The five months since our last Insurance Accounting Newsletter mostly coincided with the comment period on the International Accounting Standard Board (IASB) Exposure Draft (ED) on the new International Financial Reporting Standard (IFRS) for Insurance Contracts. At the end of this period the IASB received over 250 comment letters from insurance companies, accounting and actuarial firms, insurance and security regulators and several other stakeholders around the world.

In parallel with the IASB comment period, the US Financial Accounting Standard Board (FASB) published the ED under the cover of a FASB Discussion Paper (FASB DP) which attracted an additional 74 comment letters from a similarly extensive range of US stakeholders.

The IASB and FASB (the Boards) followed the closure of the comment period with a series of roundtable meetings to talk directly to their constituents and engage them openly on the more salient comments that had been raised in the voluminous feedback received. These roundtables were held in Tokyo (9 December), London (16 December) and Norwalk, US (20 December) with a common agenda focussed on six topics which encapsulate the key issues on the road to the finalisation of the new IFRS and a potentially convergent new US accounting standard.

We use these topics to brief readers on the outcome of the roundtables and other recent associated events described below.

As they completed their roundtables, the Boards also held a joint meeting in London to discuss the insurance contract project on 15 December 2010. At this meeting the Boards approved their plan for delivering a new IFRS and a US GAAP exposure draft with an ambitious 30 June 2011 target completion date. This meeting was followed by three additional joint sessions on 18 and 19 January and 2 February 2011.

At these meetings the Boards also received reports from their Staff on the outreach activity they carried out during the four-month long comment period (15 December meeting) and on the key themes emerging from the comment letters and roundtables (18 January meeting). The Boards received on 19 January three external presentations on "top down" methods to select discount rates for non-participating insurance contracts and discussed the issue of acquisition costs at their 2 February meeting. Some key joint tentative decisions were made at the last of these meetings.

We also observed two brief FASB only meetings on 3 and 9 February when a fourth external presentation on discount rates was delivered followed by a key strategic discussion on the approach that FASB will take on this project. At their 9 February meeting the FASB voted in favour of working with the IASB to converge US GAAP with the new IFRS. This option, defined as the "overhaul or convergence" was selected over the options of "no change" and "tweaks".

Topic 1 – Volatility and discount rates

This topic dominated the debate at each roundtable and came across as the biggest issue raised in the majority of comment letters.

The issue stems from the ED requirement to reflect the time value of money in the accounting for all insurance contracts using a discount rate that is determined from market interest rates matching the characteristics of the estimated insurance cash flows. The ED explains that, unless the cash flows are affected by the value of the assets backing the insurance contracts, the discount rate is built using risk free market rates adjusted with a market consistent illiquidity premium. This approach has been referred to by the Staff as a "bottom up" approach.

The roundtables and the comment letters noted that insurers would invariably experience a volatility in their accounting results when this measurement basis is used in conjunction with that available under the recently finalised IFRS 9 pronouncement for debt instruments.

When an insurer accounts for its investments in debt instruments at amortised cost, volatility would follow from the mismatch between constant investment incomes from the cost-accounted assets against a fluctuating interest expense from the current-accounted liabilities caused by the use of current market risk free interest rates. Some observers define this instance the "cost-current volatility".

An equally volatile result would be reported if the insurer had fair valued through income its investments in bonds. Insurers' holdings in corporate bonds would expose their reported profits to the short term volatility of credit spreads without a compensating impact on the liabilities' interest expense based on risk free interest rates. This has been defined as the "current-current volatility".

Respondents to the ED and roundtable participants demanded an alignment of accounting models between assets and liabilities with a number of solutions being proposed.

One proposal recommended an alignment of the ED to IFRS 9 by introducing a locked in discount rate that would mirror the amortised cost model on the asset side. Proponents of this approach noted that the other building blocks would remain on a current basis (probability weighted cash flows estimate and the risk adjustment – for those who supported this latter approach over the composite margin model) thus mitigating any need for liability adequacy testing. The views on how the locked in discount rate should be determined varied, with suggestions including the use of a common reference rate or to use the same "bottom up" basis set out in the ED as determined on initial recognition of the insurance contract.

