- with readers working within the Advertising & Public Relations industries

- within Law Practice Management and Strategy topic(s)

According to the general communiqué no: 311 which has been published by the Revenue Administration Directorate, explanations regarding taxation of salaries are as follows:

Taxation and declaration of salary income received from single or multiple employers

Taxed by stoppage;

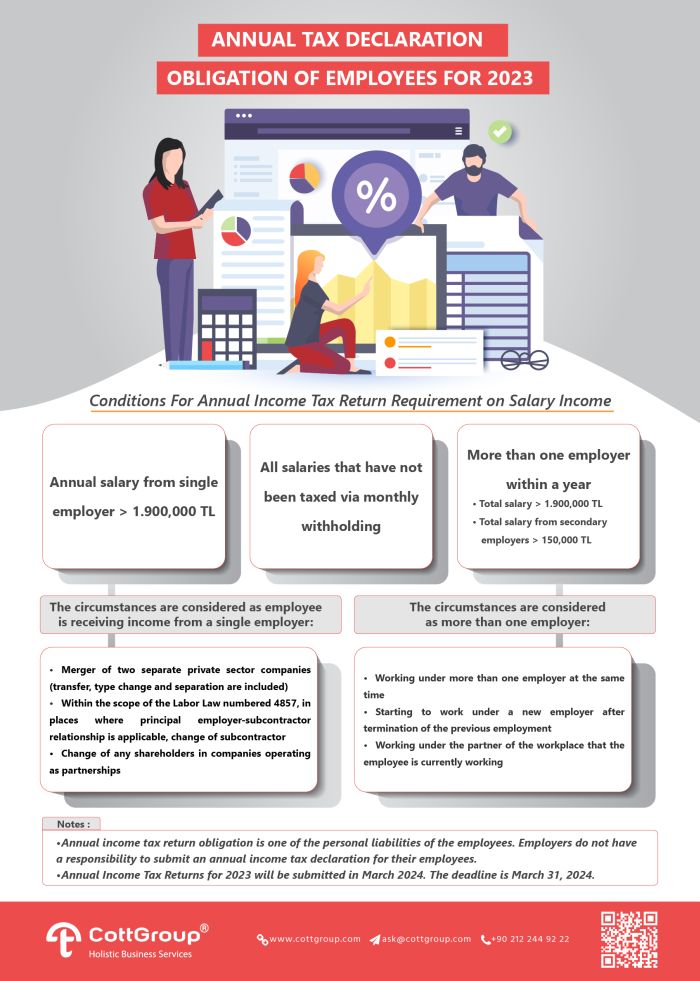

- In case of total income amount of taxpayers, who receive salary income from a single employer, exceeds the amount indicated in the fourth income bracket (1,900,000 TRY for 2023) of the tariff written in the 103rd article,

- In case of total income amount of taxpayers, who receive salary income from more than one employer, exceeds the amount indicated in the fourth income bracket (1,900,000 TRY for 2023), including the income received from primary employer,

- In case of taxpayers', who receives income from more than one employer, total income received from the secondary employers exceeds the amount in the second income segment of the income tax tariff (150,000 TRY for 2023),

salary incomes will be declared with annual declaration.

- In case of income is received from more than one employer, the employee can freely choose which income will be considered as primary.

- It will be evaluated internally whether the salary income will be declared or not, and in case of other incomes are present, they will not be included in the calculation.

- In case annual declaration is to be submitted, it is possible for expenses of education, health, donations and charities to be subject to deductions of the declared income.

- Taxes paid by stoppage can be deducted from income tax calculated over the declaration.

- Salary income which are not subject to stoppage (excluding other salaries) will be declared as per the 95th article of the same Law, regardless of their amounts.

Status of the employee who work for more than one employer in private sector workplaces

1) In below circumstances, employee is considered as receiving salary from more than one employer:

- In addition to the wage earned by an employee working alongside a private sector employer during the year, earning salary income from another private employer or public institution or organization.

- While working alongside a private sector employer, leaving job and starting to work alongside another private employer or public institution or organization within the same calendar year.

- Salary income earned by the employee working alongside income or corporate taxpayers in the same calendar year when they start working within the business partnership or ordinary partnerships which taxpayers are partners of.

2) In case of salary income is received from more than one employer, they will be taxed separately, and salary bases will not be associated with each other. In case of the employee changes employers, salary to be received from the new employer will not be associated with previous salary basis and zero basis will be based on.

3) Below circumstances are considered as employee is receiving income from a single employer:

- Merger of two separate private sector companies (transfer, type change and separation are included).

- Within the scope of the Labor Law numbered 4857, in places where principal employer-subcontractor relationship is applicable, change of subcontractor.

- Change of any shareholders in companies operating as partnerships.

4) Salaries that are considered to be received within the same calendar year will be taxed over cumulative basis.

5) Employee, who changes employers within a year, can request cumulative taxation in accordance with tariffs of income tax basis regarding salary income, by notifying the new employer. In case of a liability of declaring income as per cumulative basis of salary income, paid taxes by stoppage can be deducted by considering cumulative basis calculated over declared basis in the annual declaration.

Status of those who earn salary income within the scope of exception

Salaries paid to personnel working on ships and yachts registered in the Turkish International Ship Registry and salaries paid to R&D, design and support personnel are exempt from income tax. Within the scope of mentioned Laws, income tax deductions are not implemented on the employee salaries. Therefore, it is not possible to declare these fees within the scope of the exemption and to consider in determining whether or not to submit a declaration.

In accordance with the Law on Free Zones, income tax deducted from the employees' salaries who are working in here, R&D, design and support is left to the employer by deducting them from the tax accrued on the submitted withholding declaration.

Due to income tax deductions, it is necessary to consider whether salary payments done to the employee, who is working within this scope and fulfils the terms, shall be subject to declaration submission.

Same application is also valid for income tax exemptions in other Laws as well.

Income Tax Tariff (For only salary income)

- 15% up to 70,000 TRY

- 10,500 TRY for 70,000 TRY of 150,000 TRY, the surplus is 20%

- 26,500 TRY for 150,000 TL of 370,000 TRY, the surplus is 27%

- 85,900 TRY for 370,000 TRY of 1,900,000 TRY, the surplus is 35%

- 621,400 TRY for 1,900,000 TRY of more than 1,900,000 TRY, the surplus is 40%

rates are to be applied.

You can access Revenue Administration's Communiqué no: 311 via the link (In Turkish).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.