- within Environment topic(s)

In the first in a series on how key principles of insurance law have been developed recently by the Courts, Patrick Perry explores the issues surrounding notification of circumstances.

Requirements for notification

Determining when the insured should notify a circumstance, what that notification should (and does) comprise, and whether a subsequent claim attaches back to that notification can give rise to a number of issues.

From the insured's point of view, if it fails to notify properly, it risks a subsequent claim not attaching back to the relevant policy and falling outside of cover. From the broker's perspective, the courts have held there is a positive obligation on a broker to"...get a grip on the proposed notification, appraise it and ensure that the information was relayed to the right place in the right form." (Alexander Forbes v SBJ (2002) QBD). If the broker fails to do so, it can face a claim in negligence. For insurers, they need to understand the scope of the notification early, assess whether it complies with the policy terms, and what the consequences of it may comprise. A "blanket notification" can cause significant problems, and lead to concerns over a very large and unknown exposure potentially attaching to the policy (often just before expiry).

Most professional indemnity policies operate on a claims made basis, that is to say they provide cover for claims which are made against the insured in the policy year, even though the alleged negligence may have occurred in earlier years. A typical notification clause will include provision along the lines that

- There must be a circumstance;

- Of which the insured is aware;

- That is 'likely to' or 'may' give rise to a claim;

- That the insured has notified in accordance with the requirements of the policy.

Any claim which may subsequently be made against the insured arising out of that circumstance is then deemed to have been first made against the insured during the policy period. This "deeming" provision gives a valuable benefit to the insured by enabling him to attach a subsequent claim to the present policy. Without that provision, the insured would be placed in an impossible position, as it would be required to disclose on renewal a situation which had not yet become a claim, but which would then likely be excluded from cover.

What is a circumstance?

The majority of policies do not seek to define a "circumstance". In general terms, it is a matter which, objectively evaluated, creates a reasonable and appreciable possibility that it will give rise to a loss or claim against the insured. A typical "circumstance" would be a complaint by a client, or a threat to potentially bring a claim, but one which has not yet evolved into an actual claim (which is normally defined as a formal demand for damages). Another example of a circumstance would be a realisation by the insured that his advice or services had been negligent and that a claim may arise as a result.

Awareness

There are two keys parts for a matter to comprise a notifiable circumstance. The first is that the insured must be subjectively aware of the circumstance, as illustrated to the important English Court of Appeal decision of Kidsons v Lloyds' Underwriters (2008) ("Kidsons"). The second is that circumstance must objectively be sufficiently material that it is likely to, or may, give rise to a claim (subject to the wording).

Awareness is a matter of fact. There are three important practical consequences for the insured:

- The insured cannot notify a circumstance if it is not aware of it;

- Once the insured is aware, time starts to tick for notification purposes, subject to the notification provisions of the Policy;

- If the insured fails to notify the circumstance, it is likely to comprise material information which the insured would be required to disclose on renewal of the policy. If it failed to do so, the future policy may be void for non-disclosure, or the subsequent claim could fall to be excluded.

The awareness required is the awareness of the insured itself. Where the insured is a corporate entity or a partnership, difficult issues of attribution can arise. If a junior employee of a company receives a letter of complaint from a client, but tells no-one about it then, as a general proposition, his knowledge is unlikely to be attributed to the insured company for the purposes of such a clause. At the other end of the spectrum, knowledge by the board of directors will clearly suffice, and knowledge of one director alone may also be sufficient. Where the knowledge is held by an individual in between these two extremes, difficult questions of attribution can arise, which are very fact sensitive.

"Awareness'' of a circumstance may arise from what are known as internal or external "triggers". The latter, such as a letter of complaint from a third party, is generally far easier to judge as being sufficiently material to give rise to a notifiable circumstance.

In Kidsons, the trigger for the notification was internal. Concerns were voiced by the insured's tax manager that various tax avoidance products which the insured had marketed were fundamentally flawed.

The judge in Kidsons was concerned that an internal misgiving by the insured alone could be a sufficient trigger for notification, finding that there should be "a substratem of underlying fact over and above [internal] concerns". He stated:

'I am doubtful that an insured's own concern, without more, that he may have made a mistake is a relevant circumstance which can entitle him to give notice of circumstances, thus extending his claims made policy into future years: otherwise every insured could extend his policy indefinitely simply by a notification based on his own lack of confidence'.

He went on to compare this to the example in Thorman v New Hampshire (1987), a case concerning an insured who was an architect; 'A typical example would be a belated realisation, based upon a study of professional journals, that perhaps he had specified inadequate foundations for a building which he had designed and which had already been erected'.

