Assisted by Ms. Pallavi Payal Verma, Associate.

Introduction

In order to better understand the legal commotion surrounding crypto-currency, it is important to review the factors that have led to its development and growth in the recent past. At the root of most path breaking innovations in the world of finance is the fundamental rule of economics, that is, the rule of demand and supply. This rule is the driving force behind the transformation of money in any economy. So also in the case of crypto-currencies.

Over the last decade or two, the world economy has seen a gradual shift towards a paperless currency. In today's fast paced economy, money is required not only to be easily transferable, widely acceptable, in adequate supply and circulation, but also to instil confidence in users.

One of the key risks associated with the conventional fiat currency is that its value is interlinked with the actions and stability of a country's government.1 Since the circulation of fiat currency is exclusively in the hands of governments, they have been printing currency at a lightning pace resulting in the devaluation of the currency resulting in a state of hyperinflation and ultimate collapse of the economy.2 A glaring example of such an economic catastrophe is the sharp devaluation in the monetary value of the Zimbabwe dollar to almost zero within a span of one year during 2008 to 2009.3 This has led to the quest for a medium of exchange or currency whose supply is not controlled by any governmental institution and is independent. This has been a catalyst in the conceptualisation of crypto-currencies.

Another important contributing factor is the issue faced in the case of electronic payments, namely, the duplicity of a transaction, or, in other words, the simultaneous re-credit or re-debit of the same fund. This issue is latent in electronic payments because each electronic payment is approved or validated by a financial institution acting as a trusted third party, responsible for authenticating and recording the flow of money in a transaction.4

Presently, across the globe, crypto-currencies such as Bitcoins, Ripple, Litecoin and Auroracoin are being purchased and sold over dedicated electronic platforms called crypto-currency exchanges. These crypto-currency exchanges provide an interface to their users to purchase or sell crypto-currency from willing sellers and buyers from across the globe.5 Some of the crypto-currency exchanges also allow the interchanging of one crypto-currency for another.6

This paper analyses the issues that surround the establishment of a new crypto-currency exchange by any entity in India. The discussion is restricted to only one type of crypto-currency i.e. Bitcoins. In the first section, we discuss the technology that is at the core of Bitcoins, followed by the nature of a Bitcoin in the light of the existing legal regime, the possible legal issues that may be faced by crypto-currency exchanges in India and in the last section we discuss possible solutions to these issues.

The technology behind crypto-currency

The backbone of crypto-currencies is a path breaking technology known as 'blockchain' technology.7 This technology was first conceptualised in a white paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System" published under the alias of Satoshi Nakamato in the year 2008.8 The blockchain technology, simply put, is a computer programme that maintains an electronic ledger of transactions.9 The need for this technology stems from the lacuna that exists in the conventional ledger keeping system in relation to monetary transactions, especially electronic payments. In a conventional setup, the banks and financial institutions keep, update and authenticate the record of these transactions.10 These records are the final proof of existence or non-existence of a particular transaction. There is no means of cross verifying these records for authenticity or certainty, thereby leaving a large scope for their manipulation and likelihood of fraud. This is mainly because the knowledge about a particular transaction is not available in real time to all the interested participants.

The blockchain technology addresses this lacuna by decentralising the ledger, that is, it makes available the copy of all the records of a particular transaction to each and every participant in a concerned network. Further, if there is a new transaction, the ledger records for the same will be updated in real time for all the participants, thereby making it difficult to manipulate the transaction record. Another feature of this technology is that the record of each transaction made since its inception, in relation to underlying crypto-currencies, forms a consecutive block in a stack of information known as the ledger. This makes it difficult to manipulate the records as the entire ledger and each copy of it on all the devices in the network would have to be altered. This technology is elementary to the functioning of crypto-currency, which gives it a novelty that is commercially coveted.

It may be noted that there are no legal issues with respect to the blockchain technology per se, rather, it is the legality of the crypto-currency that uses this technology which is under scrutiny. Further, the entire transaction in relation to any crypto-currency takes place only in the virtual space without any intervention whatsoever from any governmental or regulatory authority of a country.

