Seeing The Wood For The Trees

Accounting standards, regulation and law seem to place ever increasing requirements as to the amount of information that should be disclosed in annual financial reports.

In the light of financial reporting complexity, it is not surprising that some preparers are saying it is becoming more difficult to present clearly their financial performance, and a number of users of financial statements are commenting on the difficulty of being able to understand the importance of the information they are presented with.

The growth in financial reporting requirements is largely in response to the increasing complexity and diversity of business models, coupled with the demands from regulators for greater transparency in the wake of financial crises. Many preparers therefore find it difficult to decide what information they should include in their accounts and what they can leave out without running the risk of criticism.

It is perhaps therefore understandable that there has been an increase in what the Accounting Standards Board (ASB) has recently described as "clutter". In its publication Cutting clutter the ASB identifies two specific problem areas:

- immaterial disclosures that inhibit the ability to identify and understand relevant information

- explanatory information that remains unchanged from year to year.

The publication, which is relevant to both IFRS and UK GAAP preparers, acknowledges that preparers alone cannot improve the clarity of financial statements and addresses at some length the ways in which the ASB is already working with other bodies to try to assist the process and the ideas it has for future improvements. This will take time and the ASB also identifies some places where it considers that preparers can improve the clarity of their financial statements without any change to the framework under which they report.

As part of its publication, the ASB has provided two short aids for preparers to assist with the preparation of the annual financial report. One is a planning aid which, among other things, suggests that preparers think in advance as to what they want the overall message of the financial statements to be and what they will determine to be material in the current period.

The second aid is for use at the stage when the financial statements are reviewed and includes considering whether new disclosures duplicate or replace other disclosures which should now be removed or refined. While not explicitly referred to in the aid, we suggest that this process should also include considering whether explanatory information in relation to past events is still relevant.

Smith & Williamson commentary

The remainder of this newsletter addresses a number of proposed new standards which will all result in new accounting and disclosure requirements. This is not the first time that we have seen a call for removing so-called "clutter" in financial statements. The ASB's publication and other similar documents do however identify that time pressures on preparers at the finalisation stage is one of the contributing factors to accounts containing what might be seen as unnecessary information. For anyone wanting to try and improve the clarity of their accounts, a simple starting point might be to spend a couple of hours reviewing last year's financial statements while considering the following questions.

- Do the financial statements 'flow' in a logical order or have they become confused?

- Are there are any disclosures with nil amounts where amounts are likely to be nil again?

- Are there any accounting policies for items that are either immaterial or types of activity no longer carried out by the business?

- Are notes supporting items in the primary statements actually providing any additional information about those items?

- Are there any disclosures specific to events in one period that will not need to be repeated?

The future of UK GAAP

We provide an update on the ASB's proposals regarding financial reporting following the consultation period.

In our winter 2010/11 edition we highlighted the ASB's proposals for the future of financial reporting. The proposals were for a three-tier structure reporting in accordance with EU-adopted IFRS (full IFRS), the financial reporting standard for medium-sized entities (FRSME) or the existing financial reporting standard for smaller entities (FRSSE).

The FRSME is the proposed new standard which would apply to the majority of UK entities. The period for comments on the proposed structure and the new FRSME has now closed and the ASB has been considering the responses received. The ASB has also been publishing what it describes as its 'tentative decisions to date' and so far it would appear that these may go some way to allaying at least some of the concerns we and other respondents have raised.

Transition date

Many respondents considered the proposed transition date of 1 July 2013 to be too early; a number said they would like this date to be pushed back until 2015. The IASB is currently suggesting that the effective date might be periods beginning on or after 1 January 2014.

Application of full IFRS to entities with public accountability

Financial Reporting Exposure Draft 43 (FRED 43) proposed that all entities with public accountability would be required to apply full IFRS. The definition of public accountability has caused a great deal of comment as it brings entities into the scope of full IFRS where this has not been a requirement in the past (for example pension schemes). There were also concerns that splitting sector groups across different tiers would lead to lack of consistency and that the additional cost of adopting full IFRS by small entities that would fall within the definition would be disproportionate to any benefit. At its meeting on 16 June, the ASB tentatively decided to remove the requirement for entities with public accountability to apply full IFRS, meaning that the requirements would not extend beyond what is required by law and regulation.

