Introduction

Hydrocarbon resources are typically owned by the state. The task of exploring for and developing these resources is often delegated by the state to an international oil company ("IOC") (sometimes acting in conjunction with a nominated domestic participant) that possesses the specialist expertise and financial resources necessary to undertake the task. The relationship between the state and the IOC is regulated by a legal instrument that specifies the rights and obligations of each party. The primary purpose of the instrument is to address the tensions inherent in the relationship between the state and the IOC; in particular, the allocation of risk between the parties and the provision of incentives to the IOC to accomplish the state's objectives.

While a certain level of risk is inherent in any commercial undertaking, the oil and gas sector is distinctive in terms of the significant levels of investment required for exploration and production of hydrocarbons, and the often high degree of uncertainty surrounding the ability to profit from such investment. Prior to attempting to extract hydrocarbons from the subsoil, seismic exploration and exploratory drilling must be carried out in order to determine the existence of resources sufficient to make the project commercially viable. Unfortunately, more often than not a commercial discovery will not occur, in which case it will not be possible for the IOC to recover the often substantial costs incurred by it. Even if a commercial discovery is declared, significant uncertainty surrounds the actual cost at which the hydrocarbons can be extracted, developed and produced.

The regimes developed to govern the relationship between the state and the IOC can, in general terms, be classified as licences, concessions, production sharing agreements ("PSAs") and service contracts. The regimes are actually similar in that they all require the IOC to shoulder exploration costs and risks. They vary in how they define ownership of hydrocarbons and production and associated facilities and fiscal systems: licences and concessions impose a tax/royalty-based fiscal system, while PSAs and service contracts follow a cost recovery and profit/fee-based system.

While a detailed examination of the four regimes is beyond the focus of this article, it is interesting to note that most of the hydrocarbon developments made in the first half of the 20th century were made under concession regimes. During this period the IOCs were believed to have the greater power. Since the middle of the 20th century, power has shifted from IOCs to states. This shift has also coincided with the development and increased use of PSAs. Today, more than 50% of the hydrocarbon exploration and production world follows some form of PSA regime. Even countries like Russia and Brazil, with concession regimes, introduced parallel PSAs for their biggest discoveries. This article briefly summarises the key terms prevalent in PSAs and analyses the debate currently taking place in India regarding the most appropriate PSA model.

Production Sharing Agreements

A PSA creates a contractual relationship between an IOC and the state, authorising the IOC to explore for and exploit hydrocarbons in a defined area and for a defined period. The state, as the owner of the hydrocarbons, hires the IOC as a contractor for the conduct of exploration and production work and the IOC incurs all of the costs associated with the business of exploring for and producing hydrocarbons within the geographical area defined in the PSA. If a commercial discovery is not made then these costs will not be recoverable by the IOC from the state. The PSA establishes the agreed compensation that the IOC will receive for services rendered, which will be in revenues from the sale of resultant hydrocarbons. The IOC will have a contractual right to be delivered a portion of the hydrocarbon production, which becomes available (usually after treatment and processing) at a pre-agreed point in the export pipeline. IOCs will usually book their PSA reserves in-ground, though whether such reserves can be booked or not will depend on the terms of the PSA.

Parties

The parties to the PSA will usually be the state (acting through the relevant ministry or government official), often but not always, the state oil company (which will take delivery of the state's share of production) and the IOC (as contractor). If the contractor under the PSA is a consortium of IOCs, then one of them is designated as the operator. In some countries, once a commercial discovery is made, the state party has the option to take over the role of the operator (e.g. in China), or to operate jointly with the contractor through a joint venture company (e.g. in Egypt).

Ownership of assets

Typically, all movable and fixed assets acquired by the IOC for the operations immediately become the property of the state party. The IOC is able to recover purchase costs from the cost hydrocarbons and retains the use of such assets only for operations. As a result, contractors usually use subcontractors for their drilling and other operations and, where possible, lease rather than purchase equipment and installations.

