Spain:

Community Of Madrid Fiscal Measures For 2018

18 June 2018

Andersen Tax & Legal

To print this article, all you need is to be registered or login on Mondaq.com.

On 29 May 2018, the Governing Council of the Community of Madrid

approved the draft law on tax measures for the Community of Madrid

for 2018

The draft contains important measures relating to Personal

Income Tax, Inheritance and Gift Tax, and Transfer Tax and Stamp

Duty, which are summarized below:

1. Personal income tax:

|

Deduction for birth (entered into force

1/1/2018)

|

- 600€ per year, for 3 years, for children born or adopted

from 1/1/2018 onwards. Taxpayer's income limit: 30,000€ in

individual taxation or 36,200€ together, not exceeding

60.000€ per family unit.

|

|

Deduction for housing rental (effective

1/1/2018)

|

- People under 30 years of age may apply a 30% deduction on

amounts used to rent their home, subject to a limit of €1,000.

Also, those who are not older than 40 years, provided they have

been unemployed for more than 6 months and have two dependents. The

income received may not exceed 25,620€ in individual taxation

and 36,200€ in total, and without exceeding the family unit of

60,000€.

|

|

Decrease in the regional scale of personal income tax

(entry into force 31/12/2018)

|

- Reduction of the minimum rate to 9%, applicable to the taxable

base not exceeding €12,450.

|

|

Deduction for foster care (effective

31/12/2018)

|

- Deduction of 1,500€ for the care of people over 65 who are

not related or disabled. Must be living together more than half of

the year (more than 183 days) without compensation, and the

disability must be greater than or equal to 33%. The taxpayer's

income may not exceed €25,620 in individual taxation and

€36,200 jointly, with no limit on the family unit

|

|

Deduction for school fees (entry into force

31/12/2018)

|

- 15% deduction for descendants from 0 to 3 years old, with a

maximum deduction limit per descendant of €1,000 per year. The

taxpayer's tax base may not exceed the amount of €30,000

multiplied by the number of members of the family unit.

|

|

Contribution deduction for a carer of descendants under

3 years of age (effective 31/12/2018)

|

- Deduction of 20% of the cost of social security contributions

per carer hired for descendants up to 3 years of age, with a

maximum of €400 per year per family.

- Large families: 30% deduction with a maximum of 500 euros per

year. Requirements: (i) at least one of the descendants cannot be

enrolled in a publicly supported nursery school (public place or

childcare check beneficiary), (ii) the head of the household must

have been registered as an employer and have had one or more

caregivers hired and contributing for at least 40 hours per month,

and (iii) the parent or parents must have worked each of them for

at least 183 days during the year in which the deduction applies.

Income limit of 30,000 euros per capita.

|

|

Deduction for contributions to the share capital of the

social economy (effective 31/12/2018)

|

- 50% deduction, with a maximum of €12,000 per year, for

contributions to the share capital of cooperatives and worker-owned

companies.

|

|

Deduction for donations to Foundations (effective

31/12/2018)

|

- Deduction of 15% of the amounts donated to foundations

registered in the Registry of Foundations of the Community of

Madrid. The basis of the deduction may not exceed 10% of the

taxable amount

|

|

Deduction for investment in the acquisition of shares

and holdings (effective 31/12/2018)

|

- Deduction of 30% of the investment in shares and equity in

newly created companies, but not exceeding €6,000 per year. In

the case of entities in which universities or research centres have

a stake, the deduction may be up to 50%, but may not exceed

€12,000 per year.

|

2. Inheritance and gift tax (Effective 1/1/2019)

- A new bonus is established for both inter vivos and mortis

causa acquisitions for transfers between 2nd and 3rd degree

consanguineous collateral (siblings, uncles and nephews) of 15% and

10% respectively.

- Limit of application: When the taxable person himself requests

or applies it when submitting his self-assessment or return.

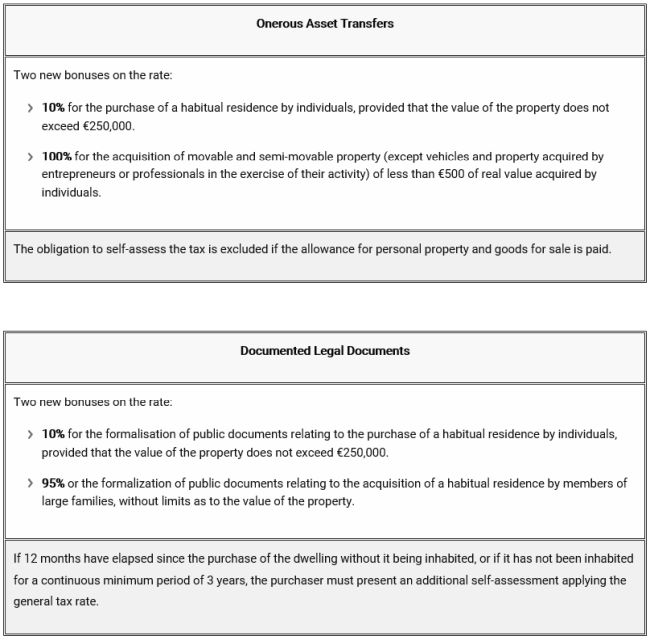

3. Transfer tax and stamp duty (Entry into force 1/1/2019)

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

POPULAR ARTICLES ON: Tax from Spain

Tax – A Shake-Up Looms

Herbert Smith Freehills

Few developments in the tax world have an impact on a truly global scale, but the so-called 'Pillar Two' rules – essentially a global minimum corporate tax – is one of them.

Tax Saving Tips For Your Cyprus Company

McMillan Woods

Cyprus has an extensive network of double tax treaties with various countries, which can help in reducing or eliminating double taxation. Take advantage of these treaties to minimize your tax liabilities.

Tax Facts 2024

Highworth

Highworth (Cyprus) Ltd, a trusted leader in financial services, proudly presents the Tax Facts of 2024.

Tax Relief On Debt For Companies

Lubbock Fine

When financing your business operations through borrowing, one of the main considerations will be whether the interest cost is deductible, and to what extent if it is. In the UK...