NERA has developed a proprietary database of fines and other enforcement activity by the Financial Services Authority (FSA), covering the period beginning 1 April 2002. This article provides a detailed analysis of trends in FSA enforcement actions over that period, based on our classification of the types of underlying alleged misconduct (extended content available at www.EnforcementTrends.com).2

Fines and criminal prosecutions announced by the FSA have risen substantially since the beginning of 2008, consistent with the more assertive enforcement stance adopted around that time. The FSA expects its new penalty framework to increase fines substantially going forward,3 though the planned transfer of responsibility for enforcement to the Financial Conduct Authority (FCA), due to be completed at the end of 2012, introduces uncertainty into the outlook.4

In this article we analyse fines and other measures announced in enforcement actions since 1 April 2002, the beginning of fiscal year 2002/03.5 We classify enforcement actions based on the underlying conduct of the defendants as described by the FSA. Our key findings are as follows:

- A recent increase in number of fines, the imposition of several very large fines, and an increase in the size of fines against individuals exemplify the apparent effects of the FSA's tougher enforcement stance. The observable trends are consistent with the FSA's stated shift away from its previous "light touch" enforcement philosophy in favour of a "credible deterrence" approach:

-

- The aggregate amount of fines assessed in 2010/11 was nearly three times the 2009/10 level (see Figure 1); however, a few very large fines account for a large share of this increase.

- Excluding the very largest fines (those large enough fall into the top 10 fines against firms or the top 10 fines against individuals), the size of the average fine against individuals rose by 37 per cent in 2010/11 compared to the prior year but against firms declined by 16 per cent. Overall, average fines outside the top 10 for firms and top 10 for individuals did not change very much, declining in size by 7 per cent in 2010/11 as compared with the prior year.

- Aggregate fines in 2010/11 substantially exceeded aggregate fines in years prior to the shift to "credible deterrence": for firms, aggregate fines in 2010/11 were seven times the annual average over the six years prior to 2008/09; for individuals, aggregate fines in 2010/11 were 22 times the average in the earlier period (see Figure 2).

- The frequency and size of fines imposed on individuals have grown more rapidly than for firms, consistent with a shift in enforcement focus towards sanctions against individuals; however, the typical individual fine (as represented by the median) is still well below £100,000.

- A high proportion of the all-time top 10 fines has been assessed over the past three fiscal years, and in 2010/11 in particular, consistent with an increasingly tough enforcement stance.

- An increase in the use of criminal sanctions against individuals is also an indicator of tougher enforcement, although to date these sanctions have been used almost exclusively in insider dealing cases.

- Sanctions other than fines can raise the costs to firms and individuals of enforcement action. Prohibition sanctions have increased in frequency and are now nearly as common as fines. The total cost of internal investigations requested by the FSA (Skilled Persons Reports) has been rising and in 2010/11 exceeded the aggregate amount of fines against firms in any prior year. The effect of new suspension powers introduced under the Financial Services Act of 2010 is yet to be realised but has the potential to impose substantial additional costs on firms.

- With the exception of insider dealing, enforcement appears to have shifted away from violations of market integrity (a classification we use for behaviour that distorts or otherwise negatively affects financial markets, as described below) and towards actions aimed at customer protection.

- Increasingly, enforcement actions are being contested and cases referred to the Financial Services and Markets Tribunal (FSMT). Referrals increased by 60 per cent in 2010/11, to 40 cases, from 25 in 2009/10.

- The FSA's new penalty framework, new suspension powers and the transfer of enforcement to the FCA create uncertainty about the future focus of enforcement and the extent of potential financial exposure stemming from market conduct and regulatory compliance risks.

Background: The Role of Financial Penalties in Enforcement

The FSA has a range of disciplinary, criminal and civil powers with which to sanction firms and individuals whose conduct fails to meet required standards or otherwise violates the law. In addition to financial penalties, the FSA has the power to:

- require firms to conduct Skilled Persons Reports to obtain independent views of aspects of firms' activities under investigation;6

- censure firms or individuals through public statements;

- effect disgorgement of any monetary benefit derived from misconduct by imposing a fine of this amount on top of any penalty;7

- require that a scheme be established to achieve customer redress (i.e. amounts paid directly to customers rather than to the FSA);

- restrict the ability of individual firms to engage in certain regulated activities for which authorisation is required (suspension or prohibition);8

- seek civil court orders to enjoin conduct, freeze assets, close down a firm (insolvency procedure) or order restitution (from entities not subject to redress requirements of the Financial Services and Markets Act (FSMA)); and

- prosecute firms or individuals for acting without authorisation or for other illegal acts.

These powers are not mutually exclusive: for example, the FSA may impose a financial penalty and restrict certain regulated activities. In addition to public disciplinary actions, FSA investigations into misconduct may also be resolved without disciplinary action,9 or with a private warning.10 Fines and prohibitions are together the dominant forms of disciplinary enforcement action taken by the FSA.11

The FSA has authority to impose fines under provisions of the FSMA (including specific provisions relating to market abuse and listing rules), the Bribery Act 2010 and under several sets of regulations.12 The stated purposes of financial sanctions in the FSA's enforcement regime are to discipline wrongdoers by imposing a penalty, to effect disgorgement of any benefits wrongly obtained and to deter further misconduct.13 According to the FSA:

"[t]o achieve credible deterrence, wrongdoers must not only realise they face a real and tangible risk of being held to account, but must also expect to face a significant penalty."14

This article focuses primarily on fines, which comprise any amount ordered to be disgorged, plus any penalty. However, we also review and analyse data on other types of sanctions, including criminal enforcement.