Commitments and operational control

In order to ensure that the IOC is "working the land", the PSA will prescribe the minimum work and expenditure commitments. Given that only a small number of exploration efforts actually lead to a commercial discovery, the work commitment and financial obligations are crucial negotiation factors as they define the extent of the exploration risk. States will want to draft these with as much specificity as possible while IOCs prefer commitments that allow maximum discretion.

Supervision and/or management of operations by the state is usually achieved through (i) the requirement to obtain the state's consent for certain key decisions; and/or (ii) the establishment of a management committee where both the state and the IOC(s) are represented. The management committee will typically approve investments, annual work programmes and budgets and any declaration of commercial discovery.

Legislative gaps

A PSA often provides an extensive contractual framework tailored to the specific circumstances of the field, the IOC and the business environment. The PSA's terms may be confined to hydrocarbon exploration, development and production (if the prevailing laws are fully developed), or may cover a range of other issues such as the right to import and export goods, work permits, foreign exchange, health and safety, taxation, planning and environmental issues. In this sense, the PSA can be used to plug gaps in the overarching regulatory system, which, for the purpose of legal certainty, can be particularly useful (to both the state and the IOC) where the legal system is less developed. The PSA could also necessarily be light in the relevant areas.

Division of hydrocarbons

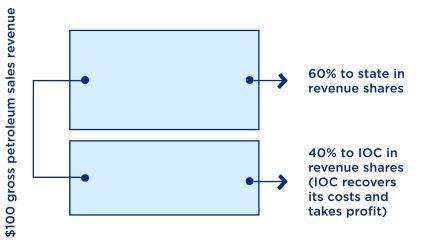

The most critical element in the PSA is the division of the hydrocarbons produced, which in its most basic form has two components: cost recovery and profit sharing. The cost recovery mechanism in the PSA allows the IOC to recover its accrued costs, where a commercial discovery has been made, from gross revenues resulting from the sale of hydrocarbons. After the cost recovery phase has ended, or simultaneously with the process of cost recovery (depending on what is agreed in the PSA), the IOC and the state will share hydrocarbon sales revenues according to agreed profit shares.

In addition to a share of profits, however, there are a number of other economic routes through which the state takes a share of the production:

- Royalties – royalties to the state payable through royalty hydrocarbons (that is, a tranche of production set aside for royalty payments).

- Bonuses – signature and/or production bonuses which may be imposed by the PSA or enshrined in the prevailing law.

- Fees – rental fees payable on the acreage available under the PSA. " Taxes and duties – income taxes, petroleum taxes, customs duties and/or VAT.

- State participation – the option to participate in the venture. This does not imply that the state will share in the exploration costs and risks. Most PSAs require the IOC to carry the state, which means that the IOC bears all the exploration costs. If the field is declared commercial, the state then has the option to participate in the production revenues.

- Domestic market obligations – an obligation imposed on the IOC to sell hydrocarbons domestically, in order to satisfy domestic demand for hydrocarbons. While some PSAs specify that a certain percentage of the production has to be made available for the domestic market, others give the state a more general option to require a sale of up to 100% of the IOC's profit hydrocarbons should the domestic market require this.

Cost recovery

There are several ways in which the interface between cost recovery and profit shares can be structured:

- Full cost recovery, deferred profit shares: Gross revenues from hydrocarbon sales are first applied towards the IOC's accrued costs without imposing any limits on cost recovery. The profit pool is shared only after the IOC has recovered all its costs. The state's share can be extremely low (and could even be nothing) after the IOC has recovered all costs.

- Full cost recovery, deferred profit shares, with first tranche hydrocarbons: First a pre-agreed tranche of the gross revenues is split between the state and the IOC, before remaining revenues are applied towards reimbursement of the IOC's accrued costs, again without imposing any limits on cost recovery. As with the previous model, the profit pool is shared only after the IOC has recovered all its costs (but subject to the first tranche).

