- within Real Estate and Construction topic(s)

- with readers working within the Property industries

- within Real Estate and Construction, Environment, Litigation and Mediation & Arbitration topic(s)

The much-discussed Real Estate (Regulation and Development) Act, 2016 ("the Act") has now been brought in force entirely. In addition to stirring the developer community and causing much delight for the purchasers, the Act also requires urgent consideration with matters connected with enforcement of security.

It is commonplace in debt transactions to 'transfer' by way of a mortgage inter alia, land and/or development rights in favour of a lender as security for the repayment of debt, although strictly speaking, development rights, by their very nature, are personal and incapable of assignment.

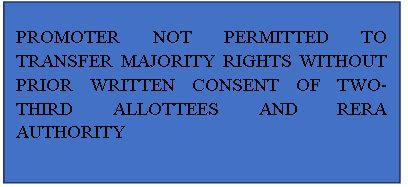

Section 15 (1) of the Act states that 'The promoter shall not transfer or assign his majority rights and liabilities in respect of a real estate project to a third party without obtaining prior written consent from two-third allottees, except the promoter, and without the prior written approval of the Authority'.

In light of the general scheme of the Act to protect consumers, it appears that the intention of the Legislature is to ensure that assignment of the promoter of his rights in the project does not adversely affect the rights of the allottees/purchasers who have purchased apartments on the basis of his reputation and credibility.

However, this restriction imposed by Section 15 has now become a matter of great concern for lenders as it begs the question as to whether enforcement of mortgage/ security would tantamount to 'transfer' of his majority rights and liabilities in respect of the project.

The pre-RERA position

Prior to the Act, it has been a well settled position under law that the lenders were entitled to enforce security over land and recover their outstanding debt, without reference to the purchasers who had also acquired rights in the unit being built on the land.

For self-owned property of the promoter, the lender was also empowered to take over the management of the borrower, or the project and cause the project to be completed. Even secured creditors and notified NBFCs under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 ("SARFAESI") could take recourse under SARFAESI which included the sale of the charged property (whether land or development rights) without the intervention of the court.

Mortgage of development rights on the other hand would typically require the consent of the society members/ landowner, unless specifically permitted in the development agreements in favour of the promoter/ developer. This is in view of the fact that development rights are in the nature of license to enter upon and construct which are personal in nature and usually extended to the developer on the basis of the repute of the specific developer and cannot be said to have created a right in rem at large.

Effect of Section 15

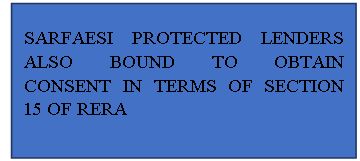

With the Act being brought into force, consent of two-thirds of the allottees of the project as well as the Real Estate Regulatory Authority ("Authority") will have to be taken before 'transferring' the promoter's majority rights and liabilities.

This is equally applicable to SARFAESI-protected secured creditors and notified NBFCs who will henceforth require prior written consent of two-third of the allottees in addition to that of the Authority for enforcement of the security interest (whether under SARFAESI or otherwise).

Upfront consent

One may consider obtaining one-time consent from the allottees (while executing the agreement for sale) for the mortgage.

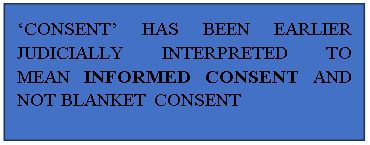

However, the concept of blanket consent has not been accepted in earlier judicial pronouncements under Section 7(1) of the Maharashtra Ownership Flats (Regulation of the promotion of construction, sale, management and transfer) Act, 1963 ("MOFA").

The Bombay High Court has consistently taken the view that blanket consent or authority obtained by the promoter, at the time of entering into agreement of sale or at the time of handing over possession of the flat, is not consent within the meaning of Section 7(1) of MOFA and that such consent has to be an informed consent which is to be obtained upon a full disclosure by the promoter.

