In addition to recently announced changes to the Green Deal (requiring certain let property energy efficiency) and the announcement of the Fourth Carbon Budget, on 11 May 2011, the Department for Environment, Food and Rural Affairs (Defra) and the devolved administrations, launched a consultation called: "Measuring and reporting of greenhouse gas emissions by UK companies: a consultation on options" (the Consultation).

The Consultation, which closes on 5 July 2011, sets out four options to promote more widespread and consistent corporate reporting of greenhouse gas (GHG) emissions. One option is for voluntary reporting and three of the options are for mandatory reporting. All are designed to help meet the Government's climate change obligations under the Climate Change Act 2008 (CCA 2008). This briefing sets out the current and proposed regime options together with concluding remarks.

Background – Climate Change Act 2008

One of the CCA 2008's objectives is to make the UK's voluntary national targets for the reduction of GHG emissions legally binding. Specifically, the CCA 2008 requires the UK to achieve an 80 per cent reduction in GHG levels (below 1990 levels) by 2050. The Government aims to meet this legally binding target to cut GHG emissions by a system of five-yearly carbon budgets beginning with the period 2008-2012, with a key interim target of a 34 per cent reduction by 2020. The Fourth Carbon Budget was announced on 17 May 2011 and proposes a legally binding interim target to reduce emissions by 50 per cent by 2027.

Section 83 of the CCA 2008 requires the Government to publish guidance on the measurement and calculation of GHG emissions. Accordingly, on 1 October 2009 Defra and the Department of Energy and Climate Change (DECC) produced guidance on how to measure and report GHG emissions with the aim of supporting UK organisations in reducing their contribution to climate change1.

Section 84 of the CCA 2008 requires the Secretary of State to review and report to Parliament on the contribution made by GHG emissions reporting to the achievement of the UK's climate change objectives by 1 December 2010. Defra subsequently published its review on 30 November 2010, which indicated that companies focusing on climate change through measuring, managing and reporting GHG emissions, experience benefits in terms of cost savings, brand building and stakeholder communications2. However, this review did not give a clear recommendation in favour of mandatory reporting.

Section 85 of the CCA 2008 requires the Secretary of State, by 6 April 2012, to either: (i) make regulations under section 416(4) of the Companies Act 2006 (CA 2006)3, requiring directors' reports to contain certain specified information about GHG emissions from activities for which the company is responsible; or (ii) lay a report before Parliament explaining why no such regulations have been made. Under this section, the Government launched the current Consultation on the options of GHG emissions reporting.

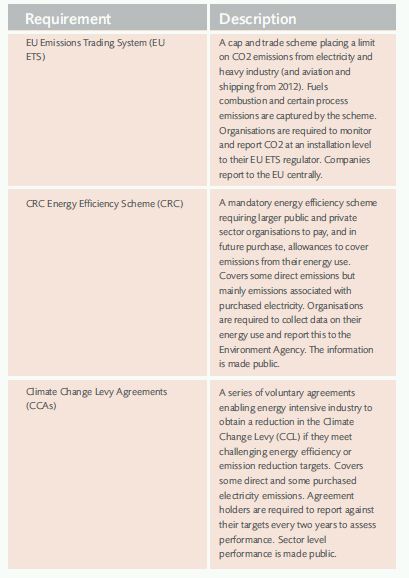

Current reporting requirements

Mandatory reporting

There are currently several requirements on organisations in the UK that require them to collect data and report on their emissions as part of the objective of improving energy efficiency. The following table provides a summary of three main requirements:

The EU ETS and the CRC are two of the main levers by which the UK will meet its climate change targets and are designed to deliver a significant proportion of the emissions reductions needed.4

Voluntary reporting

Even if a company is not required to report on environmental matters, it may still choose to do so on a voluntary basis. There are a number of schemes available for companies to do voluntary reporting, such as the Carbon Disclosure Project (CDP). CDP is a not-for-profit organisation, acting on behalf of nearly 500 institutional investors and sends a request for information to FTSE listed companies on an annual basis. The data request asks for information on companies' emissions, climate strategy and action plans and the information provided is used to compile an annual climate leaders' index which ranks companies in terms of their performance.5

Four options for corporate reporting under the Consultation

Option 1: enhanced voluntary reporting

The Consultation points out that there are already a number of companies reporting voluntarily on their GHG emissions, which is supported by guidance by Defra and the DECC. Suggested options to enhance current voluntary reporting include:

- implementing increased awareness of the benefits of reporting, of the Defra/DECC guidance and existing schemes;

- support for and collaboration with the CDP and other non-governmental organisations (NGOs) to increase the demand for and use of company reports by investors and other interested parties;

- work to develop sector-specific voluntary agreements; and

- bilateral voluntary agreements between the Government and companies by size band.

