- within Wealth Management and Real Estate and Construction topic(s)

- in European Union

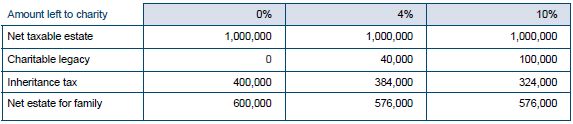

CHARITABLE LEGACIES

There have been growing calls in recent years to encourage individuals to leave 10% of their wealth to charity. Legislation was introduced in the Finance Act 2012 which came into effect on 6 April 2012 and which gives an added incentive to those who want to benefit charity on their death. This is not intended to deter those from lifetime giving where gift aid relief may be available for income tax purposes (though as announced in the recent Budget this may be capped in future).

Any legacies to charity under an individual's will are free from inheritance tax (assuming the charity is registered in the EU, Iceland or Norway) and this remains unchanged. However, if an individual leaves 10% or more of their taxable estate to charity then the rate of tax on the balance is reduced to 36%.

For those who intend to leave 10% or more of their taxable estate – which is the amount after inheritance tax reliefs and exemptions – to charity, the lower rate of inheritance tax represents a benefit to their heirs. For an individual who intends to leave 4% of their taxable estate to charity, there would be no loss to their heirs if they increased that charitable legacy to 10%. The intention behind the legislation is for the charity to benefit and this is best illustrated by the example below:

The above demonstrates the benefits to charity, at little or no loss to the family. It shows that leaving a 10% legacy to charity rather than nothing costs the family only 4% of the net taxable estate. If an individual is intending to make charitable gifts under his will, he should consider if these could be increased at no loss to the family. As the legislation only applies to an individual's net taxable estate, there is no encouragement for those who are married or in a civil partnership to leave a legacy to charity under their Will on the first death.

PROBATE AND SUCCESSION IN THE EU (BRUSSELS IV)

As long ago as March 2005, the EU Commission presented a consultation paper on ways of unifying succession law and procedure across the EU. The present system is riven with complexities and uncertainties. Each country applies its own rules to the validity of Wills and the administration of estates, but where the person who has died, lived in or was a national of another country, those rules usually involve a reference to the rules of the other country.

Take, for instance, a British national who has always lived in the UK and dies with a Will leaving his French house and bank account to his wife, ignoring his children. French rules say that you cannot do this as the children have an inalienable 'forced heirship' claim. English rules say that you can. Who wins? The rather unsatisfactory answer is that UK rules apply to the bank account (so he can leave it to whomever he wants) and French rules to the house (so he cannot). Similar, but subtly different, rules apply in most EU jurisdictions.

On 13 March 2012, the European Parliament approved a draft Regulation, known as Brussels IV, aimed at reducing these complexities. The UK and Ireland are not taking part in the adoption of the Regulation (as there are some provisions of it – the so-called 'clawback rules' which apply to certain lifetime gifts – that would be too radical for UK taste) and are not bound by it (though may still join at a later stage). The Regulation will, however, be of particular interest to British nationals or residents owning property in the EU.

The main purpose of the Brussels IV proposals is to ensure that there is one law and one law only that determines how the estate is dealt with. Basically, that law would be the law of the person's habitual residence at the date of his death. He would, however, be able to choose the law of his nationality to apply instead. If he elects for his nationality, this has to be stated in his Will.

The practical point here is that an English national with a house in France who wants to ensure that French forced heirship rules do not apply to his French assets when he dies should elect in his Will for the law of nationality (ie UK law) to apply. It may well be possible to rely on the 'habitual residence' rule but the previous draft of the Regulation was clearer than the latest version as to the effect of this and it looks like it will be safer to make a specific election in your will for the nationality rule. This will need to be considered carefully when the Regulation comes into force as part of your estate planning for your foreign property.

The Regulation contains a whole host of other provisions which will repay careful study by those with cross-border estates and their advisers. Any excitement should, however, be constrained by the thought that the Regulation still needs to be adopted by the Council. The European Parliament hopes that this will be before the end of the Danish Presidency in June 2012 but that may well be over-optimistic. Even then, it would be three years before the Regulation would come into force.

MAKING DECISIONS ABOUT WELFARE AND HEALTH CARE – LIVING WILLS AND LASTING POWERS OF ATTORNEY

Our January Private Client update reviewed the advantages of putting in place a Lasting Power of Attorney to deal with property and financial affairs in the context of estate planning. As life expectancy increases, looking ahead also involves consideration of future health and welfare issues and choices. An individual who still has mental capacity can express what they want to do however, sadly, capacity may fail or be lost. It is sensible to consider making arrangements now to express wishes about health and welfare and/or to appoint someone else to make these decisions when an individual can no longer decide for themselves.

Two documents should sensibly be considered as part of planning in this area – a Lasting Power of Attorney for Health and Welfare (LPA), under which attorneys can be appointed to make health and welfare decisions for someone who cannot decide for themselves, and a Living Will – a document in which an individual can record their wishes in relation to their healthcare to be followed at a time when they have lost their ability to express their own choices.

An LPA is a flexible document which can be tailored to an individual's requirements. It can appoint one attorney or more than one and can give them decision making powers in relation to health decisions, welfare decisions or both. These decisions can cover a wide range of issues – where someone lives, what they eat, what they wear and who they see. On the health side, attorneys could make decisions about medical treatment and tests and can review medical records. An LPA can also give attorneys the power to make decisions in the key area of consenting to and refusing life sustaining treatment and can incorporate other useful guidance for those caring for the incapable person.

Should an individual have preferences about their future healthcare but not wish to appoint someone to make decisions for them, a Living Will, also known as an 'advance decision', is a useful tool. Unlike an LPA, a Living Will does not need to be in a specified form or registered with the Office of the Public Guardian before the attorneys can act. It can be as simple or complex as required and is operational as soon as it is signed and witnessed, although it cannot be used until the maker loses capacity to make their own healthcare choices. Advance decisions commonly cover one or both of the following issues – treatments which the maker refuses to have (and this can include life sustaining treatment) and general expressions of wishes regarding their future care and treatment. An advance decision could, for example, cover religious beliefs or a preferred type of food and could also indicate who, if anyone, should be consulted before any treatment is given. This kind of information is of great use to health care professionals and those engaged in caring for a person who can no longer communicate their preferences and choices about their care.

NEWS IN BRIEF

- George Osborne's Budget on 21 March 2012 has dominated the news in recent weeks and most of the key issues raised in the Budget have been covered in minute detail. Anyone who owns any property in the UK through a company or even a trust (and this will likely catch other vehicles such as family limited partnerships) will be awaiting the consultation paper due to be issued in May and the form of any legislation which follows. Will it be possible to take steps before 6 April 2013 to avoid being caught by any new annual property charge? Likewise, charities and big charitable donors will be keen to see what will be the results of the consultation paper concerning the proposed cap on tax reliefs, due to be released in the summer.

- For those of you who have signed but not completed your LPA, take care! The Office of the Public Guardian has recently refused to register an LPA which had been signed by one of the attorneys over a year after being signed by the donor (the attorney lived in India), thereby meaning that all the parties had to start again with a new form, adding extra bother and expense. If your LPA is still being circulated for signing by all the parties, make sure that everyone is encouraged to return it as soon as possible.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.