Enforcement action by the FSA begins with an investigation and, at this stage, the FSA may make formal information requests or demand that a Skilled Persons Report be commissioned to assess conduct at issue. The FSA has three principal alternative courses of action following an investigation: to seek a High Court injunction, pursue a criminal action or use its executive powers to impose sanctions through its own administrative regulatory disciplinary process. An injunction is needed to stop ongoing conduct, seize assets or put a firm out of business. The firm or individual that is the subject of a regulatory proceeding may choose to contest the case against it or enter into a settlement. Early agreements, for example consenting to a fine, typically result in leniency (financial penalties may be discounted by up to 30 per cent under the new penalty framework)15 as an incentive to avoid appeals to the Regulatory Decisions Committee (RDC) or, subsequently, to the FSMT.

A flowchart depicting the criminal, civil and regulatory enforcement options available to the FSA is depicted in Figure 3. The chart also depicts the separate RDC and Executive Settlement paths to resolving regulatory disciplinary actions by the FSA.

Background: Recent Developments in Enforcement Policy

In 2007, the FSA adopted a tougher tone in its public statements on enforcement philosophy, moving away from its previous "light touch" philosophy and instead emphasising "credible deterrence" against wrongdoing in financial markets, including intensive supervision of regulated firms.

The light touch approach had de-emphasised enforcement in addressing non-compliant behaviour, choosing to use enforcement selectively and strategically as part of an "overall risk-based supervisory strategy and in support of the FSA's objectives".16 Proponents of light-touch regulation argued it had contributed to the attractiveness and success of the UK as a financial centre, as reflected, for example, in more new listings on the London Stock Exchange than on US stock markets.17 However, developments including the financial crisis, the related collapse of a major British bank, the need for substantial government assistance to several others and a series of mis-selling scandals led senior FSA officials to question the efficacy of light touch regulation and to signal a shift to a tougher regulatory stance, including more vigorous enforcement.18 The change in enforcement philosophy was captured in a widely reported statement by FSA Chief Executive Hector Sants: "There is a view that people are not frightened of the FSA. I can assure you that this is a view I am determined to correct. People should be very frightened of the FSA."19

In pursuit of credible deterrence, the FSA's current stated enforcement priorities consist of several elements, including:20

Consumer Protection: Involves taking action against unauthorised firms, with a particular focus on fraudulent share schemes (e.g. "boiler rooms").21

[Maintaining Confidence in] Capital Markets: Enforcement activity focussing on market misconduct, insider dealing and market manipulation in particular.

Thematic Reviews: These are the basis of a supervisory strategy of assessing and addressing the issues of greatest concern to the FSA. Issues of concern are often announced in advance to promote an increase in standards, but can also lead to enforcement action. The FSA has conducted thematic work since 2006 in areas of:

- treating customers fairly (TCF);

- mis-selling of Payment Protection Insurance (PPI);

- advice regarding pension switching;

- quality of mortgage and investment advice;

- mishandling of client money;

- mortgage arrears;

- complaints handling;

- mortgage fraud; and

- share fraud, including brokering of small capitalisation stocks.

In its recent Annual Performance Account, the FSA has articulated a belief that "action against individuals has a greater deterrent effect than action against firms".22 Starting in 2008/09, the FSA expressed a commitment to bringing senior managers to account for "competency and integrity failings". In particular, the FSA increased its investigations of Significant Influence Function holders (SIFs)23 and imposed sanctions against certain of these individuals as a part of an effort to promote behavioural change in the industry.24 Alleged competency and integrity failings of senior managers can include failure to prevent the misconduct of others.

NERA's Fines Database and Classification Scheme

NERA has compiled a database of FSA enforcement actions with which to track and analyse trends in enforcement activity. The database is based on publicly available information from the FSA and contains all enforcement actions that have resulted in fines announced since 1 April 2002.25

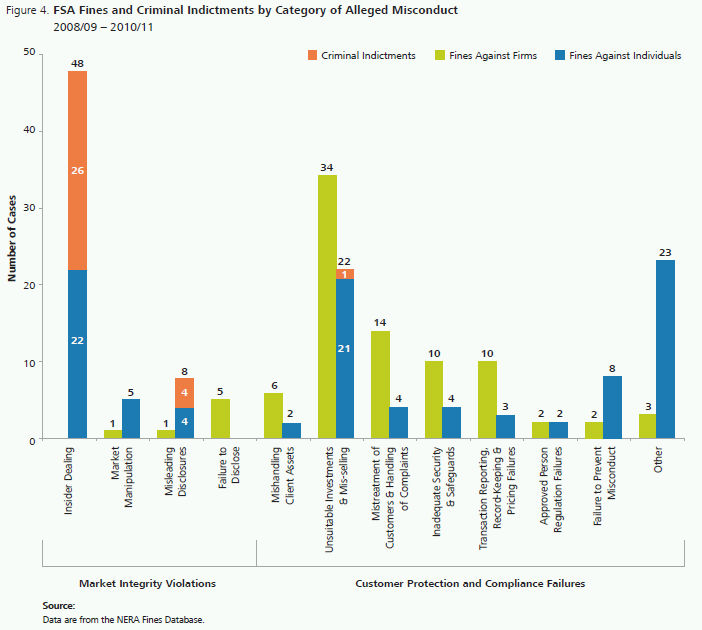

We have classified each fine according to the principal type of underlying misconduct described by the FSA.26 In cases involving multiple individuals and/or firms, the fine against each person or entity is classified and listed separately. This classification departs in certain respects from the presentation of enforcement activity by the FSA in its annual reports, which is organised largely in terms of regulatory objectives and principles such as systems and controls, treating customers fairly, unauthorised activities and market protection.27 Our conduct-based classification system reveals the types of activity sanctioned most frequently and fined most heavily, no matter under which statutory principle or rule sanctions were imposed. This provides an alternative view of the focus of FSA enforcement that can be used to track trends in enforcement. The number of recent fines in each of our 12 conduct-based categories is depicted in Figure 4.