Significant engagement with such voluntary approach could of course minimise additional regulatory burdens on companies, but is likely to require additional guidance.

Option 2: mandatory reporting for all quoted companies

This option would require all quoted companies6 to include GHG emissions reporting in their directors' report. The rationale behind this option is that the provision of information on GHG emissions by these companies is likely to be of most interest to investors and potential investors. Option 2 would cover around 1,100 companies (based on September 2010 figures) which are already required under the CA 2006 to include information about environmental matters in their business review to the extent necessary for an understanding of the development, performance or position of the company's business. It is not proposed that any new requirements would form part of the business review provisions.

This option would not include large private companies.

Option 3: mandatory reporting for all large companies

This option would require all large companies, defined in certain sections of the CA 2006 using measures of employment, gross assets and turnover, to report on their GHG emissions in their directors' report. This would cover between 17,000 and 31,000 large UK companies and would include the large private companies not captured by option 2.

Option 4: mandatory reporting for all companies whose UK energy consumption exceeds a threshold

This option would require all companies whose UK consumption of electricity exceeded a minimum threshold of half hourly metered electricity in one year to report on their GHG emissions in their directors' report.

The aim of this option is to cover the largest energy users. It would capture companies consuming more than 6,000 MWh of qualifying electricity per annum, which is the same qualifying criterion under the CRC. These companies would then be required to report using either the CRC reporting criteria or the Defra/DECC guidance. However, it would not cover companies with low UK electricity consumption but high GHG emissions from other activities, such as transport or processing or overseas activities. As approximately 4,000 companies consume more than the proposed threshold of 6,000 MWh of electricity each year, this option may involve lowering the energy threshold to potentially cover up to around 15,000 companies.

It is pointed out in the Consultation paper that one of the disadvantages of this option is that, in contrast to options 2 and 3, it does not use existing definitions for types of companies under the CA 2006. It would thus introduce separate criteria for companies to be covered by these reporting requirements.

Conclusion

While an increasing number of businesses are being open about their emissions and environmental risks, a study of over 500 FTSE All-share companies reveals that only a minority of companies are providing environmental statistics in line with Defra/DECC guidance.7 However, access to environmental information is said to be playing an increasingly important role in investors' decision-making:

"The increasing financial significance of many environmental risks and opportunities means that now more than ever investors need clear, comparable environmental information to help them decide where to invest their money. Businesses that measure their environmental impacts and risks are also better placed to manage and reduce them."8 Environment Agency Chief Executive, Paul Leinster.

Whilst reducing expensive energy consumption makes good business sense, the historic, relatively low price of energy has prevented energy efficiency being a priority. Whether business likes it or not, the UK's legally binding emissions reduction targets are now starting to bite the wider business community, first with the CRC and now with mandatory reporting on the horizon. Given that management will likely be forced to spend time measuring and reporting on emissions, now may be the time to start implementing emissions reporting tools voluntarily.

Footnotes

1 Guidance on how to measure and report your greenhouse gas emissions, DECC & Defra, September 2009

2 The contribution that reporting of greenhouse gas emissions makes to the UK meeting its climate change objectives: A review of the current evidence, Defra, November 2010.

3 Regulations made under section 416(4) of the CA 2006 apply to UK incorporated companies that are required to prepare a directors' report as part of the company's annual report and accounts.

4 See footnote 2

5 See footnote 2

6 A "quoted company" means a company whose equity share capital: (a) has been included in the official list in accordance with the provisions of Part 6 of the Financial Services and Markets Act 2000 (c. 8), or (b) is officially listed in an EEA State, or (c) is admitted to dealing on either the New York Stock Exchange or the exchange known as Nasdaq. Section 385, CA 2006

7 Environmental disclosures, Environment Agency, 9 May 2011

8 More firms come clean on green performance, Environment Agency, 11 May 2011

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.