1. EXECUTIVE SUMMARY

This year will mark a turning point for the UK retailing industry. Driven by six key pressures, the UK retailing industry is undergoing a structural change that is forcing retailers to find different ways to view and think about their business in order to be successful. Recognising and acting on this ahead of competitors represents a strategic opportunity for all. In practice this is not only about innovating new products and services, but also about efficiently and effectively delivering what the customer has already stated they value. Excellence in operational delivery will come from rigorously assessing opportunities across the entire business, looking outside for inspiration, and installing the capabilities that will deliver strategy, whilst jettisoning functions that have become superfluous. All of this needs to be done without adversely affecting the customer experience; indeed it must measurably improve customer service. The customers' position has changed and organisations must understand these changes in order to re-structure to deliver a new set of expectations.

Since the collapse of Lehman Brothers in September 2008 and the subsequent recession, UK retailers have by and large reacted effectively. Costs have been reduced by finding cheaper sources, attacking indirect expenditure, reducing overheads and cutting store costs. A few retailers whose business models lacked coherence, or who were unable to respond fast enough, have shut up shop; whilst others have continued to find growth opportunities by expanding into new channels, geographies, and new products and services. At the end of the first-half of this change game we could declare: Retailers 1: Economy 0.

Understanding the nature of the game's second-half, and grasping this early on, will give retailers the best chance of making the right decisions, acting fast, and exploiting the many opportunities that will emerge. It is important to grasp the direction and speed of the structural change, the options different retailers face, and the range of critical actions that will deliver both the required margin and the operational capability for growth. The right responses will enable businesses to underpin growth, defend market share, and exploit any weaknesses in their competitors. The rules of this game are:

- understand the turning point;

- know your costs and value to determine where to excel, defend or exit;

- reset your target operating model; and

- implement quickly and continuously.

Ian Geddes

Head of UK Retail, Deloitte

2. ECONOMIC OUTLOOK

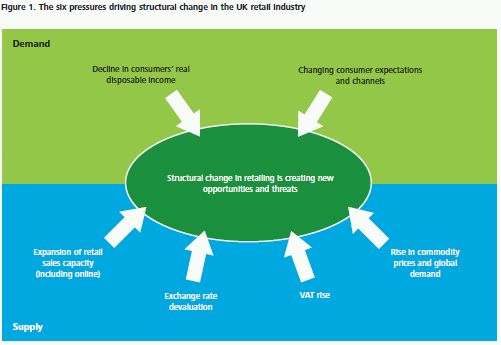

The UK retail industry has changed structurally. Consumers are increasingly faced with the situation where they might have to buy less, but spend more. Pressures on both demand and supply have been either emerging over a number of years or have begun to hit the market hard this year.

Demand

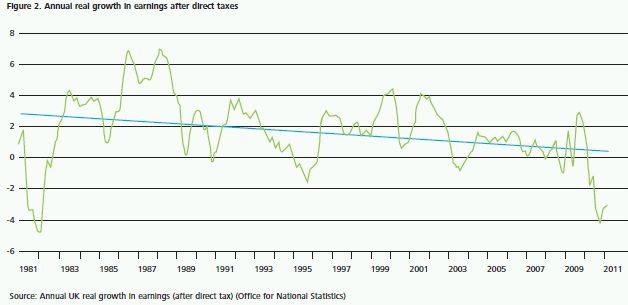

- UK disposable income is being impacted by public sector spending cuts, structural unemployment and high consumer debt. After taxes and inflation, the real spending power of UK consumers last year suffered the biggest decline in over 20 years. The start of this year has also seen consumer confidence fall faster than at any time in the last 16 years. In addition to this, it is probable that at some point interest rates will rise which will lead to further adjustment by consumers in their retail expenditure. Judging volumes, ensuring a clear targeting of segments and providing excellent service will be ever more important.

- Changing consumer expectations and channels. Over the last five years there have been substantial changes in the ways that people interact; the way that they want to interact with organisations has changed accordingly. Free delivery, Wi-Fi hotspots and a response to an email once delighted consumers but are now basic requirements, as are trust, authenticity and transparency. Consumers of all ages and backgrounds are online and mobile so retailers need to provide flexible customer service via a raft of communication channels including the internet, email, chat, social media, reviews, tweet, forums and SMS. The greatest challenge to retailers is that customer expectations are constantly changing. It is vitally important that retailers have effective, two-way communication channels with their customers so that they know when a 'delighter' has become a basic requirement.