A second group of solutions recommended the simplification of the ED using a prescribed reference discount rate for all non participating insurance contracts. The reference to a high quality corporate bond rate currently used to discount pension liabilities was the most frequent choice of the proponents in this group. This approach would have the benefits of practical implementation and would deliver a highly consistent measure of time value of money for insurance contracts. We find interesting to note the request that Stephen Cooper, a member of IASB, put to the participants of the second London roundtable to indicate if there were any objections to a scenario where the final IFRS adopted this simplified approach to the discount rate selection. We did not record any such objections.

A third set of solutions to the issue of accounting profit volatility made reference to the use of Other Comprehensive Income (OCI) as the more appropriate location in the financial statements to display the fluctuations in market variables that cause the "currentcurrent volatility" described earlier. This "OCI solution" would require an amendment to both IFRS 9 and the new insurance contract standard because, as currently drafted, the OCI accounting for changes in assets and liabilities is prohibited in both standards, except for certain investments in equity securities. The IASB gave an indication in the roundtables that they are not considering an amendment to IFRS 9 to allow more accounting through OCI. However the overall IFRS9 model is being reassessed under the convergence discussion with FASB and we will observe in the coming weeks if this brings any change.

Another group of solutions recommended the use of a "top down" discount rate selection on the grounds it would be practical to implement and it would still be aligned to the principles of the ED. Deloitte was among these proponents (see text box). The common feature of these solutions is the removal of characteristics of asset interest rates that do not relate to the insurance cash flows being discounted.

The key characteristic that would be removed was the premium for expected credit default losses with a number of commentators suggesting others could also be removed (e.g. the premium for investment expenses). Proponents of this solution commented on the interest rate an insurer should consider for the "top down" exercise. We noted that there were two main categories of reference rates: the actual assets held by the insurer and a replicating portfolio based on the liability cash flows.

The Deloitte position on discount rate

We believe insurers should have the option to determine the discount rate for cash flows that do not vary with the value of the assets backing them using a "top down" approach starting with the rate of return on a reference asset portfolio. If an insurer chooses to use this top down approach, the amended guidance should require the insurer to determine the discount rate by removing the risk of default (based on its estimate of expected credit losses) from the rate of return on a reference asset portfolio that matches the duration and currency of the insurance contract cash flows (as the risk of default is not relevant to the insurance contract cash flows). The adjustment for expected credit losses on the assets should be consistent with the approach the Board is developing for IFRS 9.

The Boards seem to have found this group of solutions of particular interest and invited Deloitte, and two other proponents of "top down" solutions to present them in an educational session held on the 19th January 2011.

One of these "top down" solutions was the US National Association of Insurance Commissioners (NAIC) "Economic Default Adjusted Rate" (EDAR) which is currently exposed as a draft in their valuation manual for US Principle Based Reserving. This approach proposes a series of adjustments to remove expected default losses and expected investment expenses from the expected yields of the assets an insurer holds in order to derive a discount rate for insurance liabilities. Rob Esson, the NAIC presenter, explained that the EDAR proposals could be an example that the Boards may wish to consider in the development of the final IFRS.

Francesco Nagari and Andrew Smith from Deloitte LLP presented the reference asset portfolio approach. This is the "top down" approach recommended in the Deloitte comment letter summarised in the text box above. It would use the same conceptual basis adopted in the ED for replicating portfolios and apply it to the selection of the discount rate for non-participating contracts. The removal of the expected cost of defaults from the reference asset portfolio market yields would deliver a discount rate that is materially aligned with the characteristics of the liability if the reference asset portfolio has been determined to match currency and duration of the liability cash flows. This solution recommends that the reference asset portfolio is constructed using financial instruments of "good credit quality" such that insurers are allowed to consider the assets available in the markets where their insurance contracts are issued. The adjustment for the expected cost of defaults would be calculated in line with the approach being developed for the new impairment model under IFRS 9 "Financial Instruments".

The last presentation delivered by Nick Bauer, a member of Eckler Ltd a Canadian actuarial firm, illustrated an approach defined as the asset-linked discount rate that is currently found in the Canadian life insurance accounting practice. This approach is actually not determining a discount rate. Instead it considers the expected cash flows of insurance contracts and those from the assets backing them to assess the degree of matching. The asset cash flows are adjusted to remove a portion of future inflows arising from the expectation of defaults and the fact that the insurer may not be able to invest the proceeds of its assets for durations as long as those of its insurance cash flows. This produces a duration mismatch that it is also taken into account in the calculation. These adjustments all start from the expected asset cash flows thus making this technique a "top down" type. The discount rate is determined for financial reporting purposes once the cash flow estimation is complete.

