Regulation

The turmoil in the markets caused by the Eurozone debt crisis is the latest manifestation of the banking crisis that almost brought the global economy to its knees in 2008. Unlike then, however, it's now the interconnection between government debt and the banking sector making the markets nervous. Breaking this link is key.

Since the crisis the focus has been on strengthening regulation of the banking sector. Banking Union is the key policy priority at present, but high capital, more liquidity and de-risking the derivatives market remain key policy targets. On October 26, 2011, the European Banking Authority (EBA) announced that a number of key banks across Europe needed to increase the size of their capital base and therefore had to raise in excess of EUR110 billion by June 2012. To achieve this, the EBA believed banks would take a number of actions including the issuing of new equity, the retention of earnings (rather than paying them out as dividends), the reduction of staff costs (thereby boosting Core Tier 1 capital) and the conversion of hybrid capital instruments into Core Tier 1 equity.

The banks were required to submit their plans, via their national authorities, to the EBA in January 2012. On July 11, 2012, the EBA reported back announcing that the majority of the banks meet the required ratio of 9 percent Core Tier 1 (CT1). For the few banks not able to meet the capital level using private sources, backstop measures are being agreed with national governments. The higher requirements were met mainly via measures directly impacting capital – retained earnings, new equity, and liability management. The EBA also reported that the exercise did not lead to reduced lending – deleveraging measures led to an overall reduction of risk weighted assets (RWAs) by only 0.62 percent.

What was clear from the exercise is that – on the equity/liability side of the balance sheet – little new capital has been raised. Indeed, profits are (at best) volatile and the debate about bail-outs has resulted in banks keeping their options open when it comes to transforming hybrid capital into Core Tier 1 equity. That being said, there are strong indications that significant action has been taken on the asset side of the balance sheet, with de-leveraging being observed.

But it is widely known that this was not the EBA's policy intention. In fact, according to the EBA, the declared objective of these measures was to avoid an aggressive and potentially disorganised deleveraging process focused exclusively on the assets side. The potentially serious implications of the restriction in new credit was widely recognized and the authorities were clearly not looking for this response from the banks.

So while they likely accepted that some assets would be sold as banks returned to their business models, they probably wanted (and expected) lower quality, high risk assets to be sold as a way of reducing balance sheet risk and mitigating the danger of future profit volatility. But, in reality, most of the sales have been of good quality, performing assets. Why did the banks have this response, and what are the wider implications? In our view, there were actually a number of factors at work here; some complimentary and some conflicting.

The political dynamic

Politicians find themselves in a difficult bind. On the one hand, there is palpable nervousness about domestic economies and growth (or the lack of it) across the European Union. But it is also clear that the overhang of government debt will likely lead to the continuation of austerity measures across Europe.

There is clear tension here between the need for economic stimulation (which governments cannot afford to fund) and new credit coming available for the wider economy, versus the disinclination to contemplate another bail out of the banks and another round of regulatory policy which is effectively driving more risk averse business models. Indeed, governments are sending out a very risk averse message, and following this up with policy interventions that are seeking to both manage the "too big to fail risk" while also pushing for the flow of credit to continue.

But this leads to a very serious debate about whether the lack of new credit is actually supply-led or demand-driven. The banks argue that demand for credit is weak, and that large corporations are instead tapping the bond markets directly. They also (somewhat justifiably) point out that the regulatory burdens now placed on them are restricting their ability to lend profitably, particularly given the wider change in the credit risk profile of the economy. Of course, it must be noted that some of the stronger corporates (and some households) are paying down debt in the normal course of business and this is also depressing the net lending numbers.

Politicians, however, take an alternate view. They believe that the banks are not willing to take their share of the responsibility and that, to do so, they need to lend and help manage the slowing levels of economic activity.

The shortage of capital on the supply side, when combined with the pressure for new lending, will likely mean that some of the lower yielding but high risk-weighted assets may need to be sold (such as mortgages that have high loan-to-value (LTV) ratios but no discernible signs of distress).

