through commercial innovation. Unlike Basic Instinct, however, there are few structural constraints. Necessary Roughness depicts a future in which media and entertainment companies don’t see their business transformed by technological advances. They turn to innovation to solve piracy and achieve growth through diversified acquisition. An example of a real-world strategy that lends credence to this scenario: a media conglomerate lining up a big joint venture for its record company.

Almost Famous (Corner 6)

This scenario is unlike the first two in that it anticipates extensive technology adoption and regulation-based IP protection. However, in the Almost Famous scenario, there are limited structural constraints. For an actual case that authenticates this scenario, consider a large cable TV company that seeks to add to its content holdings while introducing a VOD offering to try to block DVRs from wrecking the business model on which its distribution-content strategy has been built.

The Quick and the Dead (Corner 7)

The Quick and the Dead presumes a dynamic, turbulent marketplace in which conditions favor focused companies and entrepreneurial upstarts. Technology adoption is extensive, innovation-based solutions to piracy are more successful than government sanctions, and restrictive government policies on corporate structure impede industry leaders who try to leverage their vertical integration. A freestanding DVR service provider would appear to be counting on this version of the future.

The Wizard of Oz (Corner 8)

This scenario in part duplicates The Quick and the Dead in that technology adoption is extensive and innovation-based methods of IP protection prevail. It differs in that government is permissive rather than restrictive with respect to corporate structure. Support for this scenario can be found in the strategy of a media conglomerate introducing a VOD service employing a new datacasting technology platform and a previously untried subscription arrangement.

|

Table 1. |

|||

|

Disguised industry archetype |

Observed behavior |

Most likely to succeed when |

These conditions describe |

|

Independent record company |

• Assigns low priority to developing ties to companies at the bleeding edge of new distribution and consumption technologies. • Has license agreements and otherwise collaborates with online distributors such as MusicNet, Pressplay, Full Audio, Bestbuy.com, and Listen.com’s Rhapsody service. • Pursues M&A aimed at gaining scale economies in record business (horizontal integration) but resists joining or forming a conglomerate active in multiple segments (vertical integration). |

• Technology adoption: Limited • IP protection: Innovation-based • Corporate structure: Significant constraints |

Basic Instinct |

|

Conglomerate’s music joint venture |

• Shares ownership of its record arm, implying it doesn’t think it will need the ability to introduce proprietary synergies between music and hardware in response to technology upheaval. • Launches online digital music service and supports similar industry efforts, e.g., PressPlay and MovieLink, to develop copy-protection technologies for CDs and DVDs. • Undertakes a large music joint venture, implying it assumes government won’t oppose further industry consolidation. |

• Technology adoption: Limited • IP protection: Innovation-based • Corporate structure: Limited constraints |

Necessary Roughness |

|

Cable company seeking content |

• Introduces network-based technologies that provide consumers with more control over their viewing, to co-opt new DVR capabilities offered by satellite rivals and others. • Supports legal sanctions to deter consumers from accepting technologies that defeat or bypass its new system and thus enable copyright violations. • Pursues new acquisitions of content providers to augment its existing portfolio of national cable networks, implying it assumes the government won’t block such transactions. |

• Technology adoption: Limited • IP protection: Innovation-based • Corporate structure: Limited constraints |

Almost Famous |

|

Free-standing DVR service provider |

• Offers DVR service, which depends on consumers using new technology to watch TV in non-traditional ways. • Impliedly counts on DRM solutions that along with new compensation methods will maintain the industry’s economic viability while letting consumers pick and choose via DVR. • Survival arguably depends on government keeping large integrated companies from co-opting, buying, or crushing an upstart DVR service provider. |

• Technology adoption: Limited • IP protection: Innovation-based • Corporate structure: Limited constraints |

Quick and the Dead |

|

Conglomerate’s VOD service |

• Uses new technology platform and subscription model, implying faith that consumers will accept a new approach to renting in-home movies. • Incorporates DRM and extra security, suggesting it believes government sanctions will prove ineffective and/or counterproductive. • Creates its own delivery system, implying it thinks government will allow vertical integration in the movie business. |

• Technology adoption: Limited • IP protection: Innovation-based • Corporate structure: Limited constraints |

The Wizard of Oz |

Exhibit 1. Naming the five plausible scenarios

Naming scenarios is more art than science, and much underappreciated. Good scenario names capture the essence of a given set of conditions and provide an invaluable shorthand for discussing strategy and assessing the implications of current events. Borrowing from the movie industry, below is the provenance of the scenario names.

The Quick and the Dead

1995

Columbia/Tristar Studios

Starring: Gene Hackman, Sharon Stone

In a gun fighting tournament of all against all, there are only two ways to leave town: victorious, or in a pine box.

Faced with rapidly changing technology and limited diversification options, media and entertainment companies have to master the tools of their respective trades in order to stay one step ahead of the mortician.

