EXECUTIVE SUMMARY

Can the NHI make us richer and healthier?

"When analysing the potential cost of NHI, one can fall into the trap of considering healthcare expenditure only as a cost to the economy. Spending on healthcare is a long-term investment in the human capital of South Africa." Sven Byl, KPMG Head of Healthcare for Africa and South Africa.

The South African healthcare system suffers from the 'growing pains' characteristic of many emerging economies – strong economic growth, a young population and a growing and demanding middle class. It is also challenged with poor infrastructure and resource constraints. This is in contrast to the developed economies that show the signs of 'old age' – sluggish to no economic growth, rapidly ageing populations and assertive voters fighting to maintain hard-won social entitlements. Both of these sets of issues place enormous pressure on healthcare expenditure.

The recently released National Health Insurance ("NHI") government Policy Paper sets out a compelling vision to tackle the South African healthcare challenges of access to care and quality service delivery. But is the NHI affordable for South Africa?

The answer may be surprising. KPMG's Healthcare team researched whether the economic benefit of investing in healthcare outweighed the cost of increased taxes needed to fund NHI over the 14-year rollout period (2012 to 2025). We discovered that implementing the NHI could improve the health of the population, which, in turn, can increase productivity, expand the Gross Domestic Product ("GDP") and make the country more prosperous – even after taking into account the cost of funding it.

'Ka-ching' – how much and from where?

Based on the cost estimates from the policy paper, KPMG calculated that the rollout of the NHI will cost an average of R10.4 billion every year, above what is currently spent on public healthcare, amounting to a total of R145 billion in real terms over the next 14 years. Using these estimates, we set out to model different tax options to fund the NHI.

To fund the NHI wholly from:

- Personal income taxes – the average rate paid would increase 1.1 percentage points from 21.8% to 22.9%.

- Value Added Tax (VAT) – the rate would increase by 0.8 percentage points from 14% to 14.8%.

- Sin taxes (tax on those products that are the unhealthiest) – a bottle of wine would increase by R0.80, port by R1.47, a bottle of spirits (40% proof) by R12.82 and cigarettes by R4.47 for a box of 20.

While we are not arguing for increased taxes, the potential tax increases required are more accessible than first imagined.

What economic value does the NHI hold?

Beyond the cost to fund the NHI, we also turned our attention to the economic benefits of a healthier population that lives longer and can be more productive. We discovered that other countries that have implemented a form of national health insurance benefited economically from a healthier population.

Estimates show that a one year increase in a nation's 'average life expectancy' can increase GDP per capita by 4% in the long run. Having a healthier labour force can also result in increased productivity. Based on international studies, labour force productivity can increase between 20% and 47.5%.

The positive impact on South Africa would depend on the speed of implementation and the capacity of the healthcare service to remove the bottlenecks in provision and access to care.

The choice between funding the NHI through VAT or through income tax has a different impact on the economy and individuals. Both the income tax and VAT scenarios, when accounting for a modest 10% productivity increase (vs the 20% to 47.5% found in other countries), show an average improvement of 0.2 percentage points and 0.3 percentage points in GDP growth respectively. On a GDP basis this translates to an increase to 4.8% and 4.9% respectively from the baseline estimate of 4.6% between 2012 and 2020 without the introduction of the NHI.

The results of our modelling exercise imply that the introduction of the NHI could result in South African citizens getting a little richer, increasing our per capita GDP between R2 210 and R1 470 in real terms, depending on the tax scenario used.

Our analysis demonstrates that we can unlock the potential opportunity of our 'growing pains' and implement national healthcare coverage. It could be great for business and improve the country's economic situation. Moreover, it could make a significant contribution to the personal happiness of citizens for whom improved quality of life and increased longevity are within their grasp.

TECHNICAL PAPER ON FUNDING THE NHI

"When analysing the potential cost of NHI, one can fall into the trap of considering healthcare expenditure only as a cost to the economy. Spending on healthcare is a long-term investment in the human capital of South Africa." Sven Byl – KPMG Head of Healthcare for Africa and South Africa

The South African Government released its long anticipated Policy Paper on National Health Insurance1 ("Policy Paper") ("NHI") funding on the 11th of August 2011. As part of KPMG's ongoing conversation series about the NHI, we have modelled what the Policy Paper proposals could cost South Africans, depending on the funding option chosen. We have combined the outcomes of that analysis with the potential positive impact on GDP through improved productivity as a result of improved health outcomes on the back of increased health expenditure2. The question we aimed to answer was whether or not the economic benefits of investing in healthcare outweights the potential costs associated with the roll-out of NHI and the funding thereof through increased taxes.