Although such judgments were under a different section of a different statute, in our view the same principle would apply here as the intent of requiring prior consent in both Section 7 of MOFA and Section 15 of the Act is to protect the purchaser's right to a promised product and if any change has to be made to what has been earlier disclosed to him, the same can be done only after the purchaser has understood the consequences of such change and has expressly approved the same. Obtaining upfront consent from the purchasers at the time of signing the agreement to sell would defeat the entire purpose of the provision and be open to judicial scrutiny as the same would have to be necessarily vague at that premature stage.

Thus, enforcing a mortgage of development rights and land in general, has now become a long and uncertain process.

Revocation of registration of the project

Another situation which requires careful consideration is the interest of the lenders in case of revocation of the registration of the project by the Authority. The Authority has the power to revoke the registration of the project on grounds including default by the promoter in doing anything required under the Act, rules or regulations made thereunder, violation of the terms and conditions of the approval granted to the promoter and carrying out of any kind of unfair practice (as defined in the Act).

Upon such revocation, the Authority can inter alia (i) direct the bank holding 70% of the project receivables to freeze the account and take such further actions, and (ii) appoint another promoter to finish the development of the project. In the event the Authority exercises these rights, it would not be feasible for the lender to enforce its security interest and/or take over the development of the project despite the default by the borrower under the lending documents.

Some relief under the Maharashtra Rules

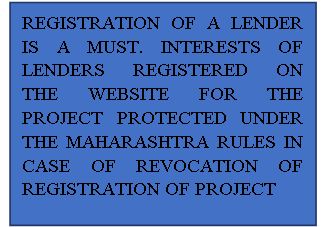

Rule 8 of the Maharashtra Rules gives some comfort to lenders registered on the website of the Authority.

In terms of Rule 8, the Authority is required to take such measures to protect the interest of other parties who, through mortgage or other investments, are interested in the project and which are disclosed by the promoter of the website of the Authority, while facilitating the remaining development of the project.

Thus, as long as a lender's charge is reflected on the website, the Authority is bound to safeguard his interests. However, while there are express provisions requiring a promoter to disclose encumbrances existing prior to registration, as of now there does not seem to be any provision allowing promoters to upload details of charges created during the life of the project. Further, lenders will have to ensure that the promoter registers such lender on the website of the Authority as the same cannot be done by the lender itself.

While the Authority is duty bound to protect the interest of lenders reflecting on the website, a window of opportunity is also given by the second proviso to Rule 8 to certain types of lenders whose charges are not reflected on the website. The Authority is required to give adequate opportunity of being heard to certain third parties which through a defined instrument of debt or equity have created third party interest in the project.

However, apart from the comfort that his rights will be safeguarded by the Authority while carrying out or causing to carry out the balance development, the lender does not have the actual right to appoint a new promoter to complete remaining development of the project. In the event of revocation, section 8 of the Act in fact gives the association of allottees the right of first refusal to complete the remaining work. Perhaps the lenders would have to be ever more vigilant in monitoring the progress of the project and taking over the management of the project before occurrence of a default under the Act by the borrower to appropriately safeguard their rights.

The Way Ahead?

A mortgage of built up areas (present and future) continues to remain perhaps the only valid and enforceable form of securing debt. Needless to add however that a lender may not be able to realise full value of these built up areas until the same are actually constructed, its rights to the same would be indefeasible even if a new developer is appointed by the Authority under Section 8.

Indirect change of control permitted?

Based on the forms required to be filed by the promoter with the Authority as per the Maharashtra Rules, a corporate promoter is not required to disclose the details of its shareholders. No provision of the Act and/or the Maharashtra Rules prohibits change of shareholding and/or the board of directors of the promoter. It thus appears that in cases of development by single project SPVs, a lender may find it useful to simply have all the shares of the promoter SPV pledged in favour of the lender.

On default, the outstanding debt can be recovered by the lender by selling the pledged shares of the promoter SPV to another developer who can continue development, of course in accordance with the sanctioned plans already disclosed to the allottees. However, typically the incoming developer would want to change the branding of the project which would highlight the fact that control of the project is effectively in new hands. Whether such enforcement which results in change of control would militate against the true intent of Section 15 is a question which is likely to come up before the courts.

Whether the Act and its provisions will induce more judiciousness and responsibility in the lenders and the developers so as to adequately protect the interests of the purchasers or whether it will create more chaos and litigations, remains to be seen!

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.