Bitcoins

One of the types of crypto-currencies available in the market is Bitcoins, which uses the blockchain technology at its core. Bitcoins are based on a system of decentralised peer-to-peer online currency that maintains a value, without any backing from a governmental or regulatory authority, sans any intrinsic value or backing of any central issuer.11

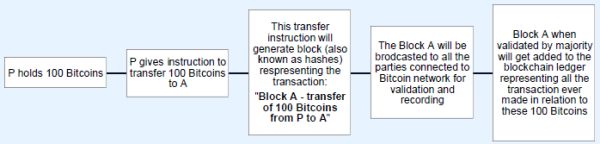

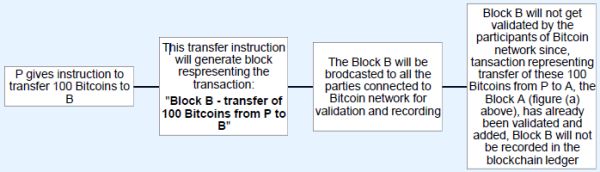

Bitcoins are based on the first-to-file system, meaning that the transaction that gets recorded in the ledger first by way of public agreement is final. For example, if a person P holds certain number of Bitcoins and issues an instruction to transfer the same to A, this transfer instruction will generate a block, also known as hash in computer language, which is broadcasted to all the participants in Bitcoin network for validation and recording. Once this block gets validated by majority of the participants in the Bitcoin network, it gets added to the blockchain ledger,12 as illustrated in figure (a) below. Now, if the same person i.e. P seeks to transfer the same number of Bitcoins to another person say, B, this transaction will not get approved and recorded, as illustrated in figure (b) below, since, the blockchain ledger for all the participants of the Bitcoin network has already been updated to record the first transfer in favour of A, as illustrated in figure (a) below.

Diagrammatic representation of first to file system used by blockchain technology

Figure (a):

Now P tries to send the same 100 Bitcoins to B:

Figure (b):

Crypto-currencies such as Bitcoins do not have any physical existence. They are purchased and held in virtual wallets that are provided by crypto-currency exchanges exclusively for this purpose.13

Crypto-currency - the existing Indian legal framework

A large number of people have made investments in various crypto-currencies, including in Bitcoins. However, the domain of crypto-currency is completely unregulated in India. The Indian monetary policy regulator, the Reserve Bank of India (RBI), has time and again issued warnings that anyone dealing in crypto-currencies will be doing so at their own risk because the creation, trading or usage of crypto-currencies, including Bitcoins, as a medium of payment is not authorised by the central bank or any other monetary authority. The RBI has cautioned that making an investment in crypto-currencies poses potential financial, operational, legal, customer protection and security related risks as crypto-currencies are akin to ponzi schemes.14 Accordingly, the RBI has prohibited all the entities regulated by it, including banks and financial institutions, from dealing in crypto-currencies or provide services for facilitating any person or entity in dealing with or settling crypto-currencies.15 Other departments of the Government such as the Income Tax department,16 Registrar of Companies17 and some commercial banks18 have also cracked down on crypto-currencies, as discussed in detail hereafter.

At the outset, it is pertinent to note that at a fundamental level, crypto-currency is nothing more than a set of computer language code, that is, it does not have any physical or tangible form, nor can it be converted into such form. However, crypto-currencies do resonate with certain characteristics found in some of the legally recognised concepts of currency, property, security and commodity. These concepts are necessary to understand and evaluate the kind of regulation the Government may or should be looking at. We analyse below the nature of crypto-currencies in the context of these recognised concepts.

Crypto-currency as currency or valid legal tender

The Constitution of India mandates that the issue and regulation of currency is the exclusive domain of the Union government,19 that is authorization of the Union government is a condition precedent for according the status of 'currency' or valid 'legal tender'. Consequently, to constitute or be designated as a valid legal tender or currency under Indian law, the issue of the crypto-currency should be in accordance with a valid legislation or ordinance enacted by the parliament, such as the Coinage Act, 1906 or the Reserve Bank of India Act, 1934, or, the Union government should, by an official order, recognise it as a currency or as valid legal tender.