Reduced tier disclosures

Although there is significant support for the proposed reduced disclosure requirements for qualifying subsidiaries, some respondents are suggesting that these should apply to all subsidiaries. As discussed below it now seems likely that there will be a number of changes to the FRSME and therefore the ASB plan to do further work on the effect this might have on the proposed reduced disclosure regime.

The FRSME

There were a number of areas of the proposals regarding the FRSME that were unpopular with respondents to the ASB's consultation, including the following.

- No revaluation of property, plant and equipment. This requirement would be inconsistent with IFRS and current UK GAAP.

- No capitalisation of development or borrowing costs. In certain businesses, such as those in the software industry and property development, the ability to capitalise these costs is seen as reflecting the entities' business model. To disallow this treatment would be a significant issue and may leave some entities with no option but to adopt full IFRS.

- The proposed treatment of capital grants differs from the current requirements under UK GAAP and those in IFRS, and could result in the deferral of income where a particular grant contract contains residual performance obligations and clawback provisions. This would have a significant impact on the financial statements of entities receiving these grants.

At the ASB meeting in June it tentatively agreed to change the principles for amending the IFRS for SMEs (the standard underpinning the FRSME) to permit or require accounting options that exist in current UK and Republic of Ireland accounting standards at the transition date where these would align with full IFRS.

This change would permit the ASB to address many of the concerns expressed by respondents should it consider this to be appropriate. Smith & Williamson commentary

It will be interesting to see how the ASB's plans will now develop and anyone wanting to follow the progress can do so by reference to the ASB website at www.frc.org.uk/asb/technical/projects/ dev_month_2011.cfm

Public benefit Accounting

A new exposure draft suggests how the ASB's proposals for UK GAAP will apply to public benefit entities.

Following on from FRED 43 and 44, the ASB has now issued an exposure draft which sets out the financial reporting requirements for public benefit entities (PBEs) which were excluded from those standards. FRED 45 'Financial Reporting Standard for Public Benefit Entities' (FRSPBE) will be an add-on standard to the FRSME. While FRED 45 currently states a proposed date of application of the FRSPBE of 1 July 2013, it is assumed that this will be aligned with any later date of application of the FRSME.

The draft FRSPBE contains guidance on a number of accounting treatments (including presentation and disclosure) specific to PBEs, many of which are consistent with current practice in the sector. These are considered briefly here.

Concessionary loans

Concessionary loans are loans at below market rate and a choice of treatment is proposed of either:

- applying the recognition, measurement and disclosure requirements of the basic financial instruments section of the FRSME – initial measurement at fair value and subsequent measurement at amortised cost using the effective interest method; or

- measuring at the amount paid or received and adjust to reflect interest payable or receivable.

Property held for the provision of social benefits

Properties held for the primary provision of social benefits, e.g. social housing, are held at cost, less any provision for impairment, and amortised over their useful economic lives. Consistent with the general approach in the draft FRSME there would be no option to carry properties at valuation and capitalisation of borrowing costs is not permitted. However, it is assumed that any change to the FRSME in this respect would also find its way to the FRSPBE.

Entity combinations

The guidance within the FRSPBE is in respect of the following types of entity combination only: those at nil or nominal consideration that are, in substance, a gift; and those that meet the definition and criteria of a merger. Other types of business combination, e.g. an acquisition, are dealt with by the FRSME.

Combinations at nil or nominal consideration that are, in substance, a gift would be accounted for in accordance with the FRSME (which requires acquisition accounting) except that any excess of fair value of assets received over liabilities assumed should be recognised as a gain in the income statement.

Combinations that meet the definition and criteria of a merger should be accounted for by applying merger accounting. The definition and criteria for mergers are set out in the FRSPBE along with guidance on the accounting treatment.

Impairment of assets

When considering indicators of impairment, PBEs will be required to consider whether there is any indication that the service potential of an asset has been impaired, for example the cessation, or near cessation, of the demand or need for services provided by the asset.

When determining an asset's fair value less costs to sell, any restrictions imposed on the asset would need to be considered. In this situation, costs to sell would include the cost of obtaining a relaxation of any restriction in order for the asset to be sold.

Where an asset is held for its service potential rather than its ability to generate cash flows, the exposure draft suggests it may be more appropriate to determine value in use as the present value of the asset's remaining service potential. This will normally be equivalent to depreciated replacement cost, although other measures may be appropriate depending on the circumstances.

