Summary and implications

Recently the FCA published a consultation paper (the CP) on the FCA's regulatory approach to crowdfunding. This briefing sets out how the CP will affect firms that operate crowdfunding platforms.

Overall, the FCA's proposals relate to protecting retail investors who, in the FCA's view, lack the knowledge, experience and resources to cope with possible significant losses, whilst promoting effective competition in the interests of consumers.

The CP outlines the FCA's proposals for regulating loan-based and investment-based crowdfunding. While the FCA has identified other types of crowdfunding, such as those involving donations to support enterprises or organisations, these other types do not fall within the scope of FCA regulation.

Regulated activities

Currently, firms operating investment-based crowdfunding platforms are regulated by the FCA, if in doing so they carry on a regulated activity (without falling within an exemption). For example, such firms would need to be authorised if they are arranging deals in relation to shares or units in a collective investment scheme. In relation to loan-based crowdfunding, from April 2014 there will be a new regulated activity which will cover the operation of a loan-based crowdfunding platform.

The FCA is proposing a lighter-touch approach for loan-based platforms (compared with investment-based crowdfunding platforms). This is based on the FCA's observation that, in general, loan-based crowdfunding activities appear to be of lower risk than investment-based activities. However, the FCA intends to monitor the market closely and plans to conduct a formal review of the crowdfunding regime in 2016.

Loan-based crowd funding

The FCA's proposals in relation to loan-based crowdfunding are outlined in the table opposite and we have also explained some of those requirements in further detail below.

Application of the conduct of business rules.

The FCA plans to treat loan-based crowdfunding platforms generally in the same way as other designated investments. In particular, firms operating loan-based crowdfunding platforms will need to refer to two conduct of business rulebooks: one that sets rules relating to investors and one relating to borrowers.

Cancellation rights under the Distance Marketing Directive (DMD)

The DMD requires that most financial services contracts made at a distance (that is, without the simultaneous physical presence of the supplier or intermediary and the customer) give customers the right to cancellation, without penalty and without giving a reason.

The DMD already applies to firms providing loan-based crowdfunding and so firms should already comply with it, where appropriate. However, the FCA understands that it is not feasible to allow each investor the opportunity to withdraw from a particular loan agreement after agreeing to fund it. In this respect, the FCA has outlined two options in relation to cancellation rights which involve allowing consumers to invest in loan agreements but repay them their money within the first 14 days, if requested, or that the cancellation period should attach to the investor's decision to register with a platform rather than to investment in a specific loan (with a restriction on entering into any loans during this period).

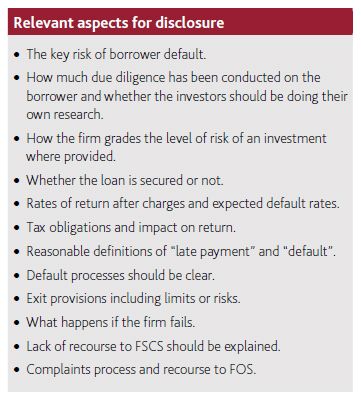

Disclosure rules

All communications from firms to retail clients must be fair, clear and not misleading. In particular, the FCA seeks to combat insufficient information being provided and a lack of balance, where disclosures emphasise benefits without a prominent indication of risks. The FCA intends to tackle these issues by requiring disclosure of the information in the table opposite.

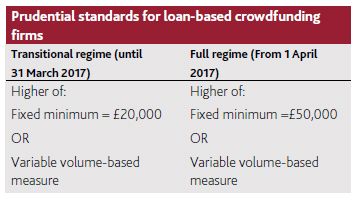

Minimum capital requirements

The prudential requirements for firms will be the higher of a fixed capital amount and a variable volume-based measure. The volume- based measure is a percentage of the total amount of loaned funds on the platform. This will be calculated annually as follows:

- 0.3 per cent of the volume of loaned funds up to £50m;

- 0.2 per cent of the volume of loaned funds above £50m up to £500m; and

- 0.1 per cent of the volume of loaned funds above £500m.

In order to minimise the burden that the prudential standards will have on firms, the FCA are proposing that the regime will only fully come into force on 1 April 2017.

Client money rules

Firms will be subject to the client money rules contained in the Client Assets Sourcebook (CASS) (with some minor amendments) because they hold client money before it is lent to borrowers.

In addition to the rules set out in CASS, the FCA is proposing to introduce a rule that firms must have arrangements in place to ensure that loans continue to be administered if the FCA-authorised firm becomes insolvent.

Proposals relating to both types of crowdfunding

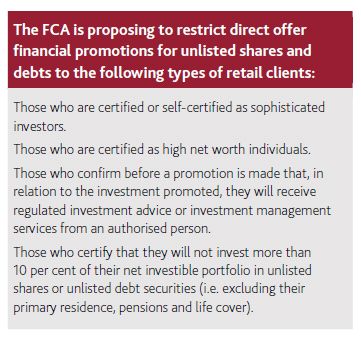

Direct offer financial promotions for unlisted equities and debt securities At present, to protect retail investors the FCA imposes restrictions on firms applying for authorisation to operate an investment-based crowdfunding platform. These restrictions are considered on a case-by-case basis but generally limit the firms to dealing with sophisticated or high net worth retail clients only. The FCA believes that the current approach of applying restrictions on an individual firm-to-firm basis at the authorisation stage is not a long term solution. As a result, the CP contains a revised approach that aims to make investment-based crowdfunding more accessible to a wider, but restricted, audience of retail clients through the promotion and access to investment-based crowdfunding platforms.

In the FCA's view the risks applying to units in an unregulated collective investment scheme, warrants and derivatives are not dissimilar to those that apply to unlisted shares or debt securities available through crowdfunding platforms. On this basis, the FCA is proposing to require firms that communicate direct offer financial promotions for investment-based or loan-based crowdfunding to ensure that they communicate such promotions only to certain types of retail client

Appropriateness test

Where no advice is to be given to retail clients, the FCA also proposes to require firms that communicate direct offer financial promotions for unlisted shares or debt securities, whether by internet-based means or by other media, to ensure that the rules on appropriateness are complied with before they arrange or deal in relation to the investment concerned. This is to ensure that clients are assessed as having the knowledge or experience to understand the risks involved before they can invest.

Next steps

In relation to loan-based crowdfunding, firms without a valid OFT licence should apply for one now to simplify their introduction to regulation by the FCA. They will be granted "interim permission" until they are fully authorised on 1 April 2016.

In relation to investment-based crowdfunding, firms and authorised representatives can opt to comply with the new rules from 1 April 2014. Alternatively, they can continue to comply with existing rules, until 1 October 2014, when the new rules will become mandatory.

Responses to the FCA consultation

The FCA consultation closes on 19 December 2013.

Nabarro intends to respond to a number of the questions raised in the CP. If you would like us to raise any questions on your behalf please contact Sam Robinson at sj.robinson@nabarro.com or John Finnemore at j.finnemore@nabarro.com

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.