AIM: SHELTER FROM THE STORM: RESULTS FROM OUR ANNUAL SURVEY

Despite the struggling global economy and double dip recession, new research by Smith & Williamson reveals high levels of confidence among UK-based, AIM-listed companies.

Two-thirds of the 152 AIM-listed companies surveyed believe that being on AIM has been good for business, with acquisition and fundraising plans remaining surprisingly robust. Nevertheless, three-quarters expect the number of companies on AIM to continue to fall.

Business confidence

Business confidence remains broadly intact among AIM companies despite a clear fall in confidence among survey respondents about the economy as a whole. In fact, over half (54%) of participating companies expected a double dip recession, compared to just under a fifth (18%) in 2010.

But, in spite of this, more than seven in ten (72%) respondents are positive about the outlook for their own business in the coming year, only slightly down from eight in ten (83%) last year. While 8% of respondents are negative in their outlook (compared to just 3% last year) this is substantially less than the 21% who weren't confident in 2009.

In keeping with this relatively upbeat mood, 59% of AIM companies plan to increase investment in their business, while another 49% intend to recruit more staff.

Philip Quigley, head of AIM at Smith & Williamson, says: "Many of the smaller businesses on AIM have now left the market; the remaining companies are generally larger and well managed. Many of these businesses are looking to grow so investment and recruitment naturally form a part of this." Half (50%) say trading has improved over the last 12 months. While this is a decrease on 2010 (65%), it is a significant improvement on 2009 when this figure was closer to 30%.

Fundraising activity

In 2011, around £4.3bn was raised on AIM through new admissions (£0.6bn) and further fundraising (£3.7bn). Two-thirds of our participating companies plan to raise further finance on AIM over the next year.

"These statistics underline the resilience of AIM as a market to raise finance," said Azhic Basirov, head of capital markets at Smith & Williamson.

While 43% of respondents are looking to raise less than £5m, 26% wish to raise between £5m and £20m. Another 7% of participants are considering potentially game-changing funding of between £20m and £50m or more.

Azhic continues: "The fact that over two thirds (69%) of participating companies are looking to raise up to £20m shows just how far AIM has come since it was first launched. However, given the general market conditions, the question is whether these levels of fundraising are a wish-list or reality."

Fundraising aspirations

Companies with a market cap of less than £5m

Over two-thirds (68%) of the smallest companies surveyed plan to raise funds of less than £5m. 13% are looking to raise sums equal to or well above their market capitalisation.

Companies with a market cap of £5m - £25m

Just over half (54%) are seeking to raise less than £5m, while a quarter (25%) want to raise between £5m and £20m.

Companies with a market cap of £25m - £50m

45% want to raise between £5m and £20m, with another 10% looking to raise more or less their market capitalisation of between £20m and £50m.

Companies with a market cap of £50m plus

29% wish to raise less than £5m and 14% are aiming for between £5m and £20m.

Acquisition plans

Nearly three-quarters (72%) of respondents are considering making an acquisition, with around half (52%) expecting to do so within the next year. This is similar to last year when these figures were 68% and 48% respectively.

Azhic says: "AIM has continued to deliver its promise of providing follow-on money to well-managed, performing companies as evidenced by the £3.7bn of further money raised on AIM last year which has enabled companies to fund their expansion plans, through acquisitions or organically, during the very difficult market conditions." While the survey reveals that companies of all sizes are keen to make further acquisitions, most notably:

- over three quarters (82%) of respondent companies with a market capitalisation of between £5m and £25m plan to make an acquisition at some stage

- just under half (46%) of participants worth between £50m and £100m anticipate making an acquisition in the next six months.

AIM: the place to be?

Nearly two-thirds (64%) of companies surveyed say being listed on AIM has been good for their business. "Being on AIM gives companies international credibility. Judging from our survey, businesses are confident about the benefits of an AIM listing despite difficult market conditions," says Philip.

Azhic adds: "It is important to consider AIM's success not in isolation but in comparison to the other equity markets around the world. When compared to the key junior or growth markets based in other jurisdictions, AIM had a higher level of activity in 2011 both in the number of primary and secondary fundraisings. A similar comparison with the key main markets in the same jurisdictions also places AIM in a favourable light."

However, the volatility on AIM over the last year has been unhelpful, according to 72% of our companies.

"Fluctuating share prices can affect bank covenants that are market-cap related and share options, as well as the ability to make acquisitions and raise capital. In short, the uncertainty makes it more difficult for companies to set their business strategies," explains Azhic.