But the practicality of selling impaired assets is also becoming more and more complex, largely because those buyers that are prepared to take the risk are also calling for larger 'haircuts' on the valuation. In turn, this creates an impasse with banks unwilling to take an accounting loss on loans that are still performing, albeit with signs of future distress.

The liquidity environment

Ever since the announcement of the Basel III accords, it has been clear that liquidity would be critical to new regulatory arrangements. Many had been hoping that the delay in announcing some of the details of the arrangement (and, keep in mind, that we are still waiting for the longer-term Net Stable Funding Ratio) meant that the stance taken on the Liquidity Coverage Ratio (the short term one) would be relaxed. But this has not proven to be the case.

It has also become clear that the willingness of retail depositors to lock up their deposits for longer terms has also not materialized, either because short-dated rates remain attractive or due to on-going nervousness about deposit protection. At the same time, the corporate market has also proven to be a non-starter, largely because of an unwillingness to lock up funds for any period of time.

As a result, there has been increased demand for High Quality Liquid Assets (HQLAs) which, in practice, can only be funded by selling other assets, namely loans. Indeed, it is now easier to sell lower-risk assets quickly without taking a haircut (which would impact overall Core Tier 1 capital), than enter into long negotiations on the poorer quality assets.

2011 also saw the onset of significant shortages of US dollar funding and, as a result, significant books of good quality, dollar denominated assets have been sold simply because the dollar funding costs have made this business unprofitable. In large part, these have involved US banks rather than hedge funds or other private equity type players.

But since these loans are generally well performing, they have been sold either at, or above, book value due largely to the fact that it is easier for US banks to source in this form rather than going out and originating new credit. This has led to the release of some capital capacity which could be used to lend in the domestic currency (subject to the other liquidity requirements to hold HQLAs).

Capital management

The capital management position is also far from straightforward, with many banks holding long-dated loans that were originated at narrow margins in the competitive pre-crisis world. But with the change in both capital and funding costs, these loans are no longer profitable.

The reality is that solvent borrowers are not likely to refinance by choice, while those that would consider refinancing are largely unable to find alternative finance due to the value of their collateral (notably domestic property). Given Basel III, one might assume that it would be reasonably easy to determine the amount of capital required by using a formulaic table, but this overlooks the vagaries of the various models now in use, and thus makes a significant difference to the risk weighted asset (RWA) value and, therefore, the profitability of the loan. As a result, lower margin loans with higher risk weighting are more likely to be sold than others.

Non-performing loans (NPLs) are somewhat trickier. For instance, even though credit is normally priced to include (on a portfolio basis) a certain level of future impairment, the actual valuation of such portfolios on a 'for sale' basis becomes much more difficult once the default rate starts to diverge from the norm. So, while future losses (whether they are booked now or in some future accounting period) will likely be a straight Core Tier 1 write off, the buyers of such books will need to have a higher risk appetite and therefore will expect higher rewards. In turn, this will drive down prices which will also impact Tier 1.

Collateral management

Collateral management is an issue that is often overlooked when assessing capital and liquidity drivers in preparation for the sale of assets from the balance sheet. True, the European Central Bank (ECB) has provided significant medium-term liquidity with large tranches injected in December 2011 and February 2012. But this lending must be supported by good quality collateral which necessitates the removal of more good quality assets from the mix. At the same time, some banks have issued new covered bonds aimed at raising longer-term liquidity from the market, but these are also secured with higher quality assets.

The impact of this has been to remove significant blocks of assets that would otherwise have typically been sold to meet the EBA requirements. And while the impact of the ECB intervention on stability was both pronounced and welcome, the downside is that it has also caused an even larger proportion of quality assets to essentially be taken out of the system.

What does this tell us?

Logic would dictate that if a board had taken the decision to deleverage and derisk, we would have seen significant books of lower quality assets being sold on the market. Clearly, this has not happened.