The Judge thought the 'significant qualification' was that the architect's concerns were 'based upon a study of professional journals', and so comprised an external source. In reality, we would see the distinction between an insured who becomes aware that their advice may have been negligent based upon something they had read and something they chanced to remember when thinking about their work to be very slight.

In Rothschild v Collyear (1999) the trigger was external. The insured was a financial adviser who had been giving pensions advice. The Securities and Investment Board had commissioned a report by accountants which highlighted a potential problem for the industry. The publication of this report, coupled with a letter from the insured's regulator, was held to be a circumstance capable of notification, even though none of the insured's files were involved in the review.

In the English Court of Appeal case of McManus v European Risk (2013) ("McManus") there was a mixture of internal and external triggers following the acquisition by a firm of solicitors of another practice:

- claims were received from former lender clients;

- an internal review was conducted by the firm which identified similarities in other files;

- a case review was conducted by an external compliance consultant which identified systemic issues;

- a further internal review supported the compliance consultant's findings;

- disciplinary proceedings were undertaken against two former partners of the prior firm;

- general internal concerns existed regarding systemic malpractice and negligence in the former firm.

It was held that these factors could constitute a notifiable circumstance.

Likelihood of circumstance giving rise to a claim

The Policy will usually stipulate that the circumstance to be notified is one which is 'likely to' or 'may' give rise to a claim. The differences in the wording can be significant.

'Likely' means:

- at least 50% likelihood of a claim occurring (Layher v Lowe (1996) CA);

- that it is "probable" or "more likely than not" (Laker Vent v Templeton (2009) CA).

'May' means:

- 'at least possible that a claim will result' (Rothschild v Collyear (1998) QB)

- 'a real as opposed to a fanciful risk of underwriters having to indemnify insured' (Aspen v Pectel (2009) QB)

The question of whether a circumstance is something which "might" or is "likely" to lead to a claim is to be construed objectively (Kidsons).

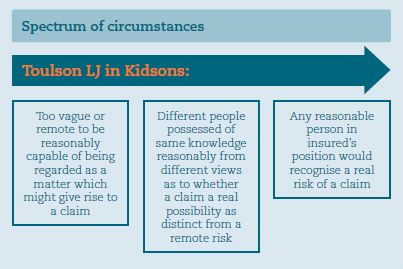

Spectrum of circumstances

The Court of Appeal in Kidsons recognised that it is not always easy to judge the materiality of a circumstance at a given time. The court gave an example of the spectrum of circumstances which can arise:

In McManus it was confirmed that the Courts can use hindsight when considering if a circumstance was sufficiently material to be capable of notification. A consequence of this is that if insurers reject a notification because it is considered too uncertain, and a claim does subsequently arise, it may be difficult for insurers to argue that the insured was not justified in notifying it at the time.

Form of notification

Unless the policy otherwise provides, there is no particular form in which a circumstance has to be notified against insurers. The form of notification, as per Kidsons, is recognised as a "loose and undemanding test" and the insured can notify:

- in different document to standard form

- in a series of documents

- by way of presentation

Where, however, the policy expressly provides that a notification must be in a particular form, that should be followed by the insured. For example, if a policy requires written notice, then oral notice will not suffice – as per Wong Wink Tak v Euro-America Insurance Ltd [1995].

The content of the notification

In Kidsons the Court of Appeal held that, although an insured has to be subjectively aware of the circumstances it is seeking to notify, valid notification had to be considered objectively, with regard to the factual context in which it is made.

The question is how, on an objective appraisal, a reasonable recipient with knowledge of the terms of the policy and the overall context, would have understood the communication that was actually made. What is required is identification of some act or omission, and of a potential plaintiff or class of plaintiffs. Importantly, the test is not:-

- What did the Insured intend to present?

- What did the Insurer understand?

It is purely an objective assessment of the contents of the document.

Blanket notifications

A "blanket notification" is a notification of an extremely broad problem, potentially without identifying the necessary plaintiffs or the specific problems experienced. It can cause a number of concerns, particularly when made shortly before expiry of the policy period, when its purpose would appear to be to ensure the policy attaches to the widest range of potential claims, known or unknown. Insurers can then be left with an unquantifiable, but potentially very large exposure, on an earlier policy year.

In Kidsons, the Court of Appeal overturned the controversial "laundry list" of requirements that the judge at first instance had imposed as to the requirements of a notification. Instead, the Court of Appeal were willing to adopt a less onerous approach.

This topic was addressed in McManus. In this case, 9 days before the end of the policy year, the insured law firm purported to notify problems affecting a prior practice it had acquired, and attached a list of an estimated 5,000 client files. The prior practice was a small High Street residential conveyancing firm. Following the acquisition a number of claims were received from former clients. An investigation revealed a number of apparently systemic issues. The notification set out these issues. The list of 5,000 files was essentially the prior practice's entire historic matter list.