- Capped cost recovery, simultaneous profit shares: In any defined period (usually annual), the gross revenues from hydrocarbon sales are first applied towards the IOC's accrued costs up to a pre-agreed cap. Once the cap is hit for the year, then the remaining gross revenues are distributed between the state and the IOC according to the agreed profit shares for the remainder of that year. Accrued but unrecovered costs are carried forward to successive periods and the same process is repeated.

- First tranche hydrocarbons, capped cost recovery, simultaneous profit shares: This a hybrid of all the above models. First a pre-agreed tranche of the gross revenues is split between the state and the IOC, before remaining revenues are applied towards reimbursement of the IOC's accrued costs up to a pre-agreed cap. Once the cap is hit, the remaining gross revenues are distributed between the state and the IOC according to the agreed profit shares.

Profit sharing

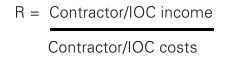

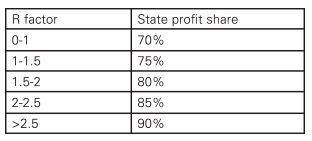

PSAs also vary in how they deal with the profit shares. The share ratios could be set as fixed percentages for the lifetime of the PSA or as a progressive (or upwardly increasing) scale designed to increase the state's participation levels as the underlying project attains greater levels of daily production. Another way of creating a sliding scale of profit shares is the use of what is popularly known as an R factor (or Ratio factor). The R factor is arrived at by dividing the revenues from a project by the costs of that project, as below:

and then ascribing a particular profit share which is payable to the state to each band of the resultant R factor calculation.

At the start of the project, costs inevitably outweigh revenues and so the R factor will be zero or low. As the R factor increases (that is, as revenues increase, and increasingly outweigh costs in the later stages of the project), then the profit share in favour of the state increases. Thus the equilibrium of the original agreement is maintained, because as the net profitability of the IOC increases, the IOC's profit share reduces.

The Indian saga

There is a heated debate taking place in India regarding the most appropriate PSA model to be used, which highlights some of the key tensions that can arise between the state and the IOC under a PSA.

In the 2000 New Exploration Licensing Policy (NELP) bid round in India, Reliance Industries Limited (Reliance) and NIKO Resources Ltd (NIKO) were awarded the KG-D6 Block under a PSA that capped cost recovery. The consortium made its first gas discovery in 2002, which was the largest gas discovery in the world that year and India's largest since the 1970s. Production in KG-D6 commenced on 1 April 2009 and peak output of 69.43 mmscmd was reached in March 2010. Today, production stands at 80% below peak. In February 2011, BP bought a 30% stake in 23 PSAs operated by Reliance across India, including the KG-D6 PSA, for $7.2bn (reducing Reliance's stake to 60%). In 2011, the Government of India (GoI) disallowed cost recovery under the KG-D6 PSA on the grounds that Reliance was in breach of its obligation thereunder to comply with the development plan. In November 2011, Reliance commenced arbitration proceedings against the GoI.

There are a number of underlying factors that are relevant when considering the dispute between Reliance and the GoI, namely:

- Reliance's claims that the decline in production was due to the geological complexity of the KG-D6 Block;

- the dispute between Reliance and the GoI about gas pricing and the accusations that Reliance was wilfully under-producing because of the low gas price;

- the high costs of exploration and development in the global oil industry which resulted in high costs under the KG-D6 PSA; and

- the accusation by the GoI and the populist view that IOCs under PSAs in India had been gold-plating their costs.

In 2012, the GoI constituted the Rangarajan Committee under the chairpersonship of Dr. Rangarajan, Chairman of the Economic Advisory Council, to inter alia look into the existing PSA cost recovery and profit sharing mechanism. In its report, the Rangarajan Committee recommended shifting to a revenue-sharing model. The state's share would commence from the first day of production (rather than post-cost recovery as under the present model) and the GoI and the relevant IOC would share revenues according to a predetermined formula. The committee suggested that the revenue share should be determined by competitive bidding for future PSAs, with the company offering the highest share to the state getting the block.