Only 4% of AIM companies anticipate a Standard Listing on the Main Market of the London Stock Exchange in the future, with another 4% considering a Premium Listing. "This is a very different picture from our 2009 survey, when 20% of respondents said that they were thinking about a move to the Full List," says Azhic.

Only 5% of companies anticipate delisting in the next year, slightly down on last year (7%). A further 5% say they will consider this option in more than 12 months. "This would suggest that most of the delisting from AIM is behind us," says Azhic.

Tax boost

Nearly 40% of companies agree that the rise in the EIS and VCT threshold from April will boost their business, while nearly two-thirds (64%) believe it will boost AIM in general. But there is a suggestion that more could be done when it comes to government economic policy – especially if AIM is to become increasingly international, as 57% of respondents believe it will.

"There is a general feeling that UK tax breaks for smaller quoted companies could be better, with just 7% of our survey respondents believing that the government supports the smaller quoted market," says Philip. "The UK is making some progress with, for example, the patent box regime, which will provide for a lower rate of corporation tax for profits derived from qualifying patents. But more could potentially be done."

About our survey

These results are from our survey of UKbased, AIM-listed companies, conducted at the end of 2011. Over 150 companies took part, representing 13% of AIM-listed companies operating in the UK and a wide range of market capitalisation values, length of time on AIM and proportion of shares in public hands. Participants were primarily FDs, CEOs, directors or similar.

WILL EIS REFORM BOLSTER AIM?

By Nick Reeve

When AIM was launched in 1995 it was hailed as a market where small, fastgrowing companies could raise equity finance from the large pool of capital available in the London financial markets. AIM quickly established itself and it wasn't long before institutional fund managers began to view the market as a source of high-growth investment opportunities.

The evolution of AIM

Seventeen years on and AIM has progressed to become the international market of choice for fast-growing companies and is a real success story for the London Stock Exchange.

At its peak in 2007, a total of almost 1,700 companies were listed. But challenging market conditions since then have meant that there are now just over 1,100 companies. Despite this, with 90 new admissions in 2011, many exchanges around the world still look to AIM with envious eyes. In fact, there have been numerous attempts to replicate it in other territories – albeit with little success.

AIM has moved from being a domestic exchange for small, fast-growing companies to an international market dominated by resource companies and investment funds, which make up more than 60% of the market between them. This transformation has been driven largely by institutional investor appetite, with resource companies favoured in anticipation of the rapid industrialisation of China and South-East Asia.

Greater incentives for private investors

Small domestic trading companies are less favoured by institutional investors unless they have a market capitalisation of at least £25m, which is far in excess of the average capitalisation of AIM-listed entities of £14m. The Government is looking to these companies to generate the growth the economy so desperately needs, so it has introduced significantly enhanced incentives to enable private investors to fill the gap left by institutions.

Most AIM companies will qualify for these enhanced incentives provided that they have gross assets of less than £15m and employ fewer than 250 people. They will be able to raise up to £5m from Enterprise Investment Scheme (EIS) investors and Venture Capital Trusts (VCTs).

The incentives for individual investors are considerable. Tax relief of 30% is given upfront on the investment, capital gains tax liabilities can be deferred, and if the investment is crystallised at a loss then this will qualify for relief against the highest marginal rate of tax for the investor, quite often 50%. Additionally, the investment limit per individual will be raised from £500,000 to £1m provided sufficient taxable income has been earned in the year. All this depends on the investment being held for a minimum of three years, so that the investee company can benefit from stability in its shareholder base and can take a more strategic and mediumterm view of its business activities.

Will these measures help to reinvigorate the AIM IPO market? They certainly have a chance. No doubt private client brokers will look forward to offering their clients some interesting IPOs within the next few months.

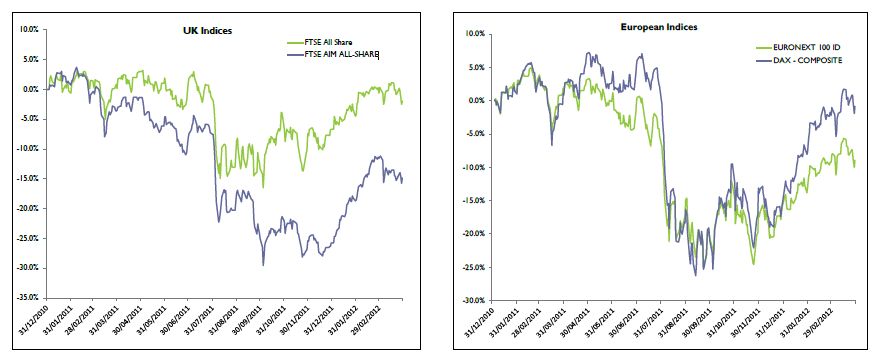

COMPARING THE MARKETS

By Azhic Basirov

Over the course of 2011, but especially during the second half of the year, stock markets around the world experienced considerable volatility. Investors, on the whole, displayed a risk-averse attitude towards new investment opportunities.