The NHI landscape

Healthcare is one of the twelve main delivery outcome priorities identified by Government3. It is also considered to be a basic human right that is protected by the South African Constitution4. The roll-out of NHI is the Department of Health's ("DoH") flagship project and is considered the most important health policy change that Government has undertaken since 1994.

Government success would be measured against its ability to achieve the objectives of NHI5. These objectives, in summary, are:

- improving access to quality health service;

- the pooling of risks to achieve equity and social solidarity;

- the procurement of services on behalf of the entire population combined with the efficient mobilisation of financial resources;

- the strengthening of the under-resourced public sector; and

- improving the health system performance.

The potential implementation of NHI is a step closer to reducing a number of the biggest challenges6 faced by the public healthcare sector in South Africa, namely:

- the insufficient prevention and control of epidemics;

- the skewed allocation of resources between the public and private sectors; and

- the weaknesses in health systems management.

The aim of NHI is to improve the allocation of resources through the centralised distribution and spending of funds and to improve the health system's management by increased quality of care and operational efficiency. Ultimately, it is envisaged that these improvements would have knockon effects that would go a long way in reducing and/or eliminating the remaining bottlenecks and challenges within the healthcare sector.

What will NHI cost?

According to the Policy Paper, Government anticipates an additional R145 billion7 funding requirement for the roll-out of NHI over the next 14 years. These additional funds will be sourced through increased tax revenues. An additional R15 billion is needed over and above the Medium Term Expenditure Framework ("MTEF") estimated health budget8 for the implementation of NHI in the 2012/13 financial year. This represents an increase of 14% in the MTEF budget estimate9 and will bring the health budget from the original estimate of R110 billion to R125 billion10 in the 2012/13 financial year.

It is anticipated that the South African Government will increase its expenditure on public healthcare from an estimated 4.1%11 of GDP in 2012/13 to 4.8%12 in 2010 real values. The per capita expenditure on healthcare would increase by approximately R29713 from R2 174 to R2 471, which represents a 14% increase in real terms.

The NHI Policy Paper is less clear about the forecasts thereafter. However, it is estimated that the required health budget based on the resources required for the roll-out of NHI, will increase to R214 billion14 from 2013 to 2020. This represents an average annual increase of approximately 9% in real values over the period. For the period 2021 to 2025, the final period in the roll-out of the NHI, it is estimated that the public sector health budget will increase to R255 billion15. This represents an average annual increase of around 4% in real values. If considered against the average real increase in the public health expenditure of around 6.6% over the last 10 years, it assumes that the NHI is expected to require an additional 2.4 percentage points increase in real public healthcare expenditure if it is assumed that the "remainder" of the health budget continues to grow at 6.6% between 2013 and 2020 and a reduction of 2.6% thereafter as efficiencies are assumed to improve and major expenditure is completed. Over the entire roll-out period the estimate equates to an average of R10.4 billion in additional funding being required on an annual basis.

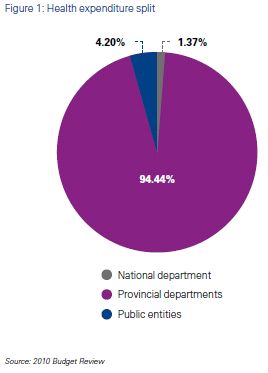

At present, health expenditure is split between the different stakeholders and spheres of government in the following way:

It is anticipated that the centralised distribution of funds and spending might change this split.

Public healthcare expenditure as a percentage of GDP has, in varying degrees, increased in most countries, even in countries with existing NHI-type systems. Examples of these countries include the United States, the United Kingdom, France, Germany, Argentina, China and Brazil16.

The real rate of growth in healthcare expenditure has also, in a number of cases, exceeded the real GDP growth rate. This has led to a scenario where a larger share of the resources has been devoted to healthcare relative to the other goods and services in the economy. South Africa is facing a similar challenge and there will be pressure on Government to deliver healthcare services more efficiently.

Possible funding options for the NHI

Governments around the world use different revenue raising tools to provide the universal coverage of medical care which the NHI seeks to provide. In South Africa, the Government expects that the NHI system will need funding over and above the current revenues that are allocated to public health expenditure. The proposed mechanisms include an increase in the VAT rate, a surcharge on individuals' taxable income and the phasing in of a payroll tax (payable by the employee)17. When considering the potential type of funding mechanisms, i.e. the tax mechanism to be used, factors such as equity, efficiency, flexibility, ease of administration and collection and potential revenue should be taken into account.