Market integrity violations

Our classification scheme makes a basic distinction between cases alleging violations of market integrity—behaviour that distorts or otherwise negatively affects financial markets—and other types of cases. We classify four types of conduct as relating to market integrity:

- Insider dealing: Unlawful trading based on non-public (inside) information and/or improper dissemination of such information.28

- Market manipulation: Transactions made, orders placed or other similar actions intended to manipulate the price of a financial instrument or otherwise create a false impression about the market for a financial instrument.29

- Misleading disclosures: Dissemination of misleading information about an investment or issuer, or other actions taken to give a false impression about, and thus distort the market for, an investment.30

- Failures to disclose: Delay or omissions by a publicly-traded company in providing the market with information that is required to be disclosed, leading to a distortion in the market for the company's securities.31

Our "violation of market integrity" classification is slightly more expansive than the concept of "market abuse" specifically authorised under the FSMA. The FSA has codified market abuse in the Code of Market Conduct, as consisting of insider dealing, market manipulation and certain misleading disclosures. Failure to disclose, by contrast, is a breach of Listing Rules but not of the Code of Market Conduct, and is therefore not officially classified as market abuse. However, the FSA typically describes failures to disclose as having distorted ("created a false market for") a company's securities.32 From an economic perspective it is therefore logical to group failures to disclose along with violations officially categorised as market abuse. We also count as violations of market integrity any case in which the following two conditions are met: accounting or other misstatements are alleged to have been made, and the FSA expresses concern about the effect of the misstatements on the market for publicly traded securities. This includes some cases in which the firm or individual was sanctioned by the FSA for recordkeeping failures or other conduct not officially classified as market abuse. There were four such cases resulting in fines over the last three years. The composition of recent market integrity cases is shown in Figure 5, which also shows how the number of cases in that category compares with the number of cases classed by the FSA as market abuse.

Customer protection and compliance failures

Our other overarching category of conduct is customer protection and compliance failures. These cases allege misconduct that does not directly affect securities markets, but instead relates to failures in customer protection or compliance, including:

- Unsuitable investments & mis-selling: This category includes cases that allege investment advice given to, or investments made on behalf of, a client or clients, which were not suitable to client risk preferences or circumstances (or both). Often these cases involve a failure to obtain "know your customer" information necessary to assess the suitability of investment recommendations or decisions.33 This category also includes improper marketing cases including failure to provide sufficient and non-misleading information in promoting or selling a security,34 and some small capitalisation stock brokerage ("boiler room") cases.35

- Mistreatment of customers & mishandling of complaints: This includes cases where clients were not catered to in a manner deemed fit by the FSA. Common examples include overcharging of customer fees, using high-pressure sales tactics,36 poor treatment of customers facing mortgage arrears or disadvantaging certain customers in any way.37 Failures to respond appropriately to client complaints are also included in this category.38

- Mishandling of client assets: This includes failure to segregate client assets from firm assets and other failures to safeguard, or misuse of, money managed on behalf of clients.39

- Inadequate security & safeguards: These include control failures relating to financial crime prevention, such as failing to screen customers against the government's "sanctions list", failing to report or appropriately monitor suspicious behaviour (such as potential bribery) or allowing third parties inappropriate access to client funds—as well as cases where identity fraud risks were posed due to the granting of access to client funds or confidential information without the adequate verification of the identity of the party seeking such access or information.40

- Transaction reporting, record-keeping & pricing failures: These are cases alleging inadequacies in maintaining accurate records and/or reporting such records in a timely and accurate manner. They often relate to failures to provide accurate and timely transaction reports or to the mis-marking of securities.41

- Approved person regulation failures: These relate to breaches of the FSA's Approved Persons regulations, for example allowing an individual to hold a SIF such as director or officer, without obtaining the FSA's approval, or a failure to notify the FSA of a regulatory investigation in respect of an approved person in the UK.

- Failure to prevent misconduct: These relate to cases in which the FSA sanctions managers (e.g. SIFs) not directly involved in underlying misconduct but in a position to have prevented misconduct committed by others.42

- Other: In recent years these cases consist mainly of fraudulent mortgage applications (the mortgage fraud cases in this category are broken out on Figure 6).43

Characteristics of Recent Enforcement Actions Involving Financial Penalties

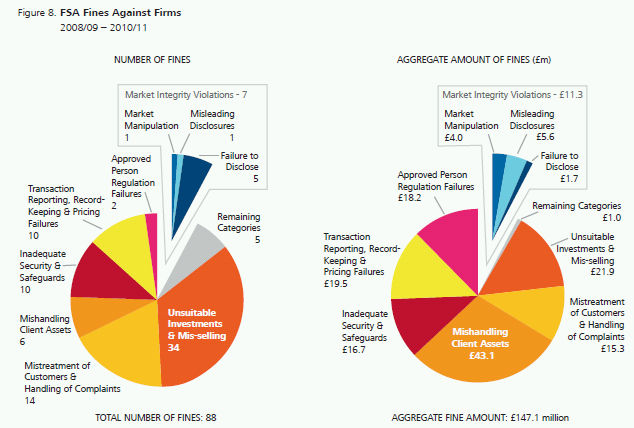

The breakdown of fines against individuals and firms over the past three fiscal years is depicted in Figures 6, 7 and 8, and is presented in terms of the number of cases, the aggregate amount of fines and the median fine in cases of each type. The mix of cases against individuals and firms differs, with relatively more fines imposed against individuals in market integrity cases. Some categories account for a larger number of fines, but a relatively small fraction of fine amount paid, while other categories account for just a few fines but a much larger fraction of fines paid. This can be due to the effect of a few very large fines or a difference in the size of typical fines in the category.