Following the Rangarajan Committee's recommendations in relation to gas pricing, in 2013 the GoI formed the Kelkar Committee (led by former finance secretary Vijay Kelkar) to suggest a roadmap for cutting import dependency in the hydrocarbon sector by 2030 (and to give its views on the recommendations of the Rangarajan Committee, although this task was later removed from the terms of reference). The Kelkar Committee proposed two alternative solutions (both based on the current PSA model):

- Model 1: PSA linked to an Investment Multiple (IM) model with modified contract administration. This model included minor tweaks to the administration of the current model so that the managing committee and directorate general of hydrocarbons would focus only on standards and best practices, without assessing costs. Oversight would be left to the tax authorities, who were already responsible for overseeing other forms of state take such as royalties and taxes.

- Model 2: Modified PSA with supernormal profit tax model. Under this model, the GoI take would comprise only of royalty payments and corporate income taxes until supernormal profits were triggered. The GoI therefore would have no right to any share of production, but would simply receive profits and taxes when profits were limited; and when profitability crossed a certain threshold, a supernormal tax would kick in, providing a much higher state take. The threshold rate could also be a biddable item. This model eliminated the need for detailed calculations and disputes on true costs and profit hydrocarbon shares.

Revenue Sharing — an Alternative to PSA Cost Recovery?

The most popular criticism of the PSA regime globally is that the priority facilitation of the IOC's recovery of costs could lead to IOCs inflating their costs in order to increase their share of cost hydrocarbon – otherwise known as "gold-plating".

There are a myriad ways in which an IOC can increase its costs under a PSA for example by (i) accounting fraud; (ii) improperly allocating costs to the PSA, for example by allocating costs from one PSA to another; (iii) improperly procuring services and goods on a non-arm's length basis, including from affiliates; and (iv) over-invoicing. The reality is that these practices can be detected through diligent audits. States, including the GoI, have a number of rights under their PSAs through which they can audit the costs of the IOC, not least through their participation in the management and/or operating committee. Another and more subtle form of gold-plating is where the IOC inflates its spending in order to enhance the profitability of the field. This is an extremely subjective analysis and imposing strictures that prevent the operational freedom of the IOC may not be in the interests of the state, as it may deter future investment.

The often mentioned alternative to the cost recovery-profit sharing model is the revenue sharing mechanism (also proposed by the Rangarajan Committee) found in the Peruvian and early Libyan PSAs. The revenue sharing model does not allow any separate cost recovery, royalty or taxation of the IOC. The hydrocarbons produced or gross revenue is split between the IOC and the state in accordance with a pre-agreed percentage. Since the IOC has to recover its costs from its share of the gross revenues, the revenue sharing model by definition incentivizes the IOC to keep costs low. The IOC recovers its costs from its share of the hydrocarbons and the state does not attempt to otherwise chip away at the IOC's take. The revenue sharing model on the face of it seems particularly attractive to India, with its inefficient bureaucracy, because it does away with the need to audit costs.

However, there are several perceived disadvantages to the revenue sharing model. The IOC is extremely vulnerable to changes in market prices which affect revenue and recovery and in a period of low prices, the IOC might be inclined to shut in hydrocarbon production and to wait for higher prices to materialise. The revenue sharing model does not incentivize IOCs to invest in higher cost or marginal fields. Much of the criticism of the Rangarajan Committee's recommendations centered on the fact that a revenue sharing mechanism is not suitable for India as the country's sedimentary basins are poorly explored and their prospects remain uncertain. Under a revenue sharing model, IOCs bidding to participate would likely only put in very low bids (that is, high IOC take and low state take). The GoI's total take under the cost recovery-profit sharing PSA is currently around 70%. With sedimentary basins that are less attractive than the Gulf countries (which use a revenue sharing model), it would be almost impossible, to achieve this take for the GoI.