The insurers accepted, as validly notified, the files specifically identified in the audit as having been shown to have problems, but the general concerns and the 5,000 client file list was rejected as failing to identify in each case a specific occurrence, act or omission which could give rise to a claim (in relation to an individual file). The insured sought a declaration that the notification was valid (in its entirety). This was somewhat unusual, as there were no claims against which to test the notification, but the insured was concerned that with the problem unresolved, it could become uninsurable.

The Court considered and applied the Court of Appeal's authorities of Rothschild and Kidson. On the facts, the Court made the finding that the insurers were wrong to reject the 'blanket notification' because it did not identify a specific problem with each individual file. This therefore upheld the legal position that there is no absolute legal requirement at the time of notification to identify the particular transaction or possible plaintiff.

The implications of McManus are that:

- The Courts do not support a too stringent test as to the form and contents of a notification.

- Unless the policy wording says something different, there is no requirement at the time of notification to identify:

- A specific transaction;

- A possible claimant; or

- A potential issue with each transaction.

- Essentially notifications can be made by category where there is sufficient basis for concern affecting a statistically high proportion of the individual matters within a category.

Timing of the notification

Many policies contain an obligation upon the Insured to notify a circumstance (or claim) within a certain time period.

The consequence of a failure to comply with the notification provisions depend upon whether the provisions are conditions precedent to insurer's liability or not:

- Conditions precedent – generally a breach of a condition precedent will entitle the insurer to deny liability for the claim, without the need to establish any prejudice.

- Not conditions precedent – the remedy for breach of a notification provision is damages. The effect of Friends Provident v Sirius (2005) is that if a condition is not classified as a condition precedent, practically speaking the obligation to pay the claim remains, no matter how grave the insured's breach and no matter how seriously they have been prejudiced.

Damages can be very difficult to prove. A rare case where damages were awarded by the court for breach of a notification provision is Milton Keynes BC v Nulty (2012). The insurer lost the chance to carry out investigations following a fire at the insured's premises. Although valuation of the loss of chance was 'fraught with difficulty', the judge concluded prejudice to insurer should be assessed at 15% of the policy limit of the indemnity to be set-off against insured's claim. The judge based this on a 'matter of impression'.

In terms of how the different timing obligations operate, the Courts have construed these as follows:

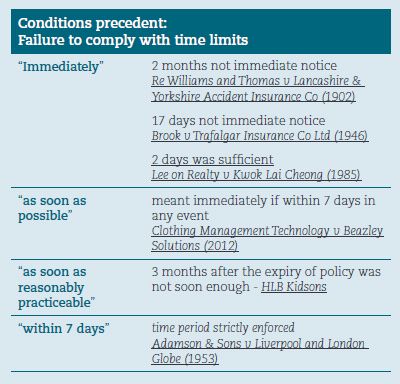

"Immediate"

In Hong Kong, the word "immediate" has been said to mean "with all reasonable speed considering the circumstances of the case." In Lee On Realty v Kwok Lai Cheong [1985] it was held that a delay of two days in the insured forwarding a summons to appear in court following involvement in a motor accident was not a breach of an immediate notification clause because the notification was with "all reasonable speed".

"As soon as practicable"

This form of wording has come before the courts on a number of occasions, and it is clear from the decisions that what is at stake is whether the insured has acted reasonably given all the surrounding circumstances of the loss. The leading authority is Verelst's Administratrix v Motor Union Insurance Co. [1925] in which the insured's accident policy required notice of any loss to be given to the insurer "as soon as possible" after it had come to the attention of the insured's representative. The insured's death in a motor accident became known to his personal representative soon after its occurrence, but the existence of the policy was not discovered by the representative until a year had elapsed from the insured's death. The court construed the words "as soon as possible" as applying not just to the fact of the insured's death, but also to all the surrounding circumstances of the case, including the ability of the representative to discover the existence of the insurance. On this reasoning, the claim was held not to have been out of time.

Verelst was applied in Fong Wing Shing Construction Co. Ltd v Assurances Generales De France (HK) Ltd [2003]. This case concerned a condition precedent claims notification clause in a Contractors All Risks policy requiring the insured to notify potential claims "as soon as possible". The insured was notified of an intention to sue for damages following injury, and informed the insurers the following day. The accident itself had occurred two years earlier. It was held that that insured did not know of the accident, and accordingly there was no breach of the clause.

By contrast, delay which is within the control of the insured or which is excessive in the circumstances will render his claim time-barred.

