WTW's Gareth Connolly set out his thoughts on the use of 'dynamic discount rates' in pension scheme funding and how they can be used create a more stable funding approach for the scheme's journey.

For a number of years1 trustees have been encouraged by TPR to think about their long term objectives. This concept has been fleshed out further in a subsequent White Paper2 and effectively rebranded as the "funding and investment strategy" in the Pensions Act 20213 . One such objective, as described in the 2018 White Paper is to "reach self sufficiency with low risk investment strategy and run off with minimal call on the sponsor".

With the final draft of the 2024 funding and investment strategy regulations4 now published and the resulting need for trustees to agree an objective, this article explores what we mean by a dynamic discount rate ("DDR") and the benefits that such an approach might bring, in conjunction with a run-off objective.

What do we mean by dynamic discount rate?

First, we need to be clear as to what we mean by the term DDR approach. This can be described as one where the discount rate used for funding purposes moves in sympathy with the expected return on the asset portfolio that is backing the liabilities. It is worth remembering that the DDR approach is not new. For example, many schemes such as those that are open and / or immature have used discount rates based on the expected return of the asset portfolio, with the discount rate reviewed at each valuation. Furthermore, the existing funding regulations5 explicitly include an option for the discount rate to be chosen taking into account "the yield on assets held by the scheme to fund future benefits and the anticipated future investment returns".

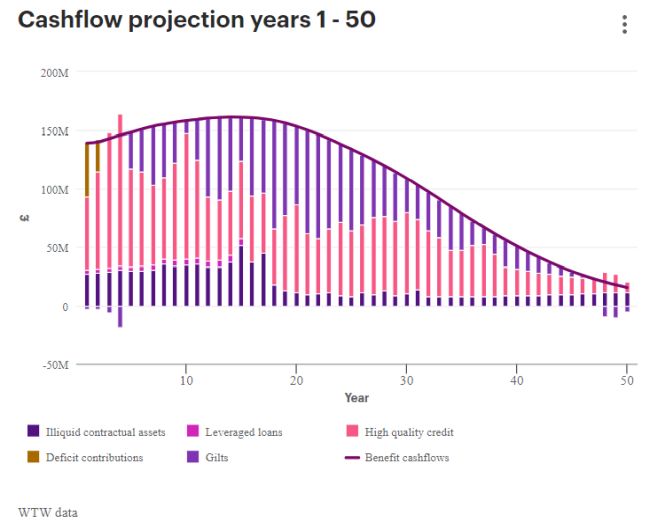

However, the primary focus of this article is the use of the DDR approach for schemes where the asset portfolio consists of investments with a high degree of contractual cash flows that are similar in nature and profile to the expected benefit outgo such as the one illustrated in the diagram below .

Why is this relevant now?

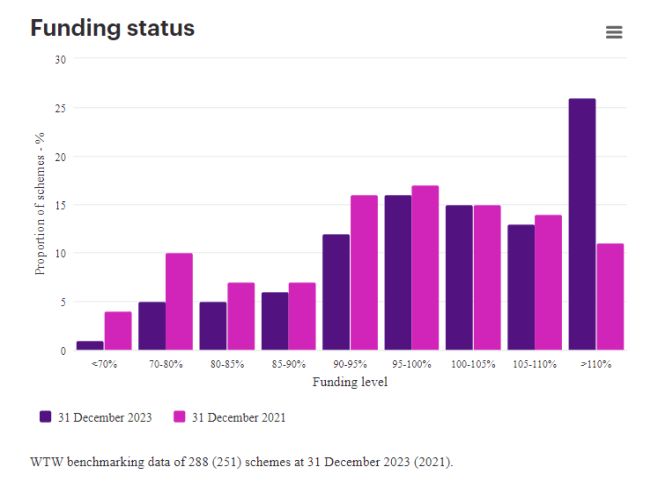

The new funding regime is being introduced against the backdrop of material improvements in funding for many schemes. The chart below, taken from the WTW Asset Liability Suite, highlights the dramatic improvement on a low-risk funding basis over the two-year period to end of 2023 for the many schemes that use this real-time monitoring tool.