Supply

- VAT has risen 2.5% in 2011 and is likely to stay at this historically record level. In a period of slumping consumer confidence an increase in VAT is effectively a tax on retailers rather than consumers. Initial attempts to absorb the increase in VAT are difficult to maintain when supply chain pressures are not equally suppressed, but as the year continues the VAT rise is likely to push up prices and further undermine demand. As with international cost changes this puts an increased focus on value and costs.

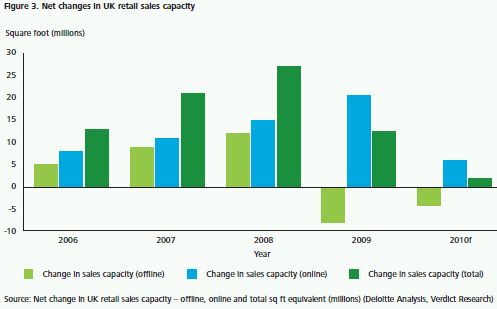

- Expansion of Total Retail Capacity. Retail floor space has grown continuously over several decades and at the same time trading hours have expanded. Demand has kept pace with this increase in space maintaining good sales density and margins. The recent recession broke the trend with a reduction in net space of 12 million square feet as retailers closed doors or exited the market altogether. In the meantime, online growth added the equivalent of 26 million square feet, resulting in a net sales capacity increase. Continued moves away from traditional bricks and mortar stores will further exacerbate existing cost pressures, endangering the survival of lower performing shops.

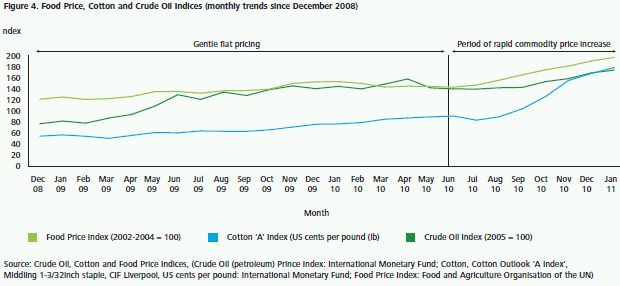

- Dependence upon international sourcing is rising. At the same time global food and raw material prices are also rising at an unprecedented rate. At the start of 2008 businesses were retailing in a market of supported demand and historically low input costs. This year the opposite is true; customer demand is constrained and input costs are rising at an extraordinary rate. Various factors are impacting global supply and demand; declining availability of resources, increased domestic consumption in emerging economies, and a scaling back of production in the sectors hardest hit by the recession, such as fashion and footwear, to name a few. These changes are difficult to reverse and have collectively contributed to a structural change in the global market. These changes will have short, medium and longterm effects, ensuring proactive sourcing strategies and the active management of costs are more critical than ever.

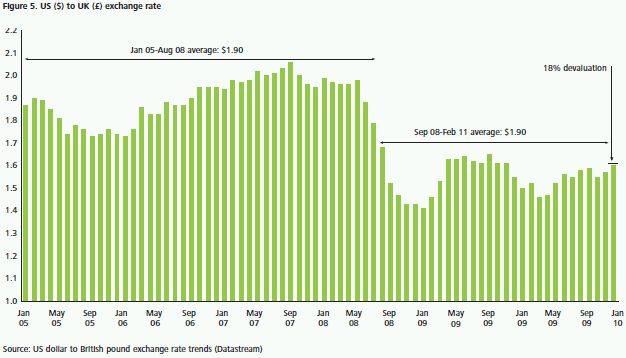

- Exchange rate devaluation. In addition to the global trends in commodities, the devaluation of sterling since 2009 has driven a marked increase in the cost of buying all imports. Together these pressures will lead to significant imported inflation pushing up cost of sales and reducing margins. Again sourcing will be crucial as will the ability to hedge effectively against adverse exchange rate movements.

In summary, the situation in 2008 was the result of a one-off event; the situation today, however, is not. These six pressures represent a structural change that will provide the backdrop for retailers for the foreseeable future. Retail margins are already generally low and the sensitivity to changes in volume and costs will be fully exposed in this year and beyond. Trading with the wind of growing demand behind your back has been comparatively easy. Going forward is going to be a considerably different game. The scores are yet to be determined.