Presently, crypto-currencies are issued outside the legal framework of a State and are neither assured nor backed by any governmental authority. For instance, Bitcoins are generated as a result of solving encrypted mathematical problems presented by the Bitcoin software. For solving these encrypted mathematical problems no human input is required, instead, a predetermined fixed amount of computing power and time is required. Therefore, Bitcoins do not have any intrinsic value nor do they have any guaranteed value since they are not backed by any governmental authority. As a result, their perceived value is superficial and susceptible to volatility. Therefore, as on date, crypto-currencies can neither be treated as currency nor as valid legal tender.

Since 24 December 2013,20 the RBI has issued public notices cautioning people about the risks involved in indulging in transactions related to the crypto-currencies, including Bitcoins. In a recent press release dated 5 December 2017,21 the RBI has reiterated that crypto-currencies, including Bitcoins, are neither regulated nor backed by any governmental authority in India and that they are not valid legal tender. By its circular dated 6 April 2018, the RBI has prohibited all entities regulated by it from dealing, providing services such as maintaining of accounts, trading, settling, clearing, giving loan against crypto-currencies for facilitating dealing with the crypto-currencies.22

In November 2017, for the first time, a public interest litigation, by way of a writ petition under Article 32 of the Constitution of India, was filed before the Hon'ble Supreme Court seeking a ban on sale and purchase of crypto-currencies in India including Bitcoin. The Supreme Court directed the RBI to examine the issues raised in the petition and communicate its response. However, the RBI, instead of clarifying its stance on the issue informed that an Inter-Disciplinary Committee had been appointed by the Ministry of Finance to look into the matter.23 Thereafter, another writ petition was filed before the Supreme Court seeking a declaration that crypto-currencies and all the platforms dealing with it, are illegal. Around the same time, another writ petition was filed before the Supreme Court requesting that the crypto-currencies should either be regulated by a legal framework or be completely banned.24 As on date all these writ petitions are pending final adjudication by the apex court.

Earlier this year, the Hon'ble Finance Minister of India, in his address to the Lok Sabha during budget session for financial year 2018-19 also reiterated that the crypto-currencies including Bitcoins are not legal tender in India.25 However, it may be noted that none of the government instrumentalities in India has declared that the crypto-currencies are per se illegal.

Crypto-currency as 'property' or 'goods'

At the fundamental level, as explained above, crypto-currency is nothing more than a set of computer language code, having no physical or tangible form. Therefore, the question that remains is whether, for the purpose of its regulation, crypto-currency can be treated as moveable property?

The main legislation in relation to property in India is the Transfer of Property Act, 1882 ("TP Act"). The TP Act does not provide for a definition of movable property. However, section 3(36) of the General Clauses Act, 1897 states:

"movable property" shall mean property of every description, except immovable property.

This definition of the term 'movable property' is wide enough to include within its ambit intangible properties as well. Further, the definition of the term 'goods' provided under section 2(7) of the Sale of Goods Act, 1930 states:

"goods means every kind of movable property other than actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale"

Therefore, crypto-currency may be considered as goods, being a movable property, for the purpose of its legal treatment. In this connection it is pertinent to note that the Indian judiciary has not deliberated much on the concept of either 'digital asset' or 'intangible property rights' in relation to the virtual sphere. However, the Hon'ble Supreme Court of India in the case of Tata Consultancy Services v. State of Andhra Pradesh26 has observed that goods may be a tangible property or an intangible one, as follows:

"Indian law does not make any distinction between tangible property and intangible property. A 'goods' may be a tangible property or an intangible one. It would become goods provided it has the attributes thereof having regard to (a) its utility; (b) capable of being bought and sold; and (c) capable of transmitted, transferred, delivered, stored and possessed. If a software whether customized or non-customized satisfies these attributes, the same would be goods.27

Given the existing legal position of property law in India, which provides that 'goods' may be intangible as well, we are inclined to believe that the crypto-currencies are intangible property rights under the Indian law.