The uncertainty created by the sovereign debt crisis in the eurozone continued to impact the direction of the markets and resulted in frequent market volatility, often on a daily basis. Against this background, the major equity capital markets around the world experienced significant reductions in the volumes of IPOs, secondary fundraisings and the aggregate amount of capital raised.

Here are highlights from some of the key stock markets in 2011.

UK – AIM reported an increase in new listings and new money raised while the Main Market saw a decline in both.

US – NYSE and NASDAQ saw a considerable decline in new listings, as well as new and further money raised.

Europe – Euronext saw a decline in the number of admissions and total money raised. The number of listed companies has been in steady decline since 2009.

Hong Kong – HKSE reported an improvement in listing activity and saw a number of high-profile IPOs from international companies.

Singapore – The total number of companies trading on SGX fell slightly. However, the exchange saw a 10% improvement in further money raised.

South Africa – JSE reported a slight improvement in listing activity. The JSE All-Share Index beat the global trend and rose 0.4% in the second half of 2011.

In the first quarter of 2012 the markets generally displayed a good level of improvement and activity levels appeared to have picked up. Catalysts seemed to have been a combination of steady, positive economic news and firmer action being pursued by the eurozone leaders in tackling the sovereign debt issue. In particular, the European Central Bank (ECB) policy and actions taken since the appointment of Mario Draghi as its chief seemed to have restored investor confidence – at least partially – and demonstrated that the EU and ECB were intent on dealing with the European debt problems.

While improvements in market sentiment and performance achieved in the first quarter of this year are much welcomed, at the time of writing lack of confidence in resolving the eurozone sovereign debt and banking issues have resurfaced and European leaders have been urged to take firm action in dealing with the unfolding crisis.

Corporate tidy-ups Time for a spring clean?

By Anthony Spicer

The corporate structure is an important and sometimes overlooked area in larger groups of companies. Multi-entity organisations can reap the benefits of a review of their current structures to identify redundant companies. These may have been accumulated over time by, for example, acquisitions and mergers or special purpose vehicles set up for specific projects or joint ventures.

On average, FTSE 100 members incur between £150,000 and £300,000 per annum in non-value-added direct costs for dormant and non-trading companies. Recent analysis into the structures of FTSE 350 organisations revealed that more than 50% of these companies are lying dormant. Such figures would suggest that there are several benefits to undertaking a streamlining exercise and eliminating unwanted entities.

Costs

Redundant entities often fall beneath the radar once they are no longer financially significant to the organisation. Yet dormant companies can tie up valuable management resources because of the need to comply with statutory requirements, such as producing annual returns and accounts and maintaining books and records. Failure to adhere to these various reporting and taxation deadlines can result in fines.

Reduce risk and corporate governance failings

Dormant entities that are not regularly reviewed or supervised can be susceptible to fraud. There are many examples of dormant companies that have been used to obtain unauthorised goods, services or credit. The risk of corporate identity fraud is increasingly commented on, particularly following regulatory changes. These changes allow the e-service of documentation to Companies House, where confirmation of filings are not confirmed to the server, but are in the public domain to enable 'verification' of the existence of company officers for example, which may or may not be accurate.

It is important to stakeholders and regulators that the board is seen to be in control of the group it manages, as an extended group structure of dormant companies can be viewed as an avoidable compliance risk.

Dissolving unwanted entities

There are two routes for dissolving unwanted corporate entities.

1. Members Voluntary Liquidation

Formally winding up a company though a Members Voluntary Liquidation (MVL) resolves any outstanding matters and brings finality to an entity by ensuring that all liabilities, including contingent liabilities, are dealt with. It can also uncover 'forgotten' assets (often tax related) and ensure that no unforeseen liabilities arise going forward. In some circumstances, it can release tied up capital and allow a tax-efficient exit route for shareholders.

2. Strike-off

A strike-off is appropriate for dormant companies where it is certain there are no actual or contingent assets and liabilities, and where the company has not traded for at least three months. The process is less stringent and costly than a MVL, but carries more risks. For example, an application can be made to restore the entity to the Registrar of Companies for investigation, whereas the MVL process is final.