Fines against individuals

Market integrity violations

For individuals, market integrity cases—comprising insider dealing, market manipulation and misleading disclosures44—account for less than a third of fines levied during the three years ending 2010/11 (31 of 98) but well over half the aggregate value (£7.3 million of £12.5 million), shown in Figure 6. In particular, cases alleging market manipulation represented just five fines levied against individuals over this period, but accounted for about £3.2 million in aggregate value, more than a quarter of the total. The market manipulation category is dominated by a single fine, assessed in May 2010 against Simon Eagle for share ramping. This accounts for £2.8 million and is the highest fine levied by the FSA against an individual by a substantial margin. It includes disgorgement of £1.3 million and a penalty of £1.5 million. The Eagle case is only the second time disgorgement has been ordered from an individual for market manipulation. (In this case, Winterflood Securities Ltd. was also fined £4 million, of which £900,000 was disgorgement.)

Insider dealing cases accounted for 22 fines over this period, about three-quarters of the fines assessed against individuals in market integrity cases and nearly a quarter of all fines against individuals. Aggregate fines for insider dealing totalled £2.8 million, of which 38 per cent or approximately £1.1 million represents disgorgement. Insider dealing cases resolved with a fine represent only about half the number of all insider dealing cases in which the FSA imposed a fine or indicted an individual. Since it issued its first indictment for insider dealing on 22 January 2008, the FSA has indicted a further 27 individuals, including 26 in the three years ended 31 March 2011.

The size of fines in typical insider dealing cases against individuals, measured by the median fine in the three years ending 2010/11, is not as high as the median fine in three other categories: market manipulation; misleading disclosures; and transaction reporting, record-keeping & pricing failures (see Figure 7). The median fine of £90,000 means that at least half the individuals fined for insider dealing would likely have received a higher fine under the new penalty framework, which imposes minimum penalties. For market abuse occurring on or after 6 March 2010, the minimum individual penalty before any early settlement discount is £100,000.45 To date, 22 per cent of market abuse fines against individuals have included a penalty of more than £100,000 and although the FSA increased its investigations of SIFs threefold in 2008/09 and fined four individuals,46 few cases have been brought against senior managers at financial sector institutions.47 Recent publicity regarding the successful prosecution of hedge fund Galleon Group co-founder Raj Rajaratnam in the US may have put pressure on the FSA to act against insider dealing by high-profile financial professionals, not just the "small fry."48 It remains to be seen whether the FSA—and, later, the FCA—will further step up and/or refocus enforcement efforts related to insider dealing as a result.

Customer protection and compliance failures

Twenty-one fines fell into the category of unsuitable investments and mis-selling, more than for any other category of customer protection and compliance failures, of which there were 67 fines total during the three years ending 2010/11 (see Figure 4). However, fines for unsuitable investments and mis-selling have tended to be relatively small, typically about £25,000, as compared to a median of £53,000 for mistreatment of customers & handling of complaints, for example (see Figure 7).

The next largest number of fines was in cases relating to mortgage fraud: 16 fines totalling £1.7 million. This is an issue that the FSA has prioritised recently.

Transaction reporting, record-keeping & pricing failures accounted for only three fines against individuals but £0.9 million in total fines. This includes a £750,000 fine assessed on a senior trader at Toronto Dominion Bank for deliberately mismarking trading positions.

Fines against firms

Figure 8 depicts the mix of types of cases in which the FSA has levied fines against firms over the last three fiscal years. During this period, there were only seven market integrity-related cases against firms. Although two fines (one for market manipulation and the other misleading disclosures) were large (£4 million and £5.6 million, respectively), the other five were for failure to disclose with a median fine of only £350,000 (see Figure 7). However, the FSA also brought 10 cases of transaction reporting, record-keeping & pricing failures, which are aimed in part at ensuring that it has the information with which to detect conduct such as market manipulation and insider dealing. The fines imposed in cases involving transaction reporting failure amounted to £19.5 million, with a median fine value of £1.5 million, the highest for any category of customer protection and compliance failure.

The largest number of fines against firms (34 of 88) was imposed in cases in the unsuitable investments & mis-selling category. However, such cases accounted for a considerably smaller fraction of the aggregate value of fines, with a median fine amount of only £35,000. The greatest aggregate value of fines was imposed in cases alleging mishandling of client assets. This category includes the £33.3 million fine against JP Morgan Chase announced in June 2010, for failure to segregate client assets, the largest fine imposed by the FSA to date. The median fine in this category was £819,000.

Other significant categories of fines against firms included mistreatment of customers & mishandling of complaints (14 fines, £15.3 million in aggregate fines) and approved person regulation failures (only two fines, but £18.2 million in aggregate fines, including the £17.5 million fine assessed on Goldman Sachs International in September 2010 for failing to inform the FSA of an active SEC investigation of approved person Fabrice Tourre as well as of Goldman itself).

Top 10 FSA Fines to Date Against Individuals and Firms

The large recent jump in aggregate fines described above is in large part due to the increased frequency of very large fines. Indeed, our lists of the top 10 fines through June 2011 against individuals and firms are dominated by recent cases.

The top 10 fines for individuals, shown in Figure 9, range from £320,000 to the £2.8 million fine against Simon Eagle, the former chief executive of a stock broking firm and client of Winterflood Securities, for manipulating the share price of an AIM-listed company. As noted above, Eagle's fine consisted of £1.5 million in penalties and £1.3 million in disgorgement. Eight of the highest 10 fines against individuals were levied since the beginning of 2010, including the top three. All but one was for alleged market integrity violations. Three were for making misleading disclosures.