There are several examples18 of other economies that have similar funding mechanisms. These include:

- The Russian Federation, which has a compulsory public healthcare system funded by a 3.6% payroll tax;

- Italy, which has a National Health Service system funded by general tax;

- Albania, which has public health insurance system that is funded by the State Budget and a payroll tax that is ring-fenced for health; and

- France, which has a combination of public and private healthcare system of which the public portion is compulsory with optional supplementary top-up packages. It is funded by a social security tax on revenue and an employer tax.

These examples and others might have formed part of the reason that there has been initial indications from Government that income tax and VAT might be the preferred funding sources for NHI.

In our analysis, we have considered an increase in the above mentioned types of taxes, as well as the possibility of using 'sin taxes' as an alternative funding mechanism. Many people believe that increasing the tax on cigarettes and alcohol could and would discourage harmful behaviour19 and, in turn, improve the health of the population. From that perspective, it makes sense to use sin taxes as a potential source of funding for public health policy initiatives. In addition, sin taxes also serve as a source of revenue and are considered by some analysts to have less distortionary effects than other types of taxes20. On the downside, research has indicated that sin taxes might be regressive in nature and if the consumption of taxed products actually reduces on the back of the introduction of sin taxes, it might have a negative impact on the estimated revenue21.

If the additional average R10.4 billion per annum required for the roll-out of NHI is to be funded from additional tax revenue over the period of 2012 to 2025, the following are the estimated once-off increases in the tax rates for the taxes under consideration:

- Revenue collected from personal income tax would need to increase by an estimated 5%22. This would imply that tax assessed as a percentage of taxable income would increase from 21.8% to 22.9%23

- Revenue collected from VAT would need to increase by an estimated 6%. This would imply that the current 14% VAT rate would have to increase to 14.8%.

- Revenue collected from sin taxes would need to increase by an estimated 46% in order to collect an extra R10.4 billion rand. Particular items such as cigarettes would increase by R4.47 for a box of 20. Unfortified wine would increase by R0.80 and fortified wine by R1.47 for a 750 ml bottle. A bottle of spirits with an average of 40% pure alcohol would increase by R12.8224.

SOME EXAMPLES OF THE BENEFITS OF INCREASED HEALTH EXPENDITURE COMBINED WITH IMPROVED HEALTH OUTCOMES

Healthcare expenditure in an economy has been estimated to create a 5% Keynesian macroeconomic multiplier effect25, i.e. each R1 extra spent on healthcare creates R0.05 extra economic activity in the long run. For example, if this were to hold true for South Africa, the estimated additional R13 billion to be spent during 2012, could potentially create an additional R650 million in economic activity nationally, in 2010 prices. Some of the potential positive impacts could stem from the economic benefits of increased life expectancy and increased labour productivity, amongst others.

Increase in life expectancy

Middle income countries who have implemented a form of national health insurance have benefited economically from a healthier population. Estimates indicate that increasing a nation's life expectancy by 1 year could potentially increase the GDP per capita by 4%26 in the long run27.

For example, in South Africa the average life expectancy is currently estimated to be 52 years28. If the same holds true for South Africa, increasing the life expectancy from the current 52 to 69 years, the global average, would increase the GDP per capita for South Africans by approximately R2 100 in the long run29.

Increase in labour productivity

The health of a country's labour force can impact on its productivity levels. If NHI is successful in its aim to reduce bottlenecks in the provision of public healthcare in South Africa, it could lead to an improvement in the health of the labour force in the long term. In turn, it could lead to an increase in productivity30. International studies have estimated the increase in labour productivity to be between 20% and 47.5% in the medium to long run31.

Other benefits we have not specifically modelled, but which might be partially "explained" by the increase in productivity, are increases in labour participation rates and reduced absenteeism. Furthermore, households might also benefit from increased independence.

Combining the costs and benefits: Will we be better off in the end?

Studies on the impact of healthcare, including those quoted in the Policy Paper, are often focused either on the cost side of the impact of an increased tax burden on citizens or the potential benefits of increased productivity to the economy.

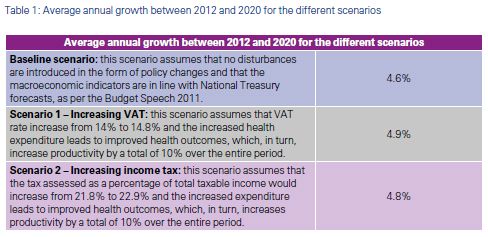

We modelled 2 different scenarios to examine the potential net effect of an increase in VAT for the first scenario and an increase in income tax for the second scenario, combined with an assumed 10% increase in productivity as a result of improved health outcomes. Due to the bottlenecks in the system, we assumed that the 10% productivity increase will only come into effect from 2018 onwards. The outcomes of these scenarios are compared with a baseline scenario where NHI is not implemented.