FASB decided to hold a fourth and final educational session at their meeting on 3 February. William Hines and Stephen Strommen from the American Academy of Actuaries presented the findings of a 2009 paper that they had developed on the issue of discounting insurance cash flows. They added further evidence on the "top down" approaches for discounting that the other presenters gave to the Boards in January.

In particular they observed that the final accounting standard should look at the universe of risks that the risk adjustment and the discount rate cover to ensure that no duplications or omissions are incorporated in the accounting measurement. They noted that an example of an area where the "bottom up" approach set out in the ED may produce an inappropriate measure of the risk retained is when the insurer has transferred to the policyholder illiquidity risk following his purchase of an insurance contract that prevents an immediate access to its cash value. In this instance the discount rate for the insurer would capture an illiquidity premium hardly observable in markets which could be measured more effectively utilising a "top down" approach.

Topic 2 – Risk Adjustment (RA) & Residual Margin (RM) vs. Composite Margin (CM)

The comment letters were divided on this topic. The ED and the FASB DP requested a view from the respondents to help the Boards resolve their own inability to elect one of the two methods with a substantial majority vote. However, the comment letters do not seem to indicate a clear favourite between the two options.

When the boards voted last summer, the IASB supported the RA and RM model with a majority of eight against seven, the FASB had reached the opposite decision with three against two. It seems that this split across the standard setters cannot be resolved simply from a majority preference of the respondents. European, Canadian, Australian, most life insurers outside Japan and the United States and the accounting profession (see text box for the Deloitte position) were in favour of a RA model with the American, Japanese life insurers and most non-life insurers favouring a CM model.

The Deloitte position on RA+RM vs. CM

We support the ED's proposal to measure the underlying estimation uncertainty explicitly because it enables users to assess management's most current view of the different degree of volatility of outcomes from the future cash flows of insurance portfolios in force at the reporting date. We believe this approach is preferable to the composite margin because it updates the assessment of the residual uncertainty based on information obtained subsequent to initial recognition of insurance contract amounts.

The key issue here is the reliability of a model that updates the measurement of uncertainty associated with portfolios of insurance contracts and that account for it directly through profit or loss. The RA model takes the view that this can be reliably achieved and because it is a very relevant piece of financial information, it mandates its explicit measurement. The CM model takes the view that only when a transaction originating an insurance contract takes place there is sufficient evidence for accounting purposes. Using data beyond the point of initial sale of an insurance contract would be possible only if there was a liquid secondary market for insurance contracts. The CM model would then require a systematic and rational release to profit of the CM liability based on the ratio between paid benefits and premiums and their expected values.

The RA model also prescribes a systematic and rational release to profit of any positive difference arising from the comparison of the transaction price (net of incremental acquisition costs) against the present value of future contractual cash flows, increased by the RA liability.

The Deloitte position on profit recognition

Restricting the calibration of the residual margin to initial recognition makes the ED internally inconsistent because the other components of the building blocks (expected cash flows and risk adjustment) are recalculated at each reporting date. This restriction may also result in more volatility in an insurer's reported performance and it may make it more difficult for financial statement users to assess the insurer's asset and liability management for the period.

Recalibrating the residual margin against the other building blocks results in a more faithful representation of the economics of the insurer's business model compared to continued recognition of the residual margin on the basis of assumptions made at inception of the cohort.

Whilst no clear preference between these two models emerged from the comment letters, most respondents were clear in recommending a fundamental shift on how the CM and RM are released to profit. Although no single solution emerged, the objectives all stemmed from the rejection of the systematic and rational release principle or the paid vs. expected ratio approach. In particular, the independence of the profit release from the underlying changes of the building blocks is not considered to represent faithfully the underlying economics. Deloitte also was in this camp and made it clear in the comment letter that our support for an RA model was predicated on the introduction of a recalibration of the RM. We believe this would also lead to mitigation of profit volatility commented above (see text box).

Topic 3 – Unbundling and discretionary participating features

The amount of discussion on unbundling differed across the roundtables, with the American and European discussions including more extensive debate on the subject than in Asia.

The themes that we observed at the roundtables also reflect the broad flavour of the comment letters received.