The top fines against firms related to a variety of different categories of misconduct, the majority of which were for alleged customer protection and compliance failures (see Figure 10).49 Unsurprisingly, even the smallest of these fines, at £5.6 million, substantially exceeds the largest ever fine for an individual (the median fine against a firm over the three years ending 2010/11 was 10 times the median against individuals). All but three of the top fines against firms were levied in the last three fiscal years. While the FSA has imposed relatively few fines against firms for alleged market integrity violations, the few fines it has imposed have tended to be large and account for four of the fines in the top 10 list: the third-highest ever fine of £17.0 million against Royal Dutch Shell for misstatements relating to its oil reserves; a nearly £14 million fine assessed in 2005 against Citigroup Global Markets Limited relating to alleged manipulation of European government bond markets; a 2006 fine against Deutsche Bank for £6.4 million relating to two instances of alleged market manipulation; and a 2008 fine against Credit Suisse for £5.6 million relating to misleading disclosures in relation to the market for certain asset-backed securities.

Trends in the Number and Mix of Cases

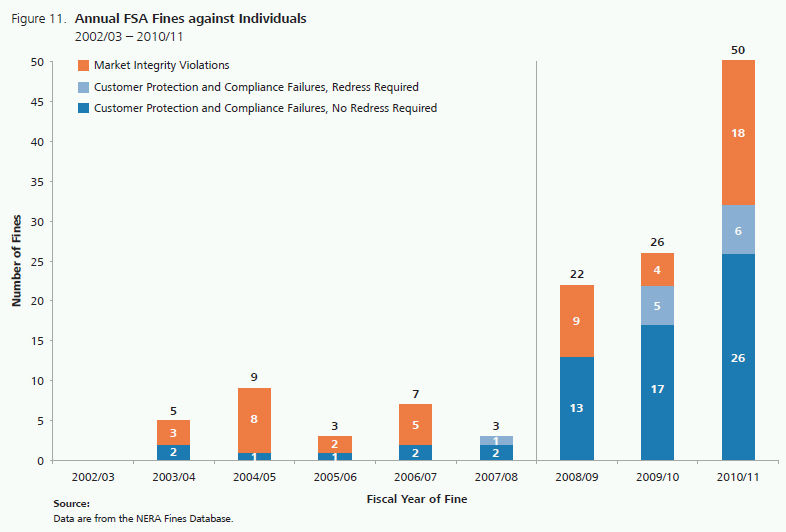

An increase in enforcement activity is apparent since the change in the FSA's stated enforcement philosophy around the second half of 2007.50 Especially for individuals, enforcement action resulting in fines against individuals and firms increased in number beginning in 2008/09. Figures 11 and 12 show the number of fines imposed in each FSA fiscal year (ending 31 March) since 2002/03 against individuals and firms. The increase in the number of fines imposed on individuals was dramatic, rising to a level in 2010/11 more than 10 times the average level over the six years prior to 2008/09. The number of fines against firms rose to a level in 2010/11 almost double the average in the six years prior to 2008/09. This increase is almost entirely explained by the increase in fines against firms for customer protection and compliance failures. Fines for market integrity violations by firms remain a relative rarity, although the five fines for failure to disclose since 2008/09 (shown in Figure 5) represent a doubling of the frequency of such cases compared to the prior six years.

We also identify cases in which redress was required by the FSA on Figures 11 and 12 based on our review of Final Notices and press releases. The proportion of cases against firms in which the FSA has required redress over the last three fiscal years is about the same as over the prior six (see Figure 12). However, whereas there was only one case against an individual in which redress was paid prior to 2008/09, there were 11 such cases in the last three fiscal years (see Figure 11).

Figures 13 and 14 show that aggregate fine amounts have increased dramatically for both firms and individuals, beginning in 2008/09. The typical size of fines rose (represented by the median fine amounts in each year) and there was a substantial increase in aggregate amounts due to a few very large fines. The proportion of penalties levied in customer protection and compliance failure cases rose. These increases are consistent with the FSA's published enforcement approach, which in 2007/08 stated, "where there is evidence that standards are not improving, despite clear messages to the industry, we have moved towards increasing the level of penalties." For individuals, the £8.6 million in fines announced in 2010/11 is more than three times the previous year's £2.5 million, which was itself a record high. The difference is largely due to the £5.0 million contribution of fines among the top 10 for individuals over fiscal years 2002/03 - 2010/11, including the largest-ever fine of £2.8 million.51 A similarly striking increase is observed in fines against firms, with total fines rising to an all-time high of £90.0 million in 2010/11 compared to £30.9 million the prior year. The top 10 fines against firms contributed £64 million to the 2010/11 total compared to £15 million in 2009/10.

While the rise in aggregate fines has been most dramatically influenced by a few very large fines, the size of more typical fines has also grown in recent years. The median fine against individuals was around £15,000 in 2004/05 and reached an all-time high of about £75,000 in 2010/11 (see Figure 13). Median fines against firms have only recently increased from a low of about £63,000 in 2008/09 to £595,000 in 2010/11.

Recent Trends in Enforcement: Additional Detail

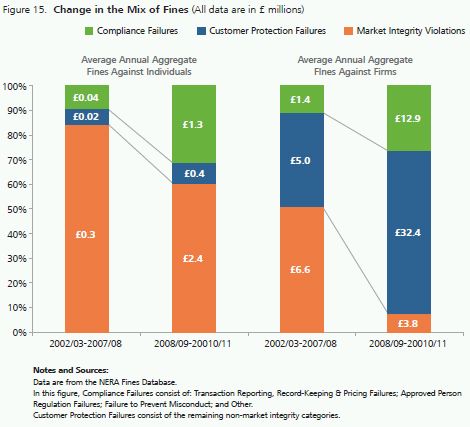

Figure 15 provides more detail on the shift in enforcement activity since the beginning of fiscal year 2008/09, focusing on the change in average annual aggregate fines. The increase in average annual aggregate fines against individuals for compliance failures is largely due to cases of mortgage fraud. The mix of the aggregate value of fines has shifted away from market integrity cases due to a slower increase in aggregate fines for such cases. The amount of fines imposed on firms for customer protection and compliance failures increased in absolute terms and relative to the amount of fines for market integrity violations. Fines for market integrity violations by firms have dropped from over half of average aggregate fines to less than 10 per cent, indicating a major apparent shift in the focus of enforcement against firms.

