When the UK Bribery Act comes into force in April 2011, the UK will have one of the most stringent anti-corruption regulatory regimes in the world. Companies, regardless of location or industry, need to act now to ensure their house is in order.

One of the most significant elements that the Act introduces is the 'corporate offence' which extends the reach of UK enforcement agencies beyond personal liability to enable the prosecution of commercial organisations for failing to prevent a bribe.

The only defence available to commercial organisations under the Act is to demonstrate that they have 'adequate procedures' in place to prevent bribery. The Ministry of Justice is scheduled to publish guidance on 'adequate procedures' in January 2011 after which organisations will have three months to get their house in order before the Act comes into force in April 2011. It is therefore in a company's best interests to take action now to satisfy themselves they have appropriate controls in place.

We would expect that a company with a strong control culture and robust operational and financial controls will have the basic foundations from which to develop an augmented control framework and mitigate their bribery and corruption risks. They will need to reassess their control environment through an 'anti-bribery and corruption lens' to consider whether existing controls remain fit for purpose in this enhanced regulatory and enforcement environment.

We believe there are four principles underpinning an effective anti-bribery and corruption control framework as demonstrated in Figure 1 below.

Four principles of an effective anti-bribery and control framework

- Values and controls: a strong set of checks and balances is a necessary foundation, but process controls cannot prevent collusion or detect the actions of every rogue employee so having an ethical company culture is vital.

- Organisation wide: an anti-bribery programme is not just the responsibility of the Compliance, Legal and Internal Audit functions – it is everyone's responsibility.

- Embedded: the programme must be an integral part of everyday business processes and it should not be underestimated how long this takes to achieve.

- Co-ordinated and integrated: the best programmes involve different areas of the business communicating, interacting and sharing information to enable effective control.

What should adequate procedures consist of?

Whilst organisations will require different levels of antibribery and corruption controls dependent on their scale; nature of business; operating locations; and degree of centralisation, we believe that there are a number of key steps that businesses must take for an anti-bribery and corruption framework to operate effectively.

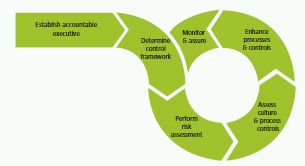

Figure 2. Adequate procedures assessment process flow

Establish accountable executive

It is vital that responsibility for implementing an antibribery programme and assessing existing controls is designated to a senior member of management with appropriate access to the Board. This will ensure that the correct level of oversight is applied and issues identified can be escalated and resolved appropriately.

Determine control framework

In order to translate those responsibilities into an effective anti-bribery and corruption programme management will need a structure against which to map these requirements.

Where possible consider using an existing control framework within your business and/or a widely recognised framework such as COSO.

Risk assessment

Before determining what level of ongoing effort is required you will need to assess the bribery and corruption risks you face and periodically refresh this assessment. Only once you have identified your risk exposure can you determine the form and scope of adequate procedures required to mitigate those risks.

Risk factors to consider may include which locations you operate in, with a red flag raised against operations in countries with a high propensity for corruption; the extent of business conducted with government and other public officials; the volume and nature of business conducted through sales agents and other third parties; and sales processes where business entertainment is a significant element of winning business. Assess and enhance controls

Following determination and prioritisation of your bribery and corruption risks, the controls you have in place to mitigate such risks will need to be documented and mapped and their operating effectiveness tested. Both specfic process and overarching organisation wide controls must be assessed and additional controls may need to be implemented.

Monitor and assure

Metrics and information to confirm anti-bribery processes and controls are operating effectively must be embedded within your programme. Thereafter you will require periodic assurance that these controls continue to be effective.

Key areas of vulnerability

Tone, ownership and awareness

It is very important that the company demonstrates that it has the right culture in place to support anti-corruption processes and controls. There are a number of elements required to embed an appropriate culture of anti-corruption in an organisation.

All areas of the business are the Board's responsibility so you need to satisfy yourself that all locations and business units in your organisation adopt the same code of conduct and anti-corruption policy.

Other control elements essential in establishing and embedding the right culture are:

- A clear anti-corruption policy and code of ethics which are visibly and consistently supported by senior management. The culture of the company must be defined, communicated and understood by all. For example, you do not want an employee to claim ignorance as a defence for unethical actions performed.

Companies will need to reassess their control environment through an 'anti bribery and corruption lens' to consider whether existing controls are fit for purpose.

- A zero tolerance disciplinary approach and a clear response plan for addressing violations of your anticorruption procedures. Staff need to know that you take breaches of company policy seriously and you need to have a defined approach to investigate and resolve breaches in a timely manner. This should include a mechanism for confidential reporting by staff of incidents of potential corruption, most typically via a hotline.