In part, this is because potential buyers of these assets are looking for significant returns which would force the banks to take large haircuts that they are unwilling to accept. But facing the need to maintain capital levels (namely by avoiding significant haircuts), meet liquidity requirements (by achieving a quick sale of good quality assets without discounts); and tie up their assets as central bank collateral, we are therefore left in the current situation where managers are selling assets that they should intuitively be keeping, rather than the higher risk, higher capital absorbing and higher margin loans (those that still carry a long-term impairment risk) that remain on their books.

This has led to a growing debate as to whether Basel III is really the right policy framework and, indeed, whether it will have a significant impact on the economy over the long-term. We believe that the level of debt – both in the wider economy and between the banks – was too high historically, and therefore experience would show that any policy response would have met a difficult transition period. Basel III is not perfect, but there are few – if any – viable alternatives being discussed.

That being said, Basel III has no hope of working in isolation and, therefore, more effort must be placed into developing the role of macro prudential tools in order to help manage the wider direction of the economy and reduce the gross risks now haunting the banking system.

Giles Williams

Financial Services Regulatory Centre of Excellence and Partner,

KPMG in the UK

Shipping Loans

Stormy waters for the shipping industry

With the global economic downturn reducing trade levels across the board, shipping companies are facing increasingly challenging circumstances. And with excess capacity on order with shipyards, the existing imbalance between supply and demand has been further exacerbated by increasing downward pressure on both time-charter and spot rates, as well as operating margins.

As a result of the excess order book, the global fleet is expected to break previous records in 2012, with 7 percent growth overall. Dry bulk will see the highest capacity increases at 12 percent, containers will experience a 7 percent rise, and tankers, a more modest 4 percent increase. Most of this growth is being built in yards in China, Korea and Japan. It seems likely that shipbuilding sectors in those territories are also exposed.

"The prolonged depression in charter and freight rates experienced between 2008 and 2012 has eaten away the available facilities and cash reserves built up by owners and operators during the extended shipping boom that ended in 2008. This means that it is not just loan-to-value (LTV) covenants giving their lenders a headache, but also debt service and the prospect of impending refinancing within a sector that many wish to decrease their exposure to."

John Luke

Global Head of Shipping and Partner, KPMG in the UK

Price trends and overcapacity

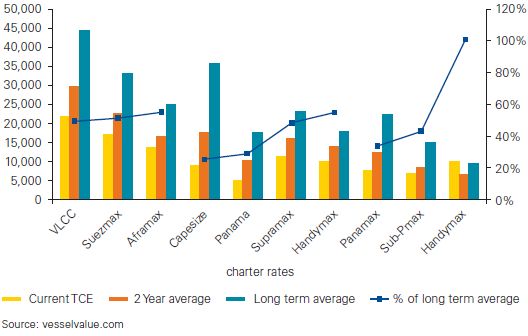

Current versus long term charter rates

Facing a prolonged period with charter rates hovering dangerously close (and in some cases below) to break even, a growing number of vessel owners and operators are now experiencing severe financial difficulties. Moreover, margins have been further eroded by sharp increases in 'bunker' (fuel oil) prices which has put severe pressure on those unable to pass these costs on to the shippers.

Indeed, in the six months ending March 2012, the Clarksea index (an index for shipping rates) fell by 35 percent to below USD10,000 per day. As illustrated in the graph on the left, the Bulk Carrier market experienced the most significant reduction in rates which collapsed from USD30,000 per day in December 2011 to somewhere between USD3,500 and USD7,000 per day by January 2012. Compounding these challenges are increasing costs for bunker and the cost of regulation which is further squeezing margins across the industry.

Liquidity is also under significant pressure as the impacts of the credit crisis take their toll on the traditional source of maritime debt: the Eurozone and Scandinavian banks. And with most of these sources now undergoing serious deleveraging, many are explicitly seeking to exit their shipping loan portfolios which, in turn, has placed further pressure on owners and operators seeking to refinance their pre-crash newbuild funding or fund final payments on new ships about to hit the water.

These pervasive issues, combined with a perceived lack of quality and transparency in corporate reporting, have created a number of issues for banks when dealing with, and restructuring, shipping connections in their portfolios.