A universal comment on the proposals for unbundling was that the ED had not yet clarified the operation of the requirements. A number of respondents had questioned the objectives of separating components of an insurance contract that were interdependent with the insurance coverage. In particular, we noted that a frequent proposal was to retain the voluntary regime of unbundling that the current IFRS 4 offers, rather than moving to one that imposes a requirement to unbundle.

Against this backdrop, some commentators indicated that the complexity of execution and the limited improvement in the quality of financial reporting were sufficient reasons for rejecting the unbundling regime as drafted. A regime aimed at capturing only those cases where the packaging of different components in a single contract had no commercial substance was preferred. Deloitte was among these commentators (see text box).

How to simplify unbundling

We are concerned that the unbundling requirements in the ED are too onerous and do not pass the cost-benefit analysis test: two of the three mandatory examples for unbundling would result in reporting that is substantially equivalent to the core model proposed for the host insurance contract. We do not believe that the proposed requirements would enhance the relevance and reliability of insurers' financial statements.

We believe that the Board should modify the proposed unbundling principle to require separation of components from an insurance contract only when those components (i) are not interdependent with the insurance coverage and (ii) have been combined with the insurance coverage for reasons that do not have commercial substance.

Others viewed unbundling as an opportunity to address the issue of volatility discussed earlier and supported a clearer unbundling regime that would permit the separation of deposit components from their host insurance contract and their measurement at amortised cost as financial liabilities.

Only at the European roundtables were the broader issues associated with participating contracts discussed and there was general support for the direction of the ED. However, there were also concerns with the limited guidance for estimating future participating benefits and the issue of allocating the surpluses of insurance participating funds between insurance liabilities and equity. Deloitte acknowledged the complexity of the accounting model proposed in the ED (see text box). Although we support the model, we have highlighted the issue of estimating cash flows on a fund basis inclusive of future policyholders' benefits as an innovative approach within the body of IFRS literature and thus deserving a more detailed explanation in the final IFRS.

Deloitte position on participating cash flows

We support the approach to include in the estimate the payments to current and future policyholders. This requirement implies that the participating fund is the unit of account for the cash flows that vary with asset performance rather than the portfolio of participating contracts that are in force at the reporting date. We recommend that the Board includes an explicit statement to that effect to help the application of this key principle for participating business.

Topic 4 – Short term insurance contracts and contract boundary

The discussion around the accounting for the pre-claim liability of short term insurance contracts highlighted the presence of several groups within the IFRS and US GAAP respondents who believe that there is merit in developing a new accounting standard with two measurement bases. One where the building blocks are used, and a second one which would extend the use of the modified approach approximation set out in the ED to a complete accounting model that would apply to those insurance contracts with a coverage period that is usually followed by a substantial period needed to settle the insured benefits.

Many commentators who made this recommendation at the roundtables or in their letters are from general insurance companies who underwrite property and casualty risks. They observed that the model for these contracts "is not broken" and investors appear to be satisfied that it enables investment decision making.

They welcomed the ED approach to introduce a modified approach for short term contracts and they also encouraged the Boards to consider in more detail their business model, which is focussed on optimising underwriting profit without relying on investment income. The conclusion of this argument is not to apply discounting and risk adjustment estimates on the postclaim liabilities associated with such insurance contracts.

The Boards have listened intently to this argument as it was articulated at several of the roundtables but have yet to indicate their reaction to it.

Other commentators (including Deloitte – see text box) who looked at the short term contract accounting requirements as a proxy to the main model had raised three major recommendations to improve an idea otherwise welcomed:

- Revise the calculation requirements for the pre-claim liability such that they would truly deliver a simple accounting calculation. A number of respondents highlighted the complexity of the ED requirements and noted that a simpler approach would deliver substantially similar results with significantly lower costs;

- Revise the classification of short term contracts from a rule-based "bright line" criterion (insurance coverage of twelve months or less) to one that is principle-based; and

- Do not require the use of this method for all short term contracts allowing instead that this method may be elected as an accounting policy choice.

Approximation for short term contracts pre-claims liabilities

We believe that there should be a modified accounting approach for short duration contracts' pre-claims liabilities as a practical approximation of the building blocks measurement that would allow the presentation of these contracts along the lines of the statement of comprehensive income presentation widely accepted by investors in insurers that sell these types of contracts, often referred to as general insurers or property and casualty insurers. We believe that any modified accounting approach should be permitted, but not required.

A critical point associated with the definition of a short term insurance contract is the application of the contract boundary concept.