3. BUSINESS MODEL CHANGES

Since 2008 retailers have taken action to reduce their costs, mainly by mobilising their internal resources to identify cost reduction opportunities. These efforts have been characterised by cost reductions in store operations and indirect expenditure, with a focus on cutting inventory levels and re-negotiating supply and payment terms.

Whilst the retailing industry as a whole has been working to reduce costs, a number of retailers have continued to identify growth opportunities and have increased sales and market share as a result. In Deloitte's experience many clients are pushing hard to develop their multichannel capability. A similar focus has been put on growing international sales, with even the smaller high street brands widening their sales opportunities outside of the UK. There has been an increase in the variety of products being offered as an increasing number of retailers seize the opportunity to augment food with non-food, or new services such as banking, insurance and media.

Many retailers have clearly made progress, but as structural change in the retail market becomes clearer, companies need to question whether their efforts are enough to deal with the challenges ahead. There are a number of important considerations:

- Tactical cost reductions make sense from a cost point of view but the impact on the customer must remain front of mind. For instance, wide-scale reductions in store staffing can reduce the ability to meet customer expectations of service and presentation.

- Continuous productivity improvement needs to be ingrained in retail organisations and it needs to address fixed as well as variable costs; to do so productivity analysis needs to become a way of life, as it has in some other industries.

- Investing in new channels, markets and products will drive sales, but as these offerings expand they require additional capabilities, which add cost. If they are simply bolted on to the existing operating model they can decrease profitability and reduce flexibility.

- The explosion of global supply is proving to be a double-edged sword. As dependence on low-cost, developing-economy suppliers has grown, the cost of their resources and production has started to rise in response to global shortages and growing demand in developing economies themselves.

We have seen that the challenges of 2008-10 have prompted numerous initiatives to reduce costs and create growth. However, the structural change in retail demand and supply mean that from now onwards retailers will need to weigh up a wider set of options, although as the next section demonstrates the number of options open to individual retailers will differ.

4. THE DELOITTE RETAILER FRAMEWORK

Tactical changes in costs and new growth initiatives, particularly since the recession, have left some retailers with a gap between customer expectations and the actual service which is delivered. As the structural pressures take effect, this gap is likely to grow. The question is how prepared are retailers for this pressure, and what actions do they need to take?

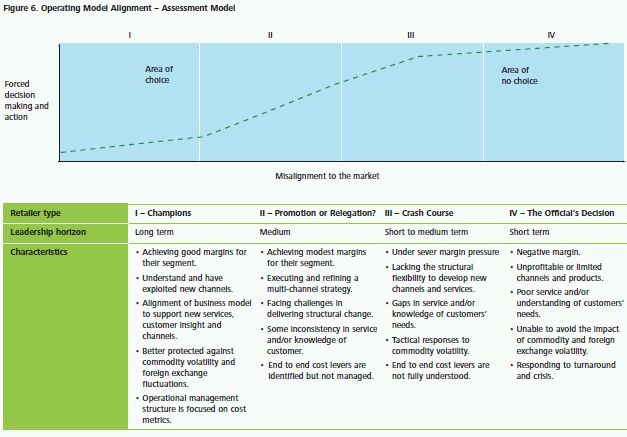

Deloitte has been using the Operating Model Alignment framework (Figure 6) to identify the types of challenges faced by businesses and options available to leaders. The dotted line maps a precipice between those businesses who have choice, and those that are significantly out of step with the market conditions and are forced down a different path. The rapidly changing retail environment is creating increasing pressure on all retailers to move towards the area of no choice, therefore this requires a proactive and sustainable effort to ensure this pressure is mitigated:

Type I retailers are Champions contemplating their position on the winners' podium. They are probably already a market leader or gaining share ahead of competitors and have an established brand position which is well understood by their target customers. Their capabilities are well aligned to the demands of both their current service and their new products and channels so as they grow, the customer expectations of service can still be met. Champions will continue to grow and will concentrate on improvement opportunities that support increasingly tailored and innovative customer offerings such as multichannel and mobile technologies. Using repeatable improvement methods and capabilities, Champions will achieve effective service and efficient delivery, implying a capability to eliminate waste in processes whilst driving improvement from a detailed understanding of customer requirements.

