Policy uncertainty and internal structural challenges plague South Africa's growth potential.

With the strike season still underway in certain industries, South Africa got a sense of its impact on the economy thus far on Thursday, 10 October 2013. Manufacturing output grew by a mere 0.2% in August 2013 from a year before, compared to the annual growth rate of 5.5% observed in July 2013, clearly reflecting lost production due to strike action across industries. On a more positive note, mining production increased by 2.1% year-on-year in August 2013 on the back of platinum group metals, from the annual increase of 1.2% observed in July 2013.1 According to Andrew Levy Employment Publications, the number of working days lost rose from 750 000 in the first half of last year to 1.8 million in the first half of this year.2

Annual wage negotiations have gone hand in hand with strike action and this year the strike action has not continued for as long or been as violent as was the case last year. However, relative to 2010, where the strike season lasted fewer than three months, this year's strike season has lasted more than ten months of the year with the economic sectors being affected increasing greatly.3 Both existing and potential investors across all sectors of the South African economy are taking note as the extent and tone of these demands from labour unions have become more threatening, with little response from government.

The Association of Mineworkers and Construction Union (Amcu) initially rejected Anglo American platinum's (Amplats) planned retrenchment of 3 158 employees and called to broaden the strike if their demands to reinstate these workers are not met. The two parties have since come to an agreement; however, the strike that started at the end of last month is estimated to have cost R605.6 million in lost production of platinum alone.4

In the automotive sector, a four-week strike cost this industry around R20 billion while slashing exports and export earnings by 75% or 50 000 cars.5 In the wake of this, BMW spokesperson Guy Kilfoil said the company lost 13,000 units of unrecoverable production and as a result of the current environment will be putting expansion plans into South Africa on hold indefinitely. In response to this statement, general secretary Irvin Jim from the National Union of Metalworkers of SA (Numsa) said that they would seek a formal meeting with the leadership of BMW to discuss this perceived threat.6

The recent labour market events have also been noted by the World Bank. In its bi-annual report on Africa released early last week, it has stated that labour unrest and mining strikes, burdensome regulations, and infrastructure gaps have held back the country's growth.7 The extent of labour market rigidities is evident when looking at selected labour market indicators from the World Economic Forum's Global Competitiveness Report for 2013-2014.

Out of 148 surveyed countries, comprising 99% of world GDP, South Africa was ranked as follows:

- Cooperation in labour-employer relations – 148th

- Flexibility of wage determination – 144th

- Hiring and firing practices – 147th

- Pay and productivity – 142nd

- (Overall) Labour market efficiency – 116th

This report also conducts a survey in which respondents are asked to identify the five most problematic factors for doing business from a list, which in South Africa's case were indicated to be:

- Inadequately educated workforce

- Restrictive labour relations

- Inefficient government bureaucracy

- Corruption

- Poor work ethic in national labour force

Government's conflicting and uncertain policy statements are further straining investment confidence into the local economy and inevitably hampering the country's Gross Domestic Output (GDP) growth and job creating ability. An example is the Min¬eral and Petroleum Resources Development Amendment Bill which is currently going through the parliamentary process. This amendment bill has come under severe scrutiny from industry stakeholders due to the lack of certainty and stability provided by the legislation. One of the concerns with the amendment bill is that explorers would not necessarily have the automatic right to mine deposits which they discover. There is also a push for mining companies to expand into benefication – something the industry is not geared to do.8

Similar concern has been heard from the retail sector, with Woolworths chairman Si¬mon Susman stating that they are watching with deep concern the flow of restrictive, populist legislation being imposed on commerce in South Africa.9 Various local economists and analysts have also echoed these sentiments.

In his address at the Broad-Based Black Economic Empowerment Summit on 3 October, President Jacob Zuma stated, among other things, that the government encouraged the growth of more SMMEs owned by black people, women, youth and persons with disability in the six New Growth Path job drivers, being mining, agriculture, the green economy, tourism, manufacturing and infrastructure development. He also indicated that intervention by way of targeted financial support and localised state procurement has seen the revitalisation of industries such as train and bus building as well as clothing, textiles and footwear manufacturing.10

While this is true, foreign direct investment cannot be ignored and is crucial to ensure economic sustainability and prosperity, especially for a developing economy such as South Africa requiring capital investment for the promotion of infrastructure expansions and job creation. The U.S bond buying programme has provided investors with additional liquidity to invest in more risky, emerging market areas such as South African government bonds. However, these portfolio flows could just as easily be redirected elsewhere when the global economic environment changes to the detriment of South Africa. It is therefore up to policy makers to table clear and concise, investor friendly legislation which guarantees efficient production levels thereby ensuring the attractiveness of foreign long term investment in South Africa.