Value decline with age by vessel type

Options available for owners, charterers and operators

The reality is that – in the current economic climate – shipping businesses have limited turn-around options at their disposal. In certain circumstances, cost reduction can be a viable option, but given the current depressed rates, any amount of cost reduction will still likely leave shipping businesses with insufficient funds to service overheads and finance costs.

Similarly, the 'hot or cold' 'lay up' of underutilized vessels is often ineffective, with the costs of idling vessels or taking vessels 'out of class' (thereby incurring various crew costs, port charges and insurance fees) remaining high. Labor costs also tend to remain fixed in the short-term. These costs differ from the airline industry where aircraft can often be kept in 'dry storage' in the desert at low cost.

What is more, the option of simply scrapping the worst performing assets is generally uneconomical and often unacceptable to the lenders who hold security over these assets, making this option unfeasible without the cooperation of the ship owner.

Facing limited options for turn-around, many lenders and borrowers have fallen into an 'extend and pretend' strategy believing there is no alternative than to ride through the cycle. But with most observers suggesting the current down-draft may last 3 to 5 years, this approach is unlikely to be sustainable.

Restructuring challenges

In our experience, the quality and timeliness of management information being presented to lenders is often very poor. As a result, neither the lender nor the borrower has sufficient forward visibility into either the potential cash flow issues or the company's operational and financial drivers and performance. This often means that when a shipping connection becomes distressed, it is difficult to properly assess how to even begin operational and financial restructuring.

Consensual negotiations are also frequently hampered by difficulties in ascertaining the current physical condition – and, hence, the real value – of each of the vessels within the connection; a task made even more complex in cases where the connection's most valuable security is still under construction in an Asian yard. Many vessel owners also hold a dogged belief that an upturn in the market is 'just around the corner', which is dampening their appetite for meaningful negotiations.

Recently, a disturbing strategy has gained greater adoption by vessel owners under pressure from banks: applying to the US courts for Chapter 11 bankruptcy protection. This generally demands a fairly low threshold for proving jurisdiction. (For example, it can be triggered by the holding of a US bank account or the fact that vessels periodically dock in US ports). In the past couple of years, this strategy has been taken by a number of companies including Omega Navigation, Marco Polo Seatrade and General Maritime Corp.

With US Chapter 11 often being seen as a more debtor-friendly process than many of the insolvency regimes in Europe, it can be a strong draw for those vessel owners who see limited short-term options and believe that a prolonged period of protection from creditors may enable them to continue operations through the downturn. At worst, some believe the delay caused by Chapter 11 represents a route to a better consensual negotiation.

However, once Chapter 11 protection is invoked, debtors often find that the legal and professional fees associated with the process run into the millions of dollars. Moreover, it can also result in Debtor-In-Possession (DIP) funding requirements. In order to protect their position, these DIP funds are often provided by the lenders (as new money on top of the already impaired debt) which effectively ranks ahead of any security already held by the lenders. There is also the risk that DIP funding may be provided by a party related to the borrower. And while the debtor may enjoy the benefit of keeping control of the vessels, depreciating asset values often diminish the value of the lenders' security.

Since maritime law (particularly the complexity surrounding the risk of vessel arrest in differing jurisdictions) traditionally requires specialist maritime lawyers, it is often this group that are driving the restructuring negotiations between banks and their borrowers. That being said, we have seen banks and borrowers increasingly bring insolvency and financial restructuring experts into the discussions at a much earlier stage.

"In 2012, we have been spending a lot of time with the work out units of our banking clients to help them identify early warning signals for their shipping portfolios and to develop solutions for the shipping loans that need to be restructured."

Justin Zatouroff

Partner, Restructuring Practice, KPMG in the UK

Solutions available to lenders

Operational restructuring – Operational restructuring can be a useful tool during a consensual restructuring process. Indeed, appropriate commercial and technical ship management should be put in place, particularly in cases where negotiations are protracted, to allow costs and revenues to be optimized in the new circumstances. While this may not necessarily achieve profitability, it will – at the very least – create a stable platform upon which consensual negotiations can be held. But in many cases, we have found that vessels continue to be traded uneconomically and receive poor maintenance by the distressed borrower even while negotiations are ongoing. In other words, competency should not be assumed during negotiations. Lloyd's List recently reported that Hong Kong's Wallem and other fleet management businesses are significantly increasing their business with vessels repossessed by banks.

