Executive summary

"…we have reason to believe that we have actually begun the long anticipated European retail banking cross-border consolidation process which, if it follows the US path, could result in hundreds of European banks disappearing."

1. Cross-border retail banking boom underway.

In the past two years, eight of the 12 financial services mergers above $3 billion (USD), with a European domiciled firm as the acquirer, have been cross-border retail banking transactions. As the European banking market enters new and previously uncharted waters – the completion of large-scale, cross-border, retail banking mergers – the question of whether this is an anomaly or the start of a longer-term trend takes on increasing urgency. Although annual predictions of an impending surge in retail banking cross-border mergers have often come to nothing, we have reason to believe that we have actually begun the long anticipated cross-border consolidation process. To date, cross-border banking deals have been constrained by perceptions of hostility from consumers and regulators, combined with more promising in-market growth and value creation opportunities for most banks. For reasons listed below, we believe this is changing.

2. Political, cultural barriers to pan-European mergers and acquisitions (M&A) eroding.

The unspoken understanding that national bank regulators would work to frustrate the acquisitive ambitions of non-domestic banks is fast fading. The fact that cross-border retail banking deals in Italy, Germany and the UK have all been completed in the past 15 months indicates an openness among the continent’s biggest economies that was only dreamt of in the past. This recent trend toward increased openness is given even more force as the EU’s commissioner for internal markets continues the investigation into financial services merger barriers following the Bank of Italy’s involvement in the recent acquisition of Banca Antonveneta by the Dutch bank, ABN AMRO. These political trends become more potent when commingled with the evidence of an increased willingness on the part of consumers to purchase financial services products from non-domestic institutions. Retail bank consumers’ openness to ‘foreign’ banks is evidenced in small ways, such as the rebadging of Barclays’ Spanish subsidiary, Banco Zaragozano, as Barclays, and is being propelled by gaping price discrepancies across different domestic markets for identical baskets of retail banking services. Taken together, we see cross-border banking mergers gathering momentum as the previously deal-breaking forces of political and cultural resistance crumble, even if tax differences persist.

3. Bank executives searching for double-digit growth.

Most bank CEOs are hard pressed to find organic growth opportunities of sufficient size to please investors’ profit growth demands. With most banks having undergone massive restructuring to strip out costs and continually scouring their operations for additional savings, the only real routes are through mergers or radical organic expansion in the range of activities into investment banking, private banking or insurance, or some combination of these. Most domestic markets, however, are too concentrated to allow a large competitor to bid for another major player. This leaves cross-border M&A as the most likely outlet for executives’ growth ambitions.

4. Market participants scrambling for supremacy.

Playing the cross-border merger game will require banks to stake out new banking territory aggressively. However, banks face a very real check on their ambitions in the form of their newly assertive institutional shareholders as evidenced by some recent deals that have been undercut by shareholders unconvinced of the deals fundamentals – for example, Deutsche Borse’s bid for the London Stock Exchange. In order to gain the consent of shareholders to engage in cross-border mergers, banks need to demonstrate the following: experience working across borders and cultures; skill in seamlessly integrating acquisitions; clearly articulated plans regarding how value will be created; regional operating and IT platforms that work.

5. US banking experience provides an outline of future European consolidation.

While we recognise the dangers of drawing conclusions from the US experience, given cultural and political differences, the fact is that the United States is the only other large, fragmented banking market that has undergone massive consolidation. Using simple comparative economic analysis, and the fact that the US market began consolidating earlier than did the EU, it is possible to get a glimpse of the future by looking across the ocean. What we see in the US market are a few very large, transcontinental retail banks – Bank of America, Wells Fargo, JP Morgan Chase, etc – competing with a variety of more traditional medium-sized and local banks and specialists. We believe that the European banking market will develop along similar lines with a few retail behemoths serving consumers across the entirety of the continent, while medium-sized and local banks, along with specialist providers continue to thrive in their niches. Additionally, the eventual winners in the banking consolidation game are those that get big quickly by buying large, established banks in new markets, integrating quickly and repeating the process. Equally important, however, is to execute each merger flawlessly so that the bank’s overall market capitalisation rises in line with the asset base.

Predictions and recent events

"We anticipate that by 2010 a handful of retail financial services firms will operate across the breadth and length of Europe."

More than five years after the introduction of the Euro on 1 January 1999 and 16 years after the collapse of the Berlin Wall, cross-border retail banking mergers are finally beginning to create pan-European financial services institutions. Although we have seen the emergence of pan-European corporate banking competitors in investment banking, syndicated loans and investment management, following previous sector specific consolidation, cross-border consolidation in retail financial services has not yet happened. Indeed, Chief Executives have found acquiring branch networks across borders a far more daunting prospect – that is until now.