In 2009/10 the FSA predicted that the adoption of its new penalty framework "could see enforcement fines treble in size".52 Aggregate fines in 2010/11 were indeed nearly three times the 2009/10 level, but this was not a consequence of the new framework, which was not in effect when the alleged misconduct penalised in 2010/11 occurred.53 Since many fines are still below the level authorised under the new framework, and the median fine against firms actually declined in 2010/11 compared to the prior year, it is likely that the size of the typical fine will increase as fines begin to be determined under the new penalty framework.

Disgorgement and the Relationship between Financial Penalties and Illicit Profit

In addition to tracking fines, we also record in our database which cases resulted in the disgorgement of profits earned by firms and individuals in connection with alleged misconduct. The FSA may order disgorgement in any case in which it is "able to identify a benefit directly derived from the breach, whether in the form of a profit made or a loss avoided, and such benefit is quantifiable."54 Over the period 1 April 2002 to 31 March 2011, for 47 of the 319 fines imposed by the FSA, at least a portion of the fine was identified as disgorgement.55

Most cases in which disgorgement has been ordered are those alleging market integrity violations. For example, over the period covered by our database, three of four market manipulation cases against firms and 21 of 33 insider dealing cases against individuals have involved disgorgement. Over the past three fiscal years, more than half of market integrity fines against individuals have involved some form of disgorgement (see Figure 5). Market integrity cases for which disgorgement is not required include insider dealing violations by individuals who the FSA determines received no direct monetary benefit. Disgorgement has also been ordered in cases alleging customer protection and compliance failures, such as mortgage fraud and kick-backs.56

Under the new penalty framework in force for misconduct taking place on or after 6 March 2010, penalties for individuals in market abuse cases, even of moderate severity, are computed based on twice the amount of any illicit profit.57 For the most serious cases of market abuse, penalties are based on four times improperly earned profits (before any discount for cooperation) and a minimum of £100,000.58 Figure 16 plots penalties and corresponding disgorgement for cases announced through 2010/11 (none of which were determined under the new framework). In the vast majority of cases to date, penalties have not exceeded four times disgorgement (used as a benchmark for illicit profit), suggesting that the new penalty framework may substantially increase penalties in many cases.

However, in some cases involving serious misconduct by individuals prior to March 2010 (mainly mortgage fraud cases), £100,000 penalties were imposed even when the improper financial benefit disgorged was much less. For penalties in many of these cases, the implied multiple of disgorgement is much greater than four.

Future Trends in Enforcement

It is more difficult to predict whether recent increases in aggregate fines will continue. In 2010/11, over £69 million of the £98.6 million in fines59 was in cases with fines among the top 10 for firms or individuals over the period from 2002/03 to 2010/11 (see Figure 2). A total of £64 million in fines was paid in just four cases. As the circumstances giving rise to the very largest fines are typically idiosyncratic, it is possible that the aggregate amount of fines could decline next year absent a handful of the types of cases that give rise to exceptionally large fines.

Continuing increases in enforcement activity may depend in part on the resources available to the FSA's Enforcement and Financial Crime Division (EFCD). Between 2007/08 and 2010/11, staffing within the enforcement division increased by 42 per cent or more from a headcount of 22560 to more than 319.61 Over the same period, the number of enforcement cases resolved with fines approximately quadrupled (from 21 to 85) and the overall number of enforcement actions/disciplinary actions taken by the RDC rose by 52 per cent (from 93 to 141).62 Possibly as a consequence of more vigorous enforcement by the FSA, a greater proportion of cases are expected to be contested by referral to the FSMT,63 putting additional demands on enforcement resources. Figure 17 shows that, as of 2009/10, fewer than half of public disciplinary actions resulted in an RDC decision and about a third of these cases were referred to and decided by the Tribunal. In 2010/11 Tribunal referrals increased from 25 to 40;64 however, this increase is yet to be reflected in an increase in Tribunal decisions. We will track future trends in Tribunal referrals, decisions in these cases, and how enforcement resources change as the FSA is superseded by the FCA.

Criminal Prosecution and Other Non-Financial Sanctions

The more forceful recent enforcement stance of the FSA appears to be reflected not only in fines but also in the increasing numbers of cases in which the FSA has used its powers to:

- censure firms or individuals;

- restrict individuals' ability to engage in certain regulated activities (prohibition);

- enjoin conduct or order restitution; and,

- bring criminal prosecutions.

As shown in Figure 18, the use of censure, prohibition and civil powers has increased alongside the increase in the number of fines. Indeed, beginning in 2007/08 the frequency with which prohibition powers were employed increased from less than half the frequency of financial penalties to about the same frequency in 2010/11. This is consistent with a shift towards taking stronger action against individuals.