FINANCIAL PR IN CHALLENGING TIMES

By Nick Lambert of Bell Pottinger

It would be easy to assume that these are difficult times for the financial PR industry amid headlines about austerity, low gross domestic product growth, the decline in print media circulation, and even the City acknowledging levels of over capacity in the UK stockbroking sector. The reality is that financial PR is more important than ever for companies, with technology and modern levels of connectivity as key drivers.

Communicating to stakeholders

Stakeholders are demonstrating an unstinting desire for information and feedback from companies. Using media coverage to communicate to a company's customers and suppliers as part of an overall reputation management campaign is now inextricably linked to more traditional financial PR activity.

New media

The print media's agenda and status have changed dramatically. The reporting of basic corporate news has been largely commoditised but with the advent of the 'blogosphere' and digital editions of newspapers, output is no longer all about the print edition.

Long gone are the days when two sets of results and two trading statements a year were punctuated by lengthy silences from a company. This has been rendered obsolete by the culture of bulletin boards and more active investors. While achieving column inches just for the sake of it can be short-sighted, not engaging for long periods is no longer an option. Giving stakeholders the courtesy of a prompt reply and reiterating key messages without overstepping disclosure levels is a core activity for a company and its financial PR adviser.

The challenge of getting your story into print has also changed dramatically. Even FTSE companies cannot expect to have their results written up as a matter of course anymore due to the proliferation of websites that provide basic financial information. Editors demand storylines that are truly interesting, while financial journalists are tweeting and blogging just minutes after meeting a company.

This situation is both an opportunity and a challenge for companies and their financial PRs. Print editions of national papers are more scrutinising than ever, but the increasing consumption of news online means that both online and offline press coverage are becoming increasingly equal in value.

A smaller story with a genuinely interesting angle still has a good chance of gaining some media traction, just don't expect it to make the front page of the Financial Times Companies and Markets section.

Going viral

The viral nature of modern news has changed crisis communications significantly. Five years ago, if a client was experiencing a crisis it may have remained localised. Today, it can rapidly proliferate and become an international news item.

All these factors have varying effects on a company's share price and the need to manage a company's overall reputation is more challenging than ever. Financial PR is not for vanity's sake but helps to allow a company to fulfil its aims and potential.

MARKET WATCH: NAVIGATING GLOBAL MARKETS

By Michael Quach

Most asset classes bar major government bonds have seen a pullback in recent weeks amid renewed concerns over the European economic and financial crisis, a slowdown in China and the weak secular economic growth in the advanced economies. The MSCI AC World Index (including both advanced and emerging equities) has corrected by some 12.7% from its year-to-date high in local currency terms, while ten-year treasuries, gilts and bunds have fallen to 1.72%, 1.83% and 1.43% respectively (as at 18 May 2012).

Europe at the epicentre of global risks

The focus is on the risk of a Greek default and eurozone exit and the lack of growth in the region. The political uncertainty in Greece is increasing the risk of a run on its banks and raising fears of contagion to other parts of Europe. Germany may eventually have to provide the backstop to the peripheral economies' debt problems. The other element of this crisis is the lack of growth in the region.

The peripheral economies are in severe recessions and the core economies, bar Germany, are seeing a sharp slowdown. While they are very much inter-related, Europe's problems are not just about austerity – they include deleveraging, uncompetitive economies, the relative strength of the euro (despite having fallen by 10% over the past year) and political uncertainties. Thus, the region's prospects over the medium term will largely be dictated by both politics and the need to implement supply side reforms.

US and emerging markets growth is key

The hope is that signs of a stabilisation in the US economic recovery and comparatively decent growth in the emerging economies hold to offset weaknesses in Europe. There are tentative signs of an improvement in US housing activity, job creation remains positive though slowing and retail sales continue to hold up.

Meanwhile, growth in the emerging economies is expected to be 5.7% in 2012 and 6% in 2013, according to the latest IMF forecasts. As a result, global growth is expected to be 3.5% this year and 4.1% next year.

Navigating in an uncertain environment

A stabilisation in the US economic recovery and decent growth in the emerging economies should provide support to corporate earnings, while equities appear inexpensively valued on most measures. However, structural risks abound, with high government debts and uncompetitive economies in certain parts of Europe, China's transition to a more domestically-orientated economy and the US 'fiscal cliff' (though the stock market has not been too concerned about this latter issue thus far). The key to navigating the uncertain environment is a focus on companies with robust business models and global franchises as well as having a well-crafted, diversified portfolio.