Debt for equity swaps

While common in standard restructuring processes, debt for equity swaps will not always appeal to lenders as they tend to lead to significant public relations issues regarding the ownership of shipping assets which lenders are often unwilling to risk. That being said, debt for equity swaps may be a necessary step towards a fleet restructuring or consolidation. Moreover, it should not be assumed that the existing owners hold all of the operational knowledge required to continue trading.

Refinancing/equity cures

Given the specialist nature of ship finance, it is often difficult for alternative debt to be found, particularly given the current economic conditions and the fact that a number of lenders now classify their shipping portfolios as non-core.

Equity cures are equally difficult as vessel ownership structures are often thinly capitalized and therefore owners are generally unwilling to commit further funds when the market starts to deteriorate.

Amend and extend

In the current economic climate, the potential for turnaround strategies based on market recovery is extremely low. Even in better times, the amend and extend strategy is seen as a last resort by lenders. With the growing realization that the market may not improve for the foreseeable future and the number of payment defaults continuously growing, this option is becoming even less feasible.

Lenders considering this strategy should note that, with the risks associated with depreciating and potentially stranded assets mounting, any waivers given by lenders should have the right terms attached (such as change of ship managers or change of charter methods) in order to provide as much leverage as possible in case consensual negotiations break down.

Secondary debt market

Since ship finance is largely a specialist field, the number of institutions involved (and therefore the liquidity of the debt in the secondary market) is limited. What is more, given the present outlook for the shipping industry and the prices being achieved at auction, values are likely to reflect the distressed nature of the industry.

Asset disposal or security enforcement

In some cases, the disposal of individual vessels – or even the entire fleet – can be agreed with the vessel owner in order to pay down debt. However, in practice this can be difficult to achieve even with the cooperation of the vessel owner and is likely to only result in distressed prices in the current market.

But if the cooperation of the vessel owner is not forthcoming, lenders may find that the only viable option is to enforce their security and either auction or sell the vessels to a third party. However, given the complexities of maritime law and logistics this course of action must be meticulously planned both in advance of, and during, consensual negotiations. The reality is that the potential consequences of an unplanned enforcement process can be costly for lenders, particularly if the borrower simply fails to deliver the ship assets to the lenders or seeks Chapter 11 protection in US bankruptcy courts (as discussed earlier in this article).

Other solutions

With all this in mind, there are a few interim solutions available to lenders when faced with a shipping group in need of restructuring. These can be implemented as a first step in reaching an amicable restructuring solution and may give the bank more transparency over the borrower's financial situation, the fleet quality and the quality of the operator.

For example, in cases where the restructuring discussions have deteriorated between the bank and the borrower, we have seen the emergence of new solutions such as the warehousing of particular shipping assets while a buyer is found. We have also seen lenders support the continued trading of the vessels by a third party ship operator reporting to the bank, which can continue until such a time as a solution can be found which maximizes value for the lenders.

Conclusion

Overall, we have noted that the number of distressed connections in shipping portfolios is increasing and, in many circumstances, lenders lack proper forewarning or planning. With the 'amend and extend' strategy proving increasingly unsustainable – due largely to unsustainable operating cash positions and the widely-held belief that the market may not turn in the near-term – more proactive management of portfolios will be required. Given the complex nature of the shipping industry in general and shipping finance in particular, lenders must have as much information and leverage as possible at the early stages of negotiations.

The reality is that shipping negotiations are starkly different from those in real estate where once a consensual negotiation breaks down, the enforcement process is relatively clean and clear cut. In shipping, faltering negotiations may lead the vessel owners or operators to take pre-emptive action to seek protection or cause disruption, which can be both time consuming and expensive for the lenders.

We therefore believe that it is vital that lenders dealing with distressed loans in their shipping portfolio start to build as much control as possible throughout the negotiation process and stand ready with a Plan B that can be quickly executed if a consensual agreement is not achievable.