On the other hand, American legal jurisprudence is rather well developed in its treatment of crypto-currencies. It recognises that there exists a property right if (a) there is an interest capable of precise definition; (b) it is capable of exclusive possession or control; and (c) the putative owner has established a legitimate claim to exclusivity.28 Crypto-currencies seemingly fulfil all the three criteria for recognition of the property right in it. They have 'interest' that is capable of precise definition, as the total amount of Bitcoins held by any person in his or her crypto-currencies wallet is capable of being calculated and its value can be ascertained in terms of any fiat currency. Secondly, there is 'exclusivity of possession' as it is only the person with the correct credentials to the respective crypto-currencies wallet who can deal with the Bitcoins lying therein. Lastly, crypto-currencies also have an element of a legitimate claim to exclusivity, as a proposed Bitcoin transaction is broadcast to the entire Bitcoin network to determine its validity and the underlying ownership interest, so as to ensure that there is no fraudulent transfer of interest. Once the transaction is validated, the transferred ownership interest is irrevocably recorded in the form of the new hash in the blockchain which is available for anyone to see.29 For these reasons it is safe to say that under American law an intangible property right does exist in crypto-currencies like Bitcoins.

Crypto-currency as 'commodity'

In the event crypto-currencies are held to have intangible property rights, it becomes significant to analyse whether crypto-currencies can also be classified as 'commodity'. Under Indian law, the term 'commodity' has neither been defined anywhere nor is there any established legal jurisprudence available on the subject. The term 'commodity' is understood to include every movable thing that is bought and sold (except animals), an article of trade, movable article of value or something that affords convenience or advantage especially in commerce.30

In the case of Tata Consultancy Services v. State of Andhra Pradesh,31 Hon'ble Justice Sinha observed that a commodity is generally understood to mean goods of any kind, something of use or an article of commerce.

Having established in the preceding sections that it is fitting to classify crypto-currencies as an intangible movable asset, it may be possible to identify them also as 'commodity' under the Indian legal framework.

Crypto-currencies as 'asset'

It is interesting to note that despite being unregulated, the tax authorities in India32 and other countries such as the United States of America have recently sought to tax the gains made out of trading in crypto-currencies, thereby providing an informal affirmation that the crypto-currencies may be treated as an asset. Although we do not have any Indian judicial pronouncement in this regard, the United States of America's revenue courts have delved into this matter in detail. The United States Internal Revenue Services, in as early as 2014, issued a formal ruling expressly stating that for the purposes of federal taxation the virtual currency will be treated as property and that general taxation principles applicable to property transactions will apply to virtual currency as well.33 Currently also, there is a matter is pending before the federal judges in the court of Brooklyn, New York, which is concerned with the question whether the crypto-currencies can be treated as securities.34

Therefore, authorities across the globe are tending towards treating the crypto-currencies as an intangible asset that may also be treated as a commodity.

Crypto-currency as security

Section 2(h) of the Securities Contracts (Regulation) Act, 1956 ("SCRA"), defines the term 'securities' as follows:

"securities to include:

- shares, scrips, stocks, bonds,

debentures, debenture stock or other marketable securities of a

like nature in or of any incorporated company or other body

corporate;

- derivative;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- security receipt as defined in clause (zg) of section 2 of the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- units or any other such instrument issued to the investors under any mutual fund scheme;

- Government securities

- such other instruments as may be declared by the Central Government to be securities;

- rights or interest in securities."

From the definition of the term 'securities', it becomes clear that all of the instruments that have been enumerated in this definition have an underlying capital asset. However, as noted in the preceding sections, there is no underlying asset in relation to Bitcoin or any other crypto-currencies for that matter. Secondly, the definition provides that the securities are issued i.e. there is an 'issuer' and an 'allottee'. However, as noted above, Bitcoins are not "issued" by anybody but are created from the activity of mining, which is, solving the cryptographic mathematical problem presented by the Bitcoin software through the application of the computing power and time.