South African trade deficit widens

South Africa's deficit on its current account11 widened unexpectedly to a 7 month high of R19.05 billion in August after the shortfall of R13.4 billion recorded in July this year. The July figure represented 6.5% of gross domestic product (GDP) in the second quarter of 2013, up from a deficit of 5.8% of GDP observed in the first quarter. The globally acceptable level over the long term for a manageable deficit is agreed to be 3% of GDP. Like last month, the latest figure, released on 30 September was far worse than market expectations, with analysts' consensus expectation before the announcement being around the R12 billion level.12

Exporters could not benefit fully from the lower export prices achieved from the recent devaluation of the rand due to the strike action and associated loss in output especially seen in the mining and manufacturing sectors. The weak currency has also lead to inflated rand prices of necessary imports such as crude oil, minerals and base metals, further affecting the size of the trade deficit.13 Globally, low demand growth from the Eurozone and China also continued to have an impact on the depressed trade figures.

With strike actions that should come to a close during the third quarter of this year, export volumes and therefore export earnings have the potential to increase on the back of the weakened rand that could help to reduce the current size of the trade deficit.

October is Global Month of Action on Energy, but are we on the right track?

With energy prices on the rise in South Africa and elsewhere, October has been deemed the Global Month of Action on Energy14 , where organizations involved in generating energy and electricity are urged to consider environmental concerns and policymakers are urged to consider more renewable sources of energy. While increases in the costs of crude oil are blamed for production constraints, insufficient power supply and consequent rising production costs, coupled with increases in labour instability, have been cited as deterrents to investment, constraining economic growth in South Africa even more than the globally-influenced commodity prices, exchange rates, and export demand15.

Without adequate access to power, investment by large multinationals is limited. This places a huge burden on domestic companies to carry growth, something they may not be able to do on their own. Without finishing Eskom's coal-fired Medupi power station, South Africa is expected to grow at 3% Y-o-Y by 2015, when almost all economies, even in the Euro zone, are expected to recover to pre-financial crisis levels. Power constraints thus become a tipping point in investment terms, even more so that labour market unrest. Infrastructure challenges, access to electricity and water, and logistics costs are also contributing factors. In general, labour market issues stop new investments, but these other factors constrain existing investments or expansions with much more regularity. This is evidenced by the fact that while labour issues put a recent controversial damper on BMWs plans for a new car model production run in SA, electricity constraints were cited as the reason for a delay in the building of an aluminium plant in Coega. According to the UN Conference on Trade and Development (Unctad) 2011/12 report, foreign direct investment flows into South Africa decreased by 24 percent to $4.6 billion in 2012 from $6bn in 2011, with enormous volatility.

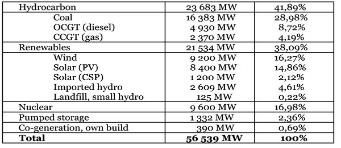

For these reasons, along with concerns around climate change, South Africa is moving towards a policy position to increase the use of renewable energy resources such as solar and wind power. Whether South Africa expects to be a leader or a follower in the renewables space is still up for debate, but progress is being made on plans for a 5GW solar park (the largest in the world). Currently, South Africa is planning a combined total of 56,359MW of new generation capacity over the next 20 years, with a mix of traditional and renewable-based energy generation. This mix is shown below:

Table 1: New-build energy mix over 20 years to

203016

This energy mix shows a greater commitment to renewable energy sources. But given that these are new technologies, many unproven at commercial scale, and only some of which able to absorb baseload responsibility, it might make sense to consider options for plugging the investment gap by providing quick access to additional power. Since coal is still a favoured technology in South Africa with which we have a comparative advantage in energy generation, it might make sense to continue to build coal-fired power plants, at least in the short-term, to overcome economic woes. South Africa still shows a preference for coal-fired power. This can be seen by considering the new-build technology mix of the Integrated Resource Plan, and subtracting generation components that are to be decommissioned by 2030:

Figure 1: Energy technology mix to 2030

This shows that while an ambitious renewable and nuclear build lies ahead, coal is still here to stay. This may be the logical choice. Environmentalists need to weigh in the negative externality cost of low investment in-country when considering energy generation options.

Footnotes

1 http://beta2.statssa.gov.za/

2 The Star, Business Report - Experts lash out at policy muddle

3 Mr. Loane Sharp, economist at Adcorp.

5 http://www.bdlive.co.za/business/2013/10/07/government-to-talk-to-car-makers-says-gordhan

6 http://www.bdlive.co.za/business/2013/10/07/blackmail-storm-over-bmw-as-strike-ends

9 The Star, Business Report - Experts lash out at policy muddle

10 http://www.thepresidency.gov.za/pebble.asp?relid=16192

11 The current account is the difference between a nation's savings and its investment and an important indicator of an economy's health. It is defined as the sum of the balance of trade (goods and services exports less imports), net income from abroad and net current transfers.

12 http://www.bdlive.co.za/economy/2013/10/01/trade-deficit-shock-raises-alarm-over-sas-exports

14 http://allafrica.com/stories/201310070435.html

15 http://www.iol.co.za/business/companies/bmw-may-set-trend-with-expansion-halt-1.1589153

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.