We anticipate that by 2010 a handful of retail financial services firms will operate across the breadth and length of Europe. These institutions will have world-class scale and efficiency and while large components will be built organically, they will be created through cross-border mergers – the opening round of which is already in motion. If US trends are anything to go by, hundreds of European banks will disappear in the next five years.

The prime driver of consolidation is the pressing need to generate earnings growth in an environment where organic growth is hard to come by; economies of scale are now more realisable too. Although this desire for growth is tempered by the mixed shareholder value creation record of retail banking deals, there is a dawning realisation among investors that highly efficient, operationally sound banks have a tremendous opportunity to ‘roll-up’ poor performers in other countries via cross-border M&A. Of equal importance with the economic drivers behind these pan-European deals are the eroding barriers to cross-border financial services mergers. Indeed, political opposition to non-domestic acquirers is retreating as the European Commission actively seeks to break down national barriers to consolidation and European consumers are much more open to purchasing products and services from non-domestic institutions.

This confluence of increasing economic pressure and eroding barriers is resulting in a surge of cross-border retail merger activity in financial services. After many years of surprisingly few deals, the pace of cross-border retail/universal banking mergers has recently accelerated. Over the past 21 months, from the beginning of 2004 through the third quarter of 2005, eight of the 12 acquisitions of $3 billion or more by European financial services firms have been cross-border retail banking deals, as shown in Exhibit 1. These broader economic forces, coupled with the recent surge in deals lead us to conclude that these recent acquisitions actually mark the start of a gathering trend toward the birth of pan-European retail financial services providers.

Earning the right to play

In order to undertake a cross-border merger and acquisition strategy, financial institution executives need to gain the blessing of their newly assertive shareholders. A number of financial services institutions now have highly efficient operating platforms, with cost/income ratios of 50% or lower, which they can introduce to the institutions they acquire, leading to considerable savings. The ‘efficiency gap’ between these institutions and the least efficient is now considerable, creating a number of cross-border acquisition opportunities. Many have proven records for integrating acquisitions, either domestically, in the European market, or outside of the EU and still others have won the confidence of shareholders through years of careful stewardship and consistent profitability. Only those institutions which have some combination of efficient operations, a track record of successful consolidation, or experience working across borders can earn the right to participate in the coming consolidation. In contrast, private equity houses are embarking on transactional deals, designed to buy individual business lines or assets, strip costs or create scale and capture gains through a further sale or from more efficient operations.

But cross-border mergers do not make sense in all areas of retail financial services. While skilled acquirers can extract scale-related synergies from banking businesses with branch networks and relatively straightforward products such as deposits, credit cards, mortgages and mutual funds, there are fewer easy synergies to be had in the more complex product areas such as life assurance.

For life assurance companies, national personal tax regimes and strikingly dissimilar savings habits in different countries mean that it is harder to identify and realise efficiencies from pan-European mergers. Similarly, we do not expect a wave of pan-European mergers among general insurance companies, although we may see some strategic acquisitions where they make sense.

Indeed, we believe that a current lack of profitability and looming capital issues will first spur continued domestic rationalisation in both of these sectors, possibly being followed by cross-border deals. See page 12 for details on insurance.

Looking forward, the number of financial services mergers in Europe is unlikely to match 1999’s peak, but the scale of the cross-border deals underway, and on the horizon, means the total value of M&A activity should approach 1999’s levels, with a handful of large banks carrying out sizeable mergers. The process of pan-European consolidation will be intermittent, as an institution makes an acquisition, integrates it, and then makes the next acquisition. The need to fully integrate and ‘digest’ each new acquisition explains why the current consolidation period will stretch out over a period that could be as long as five years.

Finally, these deals will likely all take the form of outright acquisitions, rather than mergers of equals, given the difficulty of creating value without a single partner in charge. As noted by Abbey CEO, Francisco Gómez-Roldán at the Fitch Ratings global banking conference in London this summer, "We don’t believe in (mergers of equals). They are defensive in nature and unlikely to create value." But there were "Darwinistic selective acquisitions" that had the potential to create value under certain conditions and the Abbey purchase fell into this category, he said. From the buyer’s perspective, Mr Gómez-Roldán said, there must be a clear retail business model to export, transferable IT systems and spare management capacity 1

UK building societies

Twin challenges arising from cross-border M&A

Since building societies are mutually owned, and therefore outside the reach of traditional merger and acquisition activity, most industry commentators downplay the impact that broad cross-border consolidation activity will have on building societies. However, just because building societies apparently fall outside the cross hairs of acquisitive competitors doesn’t mean this broader trend will bypass building societies completely. Instead, we see two strategic implications for building society executives arising from pan-European banking consolidation:

- An opportunity to seize customers while competitors are distracted While the rest of the industry’s executives are focused on being hunters, not prey, building societies have the opportunity to make significant inroads into the high street bank’s existing customer bases. building societies often enjoy greater trust with retail customers and, in many instances offer more cost competitive products. Focused marketing effort to target the customers of rival banks as, and when, they are embroiled in a deal will be a critical determinant of growth.