Criticisms of the Indian PSA (and other cost recovery PSAs) often ignore the reality that IOCs are in a country to make a profit and not merely recover their costs. This is not to say that IOCs never become lazy or gold-plate their expenses. As suggested by the Kelkar Committee the solution for India (and countries in a similar situation) is not a shift to a revenue sharing mechanism, but better management of the PSA and diligent exercise by the state of its rights under the PSA. However, as this issue went to print the Indian Government announced its new licensing regime, the Open Acreage Licensing Policy, which we understand will controversially abandon the current PSA in favour of revenue sharing.

What Next?

The PSA debate in India is not the first and will not be the last of its kind. Historically, once any resource or field-related uncertainties have been resolved favourably and/or if the state receives lesser proceeds from production than expected, it is quite common for it to take a bigger piece of the cake. In such circumstances, the reputational consequences of appearing to be an unreliable business partner will seem comparatively less significant for the host state. For example, the first wave of PSAs in Indonesia were reworked in favour of the state following the oil price shock of 1973 because the Indonesian government realised that the IOCs were earning higher than expected profits under the existing PSAs.

In the last decade, we have seen Russia and Brazil introduce or redesign their PSA regimes in controversial circumstances. In Brazil, following the significant pre-salt discoveries in 2007, the government made a case for a move from the prevailing concession system to a PSA system. The concession system, it argued, worked for the state when the extent of hydrocarbon resources were not clear and given that the pre-salt discoveries had removed that risk, a PSA regime would provide the state with a higher take. The new PSA provided that Petrobras (the state oil company) would be appointed as the sole operator and would hold a minimum participating interest of 30% in each new block within the pre-salt and strategic areas. This was in sharp contrast to the concessions for non-presalt projects, where IOCs are largely uninhibited by the state in exploring and producing. The PSA also required payment of a signature bonus of $6.6 billion and a low-cost recovery cap. The 2013 pre-salt auction was observed globally with much anticipation, not least because of the speculation in the press that no IOC would participate. State officials celebrated the single (and winning) bid from a consortium made up of Petrobras (40%), Royal Dutch Shell (20%), Total (20%), CNPC (10%), and CNOOC (10%). However, now both the state and the non-operating IOCs were dependent on financially and operationally strapped and scandal ridden Petrobras to lead the development as operator. Unsurprisingly, work has already begun to modify the PSA regime for future pre-salt auctions in order to incentivise IOC participation.

The PSA regime was established in Russia under the Federal Law on Production Sharing Agreements of December 30, 1995 in parallel with the prevailing licensing regime (Federal Law on Subsoil Resources of February 21, 1992) in order to encourage foreign investment in geographically isolated and technologically complex hydrocarbon projects. Three large PSA projects, Sakhalin I, Sakhalin II and Kharyaga, followed. These three rounds were signed at a time when IOCs had a strong position in the negotiations and consequently, the conditions included were favourable to the IOCs. Against a backdrop of increasing energy prices, the Russian government grew dissatisfied with the existing PSA projects. This led to a series of amendments to the PSA Law in 2003 which, in effect, forced potential PSA operators either to switch to the licensing regime under the Subsoil Law or abandon the projects altogether. Although Sakhalin I, Sakhalin II and Kharyaga were made exempt from this regime change, when Shell (the operator of Sakhalin II) announced in 2006 that project costs would increase, the Russian government withheld its approval. Subsequently, the state renegotiated the Sakhalin II PSA and ultimately took a 51% stake in the field. Long before western sanctions were imposed against Russia (due to the Ukraine crisis), IOCs such as BP were disinvesting and the Russian government was promising the return of the PSA in order to encourage investment. However, any debate about the return of PSAs or the economic terms that are necessary in order to attract investment has been suspended until sanctions are lifted.

The assumption in any upstream regime debate is that countries with large reserves can afford to impose whatever terms they desire and IOCs will continue to bang on the door requesting entry. Russia and Brazil are examples of how IOCs can lose interest in a country where they have no protection against future opportunistic behaviour by its sovereign counterparty. India, and countries like Mexico that are looking to redesign their upstream regimes, should be cautious and ensure that their desire to maximize the state's return must be balanced with the need to provide incentives for investment and the security of a stable regulatory environment.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.