Figure 19, which is based on information from press releases, shows that over the past three years the FSA brought an increasing number of criminal cases, reaching a high of five cases in 2010/11; however, the four cases brought in 2009/10 involved a larger number of individuals. In fact, the 17 individuals indicted in 2009/10 exceeded the total number indicted over the prior seven years (the balance of the period for which data is available). Ten individuals were indicted in five cases last year and there are a total of 21 individuals with criminal actions pending against them, 16 in insider dealing cases. As of the end of 2010/11, the FSA had secured convictions in six insider dealing cases (four in 2010/11), involving nine individuals, and one acquittal, which is being appealed. Most recently, David Mason was sentenced to two years in prison in a boiler room case. He pled guilty to money laundering and misleading statements charges.65

Redress

In addition to levying fines and demanding disgorgement of any benefits derived from misconduct, the FSA may also order compensation paid to those who suffered a loss but must take account of the availability of compensation available from other sources (e.g. the Financial Services Compensation Scheme, and the Financial Ombudsman Service).66 In December 2010, the FSA was given additional industry-wide powers of redress. It now has rule-making authority to establish a customer redress scheme in cases of "widespread or regular failure by relevant firms [...] [resulting in] loss or damage in respect of which, if [customers] brought legal proceedings, a remedy or relief would be available."67

The most common examples of enforcement actions involving redress are mis-selling cases and have to date involved products including: mortgage endowment policies, split capital investment trusts, high-income bonds and most notably PPI. In large cases, the amounts paid in redress can dwarf even the highest fines ever assessed by the FSA. For example, redress was estimated at £120 million to £160 million in a suitability case against Abbey National in which almost 50,000 customers may have been sold risky mortgage endowment policies; the fine in this case was £1 million.68

The FSA has brought 24 enforcement actions regarding the mis-selling of PPI, and imposed fines totalling £13 million.69 The largest individual fine of £7 million was imposed on Alliance and Leicester (listed in Figure 10). As a result of its enforcement actions against individual firms, company-specific programs of redress were established. In addition, almost 200,000 complaints were lodged for PPI violations with the Financial Ombudsman Service.70 However, the FSA decided that an expanded industry-wide program was needed, starting with a review of past sales of PPI and requiring redress even where customers had not yet made a complaint.71 It has been estimated that total redress amounts owed in connection with PPI mis-selling could total £9 billion.72 Lloyds TSB has announced that its exposure alone is expected to exceed £3 billion.73

Prior to 2005, the FSA reported the estimated amount of compensation expected to be paid out to deliver customer redress in each case resolved with a fine and listed amount on the fines table. In these specific cases, the amount of redress ranged from £10,000 to £120 million.74 Since then, estimates have been dropped from the FSA fines table and have not been consistently reported in final decisions, making analysis of redress difficult on a case-by-case basis.75

However, the FSA has recently begun to publish aggregate data on redress payments. The total paid by regulated firms in 2010/11 was £854 million. More than two-thirds of this amount was paid in connection with general insurance and "pure protection insurance" claims, driven significantly by PPI mis-selling claims.76 The other categories of claims in which redress was paid are: banking (£85 million); home finance (£11 million); decumulation, life and pensions (£75 million); and investments (£90 million). Redress payments rose in the second half of 2010/11 by 56 per cent over the same period a year earlier; however, this increase was entirely attributable to an increase in general insurance and "pure protection insurance" claims.

Although the FSA has not required redress for investor losses in market integrity cases to date, it has the mandate and powers to do so.77 One reason for this may be that investor losses caused by misconduct are in many cases difficult to define.78 However, the recent statutory expansion of issuer liability was in part due to recognition that investors can be harmed by market manipulation, misleading disclosures and disclosure failures. It may be that in future the FSA will see fit to order redress in cases involving violations of market integrity.

Increased Costs of Non-Monetary Sanctions

In addition to the cost of fines, firms and individuals face increased costs associated with prohibition, the production of Skilled Persons Reports and potential lost profits associated with suspension of selected business operations authorised under new powers introduced by the Financial Services Act 2010.

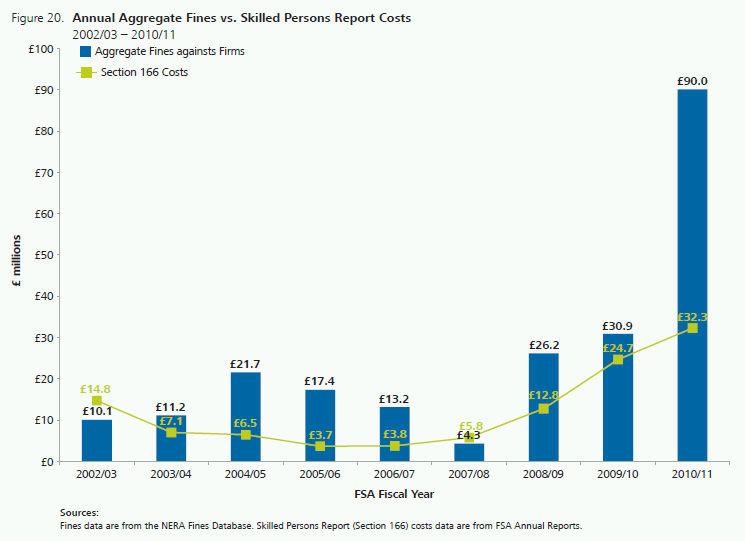

The FSA can demand Skilled Persons Reports under Section 166 of the FSMA to provide an independent view of aspects of a firm's activities under investigation.79 The costs of the expert analysis required by the FSA may be significant. Indeed, as shown in Figure 20, in aggregate these costs reached £32.3 million in 2010/11, more than the aggregate amount paid by firms in fines in any prior year. The average estimated or actual cost of the 95 Section 166 studies ordered in 2010/11 was £340,000.80 This is a 70 per cent increase in average cost per report since 2007/08. According to the Treasury's white paper, the government proposes to expand the authority of the FCA to order Skilled Persons Reports in connection with its investigation of listed firms and not just authorized financial firms it supervises, which could further increase aggregate Section 166 costs.

The FSA has yet to exercise its new power to suspend selective business operations for up to a year in conjunction with other enforcement action against firms or individuals.81 However, in the future temporarily curtailing certain operations could be disruptive and result in significant, consequential costs and lost profits. These costs could easily exceed the amount of a penalty based on a multiple of illicit profit.