Type II retailers face either Promotion or Relegation. They are confronted by the threats of structural change and, whilst they may be targeting growth, they remain at risk of being pushed off course. They have emerged from the recession with some strengths and may have been increasing their market performance. However, continuous attention is required to defend against the competition and retain market share. Improvement opportunities will focus on maintaining expected service and targeting processes that are driving lower profitability. Typically these retailers should be focused on both reducing operational costs and increasing the effective throughput of growth areas.

Type III retailers have entered the area of restricted choice and may be heading for a crash. Leadership is critical to recognising this position and mobilising the organisation. The relatively benign nature of the market in the past, and the positive market growth, may have disguised underlying cost and performance problems. A clear understanding of costs and profitability will be crucial to re-align the operating model to the market. Type III retailers should focus on a rapid assessment of their structure, costs and working capital to ensure cash flow and to move back to consistent profitability.

Type IV retailers have very limited choices. Creditors and shareholders will be demanding both structural business changes and operational action. Structural changes will include financial restructuring of debt and the business portfolio. A focus on costs will be vital and will include both tactical changes and more far reaching structural changes. At the extreme, this can be accompanied by changes in leadership, or in the worst cases, transfer of the business to an administrator.

Wherever a retailer is in its readiness to meet the challenges of the new retail market, it is critical that there is an objective and rapid appraisal of the relative strengths and weaknesses of the current performance and operating model. For some retailers this will be about delivering the growth potential and maintaining profitability; for others this will be part of a defensive strategy to maintain market share; and for the rest, a rapid shift in the organisational focus may simply be a matter of survival.

5. FIVE ACTIONS FOR UNDERPINNING GROWTH

Whether focusing on growth, defending market share or fighting for survival, there is a need to review the impact of the market changes and react. This involves building up an outside-in view of what is possible and questioning performance against competitors, some of whom may be in distant geographies and markets.

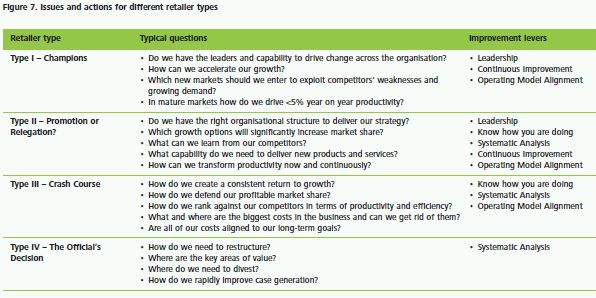

In Deloitte's experience, there are five key actions that should be considered to drive a cost reduction and operational improvement initiative:

- Leadership challenge – thinking and acting differently.

- Look outside – know how you are doing.

- Systematic analysis – structured approaches to analysing cost and value.

- Build continuous improvement capability – a competitive weapon.

- Alignment – operational capability and strategic priorities.

Figure 7 demonstrates how, for each type of business, the issues and actions will change in relative importance:

5.1 Leadership challenge – thinking and acting differently

Whilst 2008-10 was tough, today's retail leaders face a new challenge. Gone are some of the factors of the previous recession – cost deflation, low-hanging fruit, and a pre-election reluctance to make or even talk about "cuts". The shift in the UK retailing environment is having a polarising effect: the gap between 'winners' and 'losers' appears to be widening. Structural pressures are increasing and driving retailers from a Type II retailer to a Type III or IV, leaving them vulnerable to stronger competitors looking to grow their market share.

In this context leadership needs to exploit the external environment whilst aligning the organisations' functions and people. The direction of change needs to be recognised. This requires leaders throughout the organisation to recognise the changes in the external environment and the impact on customers, and the organisation's proposition.

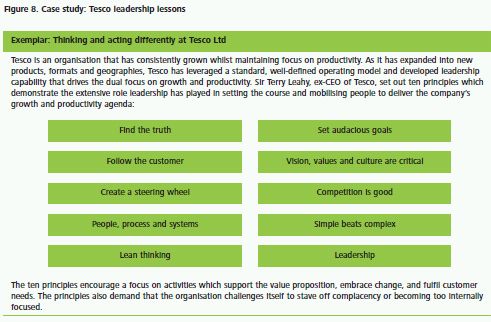

The speed of reaction of leaders and indeed the whole organisation will be crucial. This requires a consistent and widespread communication of the need for change. People need to be engaged to develop ideas to solve challenges and crises as they occur as well as to plan and prepare for the future. Tesco (Figure 8) demonstrates how leaders have consistently developed a climate and culture of challenge, external focus and change.