This concept received widespread support and respondents mostly recommended refinements rather than a fundamental change of direction.

However, several insurers who operate in the health and medical expenses protection business recommended a more substantial revision that would introduce a boundary when a group of insurance contracts are repriced as a portfolio (a practice sometimes referred to as "community rating"). Insurers in this sector explained that they are often subject to regulatory requirements that prevent individual risk reassessment. The application of the current definition of contract boundary to these contracts results in a long-term insurance contract classification with the consequential inability to use the simplification granted to short term contracts.

The members of the Boards who attended the roundtables noted the significant efforts they had put in arriving at the current definition of contract boundary and they expressed hesitation at changing it to accommodate health insurers' needs without understanding the possible implications this change may have on other insurers.

Topic 5 – Presentation

The ED proposed a margin based presentation of income and expenses from insurance contracts with the option to retain lines for premiums earned income and claims incurred expense when short term contracts are in place. The majority of commentators accepted the relevance of a margin approach to profit reporting and supported the Boards in moving forward in this direction. They also commented positively on the retention of earned income and incurred expenses information for short term contracts as an option to fit within the margin based presentation.

However, the support for the margin based presentation was frequently conditional to incorporating volume information for long term contracts, without which many respondents believed the margin based approach would be less informative.

We noted that the Asian roundtable offered a particularly strong call for the use of the traditional presentation approach using written premium as the top line that would need to be included in the income statement. The recommendations also included the introduction of expense lines that would display the full amount of actual expenses considered in the calculation of the margins for experience variances and changes in assumptions.

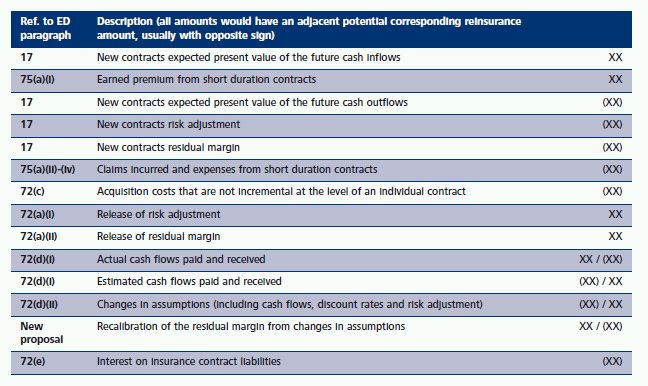

Views expressed in the other roundtables were more diverse and included other alternative approaches such as the Deloitte (see text box) proposal to utilise the present value of future contractual inflows for the contracts sold in the period (i.e. those for which the insurer had to perform the initial accounting recognition in the period). We have included in the appendix to this newsletter the amended income statement that Deloitte recommended.

Topic 6 – Transition

One area that several members of the IASB admit will change in the final IFRS is that dealing with the transition rules. The decision to state the opening balance for insurance contracts on transition without a residual margin liability will be changed to include this liability representing the unearned profits of the portfolios of contracts in force at the transition date.

In all of the roundtables the communication that this will change was welcomed and the debate focussed on the possible approaches that the Boards could consider to recognise the opening residual margin (or additional composite margin) balance.

We noted a few proposals that have been recommended:

- Allow the normal IAS 8 regime to apply to insurance contracts transition – this would require an insurer to perform a full retrospective restatement of their in-force portfolios based on the current information, calibrated against the original transaction prices less the associated release from initial recognition to the transition date. This adjustment would naturally depend on the finalisation of the discussion on how residual margin should be accounted for through income;

- Define a limited period for the IAS 8 retrospective restatement (e.g. a period between five to ten years) – this approach would aim at identifying a balance between the cost of restatement and the benefit of computing residual margins for contracts issued so far back in time that they would already have been materially earned at the date of transition. This approach would be facilitated if the mandatory implementation date is selected sufficiently in the future to allow insurers to build data for the restatement; and

- Use of a proxy value for insurance portfolios to calculate the opening residual margin – examples of these proxies include embedded value amounts the insurer may have reported on a voluntary basis, the amount that would be used in a business combination involving the portfolios in-force at transition date or the carrying amount arising from the insurer own accounting policies under the current IFRS.