That being said, debt for equity swaps may be a necessary step towards a fleet restructuring or consolidation. Moreover, it should not be assumed that the existing owners hold all of the operational knowledge required to continue trading.

UK consumer debt purchase market

Larger deals are closing, volumes and prices are reaching historic highs but are we heading for a crash?

The UK consumer debt purchase market has been particularly active recently. Indeed, over the last 12 months, we have seen more transaction volume and landmark market developments within the UK than we saw over the last 3 years combined. It is a sign of these very busy times when there is frequent talk of a first initial public offering of a UK debt purchaser within the coming years.

Sales volumes are increasing to a new peak

In 2011, the UK debt purchase industry returned to its pre-credit crunch peak with the value of investments rising to well over GBP800 million and 2012 continued this rising trend.

Facing an environment of improving collections, last year saw sellers bring more portfolios to market which, in turn, has led to firm pricing and a virtuous cycle of more and more assets coming to market. In KPMG International's 2012, Global Debt Sales Survey, the majority of respondents suggested that we will see a strong uptick in disposals by lenders in 2013 as banks continue to offload debt in their warehouses. That being said, many took the view that these sales would likely peak in the last quarter of 2012 or the first quarter of 2013, and then drop by between 10 to 20 percent once warehouses are cleared.

However, there are also clear indications that individual sales are becoming larger. At the same time, there seems to be a clear shift in the UK market away from regular 'business as usual' debt sales run by the specialist debt sales teams, to instead focus on much larger 'balance sheet driven' sales, the decisions for which are made by the C-Suite executives of the banks. As a result, we anticipate a number of sales of GBP500 million to GBP1 billion (and up) in face value from some of the major lenders within the coming months.

This is further supported by a handful of well funded buyers who seem eager to invest greater amounts of money into acquiring either performing or semi-performing loans portfolios, which will clearly require much larger check sizes. Recent examples of this trend include the sale of Egg's GBP650 million performing loan book to the syndicate of Paragon, Carval and Arrow Global, and several large sales from MBNA, both in excess of GBP1 billion in face value.

Pricing is also increasing, driven by a very high level of demand

While one might see this as a virtual Eutopia for well-funded debt purchasers, the reality is that leading consumer debt sellers are reporting ever-increasing pricing for charged-off consumer debt, which is widely considered to be driven by demand exceeding (an albeit increasing) supply. One leading seller noted that three debt purchasers had independently suggested that the market may actually be heading for a pricing crash for consumer Non-Performing Loans (NPLs) as, in their view, the market is showing signs of overheating. The seller went onto suggest that, once the collection performance metrics for recently acquired consumer NPL portfolios start to feed through into the debt purchasers' financials, we will likely see a market correction.

It should be noted, however, that this increased level of demand is predominantly being driven by six to ten well-capitalized debt purchasers who are looking to grow their portfolio size through acquisition. These include Cabot Credit Management, Arrow Global, Link Financial, CapQuest, 1st Credit, Marlin, Lowell Group and Max Recovery, to name but a few.

At the same time, at least three of these purchasers are rumored to be coming to the end of their Private Equity ownership cycles are therefore most likely to be up for sale in the coming years which, again, is fuelling competition for portfolios and driving up pricing. However, at the time of writing, RBS Special Opportunities Fund had postponed the sale process of debt buyer Arrow Global, after bids failed to meet its valuation of the business. It was rumored that the bidder interest was predominantly from other UK and overseas strategic players, denoting a shift from the historic private equity interest towards potentially greater consolidation in the sector.

A number of large overseas funds are also looking to gain a foothold in the sector by acquiring a large anchor portfolio either alone or by partnering with a UK servicer. Most of these players are looking to spend between GBP100 million and GBP300 million in 2012, often in larger chunks rather than smaller 'Business As Usual' sales. That being said, transactions of GBP50 million to GBP100 million seem to be continuing unabated. New entrants into the market include PRA's acquisition of MacKenzie Hall's platform for a reported GBP33.5 million, Cyrus Capital's acquisition of Sigma Financial and Apollo's entry into the market through a partnership with 1st Credit.