The depth of the required reaction marks a further significant difference from the previous recession. A tactical response, whilst helping in the short term, will not alone produce an effective response. Instead there is a need to structurally examine the business and produce end-to-end f lows to identify opportunities for operational improvement, cost-reduction and growth. This requires people who can take the customers' perspective and look across the organisation. The longer term vision also needs to be defined so that businesses have goals around which to structure themselves, and measures by which to evaluate success.

One thing that is clear is that the impact of structural change in UK retailing means that the role of leadership in framing the challenge, and mobilising people has never been more crucial.

5.2 Look outside – how are you doing?

To identify change opportunities it is important to examine the cost base and operational effectiveness with good data and an eye on what is going on 'outside'. Insight into how competitors are doing can dramatically improve strategy and investment decisions. This not only provides a better view of what is possible; but it can also identify how the possible can be delivered through effective operational improvement.

Traditional "financial ratio analyses" are often conducted to compare key metrics and cost structures with competitors. The difficulty in this approach is that specific elements of costs are summarised at such a high level that real cost performance cannot be easily ascertained. Furthermore, since these analyses use historical data, they do not accurately reflect the current cost realities. Process benchmarking provides a more leading indication of operational improvement areas, potentially preventing cost and poor performance issues, and ensuring a more granular understanding of the organisation's performance is developed.

Benchmarking provides objectivity, which is vital in challenging internal perceptions of performance and of what is possible. It provides insight into emerging practices as well as emphasising the upper performance of processes and functions. This helps to break away from 2-3% improvement targets that organisations will often generate through budgeting processes. Metrics such as shrinkage, merchandising cost and staffing can be compared with a defined set of industry peers to help identify cost gaps and quantify improvement opportunities. As multichannel retailing and product extensions expand, there is an increasing importance to benchmark these other channels or retailers that may become new entrants into your segment.

As a response to structural issues in the US retail industry, US retailers have been using process benchmarking to determine areas of inefficiency or excessive cost, particularly in back office functions. This includes areas such as store operations, merchandising and supply chain as well as back office areas such as IT, Finance and HR. Robust benchmarking enables targeted tactical and transformational operational improvement opportunities to be identified.

5.3 Systematic Analysis – structured approaches to analysing cost and value

Effective cost management is achieved through strategic and structured analysis of the cost base and of the value-adding parts of the business. For companies balancing increasingly complex combinations of channels and products and services, a structured, end-to-end perspective can be instrumental in gaining a competitive edge. This raises two vital questions:

- What is the cost of providing a particular service through a particular channel?

- What levers can you pull to impact business value?

The rapid development of new products, services and channels will inevitably lead to inefficiencies. What may have seemed a great business case when it was started may have left the organisation carrying excess cost for minimal contribution. Cost to Serve (CTS) is an approach that helps to establish what matters most and emphasises that bottom-line profitability, not sales volumes or gross margin, is the measure of success. Through rigorous exploration of cost drivers and profit in a company's value chain, and with a link to the Enterprise Value Map; a framework built on the relationship between shareholder value and business operations, CTS provides a cross-functional view that pinpoints how to drive profitability, enabling retailers to make quick, smart decisions on opportunities to shift spend across customers/products, change the mix across suppliers, and where necessary, even rationalise a product portfolio. In other industries that have had to address structural cost challenges, Deloitte has found that this type of analysis done at the start of a cost reduction programme can have a dramatic impact on identifying both rapid and structural improvements.

5.4 Building continuous improvement capability – a competitive weapon

The ups and downs in the economy have, as a matter of course, led to resultant ups and downs in the retail industry, forcing retailers to adapt. To perform well throughout such turbulence retailers need to be able to exploit change to their advantage. Doing so requires a Continuous Improvement (CI) capability.

Poorly executed cost reduction can result in a loss of capability that will be felt whenever demand or the organisation returns to growth. Effective CI approaches start by focusing on what the customer values and what can either be removed without impacting the customer, or what can be done more effectively to deliver what the customer wants.