- Effective monitoring mechanisms to provide ongoing assurance of compliance. Support functions such as internal audit and compliance should be in regular communication with each other, sharing experience and demonstrating an integrated approach to compliance with anti-bribery legislation.

- Regular awareness training on your ethics and anticorruption stance to all staff at all levels of the business and other key stakeholders such as business partners.

Gifts, hospitality and corporate sponsorship

Winning new business is a key area of bribery and corruption risk where organisations should adopt early and ongoing focus to ensure adequate procedures are in operation.

It is important to ensure that you have effective controls in place covering the giving and receiving of gifts; hospitality; entertainment and expenses, including customer travel. Typical controls would include:

- A clearly defined and articulated policy with defined thresholds and limits over corporate entertainment and hospitality.

- Clear, timely and practical guidance available to support gifts and hospitality policy implementation.

- Segregation of duties for approving expense claims.

- A gift register to record all gifts received and given.

Controls should also be in place to ensure corporate sponsorship and political lobbying performed is appropriate and properly authorised.

Facilitation payments

Under the Bribery Act, these remain outlawed. Your organisation must ensure employees clearly understand the company's stance in relation to these and what to do in circumstances where requested to make them.

Third party intermediaries

Wherever you make use of sales agents, business introducers or other third parties to support your sales effort you must ensure you perform robust due diligence prior to engaging them and continue to monitor the activities they perform on your behalf throughout the term of the engagement.

Elements to incorporate within an effective due diligence process are detailed below.

Effective due diligence

Effective anti-bribery and corruption due diligence controls are likely to include:

- Clearly defined due diligence policy and process for the hiring and continuous oversight of business partners.

- Integrity due diligence on potential business partners, including background checks on publicly available records on individuals/companies.

- Standard contract terms and conditions which clearly specify the scope of work and inform the third party of your anti-corruption policy and their obligations with respect to the policy and enable you the right of termination in the event of suspicion and/or breach occurring and the right of inspection/audit.

In addition, when using agents, intermediaries and other third parties, as well as ensuring that your own controls over winning new business are being applied by the third party, further consideration should be given to ensure you have:

- A hierarchy of delegated authorities for approving agreements with third parties.

- A clearly defined policy on appropriate levels of remuneration for legitimate services.

Investments, subsidiaries, joint ventures and sub-contractors

The Act extends its jurisdiction to associated parties and the definition of these is particularly far reaching. For example, your anti-corruption assessment must extend far enough to ensure that in situations where the nature of your investment does not afford control over a subsidiary or associate, you should perform appropriate oversight to ensure your associated parties implement effective anti-bribery and corruption controls as appropriate to the circumstances.

Effective financial and accounting records and controls

A robust set of financial and accounting procedures and controls designed to ensure the maintenance of fair and accurate books and records must also be an integral part of your adequate procedures.

These need to facilitate clear and transparent recording of transactions and the checks and balances necessary to verify the accuracy of financial reporting.

How Deloitte can help

Anti-corruption specialists at Deloitte have helped some of the world's leading companies navigate the risks arising from anti-corruption legislation. Our clients seek our assistance on a broad range of corruption-related matters including:

Adequate Procedures and Anti-Bribery and Corruption Compliance Programmes

We can assist with the development, implementation and review of anti-bribery and corruption compliance programmes. This can involve supporting organisations in:

- Understanding and prioritising the risks they face.

- Establishing the control objectives and key controls necessary to enable them to determine whether the risks are controlled.

- Assessing the effectiveness of the controls in place.

- Developing enhancement plans to improve controls and facilitate control improvements.

- Training and awareness facilitation.

Forensic Data Analytics

Our Forensic Data Analytics team has a number of relevant tools and techniques which are used to assist clients in their anti-corruption efforts. These include:

- Data mining and interrogation capabilities that can highlight potentially problematic transactions quickly and efficiently.

- Online survey tools that can quickly gauge the state of awareness of staff with a company's anticorruption policy and related procedures and controls as well as highlight potential corruption risk areas.

Business Intelligence Services

Our Business Intelligence team are able to obtain information relating to the background and reputation of potential joint venture partners, sales agents or other business partners who may fall into the definition of 'associates'.

Transactional Due Diligence

Our corruption specialists have worked with both buyers and sellers to identify corruption risks as part of the due diligence process. The results of such work can influence deal price and also allow acquirers to mitigate identified corruption risks both pre and post acquisition.

Forensic Investigations

Our corruption and forensic accounting specialists have deep experience of conducting investigations and producing reports that are responsive to the needs and expectations of regulators and enforcement authorities

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.