Introduction

The UK regulators are increasingly focusing on global financial services firms and the role non‑UK parent companies play in the governance and oversight of UK subsidiaries. The challenge that global financial services groups face is to demonstrate that their UK regulated legal entities maintain independence and control of their decision making whilst avoiding conflicts in relation to their parent company's objectives.

Since the Financial Services Authority transitioned to the Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) in April 2013, there has also been a shift in regulatory focus in relation to governance towards culture and individual accountability of senior management. This will increase the need for clear articulation of the roles and responsibilities of directors on UK subsidiary boards.

Clive Adamson, FCA Director of Supervision, enforced this message recently, reiterating the requirement to ensure the hearts and minds of management are based in the UK and that responsibility for setting the tone and culture of the firm sits at the highest levels of any firm. Mr Adamson also stated that the FCA expects international firms to strike a balance between global decision‑making structures and regulated legal entity considerations.

Traditionally, the banking industry has borne the brunt of regulatory scrutiny in this area, but the regulators are now expecting these principles and standards to be applied by investment firms, such as brokers and investment managers, owned by overseas parents.

This paper outlines the current expectations of regulators in relation to governance arrangements of global financial services firms; considers how the right choice of governance model and senior management can help a firm meet the expectations of UK regulators whilst facilitating the requirements of a global business; and details the practical steps currently being taken by firms to this end.

Understanding the expectations of regulators

The financial crisis, which began in 2007, exposed significant shortcomings in the governance of firms and the culture and ethics which underpin them. Since then, there has been a marked increase in direct intervention by the regulators into perceived governance failings; with a greater focus on the role of overseas parent companies in the decision making process of UK regulated legal entities.

This move to a more 'intensive' approach to supervision has included the ongoing use of s.166 skilled person reviews and increasing instances of chief executive officers (CEO), chairmen and boards being asked to provide written attestations and representations to the FCA and PRA. The use of attestations ties into the regulators' focus on culture and their attempts to gain a clear view of the business strategy and risk profile of firms – especially in complex organisations where overseas operations may affect the quality or flow of information.

The FCA and PRA Handbooks outline this expectation that senior management is responsible for maintaining control over the activities of the firm wherever it operates:

- Principles for Businesses (PRIN) – a firm must conduct its business with due skill, care and diligence and take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems.

- Threshold conditions (COND) – a firm seeking authorisation to carry on regulated activities in the UK must: have its head office (the location of its central management and control – directors, senior management, Compliance, Internal Audit etc.) in the UK (COND 2.2); clearly set out any 'close links' (e.g. parent, subsidiary, or controlling party) which is likely to prevent the FCA's effective supervision of the firm (COND 2.3); have appropriate financial resources to carry on its activities taking into account provisions made by other members of a group (COND 2.4).

- Senior Management Arrangements, Systems and Controls (SYSC) – a firm must: take reasonable care to maintain a clear and appropriate apportionment of significant responsibilities among its directors and senior managers (SYSC 2.1); ensure control is exerted across different operations and geographical areas (SYSC 3.1); and have robust governance arrangements, which include a clear organisational structure with well defined, transparent and consistent lines of responsibility (SYSC 4.1.1).

- Statements of Principle and Code of Practice for Approved Persons (APER) – an approved person performing an accountable significant‑influence function must take reasonable steps to ensure that the business of the firm for which he is responsible in his accountable function is organised so that it can be controlled effectively and must exercise due skill, care and diligence in managing the business of the firm for which he is responsible in his accountable function.

In addition to the regulators' requirements, all individuals who are appointed as statutory directors of UK companies are required under the Companies Act 2006 to comply with the following general duties of directors:

- to promote the success of the company;

- to exercise independent judgment;

- to exercise reasonable care, skill and diligence; and

- to avoid conflicts of interest.

Directors need to be aware of these responsibilities to the legal entity, as each of these duties could potentially put a director in conflict with the short term aims of the group.

Traditionally, governance has been thought of as a 'top‑down' responsibility which principally comprises the activities of the main board and board committees. However, the effectiveness of the governance model is crucially dependent on the robustness of divisional, geographic and regulated legal entity governance, particularly in large complex groups. This holistic view of the governance model is often missing from a board's consideration of governance.

What is Governance?

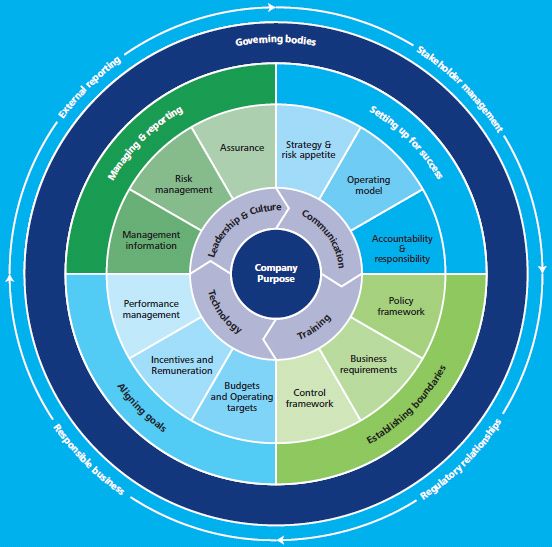

While boards, committees and other structures play a key role in governance, we consider there to be a number of important dimensions which comprise a robust framework with people and culture at the heart of effective corporate governance. The key aspects we think important are set out in figure 1.

Figure 1. Corporate governance framework

To read this Report in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.