FSA CLAMPS DOWN ON MARKET ABUSE FSA

By Siobhan Sergeant

Market abuse has become a hot topic in the past few months, with the Financial Services Authority (FSA) demonstrating its commitment to cracking down on this area. In fact, in some recent high-profile cases it has issued fines that amount to some of the largest in the regulator's history.

Market abuse can take a number of forms, including the improper disclosure of inside information, which has been the basis of a number of recent cases.

Red light for Greenlight

In January 2012, US hedge fund Greenlight Capital and its founder were fined £7.2m for market abuse relating to the June 2009 fundraising for Punch Taverns.

The company's founder and president had ordered the sale of Greenlight's shares in Punch Taverns after finding out about the imminent fundraising in a phone call with the pub company's management and broker. During the call, he had specifically stated that he did not wish to be made an 'insider' and, on this basis, believed that the information he had received was not inside information. However, the FSA was of the opinion that this was not a reasonable belief.

Other fines issued in relation to this transaction included:

- £350,000 for a former Bank of America Merrill Lynch broker, for his part in the call

- £130,000 for Greenlight's compliance officer for failing to question the trade

- £65,000 for the trading desk director at broker JP Morgan Cazenove for failing to identify the trade as suspicious and report it to the FSA.

FSA makes example of JP Morgan Cazenove

In April 2012, the FSA announced its decision to fine the chairman of capital markets at JP Morgan Cazenove, £450,000, for providing inside information. The fine related to two emails sent to a prospective client in which he disclosed information on Heritage Oil, another JP Morgan client. The FSA acknowledged that there was no intention to commit market abuse, nor any financial gain made from having disclosed what it deemed to be inside information.

However, the regulator considered the senior JP Morgan figure's failings particularly serious because of his experience and senior position. The fine was also intended to act as a deterrent against others committing market abuse. JP Morgan believes that the conclusions of the FSA are wrong and has appealed the decision to the Upper Tribunal.

Shot across the bow

Both these cases demonstrate the zerotolerance approach that the FSA is now taking when dealing with market abuse. With this in mind, it is increasingly important for individuals and companies to tread carefully if they are to avoid any suggestion of insider dealing or market manipulation.

CORPORATION TAX IS COMING DOWN (AGAIN>

By Matt Watts

There weren't many surprises in the March Budget, but the further reduction to the main rate of corporation tax was one of them. From 1 April 2012, UK companies will pay corporation tax at just 24%, a rate that is lower than any of the other G7 countries and the fourth lowest in the G20. Further reductions are planned so that the main rate of corporation tax will be as low as 22% by April 2014.

Promoting the UK

A low corporation tax rate, along with other measures such as reforming the Controlled Foreign Company rules, continuing improvements to research and development tax reliefs, and the introduction of the patent box regime from 1 April 2013 (a special lower rate of taxation for income derived from qualifying patents), are key components in the Government's plans to promote the UK as 'open for business'. But is this enough?

The carefully stage-managed announcement the day after the Budget that GlaxoSmithKline (GSK) will invest £500m in a new biotech plant in the north of England as a direct response to the Government's proposals would appear to indicate the strategy is working. But what if you're a company with a market cap of less than £70bn? What is the Government doing for those smaller companies in the UK on which the economy relies?

Access to funding

Here the evidence is less compelling. Yes, the reduction to the main rate of corporation tax is a boost and will impact any company or group earning taxable profits of more than £1.5m. However, many companies are struggling to earn profits on which they will pay tax anyway and a key reason for this is the difficulty in obtaining funding for expansion and growth. The expansion of the EIS and VCTs has opened up this valuable source of funding to many more companies, some of which will be listed on AIM. However, the increase to the limit of funds, from £2m to £5m is disappointing, as the Government initially proposed increasing this limit to £10m. On balance, although the impact of these changes will be reduced, the expansion of the EIS and VCT regimes should still be positive for companies looking for investment.

Will it be enough?

It is a bold move to reduce the rate of corporation tax down to 22% by April 2014 – 12% lower than the current rates in the US and Germany. Companies like GSK, which undertake extensive research and development will applaud the Government's efforts to promote the UK as a global centre for innovation, and the video-gaming and TV and film industries will also benefit from planned tax breaks. But what about the majority of companies that do not operate in those specialist sectors? Time will tell whether the promise of low corporate taxation, coupled with a reduction in the top rate of income tax (although a 45% top rate of income tax is still high when compared to other countries), is enough for them to play their part in the recovery of the UK economy.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.