Many retailers responded to cost reduction targets by driving functions to change operational performance within areas under their immediate control. This approach may deliver improvements within the function, but they are often limited and difficult to sustain.

CI methodology taps into the knowledge and experience of staff, and helps them to deliver improvements which benefit the customer. The CI approach is powerful because it investigates processes from a quantitative customer perspective and ensures that the entire process is tuned to deliver customer value. At one client the CFO, who had recently worked through two years of drastic cost reduction, referred to this as 'putting the spirit back into the organisation and putting the customer at the heart of change'. In Deloitte's experience this type of capability is relatively new to UK retailers compared to other UK industries.

5.5 Alignment – operational capability and strategic priorities

One of the consequences of structural market change is that the retail operating model, including organisation, systems and processes needs to change if a retailer is to continue to profitably serve the changing needs of its customers. This change must be customer led and begin with a clear articulation of the vision, target customers, proposition, products and services across all channels.

Without this clarity of direction, development programmes and investments, whilst providing point solutions to immediate issues, often add to complexity and the cost to serve the customer.

The rapid growth of eCommerce and multichannel retail has acted as a catalyst for change as customers demand new services such as visibility of stock, click and collect, and same day deliveries. This is requiring retailers to rethink their whole operation from the function and location of their physical store estate, how they measure and incentivise performance and how they adapt legacy systems and supply chains to provide a cost effective, real time, flexible, multichannel fulfilment service.

In addition the rising cost of energy and raw materials is requiring retailers to revisit all aspects of the operation to identify opportunities for efficiencies by sharing services and combining spend to leverage scale for functions, channels and buying groups that have traditionally operated in silos.

The key to all of this is recognising that this is not simply more of the same and that there is a need to fundamentally change in response to these external factors.

The impact of both the changes in demand and supply in UK retailing makes the need to revisit the operating model an essential part of a retailers strategy. This is relevant to make growth initiatives more effective as well as identifying areas of structural cost that the need to be addressed from individual stores to products.

A Type I retailer will have a clear strategy linked to investments in new capabilities that allow the rapid introduction and efficient execution of new products and services across all channels. These initiatives will be business priorities, well resourced and led from the top.

Aligning the operating model to a customer led strategy is an essential part of thriving and surviving in this time of structural change.

5.6 Conclusion

Having the ability to win in the challenging market of today has been partly determined by retailers' response to the effects of the recession. Initially retailers quickly engaged in reactive cost-cutting to strip out costs. We are now at the start of a second phase and it is imperative that long-term cost-effectiveness and operational alignment strategies are implemented. Failure to do this will lead to declining productivity, a re-emergence of costs that were taken out and the failure of growth initiatives. However, where retailers challenge their own organisation to think differently, the solutions and improvements will be more innovative, longer lasting and will deliver both the scale of growth ambitions and the cost efficiency to drive profit to the bottom line.

Current readiness to do this depends upon your retailer 'Type'. Fortunately there are means of increasing readiness from one of limited choice to a position of abundant choice. The five actions outlined in this paper provide the right starting place to consider how to strengthen any retailer's strategy for winning in this turbulent market. If the first half was characterised by surprise, reaction and reprieve, then the second half can and should be underpinned by structural change and growth. There has never been a better or more pressing time to act. Are you ready?

"The next few years in retail promise to be the most challenging seen in modern times. On the demand side of the equation, disposable incomes will be hit as public sector spending cuts raise unemployment levels and increase job insecurity. Added to this will be the cost-of-living increases which will flow from areas like transport cost hikes, cuts in welfare benefits and the end of historically low interest rates. Meanwhile, the supply side has some daunting headwinds. Most of what we buy in our shops is imported, and the majority of the countries we import from have faster growing economies than ours. We will therefore be importing inflation. However, these countries are also becoming increasingly important markets for their own output, causing supply shortages: another source of inflationary pressure.

The 2011 increase in VAT from 17.5% to 20% is yet another source of pressure. Shoppers will not be able to absorb this price rise: they will simply have to purchase fewer items. With demand flat or very possibly in negative territory, and significant cost pressures from raw material price increases and production shortage, this all adds up to a squeeze on margins. This much more intensely competitive climate will penalise the weak more, but also reward the strong with increased market share."

Richard Hyman, Strategic Retail Advisor, Deloitte

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.