With increased scale of globalisation and growing levels of economic activities, the entrepreneurs, to tap global market potentials, are expanding their business activities in various other countries. This has led to increased cross border transactions which in turn raises many issues on double taxation of income.

Every Company is taxed on its global income in the country of its residence. A Company is also exposed to tax in the country where it has its Source of income. Therefore, a Company is exposed to double taxation for the same income, if source of such income is derived from another country. This is hindrance to smooth flow of cross border transactions. Many countries therefore have signed Double Tax Avoidance Agreements (DTAA) as a solution to address this problem of double taxation.

The basic aim of the DTAAs is to allocate taxation right to country of residence as well as to the country where the source of income arises.

Different methods are used by Countries to eliminate the double taxation. They are:

Exemption method:

- Full exemption method: Under this method country of residence fully exempts the income earned by a tax payer in country of source. For eg: DTAA signed by India with Brazil provides for full exemption with respect to dividend income.

- Exemption with progression: Though exemption is given by the country of residence, the income will have to be considered for the purpose of determining rate of tax which would be required to be applied on other taxable income. For eg: DTAAs entered into by India with Greece, Austria etc.

Credit method:

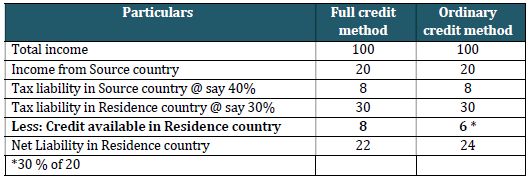

- Full credit method: Under this method the country of residence will provide full credit for the entire amount of tax paid in country of source. For eg: India – Namibia DTAA.

- Ordinary credit method: The country of residence will provide credit for the tax paid in country of source but only to the extent of the incremental tax liability due to inclusion of such income in the total taxable income in the country of residence. Therefore if the tax paid in source country is higher than the tax liability on the same income in residence country, the Company will lose out on such excess amount paid in source country. If the tax paid in source country is lower than the tax liability on the same income in the residence country, the Company will be required to pay the incremental tax in the source country. This method is often preferred by India in most of its DTAAs for eg: USA, UK etc.

Following illustration will be useful in understanding both the credit methods in eliminating double taxation:

Additional concepts related to FTC:

Underlying Tax Credit (UTC):

UTC refers to the credit that may be given in the Resident country for the tax paid on the underlying profits out of which dividend is paid by the Company in the source country.

Generally, taxes would have been paid by the Companies on the profits from which the dividends are declared. However, since the person receiving the dividend (Shareholder) is not the same as the person which paid the taxes on the profits, normally credit for such foreign tax would not be available. UTC seeks to address this double taxation and provides a benefit of tax credit to the recipients of the dividend as well. Thus in this method, the taxes paid on the profits from which the dividend is declared can be taken as credit against the taxes payable on the dividend income.

The benefit of UTC is available subject to certain conditions like threshold of shareholding etc. India has such UTC benefits in DTAAs with Australia, Japan, Mauritius, USA, UK etc.

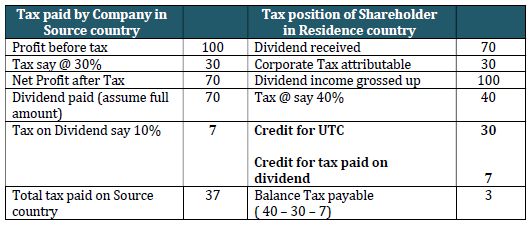

An illustration on how the UTC works:

Thus the shareholder not only gets credit of 7/- which is tax paid on dividend but also gets credit of 30/- which is corporate tax paid by Company in source state from which the dividend is declared.

Tax Sparing:

Tax sparing is also referred to as deemed tax credit. In many countries, incentives are given under the domestic law by levy of concessional rate of tax or exemption from tax to the Companies operating in specific sectors or specific geographical region to promote and advance overall economic interest in that sector or region. In such case, the Companies availing the benefit of such concession do not pay tax or pays tax on concessional basis in the source country. Since FTC provides for credit only in respect of taxes paid in the source country, no credit would be available since no taxes have been actually paid by the tax payer in the source country and thus the benefit of tax incentive in the source country would be lost and purpose of such incentive by the source country gets defeated.

Tax Sparing essentially consists of granting a tax credit in the resident country, for the amount of tax that would have been paid in the source country had there been no exemption or concession under the domestic law of source country. Thus, tax incentives offered by Source country are deemed to have been paid as a foreign tax for the purpose of computing FTC to be granted by resident country.

Absence of tax sparing clause in the DTAA would result in transfer of tax revenue from Source country to Resident country with no ultimate benefit to the tax payer.

India has conditional tax sparing clause in various DTAAs with Australia, Belgium, Cyprus, Canada, Mauritius, Singapore etc.

Unilateral Tax Credit: Section 91 of The domestic Indian Income Tax Act provides for FTC to a resident tax payer in respect of foreign taxes paid on his foreign income earned in a country with which India has not entered into any DTAA. The deduction shall be granted at the Indian Tax rate of the tax rate in foreign country whichever is lower.

Foreign Tax Credit Rules: Recently, CBDT has inserted Rule 128 to provide for the manner and extent to which the FTC would be available and procedure for granting of relief or deduction of income tax paid in foreign country.

The FTC Rules provide that no credit shall be granted in respect of any payment made towards interest, fees or penalty.

It further states that no credit shall be available in respect of any foreign tax paid which is disputed in any manner.

The Rules also provide for the documentation required to be furnished by the tax payer to successfully claim FTC.

Open issues: There are certain issues surrounding FTC which could result in denial or reduction in the amount of FTC:

- Certain taxes not covered in the DTAA

- Mismatch in accounting period between countries

- Change in characterisation of income

- Conflict in determining the source of income

- Treaty abuse

- Method of documentation for claiming credit.

Originally published July 2017

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.