Acquisition costs treatment closer to portfolio economics

The treatment of acquisition costs was not covered in the roundtable topics but was discussed at a joint meeting of the Boards held on 2 February. An important decision to change the ED was reached such that all acquisition expenses are to be included in the accounting for insurance contract on the same principle as all other contractual cash flows.

The ED originally proposed that costs to acquire, underwrite and sell an insurance contract would be included in insurance contract cash flows only if they are incremental at the individual contract level.

The Boards decided to remove this exception and to treat all acquisition cash flows on the same portfolioincremental basis used for all other cash flows. This allows additional costs such as costs of maintaining call centres and internet-based sale platforms to be included in insurance contract cash flows, which would otherwise have been required to be expensed immediately. We expect that the industry will welcome this decision as one that moves the accounting model closer to the economics of assembling and managing insurance portfolios.

New business volumes

We believe that the presentation of an insurer's performance would be more relevant if it also included information related to contracts sold in the reporting period.

One possible way to achieve this objective under the current fulfilment value model would be to present the elements of the initial calibration of the residual margin as separate lines at the top of the statement of comprehensive income. This approach would have the following benefits: (a) it would capture consistent information for contracts issued in the reporting period; (b) it would be consistent with the underlying measurement model; and (c) it would allow the calculation of common ratios that investors have developed for insurers' new business (e.g., new business margin for life insurance businesses).

The Boards agreed to continue their discussion on this topic in their future meetings to consider refining the guidance on the identification of acquisition costs and whether or not there should be guidance to limit the inclusion in the contract valuation to only those incurred for successful sales.

FASB strategic direction to converge affirmed

At their meeting on 9 February, the FASB considered whether the feedback received on the FASB DP justified an approach of preservation of the existing US GAAP for insurance contracts, one of targeted improvements to the existing body of US accounting pronouncements or a third one that aimed at achieving convergence with the IASB IFRS.

The FASB Staff recommended the third option and the vast majority of the FASB members supported it indicating in their official record of the decision that they were "affirming the objective of developing standards of accounting for insurance contracts that would improve existing U.S. GAAP and converge with International Financial Reporting Standards. The Board will pursue those objectives by deliberating the issues in this project jointly with the IASB."

We consider this important evidence of the high degree of commitment that both Boards have displayed in their determination to see this project completed with US GAAP-IFRS convergence.

Next steps and our outlook

The Boards' activity post closure of the comment period has been particularly intense with an encouraging display of firm resolve to see the project completed accompanied by genuine openness to listen to all interested parties' suggestions to produce good quality and convergent financial reporting for insurance contracts.

The completion plan to deliver the final IFRS by June 2011 and at the same time publish an ED for a new US accounting standard is ambitious.

However, there are a number of factors that in our view would contribute positively to increasing the chances of success:

- The overall US GAAP and IFRS convergence agenda has been "pruned" for success – The Boards have revised their convergence work to ensure that only certain high priority projects are delivered for the summer of 2011 when the SEC will review IFRS for adoption in the US and the IASB will undertake its decennial chairmanship rotation. These projects are: insurance contracts, financial instruments, leases and revenue from contracts with customers. All other projects will be dealt after these have been completed;

- A new FASB chairman committed to convergence who will be supported by a reconstituted insurance project team – The appointment of Leslie Seidman as the chair of FASB gives continuity to the US standard setter's commitment to the convergence agenda and it allows an immediate increase in the speed of how the FASB will engage with the IASB on the priority projects. For insurance contracts in particular the additional good news is the successful reconstitution of the FASB insurance project team. FASB saw its insurance project team reduced in the summer of 2010 but during the last few months a new team has been constituted and it appears highly engaged and able to move forward the project at the appropriate pace and, more importantly, level with the IASB project pace; and

- The IASB succession plan has been resolved with appointments that are believed to align the future of IFRS standard setting to the current agenda – The appointment of Hans Hoogervorst and Ian Mackintosh, who will take office in July 2011, together with the continuity of existing IASB members with a significant insurance knowledge and experience (Pat Finnegan and Elke König) should reduce the risk of frictional delays on the completion path, which could, at worst, lead to several years delay of the insurance project.

The Boards will tentatively resume their deliberations on 17 and 18 February 2011.

Appendix

Deloitte proposed income statement presentation

The following table illustrates the presentation described in Deloitte response letter (response to question 13), assuming an insurer elects all lines to be presented on the face of the statement of comprehensive income. The lines that could be included in the footnotes are marked with *:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.