- A need for greater efficiency The large High Street banks are actively seeking scale economies in their internal operations. Increasing M&A activity will push average costs lower across the industry as inefficient competitors are driven from the business. This, in turn, will put pressure on building societies to reach for ever greater efficiencies to allow them to continue to offer low cost, value for money products to their members. While many building societies will adapt to the cost pressures by sharing certain services to gain efficiencies, it is likely that some will be unable to respond adequately to the intense competitive pressures to reduce costs.

Outlook

We believe that there may well be acquisitions in this sector, with the financially stronger building societies seen as the natural winners attracting some of the weaker ones once the ‘hearts and minds’ of executives are won over and assurances can be provided that their members will be protected.

Consolidation: the path ahead

When considering what the path of financial services consolidation will look like across the coming years, it is useful to look to other large, fragmented banking markets and understand the lessons to be drawn from their experience. In this case, the only market comparable to the EU is the United States, where interstate banking mergers have already created some of the world’s largest pan-continental financial services groups. Both the European and the United States banking industries have a similar history – fragmented banking markets with long-standing historical legal restrictions on inter-state mergers. Looking at the United States across the past two decades we see that bank consolidation activity reached a high water mark in 1995, when furious competition among local and regional banks led to 5% of the banks in operation at the start of 1995 to cease to exist at the end of that year. This initial phase of increasing economies of scale and achieving the easy synergies from rationalising overlapping branch networks created a number of powerful regional banks, but it was not until around 2000 that we began to see the outlines of the ‘endgame’ – the emergence of truly national retail banking giants that spanned the entirety of the United States.

Europe has a heterogeneous set of national interests and cultures in comparison to the much more culturally homogenous United States; this cultural barrier, coupled with differing legal, tax and regulatory frameworks has, so far, hindered pan-European consolidation although there have been significant transactions such as HSBC’s acquisition of Crédit Commercial de France in 2000 or Barclays’ takeover of Spain’s Zaragozano in 2003, and Banco Santander acquiring UK’s Abbey in 2004. Additionally, within Scandinavia there was significant merger and acquisition activity and consolidation.

As different EU markets continue to harmonise their legal systems and as product nationalism fades, we believe that economic arguments will increasingly drive consolidation, just as happened in the United States. To learn from the US experience and to help us better predict the way forward, we analysed banking consolidation across the past 20 years. Mapping the number of mergers in the United States and Europe shows the two set on remarkably similar paths. We found the year of the most intense merger activity – 1995 in the US and 1999 in the EU – and then by overlaying Europe’s banking market onto the US trends we estimated European consolidation going forward, as shown in Exhibit 2. That analysis shows the two markets consolidating at a remarkably similar rate and allows us to make some early predictions. Looking at the US experience from its peak consolidation period in 1995, we can see that it took about five years for mergers to start creating retail banking giants with pan-US operations. If large market consolidation follows a similar pattern, which the data appear to support, 2004/2005 time period is when we are witnessing the creation of pan-European financial services giants; eg Santander/ Abbey, Unicredito/HVB, ABN/Antonveneta.

If history continues to be our guide, we would expect Europe’s path of consolidation broadly to mirror that of the United States. Indeed, this analysis, along with the other factors discussed above, is what underpins our belief that we are present at the creation of truly pan-European retail banks; today, we are witnessing the opening rounds in a five-to-ten year process of cross-border, retail banking and consumer finance consolidation.

The evidence to date

Certainly, there has been a flurry of large cross-border retail financial services deals in 2004 and the first half of 2005. In November 2004, Spain’s Grupo Santander was the first financial services group on the pan-European acquisition trail, buying the UK’s Abbey. Santander is now a top ten global bank and earns the majority of its revenues from retail financial services. In 2005, this has been followed by a furious string of proposed cross-border deals. In Europe’s largest cross-border merger to date, Italy’s Unicredito Italiano has bid for Germany’s HVB, while there have been two bids for medium-sized Italian banks. ABN AMRO of the Netherlands and BBVA of Spain, respectively, bid for Antonveneta and Banca Nazionale del Lavoro. Although BBVA’s bid has since been trumped by a bid from an Italian institution, the ABN AMRO bid for Antonveneta looks to be finalised in the final months of the year. Interest in Central and Eastern European banks has picked up, as evidenced in Romania.