In Chan Yiu Sun v Yip Kim Cheung [1990] the policy contained the words:

"in the event of any occurrence which may give rise to a claim under this policy, the insured shall, as soon as possible, give notice ..."

The insured was involved in a motor accident in which others were injured, but he did not notify the insurers until he was prosecuted, which was some time after the accident. The Judge found the delay inexcusable. Notice had not been given "as soon as possible" and the insurers were entitled to decline the claim.

Practical considerations after notification

The concern for insurers, upon receiving a potentially problematic notification, is that they do not waive their rights or become estopped from relying upon a policy point.

The English Court of Appeal case of Kosmar Villa Holidays plc v Trustees of Syndicate 1243 (2008) should however provide some comfort for insurers. The case concerned a failure by the insured, a specialist tour operator, to notify its insurers of an accident until more than a year after it happened, in breach of a condition precedent clause under the policy. The insured argued that the insurers had waived their rights to rely upon the breach, as there was a delay of 2 months between notification and insurers' declinature, based upon a breach of condition precedent. The Court of Appeal disagreed and held that insurers were entitled to a reasonable time to get to grips with what was clearly a serious and lately notified claim, and that the questions asked by insurers demonstrated that insurers were still in the process of assimilating the circumstances of the claim.

The Court went on to observe that:

"It would not be good practice for insurers to rush to repudiate a claim for late notification, or even to destabilise their relationship with their insured by immediately reserving their position - at a time when they were in any event asking pertinent questions about a claim arising out of an occurrence about which they had long been ignorant in the absence of prompt notification."

Similarly, in McManus, the Court of Appeal held that insurers are entitled, when faced with a blanket notification, to adopt a "wait and see approach". In those circumstances, insurers do however need to consider reserving their rights or using appropriate wording so that it is clear cover is not being affirmed.

Scope of the notification and causal connection to the claim

It is important not to confuse the effectiveness of the notification with the scope of the notification.

The purpose of notifying a circumstance is to obtain the benefit of the "deeming" provision within the policy, namely where it provides that any claim which may subsequently be made against the insured arising out of that circumstance is then deemed to have been first made against the insured during the policy period.

The key issue here is that the claim that is subsequently made has to arise out of the circumstance. Any claim which is brought has to be critically examined for this purpose against the scope of the original notification.

Claims must have a causal connection to circumstances notified not just a mere connection.

In Kajima UK Engineering Ltd v Underwriter Insurance Co Ltd (2008) the judge held that, although it was possible for specific or general circumstances (including a "hornets' nest" or "can of worms" type of circumstance) to be notified, there had to be a causal rather than coincidental link between the notified circumstances and the later claim. This meant that a later claim arising from other circumstances which were discovered after notification will not be within the scope of the original notification.

In Kajima, the insured erected a five-storey block of flats consisting of pre-constructed pods. In February 2001, the insured notified to insurers the fact that the pods were "settling and moving excessively causing adjoining roofing and balconies and walkways to distort under differential settlement". Thereafter it became apparent that there were serious structural problems with the building as a whole, and by the end of 2005 it had become clear that the entire building had become unstable. Ultimately the insured was forced to purchase the building. The judge held that the later problems fell outside the scope of the initial notification. The notification was effective only in respect of the specific notified circumstances and did not extend to damage unless such damage was causally linked to the notified circumstances. The insured was accordingly under an obligation to make further notifications as and when further problems were identified.

An interesting point in Kajima was whether an investigation can be a circumstance. In that case the insured had notified various defects and added that an investigation was presently underway to identify or confirm the cause and the potential effect of the risk. The insured sought to argue that the subsequent defects which emerged were all part of the ongoing investigations, and the factual "continuum" from 2001 onwards. This was rejected by the judge who considered that the investigation referred to was an investigation into the notified defects and that it was not a separate notified circumstance in itself. This meant that if the investigation unearthed, as it did, other separate defects these new defects would not be within the notification.

Checklist for consideration of circumstances

- Does the policy prescribe a particular form of notification of a circumstance?

- Does the policy set out to whom, and from whom, a notification has to be made?

- Is the insured "aware" of the matters giving rise to the circumstance as at the time of notification? Is it an internal or external trigger? Awareness is a subjective test.

- When did the "awareness" arise, and is it attributable to the insured (as a corporate entity, for example)?

- Has any requirement to notify a circumstance within a particular time period been met? Is the obligation a condition precedent?

- Is the requirement that the circumstance is "likely to" or "may" give rise to a claim? Objectively speaking, does the materiality of the circumstance meet this threshold test?

- What would a reasonable recipient have understood the contents of the notification to comprise? Is the notification sufficiently certain and does it comply with policy terms?

- Does the claim that has been made arise out of the circumstance notified? Is there a sufficient causal connection?

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.