Though the crypto-currencies are traded exclusively over the crypto-currency exchanges in a manner akin to the trade of shares, stocks and other securities over a stock exchange, the crypto-currencies may not classify as a security under the Indian legal framework because, it may not satisfy the abovementioned criteria under the SCRA, even though the definition is not an exhaustive one.

Legal Issues in relation to crypto-currency exchanges

As noted above, transactions in relation to crypto-currencies are restricted completely to the virtual space as they take place only through the online exchange platforms specifically dealing only with crypto-currency. These transactions may also be spaced across various countries, thereby raising a jurisdictional issue.

Crypto-currency exchanges do not function in a manner as understood conventionally in case of an exchange in the securities market or commodity market and crypto-currencies do not derive value from any underlying asset or security. Crypto-currency exchanges are therefore more akin to a platform for buying and selling crypto-currencies, like any other e-commerce platform, where one can buy or sell designated goods. Therefore, crypto-currency exchanges should likely be viewed as a market-place rather than an exchange where shares, stocks, debentures, bonds and the like are traded.

Another issue faced by crypto-currency exchanges is the differential treatment accorded to the crypto-currencies by different departments of the Government. This is evident from the fact that in most of the countries across the world, including India, the revenue departments are keen on taxing transactions concerning crypto-currencies as capital gains and as profit or gains from property transaction, even though the legislatures of these countries are yet to finalise the treatment to be accorded to them.35

A significant recent development that may have a resonating impact on the future of crypto-currencies is the decision of Google to ban all advertisements in relation to crypto-currencies and initial coin offerings, across all its platforms, starting June 2018.36,37 This trend in the virtual space was started by Facebook earlier this year in January, on the pretext that a majority of these advertisements were misleading or deceptive promotions or scams.38 Following suit, another player in the internet space, Twitter, is also contemplating implementation of such a ban on its platform.39 This move by the internet giants will gravely affect the business prospects of crypto-currency exchanges as they will be unable to advertise the services provided by them to a substantial portion of their target customers.

Recently, the New York Attorney General, Eric Schneiderman, has launched an official inquiry into the operations of major crypto-currency exchanges operating in United States of America in order to identify issues impacting crypto-currency investors and consumers and to provide for more transparency and accountability of these crypto-currency exchanges.40

Position in India

The existing crypto-currency exchanges in India, such as Zebpay, 41 are incorporated and registered with the Registrar of Companies as a private company providing software and IT services. 42 In view of all the issues looming around the legality of crypto-currencies per se, crypto-currency exchanges in India too are likely to face regulatory problems. The Registrar of Companies is already rejecting applications for fresh incorporation of a company seeking to function as crypto-currency exchange in India.43 In some of these instances, the Registrar of Companies has, before rejecting the application for incorporation, issued notice to the entities that have filed the application, asking them to provide an undertaking that they will not deal with cryptocurrencies such as Bitcoins and that they will procure a prior no objection from the RBI.44

Recently, a few commercial banks in India suspended and froze the accounts of some of the crypto-currency exchanges on suspicion of dubious transactions.45 Some of the investors using these exchanges' platform were not allowed by commercial banks, in which their bank accounts were maintained, to make payment of money for purchases made over these exchanges or to deposit money earned on them.46

Further, the RBI by its circular dated 6 April 2018, has imposed a blanket ban on the entities regulated by it from dealing or providing services of any nature, including bank account facility, to any person or entity dealing or seeking to deal with crypto-currencies.47 It has instructed all the entities regulated by it, providing such services, to exit the relationship with 3 (three) months from 6 April 2018.48 This, effectively, takes away the financial infrastructure required for the functioning of a crypto-currency exchange in India.