There is a strong logic for believing that consolidation across the European continent will continue at roughly the same pace as consolidation followed in North America. It is natural that CEOs should turn to cross-border mergers when the relatively easy pickings from domestic mergers have been largely exhausted, and, as in some highly-concentrated domestic markets, when further consolidation is forbidden due to a prohibition on the excessive concentration of deposits and assets in the hands of a single competitor. However, this shift in emphasis from in-country to cross-border mergers involves a change in mind set and a sharp escalation in execution risk. Synergies are harder to achieve, and there are much greater risks arising from language, culture, customs, market structures, tax issues and the different regulatory environment in the target bank’s domestic market, not to mention political risk. Yet the unrelenting search for growth is leading CEOs to re-evaluate opportunities and risks, and the deals now underway are strong evidence that cross-border retail banking mergers are, after a long wait, finally a reality.

Private equity

- Accelerating the reshaping of financial services

Historically, almost all of the acquirers of regulated financial services business lines and assets have been other financial services firms – typically large banks or insurance companies already operating within the existing regulatory oversight framework. Exceptions to this rule have been joint ventures set up with retailers or outsourcing suppliers. The emergence of private equity investors on the financial services merger and acquisition field is a relatively recent phenomenon, but given the ever increasing amounts of capital that private equity firms are raising, this is a trend that looks likely to accelerate. Indeed, across 2004 and the first half of 2005, both the number of deals and the total value of financial services deals backed by private equity investors is up, a consequence of the growing pool of investable assets controlled by private equity firms.

Impact on European banking M&A

- Identifying underperforming businesses, undervalued assets

The need for high returns is driving private equity managers to scour the landscape for underperforming business lines or undervalued assets in which to invest. In contrast to traditional intra-industry M&A activity in which entire institutions are typically bought and sold, private equity firms are aggressively seeking out illiquid assets that can be monetised – like German apartment house portfolios – or lines of business that can deliver high stand-alone returns if simply invested in to create economies of scale – like closed UK life assurance books. In addition, ‘lightly’ regulated businesses such as foreign exchange bureaux have also been bought by private equity investors.

- Accelerating the line of business rationalisation process

The spotlight of value creation that private equity firms are increasingly shining on individual business lines is forcing financial institutions to re-examine the value they derive from different assets or activities. This process of re-evaluation is accelerating the pace of change for financial services firms by highlighting potential inefficiencies or points of competitive disadvantage on a business line-by-business line basis. In particular, partly due to the change in accounting standards in regards to bad debt, a small boom has arisen in the sale of non-performing loans across Europe, with particular interest being shown in Italy and Germany, as banks find it more efficient to dispose of underperforming loans and redeploy their capital. Accounting rules on leasing are also changing, which is resulting in the first private equity transactions in the leasing business.

High expectations of future growth

There is undoubtedly increasing pressure on financial services companies to find earnings-enhancing mergers. Many domestic European markets offer little opportunity for organic earnings growth, yet the high level of share prices relative to current earnings assumes buoyant growth. For many CEOs, the only way to meet the expectations implied by share price valuations is through value-enhancing mergers that offer efficiency synergies and, perhaps, entry to markets with higher growth rates than their domestic market can offer.

Taking the average price/earnings ratio for Europe’s 40 largest financial services companies at the end of August 2005, which was approximately 19 times actual 2004 earnings, we estimate that share prices currently embed a substantial expectation of future growth. Were banks merely to maintain earnings at their current level, we estimate that shareholders would pay a price of 12.4 times for that earnings stream. In actual fact, shareholders are paying a premium of approximately 6.5 times what banks have demonstrated they can earn today. In other words, shareholders, as measured by the prices they are willing to pay, are expecting the banking industry’s future earnings to grow by nearly 53% (Exhibit 3).

Unicredito’s acquisition of HVB demonstrates the logic of a growth-enhancing merger. Unicredito plans to extract earnings growth from its acquisition in two ways. On the one hand, Unicredito will increase its presence in the high growth economies of central and eastern Europe. At the same time, it plans to achieve cost savings from increasing operating and support function efficiencies, as well as reduction in headcount in these economies.