As schemes approach full funding on their chosen longer term objective, it is more important for trustees and sponsors to understand the causes of variations in funding levels, and whether they are triggers for action. It is human nature to be more concerned in a funding level fluctuation of, say, 100% to 98% than a change from 82% to 80%. If some of the fluctuation is caused by the discount rate methodology, such as one which is based on gilt yields plus a fixed margin, then that could be considered to be unhelpful.

Another factor of relevance is that as schemes mature and typically look to invest more in cashflow matching assets, there is an increasing focus on the yields of those assets when determining the discount rate for funding purposes.

What are the benefits of a DDR approach?

Greater consistency of funding and investment strategies – for a scheme that invests in credit and other assets that are expected to provide regular contractual cashflows, the main drawback of a discount rate based on a gilts curve plus a fixed margin (or, say, a variable margin but one that doesn't reflect the specific assets held) is the funding level volatility that arises from credit spread fluctuations.

A DDR better captures changes in the yield on the assets held by the pension scheme and the funding level will exhibit a lower level of volatility over time which has a benefit to the trustees and scheme sponsor as it provides greater funding stability. There is still expected to be some amount of volatility that the trustees will need to monitor and manage; however, the approach benefits trustees as they will have higher quality funding information. They can therefore be more effective in their governance and monitoring by spending their time dealing with the things that matter rather than artificial volatility i.e., the "noise" caused by the model error in the discount rate.

Greater opportunities for investment strategy – if the focus is on finding assets that provide a stable funding level when the discount rate is expressed as the yield on gilts plus a fixed margin then this could lead to considering a smaller pool of potential assets. A DDR approach should make it easier for pension schemes to hold certain assets (e.g., infrastructure) which form part of the larger pool of available assets and therefore result in greater investment choice. There may also be wider societal benefits as envisaged in the Mansion House reforms.

Continuing with the investment theme, to the extent that a DDR approach would encourage a more integrated asset liability methodology to determining the discount rate, it is possible that some schemes would need to employ less leverage within the assets and perhaps focus more on cash flow matching. A consequence would be that there would be less need for leveraged LDI.

From the perspective of the sponsor, if DDR increases the likelihood of schemes adopting low-risk run-off targets then costs to the sponsor may be lower than those under a buyout strategy, but there will be a greater reliance on covenant and over a longer period as a consequence.

There are other points to bear in mind before adopting such an approach. For example, the modelling required will be more complex than that required for other funding methodologies, depending on how closely the discount rate is linked to the actual assets held by the scheme. This will require, for example, more detailed and regular flows of asset information. Furthermore, the judgements required are more explicit than in funding approaches involving fixed margins and can be difficult to make quickly in response to changing events. This can be challenging for trustees who, in most schemes, are ultimately responsible for setting the discount rate assumptions even if these need to be agreed with the sponsor.

What does TPR think?

Whilst not originally coined by TPR, the phrase "dynamic discount rate" does feature in the draft Code of Practice6 in the section on setting the low dependency discount rate, with the key message being as set out below:

Dynamic discount rate approach

Where a scheme has purchased cash flow matching assets that meet the expectations in this code, the discount rate can be based on the return of those assets adjusted to allow for a prudent level of default and downgrade informed and evidenced by historical data to give a return.

Whilst we await the final version of the Code, it is clear that the concept is acceptable to TPR.

In summary, I believe that the DDR approach could become more commonplace in conjunction with schemes adopting a low-risk run off strategy. Consequences of schemes adopting this approach could include very different investment strategies with investment in a wider pool of assets, less use of leveraged LDI and fewer schemes targeting buy-out as their long term objective.

Footnotes

1. "Annual funding statement for defined benefit pension schemes," The Pensions Regulator, May 2017.

2. "Protecting Defined Benefit Pension Schemes," Department for Work & Pensions, March 2018.

3. "Pension Schemes Act 2021," The National Archives.

4. "The Occupational Pension Schemes (Funding and Investment Strategy and Amendment) Regulations 2024," The National Archives.

5. "The Occupational Pension Schemes (Scheme Funding) Regulations 2005," The National Archives.

6. "Draft DB funding code of practice," The Pensions Regulator.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.