Effectiveness of the FSA's Credible Deterrence Strategy

The FSA acknowledges that it is difficult to measure the effectiveness of its deterrence strategy or to determine whether its sanctions are sufficiently severe to induce a change in behaviour.82 However, the FSA concluded that an increase in penalties was needed as part of the new penalty framework that came into effect last year, based on the observation that "breaches in particular areas (for example, the sale of PPI and market misconduct) [have repeatedly been seen] where insufficient account has been taken of previous enforcement action."83 Once the effect of increased penalties is realised in the coming years, we will have the opportunity to observe whether such patterns of repeated violations persist, in which case further increases in fines may be considered necessary.84

The FSA already publishes certain metrics of its performance in "maintaining market confidence and fairness" through minimising insider trading and market abuse. These metrics are known as "market cleanliness statistics." However, the only metric that is closely related to FSA enforcement activity85 measures abnormal pre-announcement price movements (APPMs),86 an indicator of possible insider dealing. The level of such potentially suspicious trading activity prior to initial public offerings declined in 2010/11; however, it is difficult to judge whether this is a result of stepped-up detection and enforcement.87 The FSA does not publish metrics relevant to the incidence of other forms of market abuse, specifically events of market manipulation or misleading disclosures.

While insider dealing enforcement activity is at an all-time high, the frequency of actions against firms for market manipulation and misleading disclosures has declined. There was only one fine against firms in each of these categories during the last three years (see Figure 5). According to HM Treasury, creating the right incentives for "timely, comprehensive and complete reporting by companies is a crucial element to promote the allocative efficiency of capital markets."88 While it is possible that the threat of sanctions has deterred misleading disclosures, the higher level of enforcement activity and litigation in other jurisdictions suggests that more action may be warranted to detect and sanction misleading disclosure practices.89 Potential misstatements by public companies are commonly identified in other jurisdictions by unexpectedly large drops in stock prices in connection with the revelation of adverse news that allegedly should have occurred earlier. Similar events undoubtedly occur in UK financial markets. While most unexpected stock price drops are caused by timely, accurate news and changes in market conditions, material misstatements may increase the frequency of such events. Consequently the frequency and magnitude of large stock drops, even if only modestly correlated with misstatements or delays in disclosure across the market as a whole, could provide an additional metric of market cleanliness, useful in identification of possible misconduct and in assessing the effectiveness of enforcement activities.90

Future of Enforcement by the FCA

As described in the government's recent financial regulatory white paper, when the FSA is disbanded, most of its enforcement functions will be transferred to the FCA.91 The FCA is expected to come into existence in late 2012 or early 2013.92 It will be headed by Martin Wheatley, previously the CEO of Hong Kong's Securities and Futures Commission.93

Public statements by the government and FSA indicate that the FCA will continue to pursue "credible deterrence" as the FSA has done, but that enforcement may change in several respects. For example, a consultation paper by the Financial Secretary of the Treasury warns firms to expect "a marked difference in supervisory approach, as the FCA places conduct, and more specifically the prevention of consumer detriment, at the heart of its operating model."94

As that statement suggests, it is envisaged that the FCA will prioritise the protection of retail investors. In this sphere, the new authority will aim to be more proactive, and will be given certain new enforcement powers. In particular, the FCA will scrutinise the design of new retail financial products with the aim of identifying at an early stage those that pose substantial risks to retail investors.95 If the FCA identifies such a product, it may mandate minimum standards, restrict the sale of the product to certain types of investors or ban the product altogether. The FCA will also be able to direct firms to withdraw or amend financial promotions that it considers misleading, and publicise that it has done so. In addition, the FCA will have a duty to promote competition in financial services.96

It is unclear to what extent the shift in stated policy emphasis and new powers will change disciplinary enforcement activity as compared to the FSA's approach over the past several years, and what the effect will be on trends in civil sanctions. In theory, if the FCA is successful in the early identification and mitigation of risks to retail investors, a lower level of ex post enforcement might be necessary. However, the stated intention of the FCA to adopt a proactive approach is consistent with a shift in enforcement already implemented by the FSA in recent years. For example, the first Retail Conduct Risk Outlook was published earlier in 2011, identifying risk areas and issues on which the FSA expects to focus its attention.97 This is not dissimilar to the FCA's intended emphasis on "issues-based supervision": the identification of misconduct that affects an entire sector or type of product, which could result in fines being levied across many firms simultaneously in respect of a single issue.

Similarly, while the FCA is to be focussed on protecting consumer interests, the FSA has already placed an emphasis on consumer issues, as evidenced both by its public statements and the concentration of fine activity in areas such as unsuitable investments and the mishandling of client assets. Moreover, some of the new enforcement powers to be given to the FCA already reside with the FSA, albeit in more limited form. For example, the FCA is to be given greater flexibility to publicise the fact that a warning notice has been issued, disclosing an investigation before the final notice stage.98 Currently, the FSA may disclose negotiations, though its existing authority to do so is more restrictive.99

The new product intervention powers to be given to the FCA arguably could have reined in PPI sales practices and avoided much of the fallout from mis-selling activities that have been the subject of subsequent enforcement action.100 In practice, however, drawing a line between acceptable and unacceptable product design, development and management in advance of any problem at the point-of-sale may be difficult and could risk limiting the scope of economically beneficial financial services business.

Conclusion: Looking Ahead

The imposition of fines, prohibition sanctions and criminal prosecution by the FSA have increased over the last several years, which reflects the more assertive enforcement stance articulated by the authority's enforcement division. Both the number and aggregate amount of fines have risen. Fine activity may continue to increase as enforcement cases are resolved under the new penalty framework and a greater number of cases are contested. The transfer of responsibility for enforcement to the FCA may also affect the enforcement activity and outcomes. NERA will continue to track and analyse trends in enforcement activity and report on these developments.

To read this report and footnotes in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.