While institutional shareholders have recently demonstrated their willingness to oppose high-profile deals which in investors’ opinions appear to have insufficient strategic logic (eg, Deutsche Borse’s attempt to buy the London Stock Exchange), shareholders do appear to be generally in favour of merger proposals with a sound economic rationale. For instance, there has been little opposition to Unicredito’s proposed acquisition of HVB. Indeed, with interest rates low, and equity markets generally fully valued, shareholders are keen for companies with good investment opportunities to seize them.

Growing acquisition war chests

"With large amounts of idle funds sitting on bank balance sheets..."

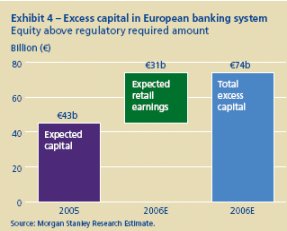

At the same time, however, financial services companies have substantial excess capital that needs to be either invested productively or returned to shareholders (even before the impact of Basel II). According to calculations by Morgan Stanley, banks will have accumulated some €74 billion in excess capital by the end of 2006 (Exhibit 4). What is more, this capital will continue to amass at a rapid rate going forward. With large amounts of idle funds sitting on bank balance sheets, we would expect that many CEOs will be tempted to deploy those funds on a high-profile shopping spree, rather than simply returning that capital to shareholders.

Falling political barriers

The European Commission is currently investigating why there have been so few cross-border financial services mergers, and has repeatedly stated that national regulators should not stand in the way of the market. Historically, certain national central banks and politicians have sought to deter acquisitions by foreign institutions, both to protect domestic jobs and, often, to try to preserve the close relationships between local banks and companies. Indeed, this issue has moved to centre stage due to the allegations of bias made against Antonio Fazio, the Governor of the Bank of Italy, in his oversight of the ABN AMRO bid for Antonveneta. At the time of writing, Governor Fazio is facing increasing calls to resign because of his alleged favouritism toward an Italian suitor in the bidding for Antonveneta, raising the issue of domestic interference in cross-border mergers within a single European market to the highest levels of political scrutiny.

An EU analysis of all merger activity in Europe over the past five years is revealing in terms of identifying the scope of the problem. According to the European Commission, only 20% of all European financial services mergers and acquisitions in the EU were cross-border deals, with the other 80% of deals being domestic acquisitions. This is very much at odds with all of the other industry sectors across the same period. Indeed, some 45% of all mergers and acquisitions in other sectors between 1999 and 2004 were cross-border, an activity rate that is over twice that found in financial services (Exhibit 5).

Many observers have attributed much of this cross-border activity deficit to national supervisory agencies blocking any approaches from foreign acquirers. Yet, evidence in the market suggests that central bank opposition, which has been seen as an insurmountable obstacle to any cross-border deal, is no longer the deal-breaker it once was. The UK authorities have not objected to foreign banks buying UK banks. In Germany, there has apparently been no objection from the central bank to the HVB merger. In Italy, there is a more complicated, but equally promising story.

Two foreign bids for Italian banks – ABN AMRO bidding for Banca Antoveneta and BBVA bidding for Banca Nazionale del Lavoro met initial opposition from the Bank of Italy. However, the Bank of Italy quickly changed to an accommodating stance once Italian bidders for both Italian banks entered the picture. Although BBVA has ultimately lost its contest for BNL, BNL’s acquisition by an Italian has contributed to overall banking consolidation in Italy, the second most fragmented domestic banking market in Europe (Exhibit 6). At the time of writing, the ABN AMRO bid for Antoveneta appears to be successful, after charges of bid rigging in favour of the Italian suitor for Antoveneta have emerged.

Finally, the tax treatment of European cross-border businesses appears, slowly, to be turning increasingly favourably. A number of European Court opinions and judgements, such as the Marks & Spencer case, have ruled against the ‘discriminatory’ treatment by the home country’s tax authorities of cross-border tax issues. We expect this trend to continue.

The reason the European Commission views the removal of obstacles to cross-border consolidation in financial services as so important is the positive effect that an efficient and competitive financial services industry is believed to have on the whole of the European economy. Speaking to a banking audience at the end of May 2005, Charlie McCreevy, European Commissioner for Internal Markets and Services, said: "There is empirical evidence to support the view that integration and consolidation in banking can enhance overall economic performance via macro economic stabilisation, risk diversification, economies of scale, lower costs of capital and enhanced consumer welfare." In fact, using the US experience as our guide, we would estimate the European banking industry as a whole can save over €18 billion of non-interest expense through the efficiency enhancements that come from consolidation. This windfall is money that flows directly back to customers, shareholders, employees and taxing authorities.

Footnotes

1 "The Banker: Western Europe: Abbey-Santander Spots an Overlooked Opportunity" The Banker, August 2005, Brian Caplen.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.