Presently, one of the interested stakeholders has filed a writ petition before the Delhi High Court, requesting the Hon'ble Court to quash the RBI circular dated 6 April 201849 on the grounds of it being arbitrary and unconstitutional. 50

Another regulatory concern related to the functioning of crypto-currency exchanges is the alleged facilitation of money laundering and terror funding.51 Many crypto-currency exchanges provide the facility to exchange crypto-currencies for its value in fiat currency. This potentially impacts money laundering and terror funding, because a single transaction or an array of transactions in relation to crypto-currencies over the crypto-currency exchanges may be utilised to transfer a large amount of funds, from one geographical location to another, in a fraction of second. These transactions may not be caught by any of the governmental authorities largely due to the fact that crypto-currency exchanges are neither required to be registered with any of them nor are they required to report52 cash transactions above a particular monetary threshold to any governmental authorities. Consequently, crypto-currencies could become an instrument for money laundering and terror funding. 53

Finally, in the event that crypto-currencies are treated as 'security' by the Indian legislators, the securities market regulator in India, the Securities and Exchange Board of India, may seek to regulate the crypto-currency exchanges.

Way forward

Both in India and on a global scale there is substantial monetary investment in crypto-currencies including Bitcoins. The future of these investments largely hinge on the fate of crypto-currency exchanges. Therefore, it is necessary to address the legal issues faced by these crypto-currency exchanges as highlighted above keeping in mind the interests of investors as well. As discussed above, the best suited genre for the crypto-currencies would be an intangible commodity, since crypto-currencies being intangible assets are being traded in value against the fiat currency over these crypto-currency exchanges. However we will have to await the outcome of the various petitions pending adjudication by the Supreme Court to see how the issues with respect to the treatment of crypto-currencies and crypto-currency exchanges are ultimately dealt with.

In the author's view, however, treating crypto-currencies as a commodity may simplify the issue of the Court's jurisdiction which may present itself in case of a dispute related to a transaction in crypto-currencies over the crypto-currencies exchanges. In such a case, the well-established principle that the courts at the place where seller or buyer is based will have jurisdiction in the event the parties have not agreed to a specified jurisdiction, would then apply.

In the authors' view, the suo moto freezing of accounts of crypto-currency exchanges by commercial banks in India disentitling investors and crypto-currency exchanges of regular banking channels to facilitate crypto-currency transactions, prima facie amounts to wrongful disentitlement of assets. In India, the right to property is protected as a legal right under its Constitution, which can only be taken away in a manner provided by law. Therefore, such suo moto action on the part of commercial banks without giving an opportunity to the affected parties to be heard and without any pre-emption from a statutory or governmental authority, purely on the basis of speculation, is against the spirit of the law.

There are various crypto-currency exchanges operational in India such as Zebpay, Unocoin, etc. The question of their legality is largely co-dependent on the legal treatment that will be accorded to crypto-currencies. However, in the authors' view, under the existing circumstances, crypto-currency exchanges are neither in violation of any existing law nor are they engaged in any activity prohibited by law. Although the crypto-currency exchanges may appear to be functioning prima facie in a legally void space, they are seemingly in compliance with the existing applicable laws. One of the basic principles of our legal system is that one cannot be held accountable for violation of a law that does not exist. Therefore, crypto-currency exchanges cannot be said to be functioning illegally.

The issue of money laundering and terror funding through crypto-currencies is being projected out of proportion. Even the existing financial systems are being exploited for terror funding and money laundering despite crack-downs and multiple checks and balances being put in place by Governments across the world. In fact, crypto-currencies afford a more secure environment than those used by existing financial systems. As noted above, details of all the transactions made in relation to crypto-currencies, from the beginning, is available in a form of an electronic public ledger which is not only easily accessible to everyone, its alteration is next to impossible. Given that money laundering and terror funding operates on the element of anonymity, if the Government puts in place proper and adequate checks and regulations for monitoring the transactions in crypto-currencies, the public nature of crypto-currencies' transaction records and the ease of accessibility to them makes crypto-currencies an unlikely cause for facilitating money laundering and terror funding.