Asset diversification is becoming key for better financial performance

As the market for traditional consumer NPLs becomes more crowded and prices increase, some of the more shrewd purchasers are looking to exploit new niches (in terms of asset classes) or new geographies. As previously noted, a number of purchasers are now looking to acquire debt earlier in the collection cycle (as performing or semi performing loans), which not only commands higher pricing and greater transaction values, but also decreases competition from those players that are unable to write significant checks. This represents a market shift from the pre-financial crisis days when almost all debt was sold at a low value having been through several collection cycles. The trend is further supported by some of the large non-core business disposals in the market, such as those from MBNA.

Additionally, even the UK government is now sufficiently comfortable with the standing of a number of the purchasers and their focus on treating customers fairly, that they are considering extending beyond the outsourcing of collections and actually considering running a number of more extensive pilot sale and 'right to collect' schemes.

Most of these players are looking to spend between GBP100 million and GBP300 million in 2012, often in larger chunks rather than smaller 'Business As Usual' sales. That being said, transactions of GBP50 million to GBP100 million seem to be continuing unabated.

With larger transaction sizes, deal structuring mechanisms are becoming more common

As portfolio sizes grow, and investment sizes increase, market participants will need to carefully consider their approach to deal structuring, which can have a significant positive impact on pricing, even in relatively short-term duration situations.

Indeed, structured deals can take a number of different forms from forward flows and Joint Venture/upside arrangements with assets transferred into Special Purpose Vehicles, through to price deferrals and post deal price adjustment agreements. Yet despite the variety of different forms now in use, what each of these structures have in common is that they can be mutually beneficial for both the seller and the purchaser which, in turn, can drive returns.

However, despite an obvious keenness on the part of more advanced purchasers to explore these deal structures with sellers, many of the debt sales teams within the banks still seem to prefer to 'keep deals simple' by focusing on speed and ease of execution and, as a result, there is likely value being left on the table for both parties.

Both parties may learn some valuable lessons from other loan portfolio asset class sales (such as RBS's CRE loan portfolio sale to Blackstone), which could be transposed to the UK consumer debt purchase market.

New and creative funding structures are being deployed

Perhaps one of the most significant recent market developments is Lowell Group's March 2012 placement of a GBP200 million high-yield bond, with a 2019 maturity and an annual interest coupon of 10.75 percent. With the proceeds earmarked for refinancing existing debt, this access to new types of money indicates that new ground is being broken in the industry. This has been more recently followed by Cabot Credit Management's issuance of a similar, albeit larger, bond.

This provides a number of potential benefits for bond originators. For one, access to public money opens up a new source of funding which, to date, has been limited to the decreasing handful of senior debt providers lending to the sector (one notable new entrant being DNB Nord). But the bond issuance also better prepares Lowell and Cabot (and other debt purchasers who may follow suit) for their private equity exit through an initial public offering or sale to a new breed of buyers such as pension funds or insurers who have longer-term investment horizons.

To assist this, debt purchasers should consider matching the Estimated Remaining Cashflow (ERC) of acquired portfolios to their funding profile in order to ensure that they are able to service their debt. The simple truth is that short-tailed collections curves are not best suited to long-term funding, as they tend to lead to increased pressure to continue acquiring portfolios, at the expense of squeezed margins.

Indeed, structured deals can take a number of different forms from forward flows and Joint Venture/upside arrangements with assets transferred into Special Purpose Vehicles, through to price deferrals and post deal price adjustment agreements.

"The UK debt purchase market is going through a period of dramatic change. On the one hand, we see a potential overheating of the consumer NPL market driven by buyers seeking refuge in less saturated markets. But on the other hand, new sources of funding are potentially opening up. Given that funding has always been a key driver in the success or failure of the sector, it will be interesting to see how this impacts the industry over the next 12 months."

Jonathan Hunt

Associate Director, Portfolio Solutions Group, KPMG in the UK

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.