Investing in property is a profitable and dependable venture but rising interest rates and an unpredictable global economy are making investors apprehensive. There are lessons to be learned from the '07–'08 crisis, especially from those who are still profitable. What many first-time investors don't know, is that yields are the key to their success.

Key

points

|

Residential property prices grow faster than commercial

You are probably already aware that buy-to-let (BTL) residential property has "low" yields, but that's no reason to write it off. In fact, prices grow faster on this type of property, contrary to, say, industrial/warehousing, retail and office real estate.

German property: a textbook example

| Property type | Annual yields, % | Price growth Q1–Q3 2015, % |

| BTL residential | 3.0–5.0 | 5.0 |

| Commercial | 4.0–7.0 | 1.5–2.0 |

Take Germany for example, which is a very attractive market for domestic and foreign investments at the moment. Yields on residential BTL are 3.0–5.0% per annum on average, compared to 4.0–7.0% on retail, industrial and office property.

-> Germany needs 50% more homes to house migrants

However, residential apartment prices gained 5.0% in 9 months (Q1–Q3 2015) according to the Association of German Mortgage Banks (Verband deutscher Pfandbriefbanken), while commercial property only grew by 1.5–2.0%.

Choosing commercial property: shops, offices or industrial?

Even within the different commercial property segments, low yields triumph in terms of price growth. Take global retail property figures, average yields on high street retail premises are just 4.7%, yet prices gained 7.2% per annum since 2009. In comparison, office prices grew 6.3% on average per year over the same period with 5.0% yields, and industrial/warehousing prices saw 5.3% price growth for 6.8% yields.

Low-yield property prices grow faster

This yield-to-price rule even holds true for competing property within segments too. Over the last decade in Germany's 60 main cities, high-yield property consistently underperformed in terms of price dynamics within the retail property segment.

-> Commercial property investments soar in Germany's "Big Seven" cities

The attractive 8% gross yield property only gained 2.1% on average per year, while retail premises with a common 5.0% yield actually gained 5.5% in value every year over the last decade. Food for thought, right?

Low-yield property in good locations is crisis-resistant

Have you noticed that the more popular the location, the lower the yields? That's because yields and price dynamics are interdependent for properties of the same type in different locations: real estate in popular markets has lower returns, yet prices grow faster.

| Investing in commercial property requires a counterintuitive profit strategy, particularly one that is crisis-resistant. Low yields are the key to this strategy, because they are the product of high demand and rising prices. |

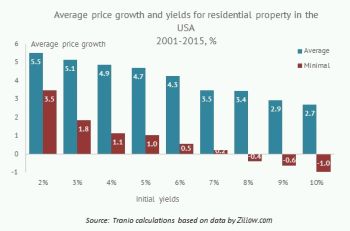

Low-risk and low-yield locations (generally, prime and downtown districts in large cities) get more expensive faster than their higher-risk and higher-yield peers. This is true of most big property markets, including the US according to our Tranio research based on data from Zillow, America's top property portal.

When they compared rental rates and price dynamics for real estate in over 5,000 city districts in the USA over the last fifteen years, it also confirmed the yield-to-price relationship.

Between 2001 and 2015, average prices grew 5.5% per annum on residential property with 2.0% yields and just 2.7% on real estate with 10.0% yields. This means that low-yielding real estate lost the least value despite the 2007 crisis. Even in the worst-case scenarios, residential property with 2.0% yields gained at least 3.5% in value, while prices of property earning 8.0% yields lost up to 0.4 % per annum and even –1.0% per annum where yields were 10.0%.

So if the market goes bad, low-yield property will lose less value and the price will rebound faster than a high-risk, high-yield investment.

Price growth makes up for smaller yields

Yields and price growth tend to balance themselves out too, so being a conservative investor doesn't induce any potential losses in earnings. If we compare residential and commercial real estate in 100 different locations across Germany, price growth makes up for reduced yield income everywhere (and these are conservative estimates).

According to Tranio research (see below), if net yields are 3%, prices grow 5%, and if the yields are 7%, price gain is 1% per annum. Either way, the cumulative returns on both options are roughly 8%, but the low yield property is less risky.

The problem with high risk is simple: it's harder to rent when the market is bad. The consequences during crises are two-fold: you could lose your revenue if your property is empty and it could lose value too.

Exceptions and conditions to the yield-to-price rule

There are some exceptions and conditions that apply. Over the short-term (1–2 years), price dynamics and yields can be affected by a number of issues like changing laws, rising interest rates or the phase of the property cycle.

-> Property cycles: how to choose the best moment to buy property

For example, the UK recently increased the Stamp Duty (tax on property purchases) and price growth on prime properties in Central London is to slow down. It could even be flat in 2016 according to Savills, a global real estate sales and lettings agent, while prime property elsewhere is set to gain 2%.

There are also some geographical exceptions. Midtown markets often have higher yields than central neighbourhoods and peripheral areas can demonstrate strong price growth in specific cases, like gentrification or urban renewal projects.

-> Europe's top five urban renovation projects

Remember that size matters: a supermarket in a small town could be a low-risk investment (it's unlikely to attract bigger competition) bringing in steady, low yields. However, the property value will not rise as quickly as in the city because there is less demand for real estate.

My advice to you

Look for a happy medium when it comes to your investment because nothing is guaranteed in life, but sensible decision-making is free. Remember, a low-yield property is not always a guarantee of price growth, nor is a high yield necessarily the most likely to lose value. From my experience in 2015, 5–6% yield (net rental income/property value) is a good target with a loan at 2% interest.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.