Attributing illegality to crypto-currency exchanges solely on the basis of the fact that they are dealing with a technology that is not regulated by any law at the moment is a very stringent stand driven largely by fear than reason. In the authors' view the decision of the RBI to ban all the entities regulated by it, from dealing with or providing services of any nature to any entity dealing in crypto-currencies, including crypto-currency exchange, is also one such decision. As technology is developing at a faster pace in comparison with the law governing such technology, there is a need to develop our legal system in order to regulate such technological advancements, rather than declaring them illegal ipso facto. Therefore, operational crypto-currency exchanges are not illegal nor is it illegal for an entity to enter the market as a crypto-currency exchange.

In any case, much will depend upon the final stance that the Indian legislature takes, if at all, in relation to regulating crypto-currencies and crypto-currency exchanges.

Footnotes

1. Abba P Lerner, "Money as a Creature of State", The American Economic Review, 37(2), 312(1947)

2. Tracey A Anderson, "Bitcon-is it just a fad? History, current status and future of cyber-currency revolution"

3. Available at: http://www.economist.com/node/11751346 (last accessed on 23 April 2018)

4. Satoshi Nakamoto, "Bitcoin: A Peer-to-Peer Electronic Cash System"

5. Available at: https://blockchain.info/wallet/wallet-faq (last accessed on 23 April 2018)

6. One such crypto-currency exchange is coinswitch details available at: https://coinswitch.co/ (last accessed on 23 April 2018)

7. Supra note 1

8. Available at: https://bitcoin.org/bitcoin.pdf (last accessed on 23 April 2018)

9. Supra note 3

10. Vitalik Buterin, "A next generation smart contract and decentralised application platform"

11. Ibid

12. Supra note 4

13. Available at: https://blockchain.info/wallet/wallet-faq (last accessed on 23 April 2018)

14. Reserve Bank of India press release no.: 2013-2014/1261

15. Reserve Bank of India Circular no.: DBR.No.BP.BC.104/08.13.102/2017-18, dated 6 April 2018

16. Available at: https://in.reuters.com/article/us-markets-bitcoin-india-taxes/india-sends-tax-notices-to-cryptocurrency-investors-as-trading-hits-3-5-billion-idINKBN1F8190 (last accessed on 23 April 2018)

17. Available at: http://knowstartup.com/2018/01/cryptocurrency-forbidden-roc/ (last accessed on 23 April 2018)

18. Available at: https://economictimes.indiatimes.com/industry/banking/finance/banking/top-banks-suspend-accounts-of-major-bitcoin-exchanges-in-india/articleshow/62576882.cms (last accessed on 23 April 2018)

19. Entry 36, List I, Seventh Schedule read with Article 246 of the Constitution of India

20. Reserve Bank of India press release no.: 2013-2014/1261

21. Reserve Bank of India press release no.: 2017-2018/1530

22. Supra note 16

23. Available at: https://www.ccn.com/india-supreme-court-cryptocurrency/ (last accessed on 23 April 2018)

24. Available at: https://www.deccanchronicle.com/nation/current-affairs/191117/supreme-court-issues-notice-to-rbi-on-bitcoin-regulation.html (last accessed on 23 April 2018)

25. Available at: https://economictimes.indiatimes.com/news/economy/policy/arun-jaitley-settles-the-bitcoin-issue-for-once-and-all/articleshow/62737852.cms (last accessed on 23 April 2018)

26. Tata Consultancy Services vs. State of Andhra Pradesh, [2004] (271 ITR 401)

27. Ibid

28. Rasmussen Associates Inc v. Kalitta Flying Service Inc, 958 F.2d

29. Although the bitcoin recipient (i.e., the new owner) does not take the affirmative step of registering its ownership the critical fact is that the bitcoin recipient's address is recorded on the blockchain just as for example the land owner's name is recorded on the revenue department's registry. Thus, for relevant purposes, ownership is publicly recorded in a materially similar manner in both cases.