Funding commitments

Liabilities will only be recognised when the obligation is such that the reporting entity cannot withdraw from it and the commitment does not depend on the performance of the recipient. Commitments made which are performance related would be recognised only when those performance conditions are met.

Incoming resources from non-exchange transactions

Examples of non-exchange transactions include donations and legacies. Where there are no specified future performance conditions imposed, receipts would be recognised at fair value when receivable. Where future performance conditions are imposed, receipts would be recognised at fair value only when those performance conditions have been met.

Smith & Williamson commentary

The FRSPBE is out for comment until 31 July 2011. PBEs will also be affected by the changes set out in the FRSME and are among the commentators whose concerns are discussed in the previous article. The additional guidance in the FRSPB is, however, broadly in line with existing practice.

Changing the rules on consolidation

Concerns over the accounting for off-balance sheet arrangements and special purpose vehicles have led to the issue of new accounting standards.

In a major project the International Accounting Standards Board (IASB), in conjunction with the US Financial Accounting Standards Board (FASB) has sought to address concerns that emerged during the financial crisis in relation to offbalance sheet arrangements. The project has looked to both tighten the rules for when consolidation is required and improve transparency of all interests in other entities by requiring further disclosure.

In May the IASB published a package of three new standards which both brought its project to an end and resulted in broad alignment of IFRS and US GAAP.

- IFRS 10 'Consolidated financial statements' continues to require consolidation based upon the existence of control, but modifies the definition of control.

- IFRS 11 'Joint arrangements' covers both joint ventures and joint control.

- IFRS 12 'Disclosure of interests in other entities' sets out the disclosures for entities that have interests in subsidiaries, joint arrangements or associates.

All three standards apply for periods beginning on or after 1 January 2013. When determining whether one entity controls another, IFRS 10 requires reference to three elements of control:

- power over the investee

- exposure or rights to variable returns from involvement with the investee

- the ability to use power over the investee to affect the amount of the investor's returns.

'Power' is defined by the new standard as when an investor has existing rights that give it the current ability to direct the relevant activities. A simple example would be voting rights, but the IFRS also requires consideration of the economic substance of the arrangements existing between the two parties.

Assessing control by reference to the three elements will not always be straightforward, and in more complex situations significant judgement will be required. Furthermore, if there are changes to one or more of the three elements of control after it is initially established, the IFRS requires an investor to reassess whether it has gained or retained control.

Smith & Williamson commentary

Many preparers of consolidated accounts will find that the new standard results in little or no change to their financial statements. However, other preparers, for example those with links to special purpose entities, will need to look at the nature of their relationships in the context of the new standard. It is possible that some related entities that were previously treated as associates, or not included in consolidated accounts at all, will become subsidiaries under the new standard.

IFRS 11 introduces two categories of joint arrangements – joint operations and joint ventures. The new categories provide a slightly different framework to that found under the previous standard, IAS 31 'Interests in joint ventures' with the category of joint operations broadly combining jointly controlled assets and jointly controlled operations.

The accounting requirements for joint ventures will change with the introduction of IFRS 11. Under the new standard a joint venturer is required to recognise an investment and to account for it using the equity method. The option that existed in IAS 31 to account subsequently for joint ventures using proportional consolidation will not be available under the new standard. Any change in accounting arising from adopting IFRS 11 will have to be accounted for retrospectively, giving rise to a restatement of comparative figures in the first year of adoption.

Smith & Williamson commentary

Proportional consolidation has been less widely used in the UK than in some other countries, but in certain industries it has become popular because preparers argue it better presents the way in which their joint ventures operate. Those preparers who have proportionately consolidated will need to consider how they will explain the effects of the change in presentation.

Any groups that are subject to loan covenants that are assessed on consolidated figures may find that the changes arising from IFRS 10 and 11 could cause them to breach existing covenants and should plan to discuss this with their banks as soon as possible.

IFRS 12 aims to provide users of financial statements with information about all interests the reporting company has in subsidiaries, joint arrangements, associates and unconsolidated structured entities. The disclosure requirements are wideranging and go beyond current requirements for all such entities. The new requirement will provide not just quantitative data about the effect of interests in other entities on the reported consolidated figures but also qualitative information about the nature of these interests and the risks associated with them.