The baseline scenario shows an estimated average annual GDP growth rate of 4.6% between 2012 and 2020. Should a policy change in the form of an increase in the VAT rate be introduced to fund NHI, combined with an increase in productivity, the average annual GDP growth rate over the same period is estimated to be 4.9%. A policy change in the form of an increase in the personal income tax rate, combined with an increase in productivity, reveals an estimated increase in the average annual GDP growth rate to 4.8% over the same period.

When comparing the effect of a change in the VAT rate to a change in the personal income tax rate, it is important to bear in mind that these two approaches are revenue neutral: the policy change introduced in the model was done in such a way that the same amount of revenue will be generated by both forms of tax increases. However, increasing VAT appears to be less distortive than increasing personal income tax, although by a relatively small margin. This implies that the negative economic impacts created by increasing VAT, are marginally less than the negative economic impacts created by increasing personal income taxes.

The reason for this difference could be as a result of the impact that an increase in personal income taxes has on the take-home pay of workers and, hence, their consumption expenditure.

The results imply that if South Africa is successful in improving the health of the labour force through the implementation of NHI and this leads to productivity gains of only 10% between 2012 and 2020, half of the improvement in productivity seen in other countries, the economic benefits could outweigh the economic costs of implementing NHI.

Conclusion

The difference between the GDP growth rate under the baseline scenario and the GDP growth rate under the VAT scenario, is equal to 6.5%, while the difference between the baseline and income tax scenario is equal to 4.3%, the latter being similar to findings of the international study previously mentioned. If this were to be translated to GDP per capita32 expressing the values in 2010 terms, the improvement in GDP per capita under the VAT scenario is equal to approximately R2 210 over the period 2012 to 2020. For the income tax scenario the improvement in GDP per capita is equal to approximately R1 470 over the period 2012 to 2020.

To read this article in full, please click here.

Footnotes

1 Department of Health, National Health Insurance in South Africa, Policy Paper

2 We assume that the increased health expenditure would lead to improved health outcomes, which in turn will improve productivity.

3 The Outcomes Approach, The South African Government

4 Constitution of the Republic of South Africa (1996)

5 Department of Health, National Health Insurance Policy Paper

6 An Overview of Health and Healthcare in South Africa 1994 – 2010, David Harrison, December 2009

7 All values based on 2010 real values

8 Policy Paper

9 Medium Term Expenditure Framework

10 2010 real terms

11 Health Systems Trust – www.hst.org.za

12 KPMG Calculation

13 KPMG Calculation, Population estimates StatsSA Midyear Population Estimates 2011

14 Policy Paper, in 2010 real values

15 Policy Paper, in 2010 real values

16 IMF Finance and Development Article – Healing Healthcare Finances by B. Clements, D. Coady, B. Shang and J. Tyson, March 2011, Vol. 48, No.1

17 South African Revenue Service, Tax Proposals, Budget 2011

18 Healthcare in Europe, Best practises and an overview – KPMG 2008

19 Consumption taxes in a life-cycle framework: Are sin taxes regressive, A.B. Lyon, R.M Schwab, (August 1995)

20 Promoting Smokers Welfare with Responsible Taxation, W. Kip Viscusi

21 Distortionary Tax and Labour Supply; E. Cardia, N.Kozhaya, F.J Ruge-Murcia

22 In 2010 real values based on 2010 revenue collections as contained in the 2010 Budget Review, Annexure B: Statistical Tables

23 Based on the 2009 Tax Statistics published by the South African Revenue Service

24 These estimations are based on the assumption that the increase in sin taxes are spread equally over the different types of products that are taxed

25 Dr. Bianca Frogner, Presentation to the round table on NHI: exploring key questions, Oxfam Australia, May 2010

26 Policy Paper

27 The effect of Health on Economic Growth: A Production Function Approach, D. Bloom, D. Canning and J.Sevilla, World Development, 2003 – no clarity was provided as to how long the long run is.

28 World Bank Country Data 2009

29 2010 real values

30 Dr. Chris Malikane – Presentation to the round table on NHI: exploring key questions, Oxfam Australia, May 2010

31 For more detail on these findings, see Appendix C.

32 StatsSA Midyear population estimates and 2010 GDP values.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.