30. Dr. H. K. Saharay & P. M. Bakshi, "Judicial Dictionary of Words and Phrases", Thomson Reuters, 2nd Edition Volume I (2016)

31. Supra note 26

32. Available at: https://in.reuters.com/article/us-markets-bitcoin-india-taxes/india-sends-tax-notices-to-cryptocurrency-investors-as-trading-hits-3-5-billion-idINKBN1F8190 (last accessed on 23 April 2018)

33. I.R.S. Notice 2014-21, 2014-16 I.R.B. 938 (14 April 2014) § 4, A-1

34. Available at: http://time.com/money/5123510/are-cryptocurrencies-and-icos-scams-the-government-will-soon-decide/ (last accessed on 23 April 2018)

35. Dinesh Sharma Committee constituted by the Government of India to look into issues relating to cryptocurrencies is yet to submit its final recommendations to the government

36. Available at: https://support.google.com/adwordspolicy/answer/7648803?hl=en&ref_topic=29265 (last accessed on 23 April 2018)

37. Available at: https://www.reuters.com/article/us-crypto-currencies-google/google-bans-cryptocurrency-advertising-bitcoin-price-slumps-idUSKCN1GQ0GD (last accessed on 23 April 2018)

38. Available at: https://www.theguardian.com/technology/2018/jan/31/facebook-bans-ads-cryptocurrencies-scams (last accessed on 23 April 2018)

39. Available at: https://economictimes.indiatimes.com/magazines/panache/after-google-twitter-likely-to-ban-cryptocurrency-advertisements/articleshow/63361872.cms (last accessed on 23 April 2018)

40. Available at: https://www.bloomberg.com/news/articles/2018-04-17/cryptocurrency-exchanges-get-fact-finding-letter-from-new-york (last accessed on 23 April 2018)

41. Available at: https://www.zebpay.com/ (last accessed on 23 April 2018)

42. Available at: http://knowstartup.com/2018/01/cryptocurrency-forbidden-roc/ (last accessed on 23 April 2018)

43. Available at: http://www.business-standard.com/article/economy-policy/bitcoin-mania-amid-haze-around-crypto-know-all-about-regulations-in-india-118012400321_1.html (last accessed on 23 April 2018)

44. Available at: http://smartinvestor.business-standard.com/market/Marketnews-508769-Marketnewsdet-RoC_halts_registering_new_cryptocurrency_exchanges_under_Companies_Act.htm#.WrM4P7tPoUA (last accessed on 23 April 2018)

45. Available at: https://economictimes.indiatimes.com/industry/banking/finance/banking/top-banks-suspend-accounts-of-major-bitcoin-exchanges-in-india/articleshow/62576882.cms (last accessed on 23 April 2018)

46. Available at: https://www.thehindubusinessline.com/money-and-banking/investors-in-a-bind-as-banks-pull-the-plug-on-bitcoin-accounts/article22545347.ece (last accessed on 23 April 2018)

47. Supra note 16

48. Ibid

49. Ibid

50. Available at: https://www.coindesk.com/indian-crypto-startup-files-petition-central-bank-ban/ (last accessed on 23 April 2018)

51. Available at: https://www.forbes.com/sites/jasonbloomberg/2017/12/28/using-bitcoin-or-other-cryptocurrency-to-commit-crimes-law-enforcement-is-onto-you/#3e519b283bdc (last accessed on 23 April 2018)

52. According to the Know Your Customer Norms/Anti-Money Laundering Standards/Combating of Financing of Terrorism/Obligations under PMLA, 2002 and Reporting of Cross Border Wire Transfers regulations issued by the Reserve Bank of India all the concerned financial institutions in India are required to closely monitor all the transaction of value more than equal to Rs. 50,000 and are required to report cross border wire transfers of value more than Rs. 5 lakh or its equivalent in foreign currency respectively.

53. CRISIL report, "Bitcoin: Currency of the future or money laundering vehicle?", June 2017

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.