Smith & Williamson commentary

IFRS 12 will provide valuable information to users who are interested in understanding the true risk exposure of a group. However, the standard will also increase the disclosure burden on preparers of consolidated accounts, and in some instances preparers' existing financial reporting systems may not capture all the information required, particularly in relation to unconsolidated entities.

A comprehensive model for fair value

Within IFRS the term 'fair value' is widely used across a number of standards but until now there have been inconsistencies between those standards as to how fair value should be measured.

In May the IASB issued IFRS 13 'Fair value measurement'. The new standard does not change the rules for when an entity is required to use fair value, but does introduce one single definition and a consistent measurement approach to fair value throughout IFRS. The new standard also introduces enhanced fair value disclosures. IFRS 13 is the result of a joint project between the IASB and FASB and was issued in conjunction with equivalent US guidance.

Fair value will be the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. The standard explains that the fair value will be measured with reference to what is termed the principal market for the asset or liability being measured. In the absence of a principal market, reference should be made to the 'most advantageous market'. The standard defines the principal market as the market with the greatest volume and level of activity for the asset or liability that can be accessed by the entity. Generally, the market in which the entity transacts most frequently will also be the market with the greatest volume and deepest liquidity. Hence, the principal market would likely be the same as the most advantageous market. However, in some cases this will not be the case and applying IFRS 13 could change current measurement bases.

The new standard also states that the value of a non-financial asset must be based on the 'highest and best use' of the asset which is physically possible, legally permissible and financially feasible. IFRS 13 presumes that an entity's current use of an asset is generally its highest and best use, unless market or other factors suggest that a different use of that asset by market participants would maximise its value.

Among the new disclosure requirements is a specific requirement to quantify and disclose any unobservable inputs used in fair value calculations. This could result in disclosures which may be commercially sensitive to some entities. Furthermore, detailed fair value disclosures previously only made in relation to financial instruments will be extended to some nonfinancial assets and liabilities at fair value.

Smith & Williamson commentary

Any steps to increase the consistency and cohesiveness of the IFRS framework should be welcomed. However, preparers need to be aware that IFRS 13 is not simply a codification of best practice, or a gathering together of existing guidance. The standard creates new rules in specific areas and businesses will have to assess how the changes will impact them. For example, some preparers may find that they are not currently using an exit price for all their fair value measurements, and that they need to revise their measurements accordingly. In addition, preparers working in certain industries, such as real estate, may find that the requirement to measure a non-financial asset based on its 'highest and best use' pushes valuations upwards. As a result, many businesses will find that adoption of IFRS 13, which is not retrospective, leads to significant volatility in total comprehensive income in the year of initial application.

Revenue recognition and leasing – the debate continues

The development of new revenue recognition and leasing standards was discussed in the previous edition of Financial reporting.

Since then the IASB has been considering how to respond to comments received. It appears clear that the core principle of each new standard will remain – revenue recognised when the goods or services are transferred to the customer and all leases will be on balance sheet. However, there are also a number of key areas where it is probable that there will be significant change before any final standard is issued.

Revenue recognition

While no significant changes are anticipated in relation to revenue recognition from sale of goods, the provision of services and long-term contracts has been more challenging. Among the areas being addressed by the IASB are:

- defining when, in the context of services, a transfer is deemed to be continuous and how it should be recognised in the accounts

- clarifying what is meant by 'distinct' in terms of identifying separate performance obligations within a contract following concerns that the proposed definition could result in an overly large number of separate performance obligations being identified

- modifying the method by which revenue is recognised in circumstances where there is uncertain consideration. The IASB appears to have accepted that the originally proposed probabilityweighted method was unlikely to be useful or relevant except for portfoliotype transactions. It is now suggested that the 'best estimate' should be used for most such transactions.

Leasing

In considering the responses to the exposure draft, the IASB is particularly focusing on changes regarding initial recognition and subsequent measurement. Some of the key changes highlighted to date are summarised below.

- A lessor and a lessee will recognise and initially measure lease assets and lease liabilities at the date of the commencement of the lease.

- The method used in terms of recognising the present value of lease payments when extending or terminating a lease will be modified. A lessee will be required to determine the present value of lease payments payable during the lease term on the basis of expected outcome, not probability weighted as previously proposed.