Basic Instinct

1992

Artisan Entertainment

Starring: Michael Douglas, Sharon Stone

Trying to smoke out a suspected killer, a San Francisco detective finds his ruin and his redemption by listening to his most basic instincts.

Unable to rely on new technologies or new approaches to their value chains, the key to survival lies in focusing on the basics.

Necessary Roughness

1991

Paramount Studio

Starring: Scott Bakula, Hector Elizondo Unable to recruit the most talented players from America’s high schools, a college football program must rely on the players it can find within the existing student body.

Free to pursue scale or scope strategies, but with limited adoption of new technologies, the most attractive response seems to be to work within existing industry boundaries to bulk up and dominate the competition without the help of radically new business models.

Almost Famous

2000

Dreamworks SKG

Starring: Billy Crudup, Kate Hudson, Jason Lee

The bittersweet tale of a rising rock band that can’t come to terms with its own incipient success, ultimately flying apart in the accelerating centrifuge of fame and fortune.

Upstart firms make a run at the incumbents but prove unable to cope with the ability of entrenched, well-resourced, diversified conglomerates to create new business models on the back of rapidly changing technology.

The Wizard of Oz

1939

Warner Studios

Starring: Judy Garland, Frank Morgan, Margaret Hamilton

Dorothy and her companions – Tin Man, Scarecrow, and Cowardly Lion – embark on a perilous journey to find the Wizard of Oz: a great and powerful magician who can solve all their problems.

Consumers turn to large, diversified conglomerates who command the resources and the expertise necessary to make technological wizardry affordable and available.

Implausible scenarios

Just as crucial as the creation of scenarios that seem plausible and thus worthy of strategic focus is the elimination of scenarios that are sufficiently implausible. The following are those scenarios this report decided to eliminate, along with the rationale for doing so.

The Bone Collector (Corner 1)

This scenario is marked by limited adoption of technology, regulation-based IP protection, and significant structural constraints. The scenario would play out as though media companies facing low technology adoption and regulatory constraints on scope would pursue regulatory relief from piracy, hunkering down to focus on protecting their core business. Of course, this seems implausible owing to the fact that focused companies would have the advantage in creatively solving the piracy problem and would likely turn to innovation without the size and clout to lobby as effectively as their large, diversified competitors. Therefore, this scenario collapses into Basic Instinct.

Giant (Corner 2)

Giant is marked by limited adoption of technology, regulation-based IP protection, and limited structural constraints. With little room for growth through technology adoption, companies seek to protect existing revenue through piracy regulation and to grow revenue through diversified acquisition. However, if technology adoption is limited, broadband adoption is also likely slow. Thus, piracy would be less threatening and media and entertainment companies would not need to invest significant resources in regulatory solutions. Additionally, it seems unlikely that government would both allow vast scale and crack down on digital downloads. If policy were liberal on structure, government would probably tend to allow the market to address the IP protection problem.

Wild, Wild West (Corner 5)

This scenario is marked by extensive technology adoption, regulation-based IP protection, and limited structural constraints, and ultimately collapses into The Wizard of Oz in the following manner: With extensive technology adoption and limited structural constraints, there would be ample opportunity for firms – large incumbents, focused firms, and new entrants alike – to explore innovation-based solutions to IP protection. In this report’s formulation of that world, innovative conglomerates have the upper hand. However, in the event that larger firms rest on regulationbased IP protections and seek to dominate the market by their sheer size, the rapid adoption of technology would provide niches for more focused companies or new entrants to develop innovationbased solutions and outmaneuver their larger competitors. This is a Wizard of Oz world, but one in which larger firms cede the high ground to more innovative adversaries.

Exhibit 2. Naming the three implausible scenarios

In the interest of completeness, here are the stories behind the names given to the scenarios that DTT’s TMT group ultimately decided were implausible.

The Bone Collector

1999

Universal Studios

Starring: Denzel Washington, Angelina Jolie, Queen Latifah

A bed-ridden detective must use what limited data can be gathered for him by a reluctant and inexperienced crimescene photographer to decipher the cryptic clues left behind by a brutal killer.

Media and entertainment companies have little to rely on: new technologies are slowly embraced if at all, and regulatory restrictions make it difficult to explore new value chain configurations.

Giant

1956

Warner Brothers

Starring: James Dean, Elizabeth Taylor, Rock Hudson

A Texas-based oil baron uses his wealth to thwart the ambitions of his life-long rival.

With new technologies slow to emerge and regulatory remedies to IP proving adequate, media and entertainment companies grow through acquisition and diversification. The result is a large but slow, plodding, and unimaginative leviathan.

Wild, Wild West

1999

Warner Bros.

Starring: Will Smith, Kevin Kline, Salma Hayek

A pair of mis-matched government agents does battle with an evil genius who relies on over-engineered and ultimately vulnerable steam-powered engines of war.

With rampant advance on the technological frontier, entrants and focused companies seize the opportunity to send overwrought diversified incumbents to their doom.

End of Part One

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.