- On subsequent measurement, the IASB has tentatively decided that a lessee and a lessor should reassess the lease term only when there is a significant change in relevant factors such that the lessee would then either have, or no longer have, a significant economic incentive to exercise any options to extend or terminate the lease.

The IASB has stated that it intends to re-expose both the revenue recognition and leasing standards later in 2011.

Smith & Williamson commentary

Both revenue recognition and leasing are very important subjects for a large number of entities. It is not therefore surprising that the IASB has received so much comment in response to its proposals. It would also appear that many of the concerns of respondents may be addressed and we will return to these topics when the new exposure drafts and standards are issued.

Financial reporting round-up

Late filing penalties

The level of late filing penalties at Companies House were increased for periods beginning on or after 6 April 2008 to coincide with the introduction of parts of the Companies Act 2006. In addition to increasing the flat rate penalties, where a company fails to file accounts on time for two years in a row (and the earlier began on or after 6 April 2008) the level of penalty is doubled. For example, a private company which files its accounts more than three months late for two consecutive financial periods will incur a penalty of £750 in relation to the second year. In order to avoid these costs it is important to ensure that accounts are filed within the required timescale of nine months from the end of the accounting period for private companies and six months for public companies.

Changes in tax rates and deferred tax

From 1 April 2011 the main rate of corporation tax changed from 28% to 26% with a further three 1% annual reductions starting on 1 April 2012 culminating in a rate of 23% in the tax year commencing 1 April 2014. The change in rates will impact the deferred tax calculations of companies reporting under UK GAAP and IFRS as changes in tax law are not reflected in the balance sheet/statement of financial position until the law has been substantively enacted at the relevant financial reporting period-end date.

The date of substantive enactment is either the date the Bill has been passed by the House of Commons and is awaiting passage through the House of Lords and Royal Assent, or the date a resolution has been passed under the Provisional Collection of Taxes Act 1968. As of 5 July 2011, only the changes to the main rate of tax to 26% and the reduction to 25% from 1 April 2012 had been substantively enacted. This means that an entity with a 31 August 2011 year end would base its deferred tax liability on a rate of 26% for the seven months to 31 March 2012 and then on 25% thereafter

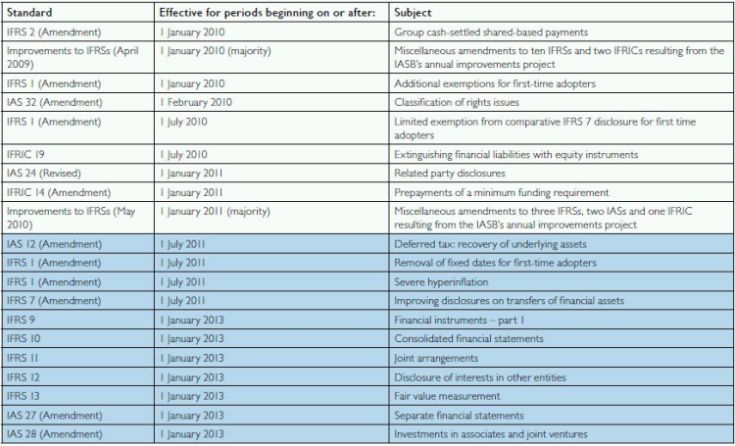

On the horizon

The table below summarises the effective dates for new and revised IFRS and IFRIC interpretations. Those that are shaded have not yet been endorsed by the EU and the effective date will be contingent on successful endorsement.

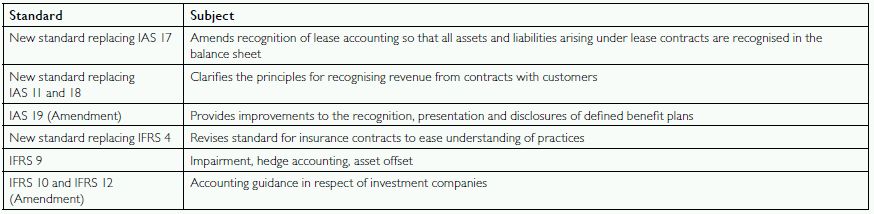

In addition, the following standards are due to be published by the IASB before the end of 2010. Standard title, effective date and EU endorsement will be confirmed following publication.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.